Low Carbon Flooring Market Size, Share, Trends and Forecast by Material Type, Design Type, Type, End-Use Industry, and Region, 2025-2033

Low Carbon Flooring Market Size and Share:

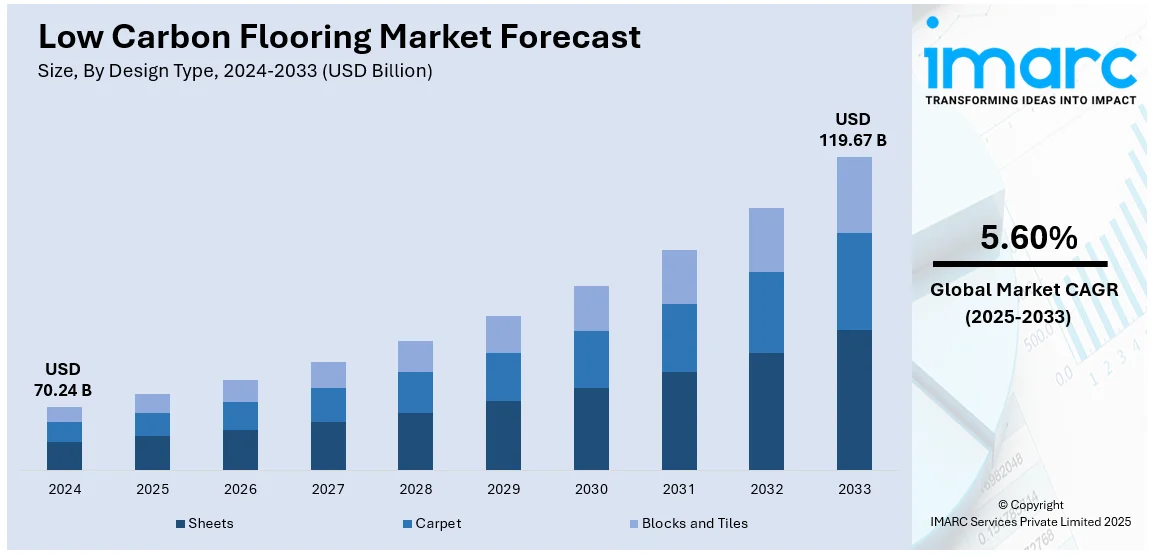

The global low carbon flooring market size was valued at USD 70.24 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 119.67 Billion by 2033, exhibiting a CAGR of 5.60% from 2025-2033. North America currently dominates the market, holding a market share of over 43.7% in 2024. The increasing environmental awareness, rising demand for energy-efficient and sustainable building materials, rapid technological advancements in eco-friendly flooring options, imposition of government regulations, and rising consumer preferences for healthier indoor environments, are major factors bolstering the low carbon flooring market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 70.24 Billion |

| Market Forecast in 2033 | USD 119.67 Billion |

| Market Growth Rate (2025-2033) | 5.60% |

One of the major factors driving the low carbon flooring market growth is the increasing awareness about environmental sustainability. Nowadays, people are increasingly aware of how their decisions affect the environment. This growing consciousness has resulted in a rise in the demand for environmentally friendly products in various industries. As per an industry survey, more than half of individuals in the United States showcased an increased demand for green homes in 2024. Traditional flooring options, such as vinyl and certain types of carpets, often use harmful chemicals in production, require significant resources to make, and do not have easy recycling options. Low carbon flooring, on the other hand, is made from renewable, recycled, or naturally sourced materials, which helps reduce its overall carbon footprint. As consumers look for ways to live more sustainably, they are turning to low carbon flooring to reduce their homes’ or businesses’ environmental impact.

The United States plays a key role in disrupting the market, holding 76.50% of the market share in North America. This is because energy efficiency is becoming a central focus in modern building design, and this directly affects the demand for low carbon flooring in the country. Buildings are increasingly being designed to meet stringent energy standards, with a focus on minimizing heating, cooling, and lighting energy needs. According to a recent survey, 96% of home builders and remodelers admit that they are actively improving home-building performance by using energy, water and materials resource efficiency, healthier and cleaner indoor living environments, resiliency, and by providing operation and maintenance manuals for green features. Flooring is crucial in this aspect, as selecting low-carbon options can enhance a building's overall energy efficiency. Sustainable materials such as cork and natural wood, for instance, offer thermal insulation, which reduces the reliance on heating and cooling systems. These materials contain air pockets within their structure, helping to regulate temperature naturally.

