Lyocell Fiber Market Size, Share, Trends and Forecast by Product, Application, and Region, 2026-2034

Global Lyocell Fiber Market Size, Share, Trends & Forecast (2026-2034)

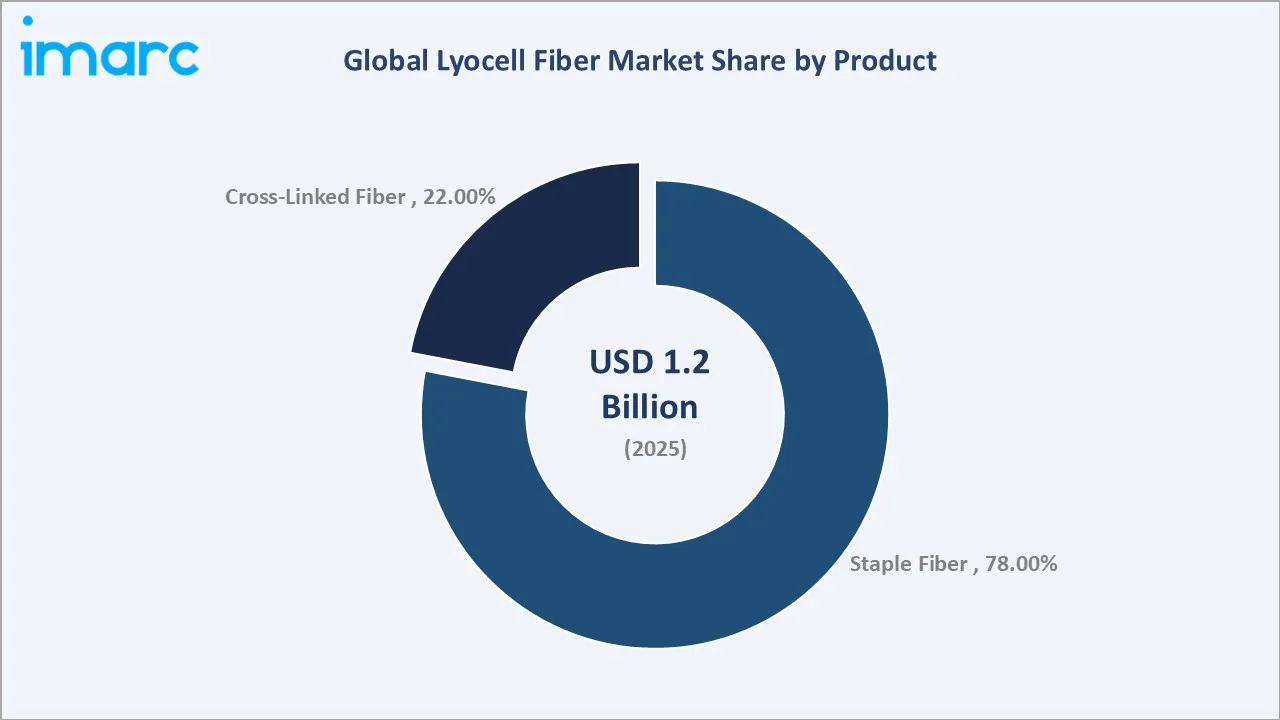

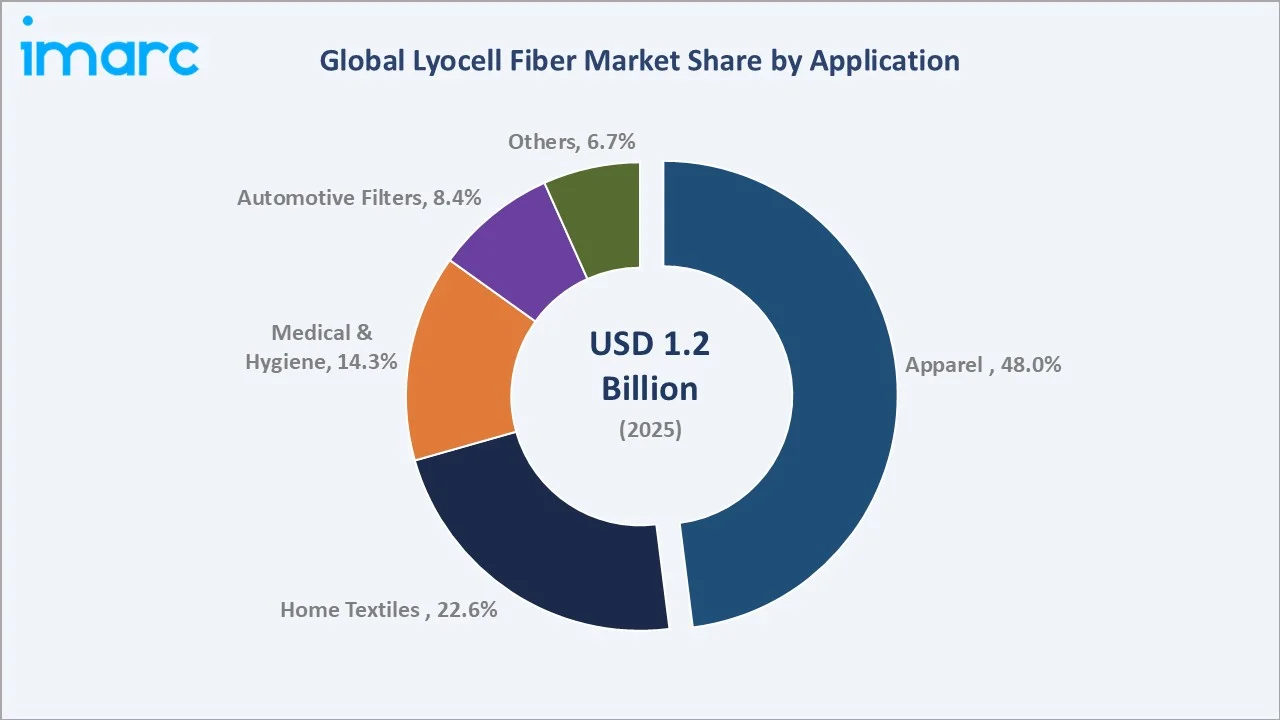

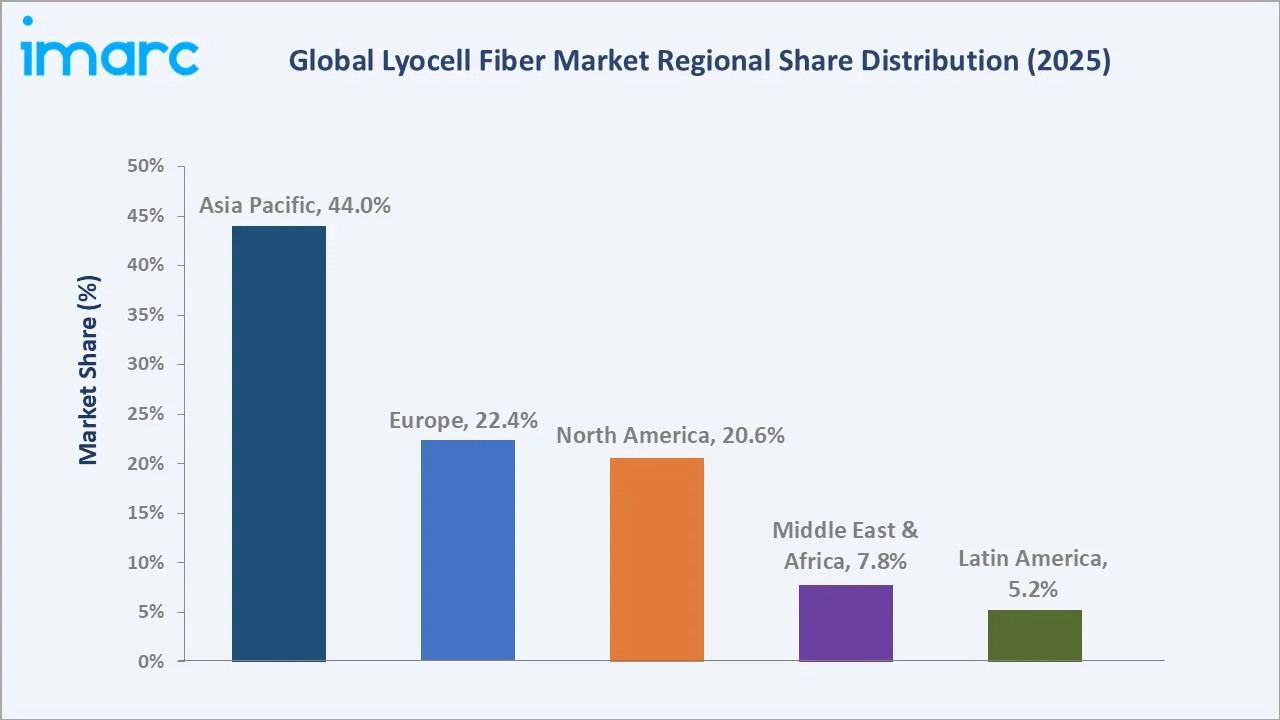

The global lyocell fiber market size was valued at USD 1.2 Billion in 2025 and is projected to reach USD 2.3 Billion by 2034, exhibiting a CAGR of 5.2% during the forecast period 2026-2034. Rising consumer demand for sustainable, biodegradable textiles, tightening environmental regulations mandating eco-friendly fiber production, and expanding applications across apparel, home textiles, healthcare, and automotive filtration are driving the lyocell fiber market growth. Staple