Managed Services Market Report by Type (Managed Infrastructure, Managed Data Center, Managed Security, Managed Communications, Managed Network, Managed Mobility), Deployment Mode (On-premises, Cloud-based), Enterprise Size (Large Enterprises, Small and Medium-sized Enterprises), End Use (IT and Telecommunication, BFSI, Healthcare, Entertainment and Media, Retail, Manufacturing, Government, and Others), and Region 2026-2034

Managed Services Market Size & Trends (2026-2034)

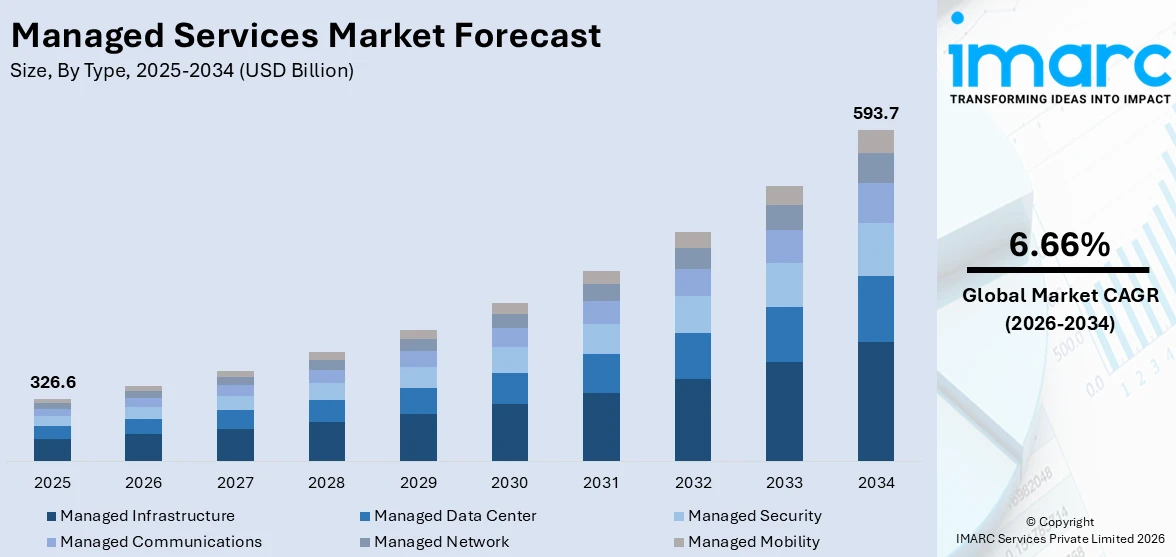

The global managed services market size reached USD 326.6 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 593.7 Billion by 2034, exhibiting a growth rate (CAGR) of 6.66% during 2026-2034. The increasing demand for IT outsourcing solutions, the growing complexities in IT infrastructure management, and the rising need for cost-effective and scalable business solutions are some of the major factors propelling the growth of the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 326.6 Billion |

|

Market Forecast in 2034

|

USD 593.7 Billion |

| Market Growth Rate 2026-2034 | 6.66% |

Managed Services Market Analysis:

- Major Market Drivers: The increasing need for IT cost reduction and efficiency enhancement among businesses represents the major driver of the market. Organizations seek to outsource IT operations to focus on core business activities, leveraging managed services to access expertise, advanced technologies, and continuous support.

- Key Market Trends: The rise of artificial intelligence (AI) and automation in service delivery, enhances efficiency and reduces human error which represents key trends in the market. There is also a growing emphasis on cybersecurity-managed services and the increasing frequency and sophistication of cyber threats.

- Geographical Trends: North America dominates the global managed services market growth, driven by a strong presence of technology firms, robust IT infrastructure, and high adoption rates among enterprises. Asia-Pacific is witnessing rapid growth, fueled by increasing digitization efforts, expanding IT spending, and rising demand for managed services among small and medium-sized businesses.

- Competitive Landscape: Some of the major market players in the managed services industry include Accenture plc, AT&T, Capgemini, Dell Inc., Fujitsu Limited, Hewlett Packard Enterprise Development LP, Infosys Limited, International Business Machines Corporation, Nokia Corporation, Open Text Corporation, Rackspace Technology, Telefonaktiebolaget LM Ericsson, Verizon among many others.