Low Carbon Flooring Market Trends:

Technological Advancements in Sustainable Flooring Materials

Another key factor driving the low carbon flooring market share is the continuous advancement in materials and technologies that make sustainable flooring more accessible and affordable. In recent years, there have been significant breakthroughs in the manufacturing of low carbon materials that maintain high performance, aesthetic appeal, and durability. For example, improvements in recycled materials like recycled rubber, glass, and plastic have made it easier to create high-quality, low-carbon flooring options without compromising on the strength or look of the product. Manufacturers are now using innovative techniques to create flooring that can be easily recycled or reused at the end of its life, making it a more sustainable option. For instance, many manufacturers are using cork which is a 100% natural material for green flooring. It is created from recyclable materials sourced from the production of wine cork stoppers. The waste generated during the manufacturing of cork stoppers is repurposed to create these attractive flooring tiles. These innovations have made it easier for manufacturers to provide high-quality, low-carbon flooring options at a more competitive price point, making it an attractive choice for both commercial and residential spaces.

Government Policies and Regulations on Carbon Emissions

Governments worldwide are placing increasing pressure on industries to reduce their carbon emissions. Many countries have introduced strict regulations and policies to combat climate change, and the building industry is one of the most significant contributors to carbon emissions due to the production and disposal of building materials, including flooring. As a result, building and construction companies are seeking ways to comply with environmental regulations while also meeting the growing demand for sustainable, low-carbon products. For example, in 2023, the European Union (EU) set stricter guidelines for carbon emissions in the construction sector, aiming to cut down the sector’s emissions by 60% by 2030. As part of this initiative, the European Commission encouraged the use of low-carbon materials in building construction, including flooring. Similarly, the U.S. government has provided financial incentives for the adoption of energy-efficient materials, with the Inflation Reduction Act of 2023 offering up to $500 million in rebates for building projects using sustainable materials. This has directly increased the low carbon flooring market demand, as builders and developers seek to comply with these new policies.

Rising Consumer Demand for Healthier Indoor Environments

As people become more health-conscious, the demand for products that promote healthier indoor environments is growing. Flooring is an essential aspect of this, as many traditional flooring materials, such as certain types of vinyl or synthetic carpets, can emit volatile organic compounds (VOCs) and other harmful chemicals into the air, negatively affecting indoor air quality. In 2024, the World Health Organization (WHO) reported that exposure to indoor air pollutants leads to 3.8 million premature deaths annually. Low carbon flooring options, such as natural wood, cork, or linoleum, do not contain harmful chemicals and are much safer for indoor environments. These materials are made without the use of toxic adhesives or finishes, ensuring that the air inside homes and offices remains fresh and healthy. In addition, low-carbon flooring is often more resistant to mold and mildew, contributing to a healthier indoor environment.

Low Carbon Flooring Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global low carbon flooring market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on material type, design type, type, and end-use industry.

Analysis by Material Type:

