Macular Edema Market Size, Epidemiology, In-Market Drugs Sales, Pipeline Therapies, and Regional Outlook 2025-2035

Market Overview:

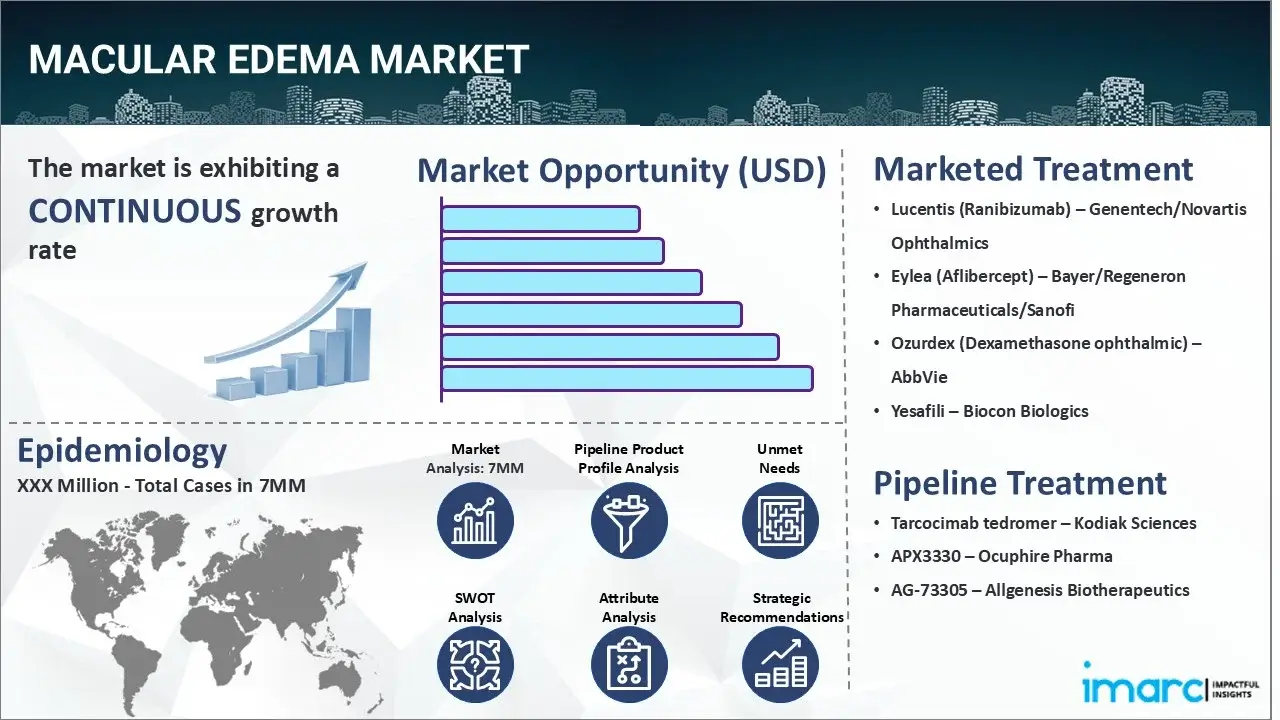

The Macular Edema market reached a value of USD 3.6 Billion across the top 7 markets (US, EU4, UK, and Japan) in 2024. Looking forward, IMARC Group expects the top 7 major markets to reach USD 5.9 Billion by 2035, exhibiting a growth rate (CAGR) of 4.51% during 2025-2035.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Base Year |