- Challenges and Opportunities: The market faces challenges in the market including cybersecurity threats, data privacy concerns, and the need for continuous innovation to stay ahead in a competitive market. However, the market also faces several opportunities for managed service providers to capitalize on emerging technologies, expanding market segments, and the growing demand for specialized expertise.

To get more information on this market Request Sample

Managed Services Market Trends:

Increasing Complexity of IT Infrastructure

The escalating complexity of IT systems, with hybrid cloud environments, extensive data networks, and advanced cybersecurity demands, is a significant driver for the managed services market. Businesses are finding it increasingly challenging to manage and maintain their IT infrastructure due to rapid technological advancements, diverse software applications, and the integration of various platforms. Managed service providers (MSPs) offer specialized expertise, resources, and advanced tools to efficiently manage this complexity, ensuring optimal system performance, reliability, and security. For instance, in April 2023, Cognizant launched a multi-hybrid cloud and edge management platform designed to transition to modern cloud-native architectures and streamline their cloud management operations. Cognizant Skygreed applies an industry focus on approach through a curated library of solution accelerators, enabling enterprises to realize greater business value quickly and efficiently while driving simplification, sustainability, and cost-effectiveness. This is expected to boost the managed services market forecast over the coming years.

Increasing Cybersecurity Challenges

In an era of ever-evolving cyber threats, ensuring robust cybersecurity has become paramount for businesses of all sizes. Managed services providers offer specialized security solutions, including 24/7 monitoring, threat detection, incident response, and compliance management. They help businesses protect their critical data and IT assets from a wide array of cyber threats while ensuring compliance with relevant regulations and standards. This is particularly crucial for industries subject to stringent data protection laws, such as finance, healthcare, and retail. By leveraging the expertise of MSPs, companies can maintain high-security standards, mitigate risks, and avoid potential legal and financial penalties associated with data breaches or non-compliance. According to industry reports, there were 2365 cyber-attacks in 2023 with 343,338,964 victims. 2023 saw a 72% increase in data breaches since 2021, which held the previous record. A data breach costs $4.45 million on average. e-mail is the most common vector for malware, with around 35% of malware delivered via e-mail in 2023. 94% of organizations have reported e-mail security incidents. Business e-mail compromises accounted for $2.7 billion in losses in 2022. Information security jobs are projected to grow by 32% between 2022 and 2032. This is influencing the managed services market statistics significantly.

Widespread Adoption of Cloud Technologies

The rising shift toward cloud computing is acting as a major growth-inducing factor in the market. As businesses migrate to cloud-based solutions to benefit from cost efficiency, enhanced collaboration, and improved accessibility, they often require expert assistance to manage these environments effectively. Managed services providers offer comprehensive cloud management solutions, ensuring optimal performance, security, and cost-effectiveness. For instance, in May 2024, Rackspace Technology, the leading end-to-end, hybrid multi-cloud, and AI solutions company announced working with young Hollywood on a multi-stage Google Cloud solution to transform video content management. The collaboration successfully created the necessary infrastructure, third-party metadata, video assets, and processed videos using the Google Cloud Video Intelligence Application Programming Interface (API). The new cloud infrastructure provides the pioneering entertainment network with 10 times faster video processing and improved data accessibility while enabling new monetization and distribution opportunities.

Managed Services Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on type, deployment mode, enterprise size, and end use.

Breakup by Type:

- Managed Infrastructure

- Managed Data Center

- Managed Security

- Managed Communications

- Managed Network

- Managed Mobility

Managed infrastructure accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the type. This includes managed infrastructure, managed data center, managed security, managed communications, managed network, and managed mobility. According to the report, managed infrastructure represented the largest segment.

Managed infrastructure services encompass the outsourcing of IT infrastructure components such as servers, storage, and networking equipment to third-party providers. This segment is the largest within the managed services market, driven by the increasing complexity of IT environments and the need for businesses to optimize infrastructure management while reducing costs. Managed infrastructure services offer benefits such as improved reliability, scalability, and performance, enabling organizations to focus on core business activities while leveraging the expertise of service providers to maintain and support their IT infrastructure.

Breakup by Deployment Mode:

- On-premises

- Cloud-based

On-premises holds the largest share of the industry

A detailed breakup and analysis of the market based on the deployment mode have also been provided in the report. This includes on-premises and cloud-based. According to the report, on-premises represents the largest segment.