- Linoleum

- Wood

- Cork

- Bamboo

- Stone

- Others

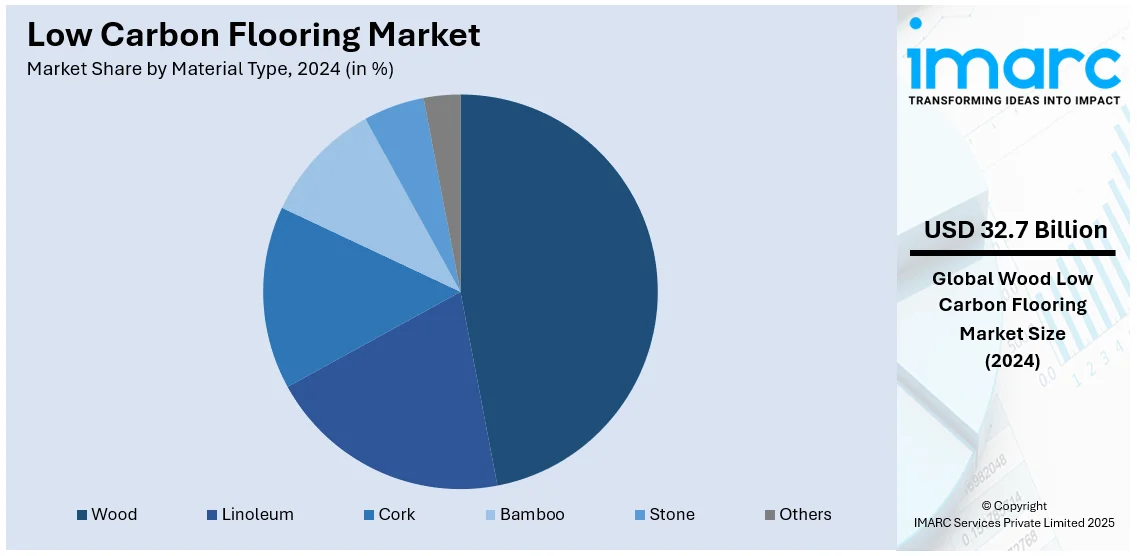

As per the low carbon flooring market forecast, wood leads the market share in 2024 with 46.5%, due to its widespread popularity, natural aesthetic appeal, and sustainable sourcing. Wood, especially bamboo, oak, and maple, is highly valued for its durability, timeless beauty, and ability to be recycled or repurposed at the end of its life cycle. The growing emphasis on eco-friendly building materials has boosted the adoption of sustainably sourced wood, such as certified products from organizations like the Forest Stewardship Council (FSC). Wood flooring provides excellent insulation, helping to enhance the energy efficiency of buildings. As consumers increasingly seek out materials that are both functional and environmentally responsible, wood flooring's combination of style, sustainability, and performance continues to make it the preferred choice, dominating the market for low carbon flooring.

Analysis by Design Type:

- Sheets

- Carpet

- Blocks and Tiles

Based on the low carbon flooring market trends, sheets make up the largest segment due to their versatility, simple installation, and affordability. Flooring sheets, such as vinyl, linoleum, and rubber, offer a seamless and uniform surface, making them popular for both residential and commercial spaces. Their ability to cover large areas quickly and with minimal waste appeals to builders and designers focused on efficiency and sustainability. Additionally, sheet flooring can be made from renewable or recycled materials, enhancing its appeal as an eco-friendly option. The durability of sheet flooring, along with its resistance to stains, scratches, and moisture, has made it the preferred choice in high-traffic areas like hospitals, schools, and offices. As consumers and businesses continue to prioritize low-carbon, durable, and low-maintenance flooring solutions, sheets maintain their dominant position in the market.

Analysis by Type:

- Virgin Products

- Recycled Solution

Virgin products dominate the low carbon flooring market, considering their quality, sustainability, and strong performance characteristics. These products are made from newly sourced materials and are not recycled or repurposed, thus offering pristine aesthetics and durability. While carrying a higher upfront cost, virgin products, like virgin wood or newly manufactured natural fibers, are often considered to be more dependable for specific uses because of their consistency and long-lasting properties. The increasing need for premium and environmentally friendly flooring options has propelled the demand for virgin products, especially those made from certified sustainable forests or renewable resources. With tightening environmental standards, manufacturers are now focusing more on producing virgin materials with less environmental impact. Thus, this has made it a very sought-after choice for consumers who want premium, low-carbon options for residential and commercial use.

Analysis by End-Use Industry:

- Residential

- Non-Residential

In 2024, the residential sector dominates the market, holding a 62.6% share, driven by rising consumer demand for sustainable, eco-friendly, and visually appealing home upgrades. Customers are increasingly looking for flooring solutions that reduce the environmental impact of a space, enhance indoor air quality, and comply with green living values. Of late, low carbon flooring such as bamboo, cork, and sustainable wood are highly in demand owing to their natural look, durability, and even regulating temperature and humidity. Moreover, many residential consumers seek materials that are non-toxic and free from harmful chemicals, which itself boosts the appeal of eco-friendly flooring. As awareness of environmental and health advantages of sustainable living increases, there is an ever-growing investment of homeowners in low-carbon flooring, and as a result, the residential sector is leading in the market.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East

- Africa

In 2024, the largest regional market for low carbon flooring was North America with 43.7%. This is due to strong demand among consumers for sustainable building materials and government initiatives to promote eco-friendly construction practices. Also, in the U.S. and Canada, significant growth is being witnessed in green building certifications, such as LEED, that encourages low-carbon flooring solutions both in the residential and commercial sectors. This region is equally pushed by the awareness toward environmental issues and a desire for a healthier indoor environment. Moreover, people now find it even easier to opt for low-carbon flooring options owing to advancements in green building codes coupled with incentives available for energy-efficient products. This has led North America at the forefront of market adoption, innovation, and regulatory support for sustainable flooring materials.