2024

|

| Forecast Years | 2025-2035 |

| Historical Years |

2019-2024

|

|

Market Size in 2024

|

USD 3.6 Billion |

|

Market Forecast in 2035

|

USD 5.9 Billion |

|

Market Growth Rate (2025-2035)

|

4.51% |

The Macular Edema market has been comprehensively analyzed in IMARC's new report titled "Macular Edema Market Size, Epidemiology, In-Market Drugs Sales, Pipeline Therapies, and Regional Outlook 2025-2035". Macular Edema refers to a condition characterized by the accumulation of fluid in the macula, which is the central portion of the retina responsible for sharp, detailed vision. This disease causes the macular tissue to swell, leading to distorted or blurred vision. The symptoms of the ailment can vary depending on the severity of the illness but may include impaired central vision, blank spots, decreased color perception, difficulty reading or performing detailed tasks, a sense of a dark or empty area in the center of vision, etc. The diagnosis of Macular Edema typically involves a comprehensive eye examination, along with a review of the patient's medical history and clinical features. The healthcare provider may also perform retinal imaging techniques, including optical coherence tomography (OCT), to obtain detailed cross-sectional pictures of the macula, which help to visualize any fluid accumulation and assess the severity of the ailment. Furthermore, indocyanine green angiography or fluorescein angiography is utilized to confirm a diagnosis by observing leakage or blockage in the retinal blood vessels.

To get more information on this market, Request Sample

The increasing cases of diabetic retinopathy, in which high blood sugar levels damage the retinal vessels, are primarily driving the Macular Edema market. In addition to this, the rising prevalence of trauma to the eye that can disrupt the normal structures and functions of the macula is creating a positive outlook for the market. Moreover, the widespread demand for intravitreal injections of anti-vascular endothelial growth factors to treat the ailment is further bolstering the market growth. These drugs inhibit the action of specific proteins that promote the development of abnormal blood vessels and increase vascular permeability in the retina, thereby reducing the leakage of fluid into the macula. Apart from this, the escalating application of laser therapy, since it delivers precise and controlled energy to the affected areas of the retina to stabilize vision and prevent the progression of the condition, is acting as another significant growth-inducing factor. Additionally, the emerging popularity of sustained-release implantable devices, which can slowly discharge medication over time and reduce inflammation in patients, is expected to drive the Macular Edema market during the forecast period.

IMARC Group's new report provides an exhaustive analysis of the Macular Edema market in the United States, EU4 (Germany, Spain, Italy, and France), United Kingdom, and Japan. This includes treatment practices, in-market, and pipeline drugs, share of individual therapies, market performance across the seven major markets, market performance of key companies and their drugs, etc. The report also provides the current and future patient pool across the seven major markets. According to the report, the United States has the largest patient pool for Macular Edema and also represents the largest market for its treatment. Furthermore, the current treatment practice/algorithm, market drivers, challenges, opportunities, reimbursement scenario, unmet medical needs, etc. have also been provided in the report. This report is a must-read for manufacturers, investors, business strategists, researchers, consultants, and all those who have any kind of stake or are planning to foray into the Macular Edema market in any manner.

Recent Developments:

- In April 2025, Regeneron Pharmaceuticals stated that the U.S. FDA had accepted for Priority Review the supplemental Biologics License Application (sBLA) for EYLEA HD (aflibercept) Injection 8 mg. The sBLA seeks approval for EYLEA HD for both the treatment of macular edema following retinal vein occlusion and for broadening the dosing schedule to include every 4-week dosing across approved indications.

- In November 2023, Allgenesis Biotherapeutics released exciting preliminary data from the first-in-human, Phase 2a clinical trial assessing the safety, tolerability, and efficacy of AG-73305 in diabetic macular edema patients.

Drugs:

Lucentis (ranibizumab) treats macular edema by inhibiting vascular endothelial growth factor A (VEGF-A), a protein that promotes abnormal blood vessel growth and leakage. By binding to VEGF-A, ranibizumab prevents it from interacting with its receptors on endothelial cells, thus reducing their proliferation, vascular permeability, and the formation of new blood vessels. This mechanism helps to decrease fluid buildup in the macula, a key area of the retina, and improve or stabilize vision.

Tarcocimab tedromer, is an investigational anti-VEGF (Vascular Endothelial Growth Factor) therapy developed by Kodiak Sciences. It works by binding to VEGF-A, a protein that promotes the growth of new blood vessels and increases vascular permeability, to inhibit its activity and reduce the effects of macular edema.

