Machine Risk Assessment Market Size, Share, Trends and Forecast by Type, Enterprise Size, Vertical, and Region, 2025-2033

Machine Risk Assessment Market Size and Share:

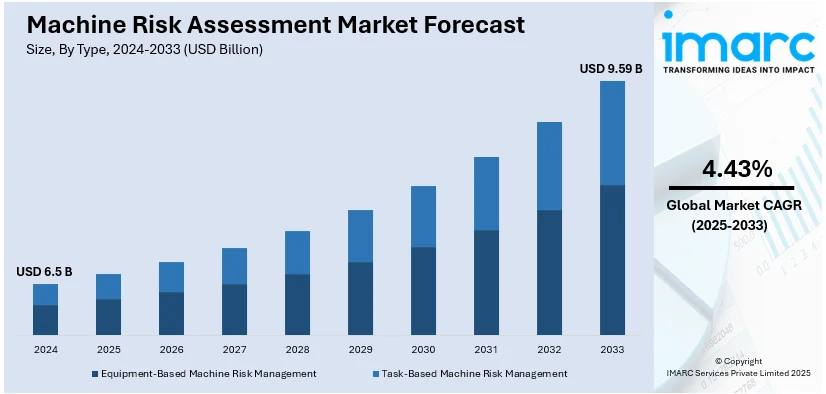

The global machine risk assessment market size was valued at USD 6.5 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 9.59 Billion by 2033, exhibiting a CAGR of 4.43% from 2025-2033. North America currently dominates the market, holding a market share of over 36.5% in 2024. Rapid industrialization, a rising incidence of accidents and injuries related to industrial machinery operations, and a heightened emphasis on workplace safety standards represent some of the key factors boosting the machine risk assessment market share in this region.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024 |

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 9.59 Billion |

| Market Growth Rate (2025-2033) | 4.43% |

Increasingly stringent workplace safety regulations, particularly in sectors such as manufacturing and construction, are driving the global market for machine risk assessment. Strict laws for safety insist on the frequency of risk assessments to remain compliant and protect workers because the international construction industry will be expected to grow more than USD 4.2 trillion in the next 15 years. The emerging cases of machinery and the inadequacies in regulatory frameworks are another factor driving the call for advanced risk management systems. Additionally, the market grows due to widespread application of automation and technological advancements such as artificial intelligence (AI), the Internet of Things (IoT), cloud computing, and machine learning. Moreover, the surge of IoT-connected devices to 18.8 billion and cybersecurity threats increase emphasize that machines are more than just need to undergo a critical assessment.

The United States is emerging as a key market with 83.8% shares. Increasing focus on workplace safety standards, especially in risky sectors such as manufacturing and construction, where regular risk assessments are mandatory is driving the growth of the market. In addition to this, the growing machinery-related accidents have led to an increased demand for specific, all-risk risk management solutions. The complexity of regulatory frameworks is increasing, and hence organizations need to have strong risk assessment protocols in place to comply with the rules. In addition, the growing use of automation and advanced technologies, such as AI and IoT, emphasizes the growing need for strong risk assessment strategies to mitigate potential hazards associated with modern industrial machinery.

Machine Risk Assessment Market Trends:

Rising Workplace Safety Standards and Regulatory Compliance

The increasing emphasis on employee safety, especially in high-risk industries such as manufacturing and construction, is one of the primary drivers fueling the growth of the machine risk assessment market. Governments and regulatory agencies around the globe are imposing stringent safety laws to minimize the risks involved with industrial machinery. In order to ensure the safety of workers, industries need to undertake risk assessments periodically, which in turn increases the demand for risk assessment tools. For example, there needs to be a thorough safety analysis because the global construction industry is predicted to expand to a value greater than USD 4.2 trillion in the coming 15 years. In addition to this, compliance with occupational health and safety standards needs to be followed by this changing regulatory landscape. To achieve this, organizations are compelled to establish strong risk management systems.

Rising Machinery-Related Accidents and Complex Compliance Requirements

Successful risk assessment procedures are paramount, as proven by the increased incidence of occupational injuries with industrial machinery. Companies should institute active risk management strategies in order to identify and effectively deal with any threats in light of increasing complexity within industrial environments. The need for systematic assessments is also heightened by the continuously evolving compliance and regulatory landscape, which ensures that companies keep responding to industry safety standards. Companies are investing in advanced risk assessment systems to deal with intricate regulatory regimes and minimize the risk of fines and disruptions to their operations.