Key Regional Takeaways:

United States Low Carbon Flooring Market Analysis

United States dominated the market in North America with 76.50% in 2024. Currently, it is the biggest and most developed industry for low carbon flooring, driven by an increase in customer demand for green products, strict building codes, and government initiatives to curb carbon emissions. For example, the government intends to invest $3.4 billion into sustainable materials and technologies that will be used to transform federal facilities into high-performance green buildings. This growth is due to increasing awareness about the environmental effects of building materials and a great push toward energy-efficient construction practices, focusing much on flooring. The U.S. Green Building Council also reported that by 2024, over 100,000 buildings had achieved LEED certification, many of which incorporated sustainable flooring materials such as bamboo, linoleum, and recycled wood. Further support towards the adoption of low-carbon flooring is brought about by other government incentives that include rebates for sustainable and energy-efficient materials under the Inflation Reduction Act of 2023. As sustainability stays at the helm of U.S. homeowners, businesses, and government priorities, low-carbon flooring is expected to continue dominating the world market.

Asia Pacific Low Carbon Flooring Market Analysis

As per the low carbon flooring market outlook, Asia Pacific is a rapidly growing region, as demand for sustainable building materials is on the rise in countries such as China, Japan, and India. The region is experiencing rapid urbanization and infrastructure development, with an increasing push for eco-friendly products to support green building initiatives. The flooring sector reflects this growth. With environmental benefits and climate suitability for the region, bamboo, cork, and sustainable wood have emerged as the future low-carbon materials in this industry. For example, China has made huge investments in green building practices. As a step forward to carbon neutrality by 2060, this investment has driven low-carbon flooring solutions further into the industry. For instance, the country plans to expand its green building materials industry from RMB 1.3 trillion (US$180 billion) by 2025, with an annual growth rate of 3%. Even Japan's commitment toward sustainability through green building programs are also driving this demand. As consumer awareness regarding sustainability increases, Asia Pacific will continue to be a prime location for the low-carbon flooring market.

Europe Low Carbon Flooring Market Analysis

Europe is one of the leading regions in the low carbon flooring market, owing to its progressive regulations on sustainability and a high demand for eco-friendly building materials. The European Union has always been at the forefront of environmental initiatives and policies such as the European Green Deal that aim at making Europe the first climate-neutral continent by 2050. As reported by the European Commission in 2024, sustainable building materials represent an integral part of achieving these goals, and flooring solutions make no exception. Low-carbon flooring markets in the regions of Germany, France, and the UK continue to be important, driven primarily by demand from residential and commercial projects that follow stringent sustainability standards. Thus, Europe will remain a major market for the adoption of low-carbon flooring solutions as the awareness continues to build up and regulatory frameworks remain more stringent.

Latin America Low Carbon Flooring Market Analysis

Latin America's market is emerging as countries are showing high interest in sustainable building products to reach environmental and economic objectives. Though it is lagging behind other regions, both Brazil and Mexico are driven by government incentives and increasing environmental awareness to adopt low-carbon technologies. Fast urban development and an increasing demand in energy-efficient houses and commercial spaces have aggravated the demand. Currently, Brazil is concentrating on sustainable building materials in support of the Paris Climate Agreement, which is also boosting the use of low-carbon flooring. Adoption rates remain slow, keeping them behind North America and Europe. However, expansions in the Latin America market of sustainable flooring are expected with more businesses and consumers prioritizing eco-friendly options in constructing projects.

Middle East Low Carbon Flooring Market Analysis

Low carbon flooring market growth is experiencing a progressive development in the Middle East countries including the UAE, Saudi Arabia, and Qatar. The region invests a substantial amount in sustainable building practices as part of its broad vision for urban development and is also seeing increasing numbers of LEED-certified buildings under construction. Vision 2030 in Saudi Arabia and the United Arab Emirates' plans for committing billions of dollars to eco-friendly construction is also expanding the market. Consequently, various governments in the area are including green building standards in their national agenda for the use of low-carbon floorings in both commercial and residential projects. The rate of using low carbon flooring is still low compared to other regions because of increased material price and weather conditions. But with green building practices picking up in the luxury residential and commercial segments, the adoption of sustainable flooring materials in the Middle Eastern region will continue to grow.