APX3330 is a small molecule that inhibits Ref-1, a transcription factor regulator. This dual mechanism blocks downstream pathways involved in angiogenesis (like VEGF) and inflammation (like NF-κB), which are implicated in diabetic macular edema and other ocular diseases. By inhibiting Ref-1, APX3330 aims to reduce abnormal blood vessel growth (angiogenesis) and inflammation, both of which contribute to diabetic macular edema.

Time Period of the Study

- Base Year: 2024

- Historical Period: 2019-2024

- Market Forecast: 2025-2035

Countries Covered

- United States

- Germany

- France

- United Kingdom

- Italy

- Spain

- Japan

Analysis Covered Across Each Country

- Historical, current, and future epidemiology scenario

- Historical, current, and future performance of the macular edema market

- Historical, current, and future performance of various therapeutic categories in the market

- Sales of various drugs across the macular edema market

- Reimbursement scenario in the market

- In-market and pipeline drugs

Competitive Landscape:

This report also provides a detailed analysis of the current macular edema marketed drugs and late-stage pipeline drugs.

In-Market Drugs

- Drug Overview

- Mechanism of Action

- Regulatory Status

- Clinical Trial Results

- Drug Uptake and Market Performance

Late-Stage Pipeline Drugs

- Drug Overview

- Mechanism of Action

- Regulatory Status

- Clinical Trial Results

- Drug Uptake and Market Performance

| Drugs | Company Name |

|---|---|

| Lucentis (Ranibizumab) | Genentech/Novartis Ophthalmics |

| Eylea (Aflibercept) | Bayer/Regeneron Pharmaceuticals/Sanofi |

| Ozurdex (Dexamethasone ophthalmic) | AbbVie |

| Yesafili | Biocon Biologics |

| Tarcocimab tedromer | Kodiak Sciences |

| APX3330 | Ocuphire Pharma |

| AG-73305 | Allgenesis Biotherapeutics |

*Kindly note that the drugs in the above table only represent a partial list of marketed/pipeline drugs, and the complete list has been provided in the report.

Key Questions Answered in this Report:

Market Insights

- How has the macular edema market performed so far and how will it perform in the coming years?

- What are the markets shares of various therapeutic segments in 2024 and how are they expected to perform till 2035?

- What was the country-wise size of the macular edema across the seven major markets in 2024 and what will it look like in 2035?

- What is the growth rate of the macular edema across the seven major markets and what will be the expected growth over the next ten years?

- What are the key unmet needs in the market?

Epidemiology Insights

- What is the number of prevalent cases (2019-2035) of macular edema across the seven major markets?

- What is the number of prevalent cases (2019-2035) of macular edema by age across the seven major markets?

- What is the number of prevalent cases (2019-2035) of macular edema by gender across the seven major markets?

- What is the number of prevalent cases (2019-2035) of macular edema by type across the seven major markets?

- How many patients are diagnosed (2019-2035) with macular edema across the seven major markets?

- What is the size of the macular edema patient pool (2019-2024) across the seven major markets?

- What would be the forecasted patient pool (2025-2035) across the seven major markets?

- What are the key factors driving the epidemiological trend macular edema of?

- What will be the growth rate of patients across the seven major markets?

Macular Edema: Current Treatment Scenario, Marketed Drugs and Emerging Therapies

- What are the current marketed drugs and what are their market performance?

- What are the key pipeline drugs and how are they expected to perform in the coming years?

- How safe are the current marketed drugs and what are their efficacies?

- How safe are the late-stage pipeline drugs and what are their efficacies?

- What are the current treatment guidelines for macular edema drugs across the seven major markets?

- Who are the key companies in the market and what are their market shares?

- What are the key mergers and acquisitions, licensing activities, collaborations, etc. related to the macular edema market?

- What are the key regulatory events related to the macular edema market?

- What is the structure of clinical trial landscape by status related to the macular edema market?

- What is the structure of clinical trial landscape by phase related to the macular edema market?

- What is the structure of clinical trial landscape by route of administration related to the macular edema market?

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Inquire Before Buying

Inquire Before Buying

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Request Customization

Request Customization

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)