Growing Adoption of Automation and Technological Advancements

Demand is the main contributor to the increase in machine risk assessments caused by widespread automation in the manufacturing, shipping, and warehousing industries. Automated systems also present new risks that must be constantly evaluated and managed to avoid operational failure and workplace hazards. Risk assessment techniques have also changed with advancements in machine learning, artificial intelligence, cloud computing, and the Internet of Things. For example, 18.8 billion IoT-connected devices are available globally today, a 13% rise. This is one of the crucial roles played by technology in managing and assessing risk. Also, companies are compelled to implement advanced risk management systems as there is increased worry over cybersecurity threats to automated systems.

Machine Risk Assessment Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global machine risk assessment market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on type, enterprise size, and vertical.

Analysis by Type:

- Equipment-Based Machine Risk Management

- Task-Based Machine Risk Management

Equipment-based machine risk management dominates the market, accounting for 57.6% of the total share, owing to the growing need for safety evaluations in industries that rely largely on machinery, such as manufacturing, construction, and logistics. Strict regulatory requirements requiring frequent risk assessments to guarantee worker safety and avoid operational breakdowns are driving this segment's growth. In order to reduce possible risks, the growing use of automation and smart manufacturing also calls for ongoing equipment monitoring and evaluation. Additionally, the efficacy of equipment-based risk assessments is being improved by developments in technologies like as IoT, AI, and predictive analytics. Businesses are spending more money on sophisticated risk management systems to guarantee compliance and raise workplace safety standards as a result of the complexity of industrial safety requirements.

Analysis by Enterprise Size:

- Small and Medium-sized Enterprises

- Large Enterprises

Large enterprises have dominated the market for machine risk assessment, with 63.8% of the market share, as they make significant use of industrial machinery and follow strict rules and regulations. They operate in industries such as construction, manufacturing, oil and gas, and logistics, which are considered to be high-risk, and still consider worker safety paramount. Large enterprises with sufficient funds allocate large sums in advanced risk assessment technologies, employing AI, IoT, and predictive analytics to secure operations and minimize operational risks. In addition, the complexity of automation and machinery in large-scale operations requires routine and comprehensive risk assessments to ensure legal compliance and avoid costly blunders. Large businesses will remain at the forefront of implementing new risk management approaches for better operational safety as industrial automation continues to grow.

Analysis by Vertical:

- Automotive

- Food & Beverages

- Consumer Electronics

- Industrial

- Healthcare

- Others

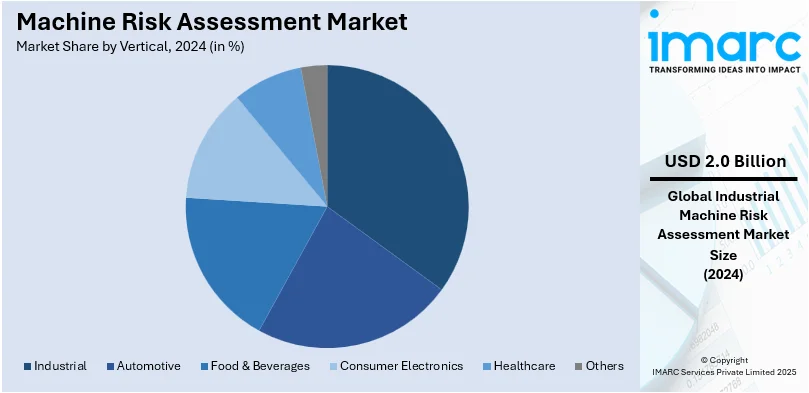

With 30.0% of the market share, the industrial sector is the largest vertical in the machine risk assessment industry. The extensive use of automated systems and large machinery in sectors like manufacturing, automotive, oil and gas, and energy is what is responsible for this domination. The need for risk assessment solutions is being driven primarily by the requirement for operational efficiency, strict workplace safety rules, and an increase in accidents involving machinery. Additionally, by enabling real-time monitoring and proactive hazard mitigation, the rapid integration of Industry 4.0 technologies—such as IoT, AI, and predictive analytics—is enhancing risk assessment capabilities. Businesses are spending more money on thorough safety evaluations as industrial automation grows in order to guarantee regulatory compliance, minimize downtime, and improve worker safety, which strengthens the industry's leadership.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