Africa Low Carbon Flooring Market Analysis

The low carbon flooring market in Africa is experiencing growth due to increasing urbanization, stringent environmental regulations, and rising awareness of sustainable construction. Governments across the continent are implementing green building standards and energy-efficient regulations, driving demand for eco-friendly flooring solutions. Additionally, Africa’s growing real estate and commercial infrastructure sectors are incorporating sustainable materials to meet international environmental certifications, such as LEED. For instance, Nydree Flooring has launched its Zero Collection, an acrylic-infused hardwood flooring line featuring third-party verified Environmental Product Declaration (EPD) and Life Cycle Assessment (LCA) from SCS Global Services. The affordability and durability of low-carbon flooring, including bamboo, recycled wood, and bio-based composites, are appealing to both residential and commercial consumers. Furthermore, Africa’s abundant availability of raw materials, such as agricultural waste and recycled plastics, supports local production, reducing dependency on high-emission imports.

Competitive Landscape:

Major players in the market are prioritizing innovation, sustainability, and expanding their product offerings in response to the growing demand for eco-friendly solutions. Major companies are investing in new low-carbon products with sustainable materials such as bamboo, cork, recycled content, and natural fibers. Some companies are applying circular economy principles in the design of the products along a longer life cycle and recyclability for waste reduction. They are actively pursuing certifications such as LEED, Cradle to Cradle, and FloorScore to prove their commitment towards sustainability and adherence to the environmental standards set by governments and organizations across the world. Furthermore, partnerships and collaborations with environmental organizations and green building councils are now becoming more common in order to keep up with changing regulations and bring about industry-wide change. These initiatives go hand in hand with the advancements in the manufacturing process and optimizing the supply chains, allowing companies to lower their production costs, improve sustainability in their product, and strengthen their position in the growing low-carbon flooring market.

The report provides a comprehensive analysis of the competitive landscape in the low carbon flooring market with detailed profiles of all major companies, including:

- Forbo Group

- Gerflor

- Interface, Inc.

- Kingspan Group

- Milliken & Company

- Mohawk Industries, Inc.

- Shaw Industries Group, Inc. (Berkshire Hathaway, Inc.)

- Tarkett

- Teragren

Latest News and Developments:

- In November 2024, Gerflor declared the release of Taraflex which is used for indoor sports flooring. It is an eco-designed flooring solution that reduces carbon emissions without compromising on technical performance of sportspersons.

- In October 2024, Forbo Flooring Systems and Universal Fibers have formed a partnership in which Universal Fibers introduced Forbo Flooring Systems' new Tessera Topology collection, the first in their Evolve+ series, featuring Thrive Matter yarn. Thrive Matter is a yarn with the lowest carbon footprint, made from 100% solution-dyed nylon 6 and containing 90% recycled content.

Low Carbon Flooring Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | USD Billion |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Material Types Covered | Linoleum, Wood, Cork, Bamboo, Stone, Others |

| Design Types Covered | Sheets, Carpet, Blocks and Tiles |

| Types Covered | Virgin Products, Recycled Solution |

| End-Use Industries Covered | Residential, Non-Residential |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East, Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Forbo Group, Gerflor, Interface, Inc., Kingspan Group, Milliken & Company, Mohawk Industries, Inc., Shaw Industries Group, Inc. (Berkshire Hathaway, Inc.), Tarkett, Teragren, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the low carbon flooring market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global low carbon flooring market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the low carbon flooring industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The low carbon flooring market was valued at USD 70.24 Billion in 2024.

IMARC Group estimates the market to reach USD 119.67 Billion by 2033, exhibiting a CAGR of 5.60% from 2025-2033.

Key factors driving the low carbon flooring market include increasing environmental awareness, growing demand for sustainable and energy-efficient building materials, government regulations promoting green building practices, technological advancements in eco-friendly flooring solutions, consumer preference for healthier indoor environments, and cost-effectiveness through long-term savings and durability.

North America currently dominates the market with a share of 43.7%, driven by strong consumer demand for sustainable building materials, imposition of government incentives, and widespread adoption of green building standards like LEED.

Some of the major players in the low carbon flooring market include Forbo Group, Gerflor, Interface, Inc., Kingspan Group, Milliken & Company, Mohawk Industries, Inc., Shaw Industries Group, Inc. (Berkshire Hathaway, Inc.), Tarkett, Teragren, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)