Fiber leads the product segment at 78.0% in 2025, while Apparel dominates the application segment at 48.0%. Asia Pacific accounts for 44.0% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.2 Billion |

|

Forecast Market Size (2034) |

USD 2.3 Billion |

|

CAGR (2026-2034) |

5.2% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (44.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Product Segment |

Staple Fiber (78.0%, 2025) |

|

Leading Application Segment |

Apparel (48.0%, 2025) |

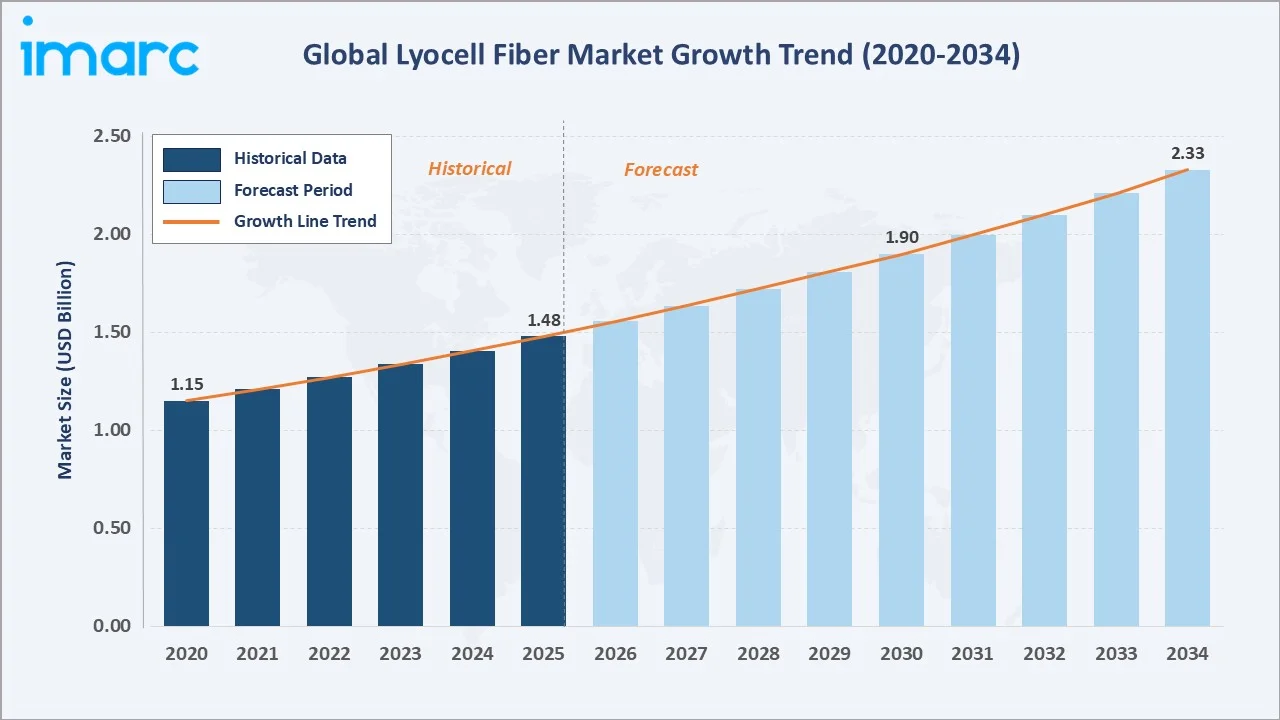

The global lyocell fiber market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by sustainability mandates, eco-conscious consumer demand, and expanding technical applications across healthcare, automotive, and industrial sectors.