With 36.5% of the market share, North America leads the machine risk assessment industry. A greater focus on workplace safety laws and an increase in industrial accidents are the main drivers of this growth. Industries are adopting sophisticated safety solutions as a result of regulatory agencies like the Occupational Safety and Health Administration (OSHA) enforcing strict adherence to risk assessment processes. The need for machine risk assessments is also being driven by the quick spread of automation and Industry 4.0 technologies in the construction, manufacturing, and logistics sectors. Businesses are able to proactively identify and minimize machinery-related dangers because to the increasing deployment of IoT, AI, and predictive maintenance technologies. Due to the United States' leadership in industrial automation, businesses are giving risk management solutions top priority in order to improve worker safety, operational effectiveness, and regulatory compliance. This trend is expected to continue as automation and safety standards evolve.

Key Regional Takeaways:

United States Machine Risk Assessment Market Analysis

The expanding demand in the automotive sector is a major factor driving the increased acceptance of machine risk assessment in the United States. For example, since the beginning of 2021, automakers have declared plans to invest over USD 75 billion in the United States. Improved safety regulations, economy, and risk reduction are more important than ever as the automobile industry grows. As a consequence, machine risk assessments are used to analyze possible risks, find weaknesses in equipment, and improve general safety procedures in production operations. The requirement to operate complicated machinery and the increase in automation both promote the use of risk assessments. Additionally, the trend toward the implementation of risk assessments is fueled by rules in the automobile industry that require more thorough safety procedures. As such, the growing automotive sector leads to a surge in machine risk assessments, ensuring operational reliability and worker safety, while minimizing downtime and ensuring compliance with industry standards.

Europe Machine Risk Assessment Market Analysis

Machine risk assessments are increasingly common across Europe due to the rapid growth of the industrial sector and increased production capacity. Industrial production within the EU grew by 8.5% in 2021 from 2020 and by 0.4% in 2022 from 2021. With increasing industrial production, more emphasis is laid on ensuring regulatory compliance, streamlining safety protocols, and reducing machinery risks. Machine hazard assessment and mitigation are more critical as automation increases to ensure a safe and efficient workplace. The evaluation of potential hazards at every production stage is increasingly becoming essential as industrial technology advances.

Asia Pacific Machine Risk Assessment Market Analysis

The growth of small and medium-sized businesses (SMEs) in the Asia-Pacific area is fueling the expanding use of machine risk assessment. The number of MSMEs in the nation is expected to increase from 6.3 crore to around 7.5 crore at a compound annual growth rate (CAGR) of 2.5%, according to the India Brand Equity Foundation. The need to control operational risks, guarantee machine safety, and simplify operations has become increasingly important as SMEs proliferate across a variety of industries. Small firms understand how important it is to reduce machine risks in order to prevent expensive interruptions, legal penalties, and equipment failure. The need for improved safety procedures, which guarantee the efficient operation of machinery and avoid accidents, is fueled by the region's growing industry.

Latin America Machine Risk Assessment Market Analysis

Latin America has seen the growing adoption of machine risk assessments mainly due to increasing demand for consumer electronics because of rising disposable income. Latin America's total disposable income is likely to grow by nearly 60% between 2021 and 2040, as per reports. The growing demand for electronics forces manufacturers to ensure their machinery is safe, efficient, and without any risk to the workers or consumers. The pressure for sustained production along with the integration of safety enhances the adoption rate of machine risk assessment. Enhanced disposable income opens doors to spending in safety technology that makes risk management easier, helping manufacturers not just reduce risk levels but ensure optimum efficiency during the process. Along with that expansion, there arises a demand to have adequate measures for proper control over risk regarding production as well as safety risks.

Middle East and Africa Machine Risk Assessment Market Analysis

Increasing construction sectors of the Middle East and African continents are driving machine risk assessment into these regions. The Saudi construction sector is seen to be booming, with over 5,200 projects valuing USD 819 billion in progress. To assess and monitor the risk attached to the operation of heavy machines used in construction, there has been increasing necessity. Since construction equipment is often used intensively and in harsh conditions, machine risk assessments are crucial to ensuring the safety of people and equipment. Businesses are prompted to incorporate machine risk assessments into their operations by the growing focus on safety and risk minimization, which reduces accidents and ensures compliance with safety regulations. The rising demand for construction-related machinery and safety management leads to a growing emphasis on risk assessments in the sector.