The on-premises segment in the managed services market refers to services and solutions that are deployed and maintained within the physical infrastructure of the client's premises. This segment typically includes services such as hardware procurement, installation, configuration, and ongoing maintenance provided by managed service providers. Despite the growing popularity of cloud-based solutions, the on-premises segment remains significant, particularly for organizations with stringent security and compliance requirements, as well as those operating in highly regulated industries such as healthcare, finance, and government. These organizations prefer to retain full control over their IT infrastructure and data, opting for on-premises solutions to ensure data sovereignty and mitigate concerns related to data privacy and security breaches.

Breakup by Enterprise Size:

- Large Enterprises

- Small and Medium-sized Enterprises

Large enterprises represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the enterprise size. This includes large enterprises and small and medium-sized enterprises. According to the report, large enterprises represented the largest segment.

Large enterprises represent the largest segment in the managed services market, characterized by extensive IT infrastructure, complex operations, and significant budget allocations for IT services. These organizations often require a wide range of managed services to support their diverse business needs, including network management, cybersecurity, data analytics, and cloud computing. Key factors driving the adoption of managed services among large enterprises include the need for scalability, agility, and cost optimization, as well as the desire to offload routine IT tasks and focus on core business objectives.

Breakup by End Use:

Access the comprehensive market breakdown Request Sample

- IT and Telecommunication

- BFSI

- Healthcare

- Entertainment and Media

- Retail

- Manufacturing

- Government

- Others

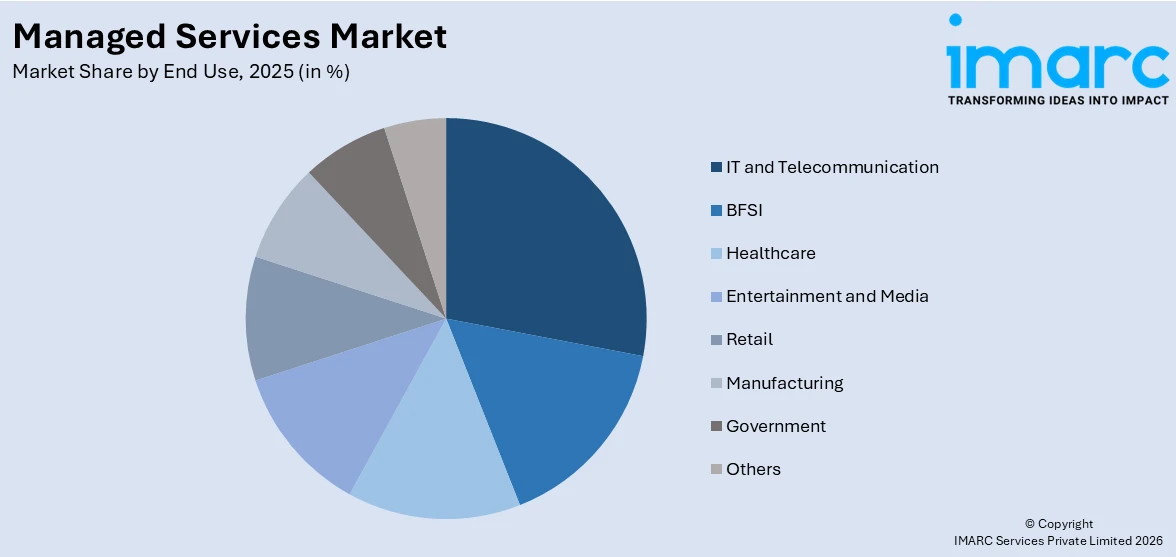

IT and telecommunication exhibit a clear dominance in the market

The report has provided a detailed breakup and analysis of the market based on the end use. This includes IT and telecommunication, BFSI, healthcare, entertainment and media, retail, manufacturing, government, and others. According to the report, IT and telecommunication represented the largest segment.

The IT and Telecommunication segment is the largest in the managed services market, driven by the constant need for reliable IT infrastructure and communication networks. Managed service providers in this segment offer a wide range of services, including network management, data center services, cloud computing, cybersecurity, and communication solutions. With rapid technological advancements and increasing complexity in IT environments, businesses in the IT and telecommunications sector rely heavily on managed services to enhance operational efficiency, reduce downtime, and ensure data security.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest managed services market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America represents the largest regional market for managed services.