To get more information on this market, Request Sample

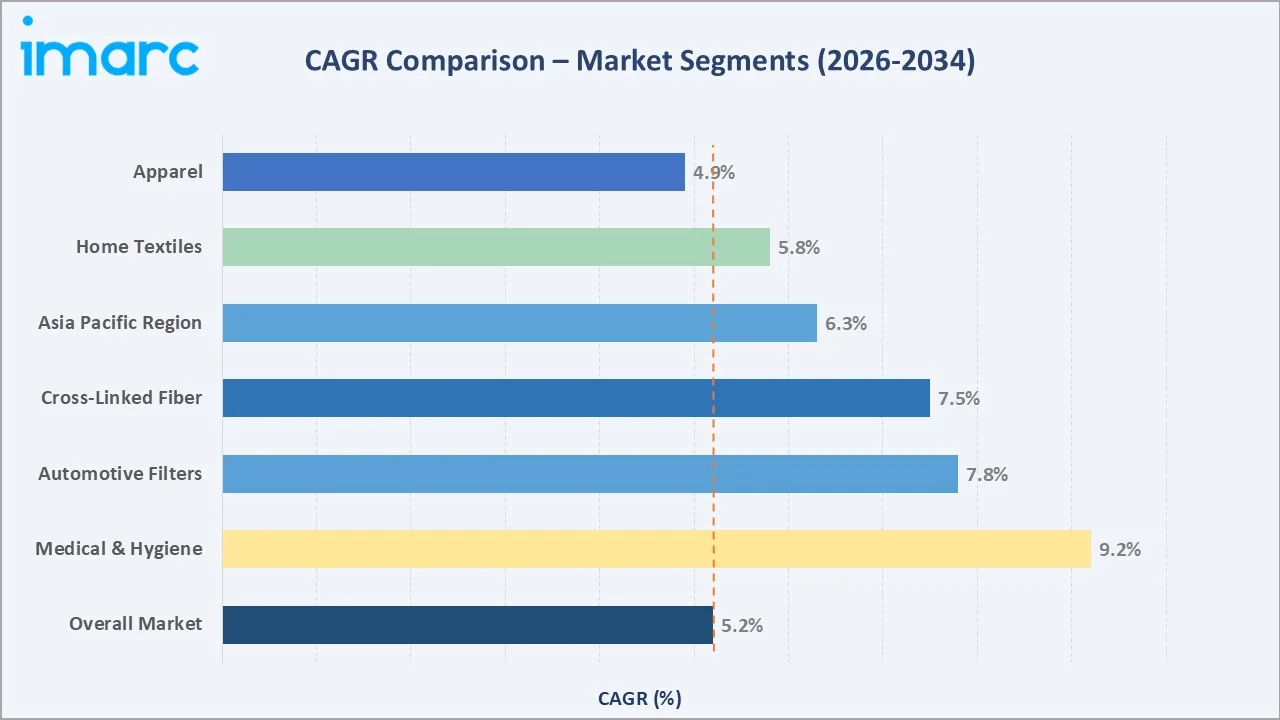

CAGR growth curve highlighting the lyocell fiber market's steady compounding trajectory from USD 1.2 Billion in 2025 to USD 2.3 Billion by 2034 at 5.2% CAGR, driven by accelerating sustainable textile adoption across major global end-use industries.

Executive Summary

The global lyocell fiber market is undergoing a structural expansion driven by the worldwide textile industry's transition toward sustainable, biodegradable, and low-impact materials. Valued at USD 1.2 Billion in 2025, the market is forecast to reach USD 2.3 Billion by 2034 at a CAGR of 5.2%. Lyocell – derived from wood pulp via a closed-loop solvent process recovering over 99% of chemicals – is gaining significant traction as a premium eco-alternative to polyester, viscose, and conventional cotton.

Staple fiber commands 78.0% of the product mix in 2025, supported by its compatibility with conventional cotton-system spinning machinery, which reduces capital investment for mills adopting lyocell. Cross-linked lyocell at 22.0% is gaining momentum in automotive filter media and technical nonwovens. Apparel represents the largest application at 48.0%, driven by Lyocell's moisture management, hypoallergenic properties, and silk-like drape. The medical and hygiene segment – growing at approximately 9.2% CAGR – is the fastest-expanding application, fueled by plastic bans and biodegradable disposable product mandates across multiple jurisdictions.

Asia Pacific leads global consumption with a 44.0% revenue share in 2025, supported by China's vast textile manufacturing base, India's expanding sustainable fiber industry through producers such as Birla Cellulose, and government-mandated environmental compliance. Europe (22.4%) and North America (20.6%) follow, driven by EU Circular Economy regulations and growing eco-conscious consumer spending.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Staple Fiber - 78.0% share (2025) |

|

Largest Application Segment |

Apparel - 48.0% share (2025) |

|

Fastest Growing Application |

Medical & Hygiene - ~9.2% CAGR (2026-2034) |

|

Leading Region |

Asia Pacific - 44.0% revenue share (2025) |

|

Second Largest Region |

Europe - 22.4% revenue share (2025) |

|

Top Companies |

Lenzing AG, Aditya Birla, Sateri, AceGreen, Baoding Swan |

Key Analytical Observations Supporting The Above Data:

- Staple Fiber's 78.0% dominance in 2025 reflects its broad commercial versatility and compatibility with existing spinning infrastructure, making it the preferred form for apparel and home textile mills globally.

- Apparel's 48.0% application share is driven by lyocell's superior moisture absorption (50% greater than cotton), hypoallergenic properties, and its growing adoption in sustainable denim, activewear, and intimate apparel by eco-committed brands.

- Asia Pacific's 44.0% global revenue dominance reflects the region's position as the world's largest textile manufacturing hub, with China, India, Vietnam, and Bangladesh collectively accounting for the majority of lyocell spinning and weaving capacity.