Competitive Landscape:

To enhance their market share, some prominent players in the highly competitive global machine risk assessment market are focusing on technology advancements, regulatory compliance solutions, and strategic partnerships. Dominant businesses dominate the market by offering comprehensive risk assessment services, industry-specific certification, and compliance solutions. To enhance their service portfolio, these businesses are investing heavily in AI-based risk analysis, IoT-based safety monitoring, and predictive maintenance solutions. Apart from that, in their bid to expand their global reach and service the increased need for security solutions, the industry is also witnessing mergers, acquisitions, and partnerships increasing in numbers. The industry is witnessing entries from startup firms and middle-tier businesses aimed at attracting small and medium-scale businesses (SMEs), along with automated and affordable risk assessment solutions. With the growing complexity of safety regulations and industrial automation, competition is expected to intensify, driving further innovation in risk assessment solutions.

The report provides a comprehensive analysis of the competitive landscape in the machine risk assessment market with detailed profiles of all major companies, including:

- Advanced Technology Services Inc.

- Intertek Group plc

- Keyence Corp.

- Omron Corporation

- Pilz GmbH & Co. KG

- Rockford Systems LLC

- Rockwell Automation Inc.

- SICK AG, Stantec Inc.

- TÜV Nord Group

Latest News and Developments:

- October 2024: SailPoint has launched Machine Identity Security, a new product designed to simplify the management, security, and lifecycle of machine identities like service accounts and bots. This product addresses the gap in enterprise security, as 66% of companies still use manual processes for machine identity management. The move comes in response to the growing risk of unmanaged machine identities, with 72% of security professionals finding them more difficult to handle than human identities.

- September 2024: MicroSec has launched CyberAssessor for OT/ICS, an AI-based cybersecurity platform designed for IEC 62443 assessments. The tool automates risk evaluations, enhancing compliance accuracy at both site and device levels. It offers a comprehensive risk summary and automatic reports on an organization’s security and compliance status.

- September 2024: Doitup Innovative Technologies has launched IntelliRMS, an AI-driven Integrated Risk Management System tailored for SMBs. The system uses machine learning to assess and predict risks like cyber threats, operational disruptions, and regulatory changes. IntelliRMS enables businesses to identify, mitigate, and monitor risks with real-time adaptability.

- August 2024: HITRUST has launched its AI Risk Management (AI RM) Assessment, the first comprehensive approach to managing AI-related risks. This new offering aligns with standards from NIST and ISO/IEC, providing companies with tools to demonstrate effective AI risk governance. The assessment aids organizations in communicating their AI risk management efforts to stakeholders, ensuring alignment with industry best practices.

- January 2024: Tech Mahindra has launched i.Riskman, an ESG risk assessment platform to help organizations identify and manage climate-related risks. The platform offers automated risk registers and supports enterprise risk management with a flexible, scalable solution. i.Riskman enables businesses to assess the impact of climate risks on strategies, finances, and overall exposure.

Machine Risk Assessment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Equipment-Based Machine Risk Management, Task-Based Machine Risk Management |

| Enterprise Sizes Covered | Small and Medium-Sized Enterprises, Large Enterprises |

| Verticals Covered | Automotive, Food & Beverages, Consumer Electronics, Industrial, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Advanced Technology Services Inc., Intertek Group plc, Keyence Corp., Omron Corporation, Pilz GmbH & Co. KG, Rockford Systems LLC, Rockwell Automation Inc., SICK AG, Stantec Inc., TÜV Nord Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the machine risk assessment market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global machine risk assessment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the machine risk assessment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The machine risk assessment market was valued at USD 6.5 Billion in 2024.

IMARC Group estimates the market to reach USD 9.59 Billion by 2033, exhibiting a CAGR of 4.43% from 2025-2033.

The market is driven by stringent workplace safety regulations, increasing industrial accidents, and the rapid adoption of automation and Industry 4.0 technologies. Additionally, advancements in AI, IoT, and predictive analytics enhance risk assessment efficiency, while rising cybersecurity concerns further boost demand for robust safety solutions.

North America currently dominates the market, accounting for 36.5% of the total share, due to strict regulatory compliance (OSHA), rising industrial automation, and increasing workplace safety concerns. The region's focus on advanced risk management technologies and the high adoption of predictive maintenance solutions further contribute to its market leadership.

Some of the major players in the machine risk assessment market include Advanced Technology Services Inc., Intertek Group plc, Keyence Corp., Omron Corporation, Pilz GmbH & Co. KG, Rockford Systems LLC, Rockwell Automation Inc., SICK AG, Stantec Inc., TÜV Nord Group, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)