The robust technological infrastructure, high levels of IT spending, and strong presence of key market players are driving the growth of the market in the North American region. The region is characterized by a mature landscape, with a wide range of industries such as healthcare, IT, manufacturing, and finance, relying heavily on managed services to streamline operations and enhance efficiency. Cloud computing adoption is particularly high in North America, further fueling the demand for managed services. According to the International Trade Administration, One-third of the $5 trillion global information technology (IT) market is in the United States, making it the largest tech market in the world. The industry accounts for $1.9 trillion of U.S. value-added GDP (more than 10 percent of the national economy) and 12.1 million jobs. According to CompTIA, there are more than 557,000 software and IT services companies in the United States (approximately 13,400 tech startups were established in 2019 alone).

Competitive Landscape:

The competitive landscape of the managed services market is highly competitive with major players such as Accenture, and IBM. These companies provide a broad range of services including IT infrastructure management, cloud solutions, and security services. Emerging players focus on niche markets and specialized services, driving differentiations and innovations. For instance, in May 2022, IBM announced that it had signed a strategic collaboration agreement (SCA) with Amazon Web Services, Inc. (AWS), with plans to offer a broad array of its software catalog as Software-as-a-Service (SaaS) in AWS.

The report provides a comprehensive analysis of the competitive landscape in the global managed services market with detailed profiles of all major companies, including:

- Accenture plc

- AT&T

- Capgemini

- Dell Inc.

- Fujitsu Limited

- Hewlett Packard Enterprise Development LP

- Infosys Limited

- International Business Machines Corporation

- Nokia Corporation

- Open Text Corporation

- Rackspace Technology

- Telefonaktiebolaget LM Ericsson

- Verizon

Managed Services Market News:

- In May 2024, Accenture announced the acquisition of Customer Management IT and SirfinPA, a pair of jointly owned Italian consultancies that operate in close synergy and offer innovative services and technology solutions in the justice and public safety sectors.

- In November 2023, AT&T announced an agreement to create a standalone managed cybersecurity services business, and a capital investment in that business from WillJam Ventures, a Chicago-based investor with deep cybersecurity industry and leadership experience.

- In March 2024, Dell Technologies and CrowdStrike announced an expanded strategic partnership to deliver Dell’s Managed Detection and Response (MDR) services with the industry-leading AI-native CrowdStrike Falcon XDR platform, helping customers defend against increasingly complex cyberattacks.

Managed Services Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Managed Infrastructure, Managed Data Center, Managed Security, Managed Communications, Managed Network, Managed Mobility |

| Deployment Modes Covered | Cloud-based, On-premises |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium-sized Enterprises |

| End Uses Covered | IT and Telecommunication, BFSI, Healthcare, Entertainment and Media, Retail, Manufacturing, Government, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Accenture plc, AT&T, Capgemini, Dell Inc., Fujitsu Limited, Hewlett Packard Enterprise Development LP, Infosys Limited, International Business Machines Corporation, Nokia Corporation, Open Text Corporation, Rackspace Technology, Telefonaktiebolaget LM Ericsson, Verizon, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the managed services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global managed services market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the managed services industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global managed services market was valued at USD 326.6 Billion in 2025.

We expect the global managed services market to exhibit a CAGR of 6.66% during 2026-2034.

The rising integration of advanced technologies, such as Artificial Intelligence (AI), the Internet of Things (IoT), and Machine Learning (ML), to reduce error rates, enable smart monitoring and compliance management, ensure the efficiency of processes, etc., is primarily driving the global managed services market.

The sudden outbreak of the COVID-19 pandemic has led to the growing adoption of managed services to focus on business continuity and constant monitoring, identity, and access management applications, during the remote working scenario.

Based on the type, the global managed services market has been segmented into managed infrastructure, managed data center, managed security, managed communications, managed network, and managed mobility. Among these, managed infrastructure currently holds the majority of the total market share.

Based on the deployment mode, the global managed services market can be divided into on-premises and cloud-based. Currently, on-premises exhibit a clear dominance in the market.

Based on the enterprise size, the global managed services market has been categorized into large enterprises and small and medium-sized enterprises, where large enterprises currently account for the majority of the global market share.

Based on the end use, the global managed services market can be segregated into IT and telecommunication, BFSI, healthcare, entertainment and media, retail, manufacturing, government, and others. Currently, the IT and telecommunication sector holds the largest market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global managed services market include Accenture plc, AT&T, Capgemini, Dell Inc., Fujitsu Limited, Hewlett Packard Enterprise Development LP, Infosys Limited, International Business Machines Corporation, Nokia Corporation, Open Text Corporation, Rackspace Technology, Telefonaktiebolaget LM Ericsson, and Verizon.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)