- The Medical & Hygiene segment at 14.3% is the fastest growing application, with multi-country plastic bans and hospital procurement mandates for biodegradable nonwovens driving lyocell adoption in wound care, baby care, and feminine hygiene.

- Cross-linked lyocell (22.0% product share) is gaining traction in automotive filters and technical textiles due to enhanced dimensional stability and fibrillation resistance versus standard lyocell grades.

Global Lyocell Fiber Market Overview

Lyocell fiber is a cellulose-based regenerated fiber produced by dissolving wood pulp – typically from eucalyptus, spruce, or pine – in an amine oxide solvent (NMMO) through a patented closed-loop process. The system recovers over 99% of chemicals in continuous cycles, generating minimal waste and no harmful effluents. Lyocell delivers exceptional performance: high tensile strength in both wet and dry states, moisture absorption, breathability, biodegradability, and hypoallergenic skin compatibility.

Applications span the full textile and industrial spectrum: apparel (activewear, denim, intimate wear), home textiles (bedsheets, curtains, upholstery), medical and hygiene products (wound care, wipes, nonwovens), automotive filter media, and emerging technical composite uses. By 2025, leading producers such as Sateri have individually scaled lyocell fiber capacity to ~400,000 metric tons annually, reflecting the rapid industrialization of the segment, while total global capacity has already exceeded this level.

Macroeconomic enablers include intensifying ESG investment mandates and a sharp rise in consumer sustainability awareness, with over 60% of consumers willing to alter purchasing behaviour and nearly 80% prioritizing sustainable products. Concurrently, increasing regulatory scrutiny and disclosure requirements across Europe, North America, and the Asia Pacific are structurally reshaping textile supply chains, creating favourable conditions for bio-based fibers such as lyocell.

Market Dynamics

To evaluate market opportunities, Request Sample

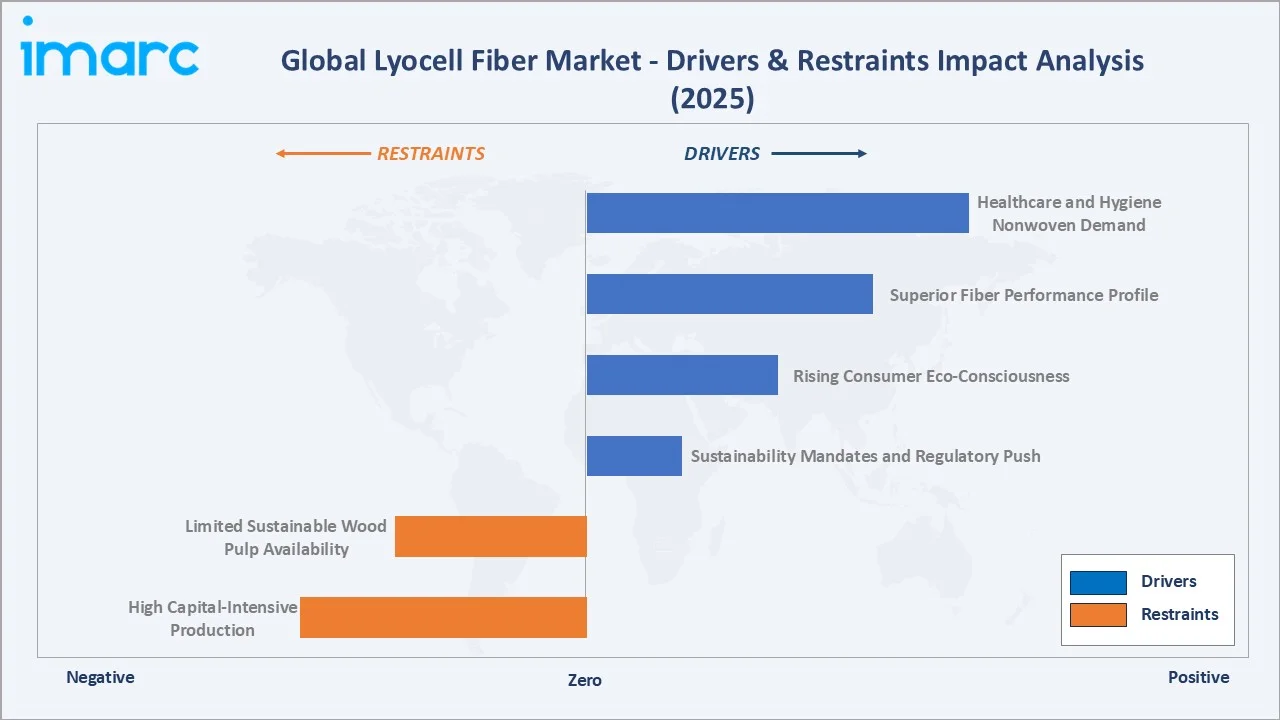

Market Drivers

- Sustainability Mandates and Regulatory Push: The EU’s textile strategy targets fully durable, repairable, and recyclable products by 2030, backed by eco-design and extended producer responsibility rules. In parallel, tightening but fragmented Asia Pacific regulations on water, emissions, and circularity are collectively driving demand for low-impact fibers like lyocell.

- Rising Consumer Eco-Consciousness: Sustainability-driven consumption is becoming a key demand driver, with consumers increasingly factoring environmental impact into purchases. In response, fashion brands are expanding the use of lyocell and other MMCFs, driven largely by Generation Z’s influence on sustainable fashion and brand accountability.

- Superior Fiber Performance Profile: Lyocell absorbs up to 50% more moisture than cotton and dries significantly faster. Its closed-loop manufacturing cuts water use by up to 80% versus conventional viscose. These measurable performance and sustainability advantages are compelling manufacturers to reformulate sourcing strategies.

- Healthcare and Hygiene Nonwoven Demand: Restrictions on single-use plastic nonwoven materials across multiple markets, coupled with tightening hospital procurement standards favouring biodegradable disposables, are driving sustained structural demand in the medical and hygiene segment.

Market Restraints

- High Capital-Intensive Production: Lyocell's closed-loop NMMO solvent infrastructure requires significantly higher capital investment versus conventional viscose or polyester production, limiting market entry and restricting adoption in cost-sensitive emerging market applications.

- Limited Sustainable Wood Pulp Availability: Lyocell production depends on FSC or PEFC-certified wood pulp from responsibly managed forests. Supply constraints and deforestation concerns can disrupt supply chains and create cost volatility, particularly when certification capacity is insufficient to meet rapidly growing demand.

Market Opportunities

- Technical Textile and Composite Applications: Lyocell-based carbon fiber precursors are emerging as a sustainable alternative to PAN, offering renewable feedstocks and potential cost advantages. Though still at an early stage, they present a high-value opportunity in lightweight automotive and aerospace composites.

- Emerging Market Adoption: India, Vietnam, and Bangladesh are accelerating lyocell adoption to meet the sustainable sourcing requirements of European and North American brands, with India's Birla Cellulose expanding capacity to serve both domestic and export demand.

Market Challenges

- Competition from Established Fibers: Cotton, polyester, and viscose have deeply entrenched supply chains and cost advantages. Lyocell's higher price point deters cost-sensitive manufacturers, and well-established economies of scale in alternative fibers make market-share gains challenging at the mass-market level.

- Inconsistent Certification Standards: Differing sustainability certification standards across geographies complicate compliance for global producers and create barriers to seamless cross-border procurement and consumer-facing sustainability claims.

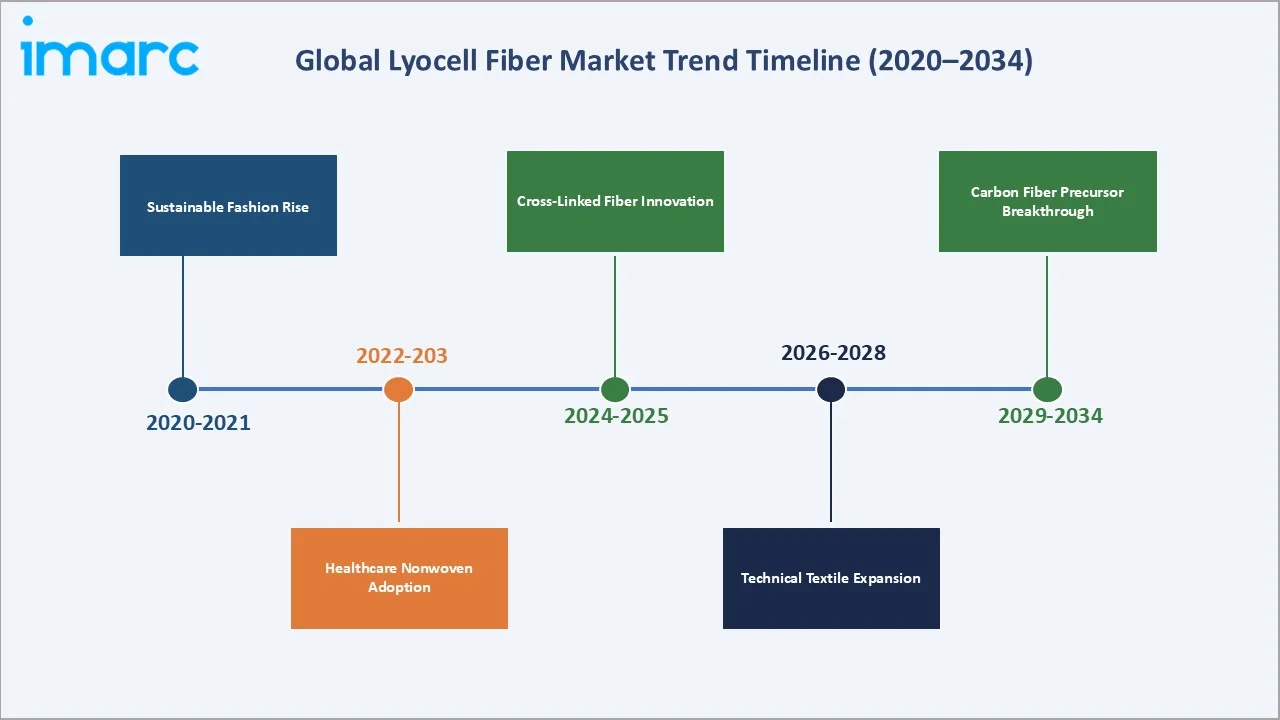

Emerging Market Trends

1. Accelerating Sustainable Fashion Integration

Fashion brands are accelerating the use of lyocell and other man-made cellulosic fibers in response to sustainability-driven consumer demand, particularly from Generation Z. At the same time, initiatives such as Asia Pacific Rayon’s collaborations at Jakarta Fashion Week reflect the expanding adoption of sustainable fibers beyond traditional European markets into emerging fashion ecosystems.

2. Healthcare Nonwoven Demand Structural Surge

Regulatory curbs on single-use plastics—led by the EU’s Single-Use Plastics Directive—are accelerating the shift toward biodegradable nonwovens in hygiene and medical applications, driving increased adoption of lyocell and other cellulosic fibers as sustainable alternatives.

3. Cross-Linked Fiber Innovation for Technical Applications

Advances in cross-linking and surface engineering are enhancing Lyocell’s structural stability, unlocking applications in high-performance nonwovens, filtration, and composite materials. In parallel, the development of lyocell-derived carbon fiber precursors highlights a longer-term opportunity to introduce renewable feedstocks into advanced composites, positioning the segment as a potential high-value growth frontier.

4. Closed-Loop Technology Advancement Improving Cost Position

Advancements in NMMO solvent recovery systems are pushing chemical recovery rates to near-complete levels, improving process efficiency and reducing production costs. In parallel, Lenzing Group’s introduction of stretch lyocell technologies in 2024 highlights the growing viability of cellulosic fibers as alternatives to synthetic stretch materials, supporting more sustainable apparel solutions.

5. Blended Fiber Development for Luxury and Performance Markets

Lyocell blends with silk, wool, recycled cotton, and recycled polyester are gaining traction in luxury fashion. Milano Unica featured lyocell-blend lay-up fabrics combining recycled silk and wool, proving versatility for luxury houses seeking circular inputs. Recycled-content lyocell variants are improving consistency through newly calibrated pulp homogenization processes.

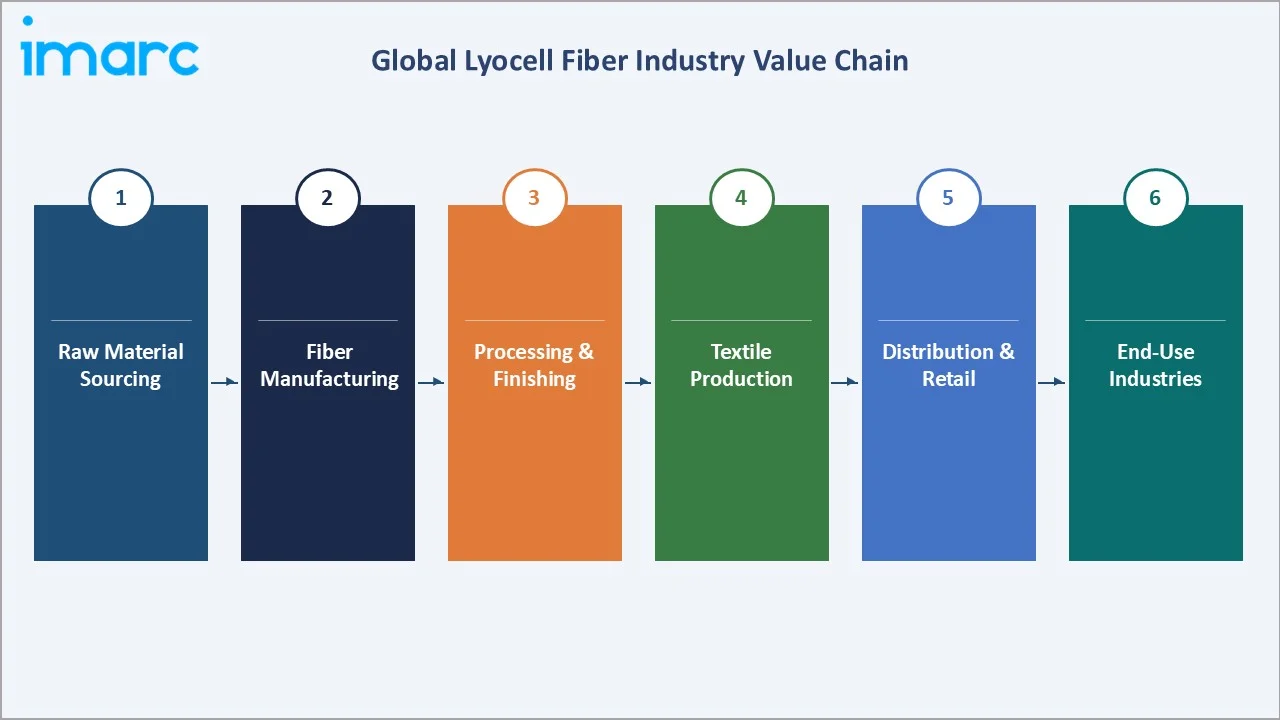

Industry Value Chain Analysis

The lyocell fiber industry value chain spans six integrated stages from sustainable wood pulp sourcing through end-consumer product delivery. Each stage presents distinct competitive dynamics, margin profiles, and sustainability investment requirements that collectively define the market's structural positioning.

|

Stage |

Key Activities / Players |

|

Raw Material Sourcing |

FSC/PEFC-certified wood pulp procurement from Austria, Sweden, Brazil, and South Africa; sustainable forestry management |

|

Fiber Manufacturing |

NMMO solvent dissolution, closed-loop spinning, and solvent recovery; Lenzing AG, Aditya Birla (Birla Cellulose), Sateri, AceGreen, Baoding Swan |

|

Processing & Finishing |

Cutting into staple or filament forms; surface treatment, dyeing, and bleaching by certified textile processors in China, India, and Austria |

|

Textile Production |

Spinning, weaving, knitting, and nonwoven production by mills across the Asia Pacific, Turkey, and Eastern Europe |

|

Distribution & Retail |

B2B fiber and fabric distribution; retail distribution through sustainability-certified fashion retailers and e-commerce platforms globally |

|

End-Use Industries |

Apparel (48.0%), Home Textiles (22.6%), Medical & Hygiene (14.3%), Automotive Filters (8.4%), Others (6.7%) |

Fiber manufacturers occupy the highest strategic value position in the lyocell value chain, combining proprietary closed-loop technology, sustainability certifications, and branded fiber positioning (TENCEL, Birla Cellulose, Ecocosy) that command premium pricing throughout the downstream supply chain. However, this position is increasingly being challenged as vertically integrated textile mills invest in in-house lyocell production capabilities.

Technology Landscape in the Lyocell Fiber Industry

Closed-Loop Solvent Technology (NMMO Process)

The NMMO closed-loop system underpins lyocell production, enabling over 99% solvent recovery and repeated reuse with minimal chemical waste, while ongoing improvements are enhancing energy efficiency and lowering costs. In 2024, Lenzing Group introduced stretch lyocell technology, enabling fossil-free elasticity and expanding the fiber’s application scope.

Cross-Linking and Fiber Modification Technologies

Chemical cross-linking of lyocell filaments reduces fibrillation tendency and improves dimensional stability, enabling penetration into automotive filter media, technical nonwovens, and specialty composites.

Biocomposite and Carbon Fiber Precursor Development

Lyocell-derived carbon fiber precursors are under active development for lightweight automotive and aerospace components, with prototype testing demonstrating up to 20% weight reduction versus conventional carbon fiber inputs. These high-value applications could materially offset Lyocell's higher production costs and improve industry-wide profitability, representing the technology frontier most likely to transform the market's growth trajectory toward 2034.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Staple Fiber |

78% |

2025 |

|

Application |

Apparel |

48% |

2025 |

|

Region |

Asia-Pacific |

44% |

2025 |

By Product

Staple Fiber commands a 78.0% majority share in 2025, reflecting its role as the commercially versatile workhorse of the lyocell market. Staple fiber is produced by cutting continuous filament tow into short discrete lengths (typically 38-60 mm) compatible with conventional cotton and wool spinning systems without significant equipment modification – dramatically lowering adoption barriers. Global staple lyocell production capacity exceeded 400,000 metric tons annually by 2025.

To access detailed market analysis, Request Sample

Cross-Linked Fiber at 22.0% in 2025 is the fastest-growing product segment, driven by its enhanced durability and dimensional stability, making it ideal for nonwoven applications in medical products, automotive filter media, and technical textiles. Cross-linked lyocell's improved resistance to fibrillation – a historical weakness of standard lyocell in high-abrasion applications – has unlocked new end-use categories that standard grades cannot serve.

By Application

Apparel represents the largest application at 48.0% in 2025, driven by Lyocell's outstanding combination of comfort, aesthetics, and sustainability credentials. Its hypoallergenic properties make it ideal for intimate wear and sensitive-skin garments, while its high tensile strength ensures durability. The sustainable denim category has become a notable growth vector, with lyocell-denim blends using significantly less water than conventional cotton denim processing.

Home Textiles at 22.6% is the second-largest application, with lyocell used in bedsheets, towels, curtains, and upholstery due to its luxurious softness and biodegradable properties. The Medical and Hygiene segment (14.3%) is projected to grow the fastest at approximately 9.2% CAGR through 2034. Automotive Filters (8.4%) benefits from cross-linked lyocell's controlled porosity and thermal stability. Others (6.7%) encompass technical composites and industrial wipes.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

44.0% |

China textile scale; India Birla Cellulose expansion; Vietnam/Bangladesh export adoption; urban disposable income growing ~6.5% p.a. |

|

Europe |

22.4% |

Lenzing AG, Austria production base; EU Circular Textiles Strategy (2030); strong premium sustainable fashion demand |

|

North America |

20.6% |

27% U.S. eco-committed consumers; New York Fashion Sustainability Act; growing activewear and sustainable denim demand |

|

Middle East & Africa |

7.8% |

Expanding Turkish and Egyptian textile manufacturing, GCC premium apparel imports, and youth-driven sustainability awareness. |

|

Latin America |

5.2% |

Brazil/Colombia denim and activewear manufacturing; Brazil Fashion Forward sustainability initiative; export compliance requirements |

Asia Pacific commands a 44.0% global revenue share in 2025, the most dominant regional position in the global lyocell fiber market. China is the single most important national market within Asia Pacific, combining the world's largest textile production volume with rapidly tightening domestic environmental regulations requiring the textile industry to reduce water consumption and carbon emissions. China’s urban disposable income has been growing at mid-single-digit rates (around 4–6% annually in recent years), supporting a gradual shift toward premium and sustainable textile consumption, which benefits fibers such as lyocell.

Europe, with 22.4% in 2025, is anchored by Austria, home to Lenzing AG's industry-defining TENCEL Lyocell production. North America, at 20.6%, is driven by the U.S. market, where the New York Fashion Sustainability and Social Accountability Act requires brands with revenues exceeding USD 100 million to disclose environmental impacts. Middle East and Africa (7.8%) and Latin America (5.2%) represent emerging growth markets, driven by expanding manufacturing capacity and compliance with international sustainable sourcing standards.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Lenzing AG |

TENCEL Lyocell |

Leader |

Certified sustainability; 100K+ MT/year capacity; CDP double-A rating |

|

Aditya Birla Mgmt. Corp. |

Birla Cellulose |

Leader |

Large-scale Asia production; performance fiber innovation (Feb 2025) |

|

Sateri |

EcoCosy® |

Leader |

China market dominance; viscose-to-lyocell capacity transition |

|

AceGreen Eco-Material |

AceGreen Lyocell |

Challenger |

Eco-material specialization; expanding regional presence |

|

Baoding Swan Fiber Co. |

Swan Lyocell |

Challenger |

Cost-competitive Chinese production; growing export penetration |

|

Smart Fiber AG |

SeaCell Lyocell |

Niche Player |

Seaweed-enriched functional fiber innovation (Oct 2024) |

|

Jinan Hengtian Hi-Tech |

Hengtian Lyocell |

Emerging |

Growing domestic Chinese industrial/technical fiber capacity |

|

KO-SI d.o.o. |

KO-SI Fiber |

Niche Player |

European specialty producer; sustainable textile brand partnerships |

The global lyocell fiber market exhibits moderate-to-high concentration, with leading producers such as Lenzing AG, Aditya Birla Group, and Sateri collectively accounting for a dominant share of global capacity. Competitive differentiation is driven by sustainability certifications, proprietary closed-loop production technologies, and strong fiber branding. Increasingly, competition is shifting toward innovation, with manufacturers developing advanced variants such as cross-linked, stretch, and specialty functional fibers to capture premium segments.

Key Company Profiles

Lenzing AG

Lenzing AG is the global leader in sustainable man-made cellulose fibers, headquartered in Lenzing, Austria, with over 80 years of manufacturing expertise. As the inventor and largest producer of TENCEL Lyocell, Lenzing defines the industry's sustainability benchmark, operating one of the most advanced closed-loop fiber manufacturing systems in the world.

- Product & Platform Portfolio: TENCEL Lyocell staple and filament fibers for apparel, home textiles, and hygiene applications; carbon-neutral certified grades; LENZING Lyocell Dry hydrophobic variant for hygiene; stretch Lyocell for elastic garment applications.

- Recent Developments: In January 2024, Lenzing Group introduced a stretch lyocell process enabling fossil-free elastic fabrics as a sustainable alternative to synthetics. The company also achieved CDP double-A ratings for climate and forest stewardship, with 99% certified wood sourcing.

- Strategic Focus: Lenzing's strategy centers on sustainability leadership (maintaining PEFC/FSC certification leadership and net-zero commitment), production capacity expansion, brand partnership programs with luxury and mainstream fashion brands, and innovation in specialty lyocell variants that command premium pricing versus commodity cellulose fibers.

Aditya Birla Management Corporation Pvt. Ltd.

Aditya Birla's Birla Cellulose division is one of the world's largest producers of man-made cellulose fibers, operating multiple manufacturing sites across India, Southeast Asia, and Canada. Birla Cellulose has emerged as a major innovation leader in lyocell fiber, particularly for performance and technical textile applications.

- Product & Platform Portfolio: Birla Cellulose™ lyocell for apparel, sportswear, and home textiles; Nullarbor ultra-fine lyocell fiber (finer than silk); expanded range for technical and outdoor applications leveraging proprietary fiber strength and moisture management innovations.

- Recent Developments: In March 2026, Birla Cellulose announced the launch of its new sustainable fibre, Livaeco Lyocell, at its flagship event Confluence 2026, held in Coimbatore.

- Strategic Focus: Birla Cellulose's strategy prioritizes Asia Pacific capacity expansion to serve both domestic Indian demand and global export markets, penetration of the performance sportswear and outdoor segment, and R&D investment in next-generation lyocell variants. The company's Pulp and Fiber Innovation Center drives continuous product development aimed at differentiating from commodity lyocell production.

Sateri

Sateri is a leading producer of viscose and lyocell fibers in China, operating as part of the Royal Golden Eagle (RGE) Group. With significant Chinese domestic market presence and growing export capabilities, Sateri is a key driver of Lyocell's commercial scale expansion in the Asia Pacific.

- Product & Platform Portfolio: EcoCosy lyocell fibers for fashion and home textile markets; standard and specialty viscose grades; sustainable fiber solutions targeting domestic Chinese and international brand markets with verified environmental credentials.

- Recent Developments: In July 2022, Sateri launched three zero-carbon fibre products: EcoCosy, Lyocell, and FINEX. All three products have obtained the PAS2060 assessment certification for carbon neutrality and have been launched in their respective markets.

- Strategic Focus: Sateri's strategy focuses on domestic Chinese market consolidation, where ESG-driven fiber procurement is accelerating; export growth to EU and North American brand customers seeking verified sustainable sourcing; and managing the industry transition from conventional viscose toward lyocell as the regulatory and consumer landscape tightens.

Market Concentration Analysis

The global lyocell fiber market is moderately to highly concentrated, with leading players such as Lenzing AG, Aditya Birla Group (Birla Cellulose), and Sateri collectively holding a dominant share of capacity. High capital intensity, complex closed-loop NMMO technology, stringent sustainability certifications, and strong fiber branding (e.g., TENCEL) reinforce entry barriers.

At the same time, the market is bifurcating: while global leaders consolidate the premium segment, emerging Chinese producers such as AceGreen, Baoding Swan, and Jinan Hengtian are scaling cost-competitive capacity to serve domestic demand, intensifying competition in the world’s largest textile market.

Investment & Growth Opportunities

Fastest-Growing Segments

Medical and hygiene nonwovens represent the highest-growth application at approximately 9.2% CAGR through 2034. Biodegradable lyocell substrates for wound care, feminine hygiene, and baby care are benefiting from plastic ban legislation and hospital procurement mandates. Cross-linked lyocell for automotive filter media is the fastest-growing product innovation within the technical textile category, driven by tightening vehicle interior air quality standards and EV platform adoption.

Emerging Market Expansion

Asia Pacific—particularly India, Vietnam, and Bangladesh—offers cost-efficient manufacturing for scaling lyocell to meet Western sustainability-driven sourcing demand, supported by favourable policies such as India’s textile incentives. At the same time, functional innovations in stretch, antimicrobial, and bioactive lyocell present the strongest near-term premium and margin opportunities for producers.

Venture and Strategic Investment Trends

Key investment themes include Asia Pacific capacity expansion, advanced solvent recovery to enhance cost efficiency, and fiber modification R&D for technical applications. Emerging lyocell-based carbon fiber precursors present a high-potential frontier, offering early-mover advantages in advanced composites.

Future Market Outlook (2026-2034)

The global lyocell fiber market forecast projects steady value expansion from USD 1.2 Billion in 2025 to USD 2.3 Billion by 2034 at a CAGR of 5.2%, underpinned by regulatory compliance demand, sustainable fashion growth, expanding medical and technical applications, and continued premiumization of home textiles. Three structural forces are most likely to reshape the market through 2034.

Regulatory convergence—driven by EU circular textile targets, expanding plastic bans, and stricter Asian standards—is set to make lyocell a compliance-driven material across major markets, acting as a key demand catalyst.

By 2034, the market is expected to evolve into a three-tier structure: premium global producers such as Lenzing AG and Birla Cellulose, cost-competitive Asian manufacturers serving mass demand, and niche innovators like Smartfiber AG targeting high-value applications..

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with lyocell fiber industry stakeholders, including production directors at fiber manufacturers, textile mill procurement managers, sustainability officers at fashion brands, nonwoven product developers in the medical sector, and trade association representatives across Asia Pacific, Europe, and North America. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include company annual reports (Lenzing AG Annual Report 2024, Aditya Birla Group sustainability reports), EU regulatory publications (EU Strategy for Sustainable and Circular Textiles), International Textile Manufacturers Federation production data, EDANA nonwovens industry statistics, North America Lyocell Fiber market data from IMARC Group, trade publications including Textile World, Fiber2Fashion, and Specialty Fabrics Review, and verified press releases from key market participants.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating textile production growth rates, sustainable fiber adoption curves, regulatory implementation timelines, and historical lyocell market evolution patterns anchored to exact values: USD 1.1 Billion (2020), USD 1.2 Billion (2025), USD 1.9 Billion (2030), and USD 2.3 Billion (2034). Scenario analysis (base, optimistic, and conservative cases) was performed to account for regulatory timeline uncertainty.

Lyocell Fiber Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Staple Fiber, Cross Linked Fiber |

| Applications Covered | Apparel, Home Textiles, Medical and Hygiene, Automotive Filters, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Lenzing AG, Aditya Birla Mgmt. Corp., Sateri, AceGreen Eco-Material, Baoding Swan Fiber Co., Smart Fiber AG, Jinan Hengtian Hi-Tech, KO-SI d.o.o., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the lyocell fiber market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global lyocell fiber market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the lyocell fiber industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Lyocell Fiber Market Report

The global lyocell fiber market was valued at USD 1.2 Billion in 2025, with Asia Pacific accounting for the largest regional share at 44.0% of global revenue.

The market is projected to reach USD 2.3 Billion by 2034, growing at a CAGR of 5.2% during 2026-2034, driven by sustainability mandates, healthcare demand, and expanding technical applications.

Key drivers include EU Circular Textiles mandates, rising eco-consumer demand, healthcare nonwoven adoption, closed-loop manufacturing advantages, and expanding performance apparel applications.

Asia Pacific leads with 44.0% market share in 2025, supported by China's textile scale, India's Birla Cellulose expansion, and Vietnam/Bangladesh export-driven lyocell adoption.

Staple fiber leads at 78.0% in 2025 due to compatibility with conventional spinning systems and broad applicability across apparel, home textiles, and industrial uses.

Medical and Hygiene is the fastest growing at approximately 9.2% CAGR, driven by plastic bans and hospital procurement mandates for biodegradable nonwoven disposables.

Key companies include Lenzing AG, Aditya Birla Mgmt. Corp., Sateri, AceGreen Eco-Material, Baoding Swan Fiber Co., Smart Fiber AG, Jinan Hengtian Hi-Tech, and KO-SI d.o.o.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)