Logistics Robots Market Size, Share, Trends and Forecast by Component, Robot Type, Function, Operation Area, End Use Industry, and Region, 2026-2034

Global Logistics Robots Market Size, Share, Trends & Forecast (2026-2034)

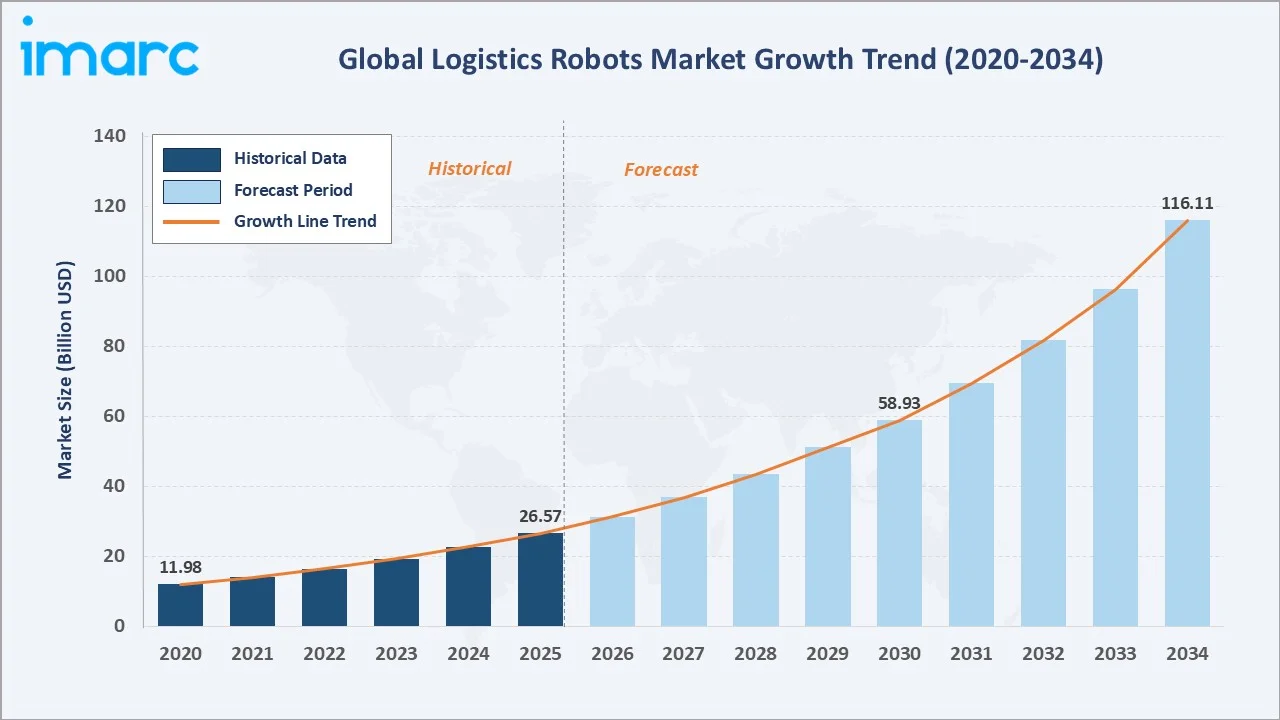

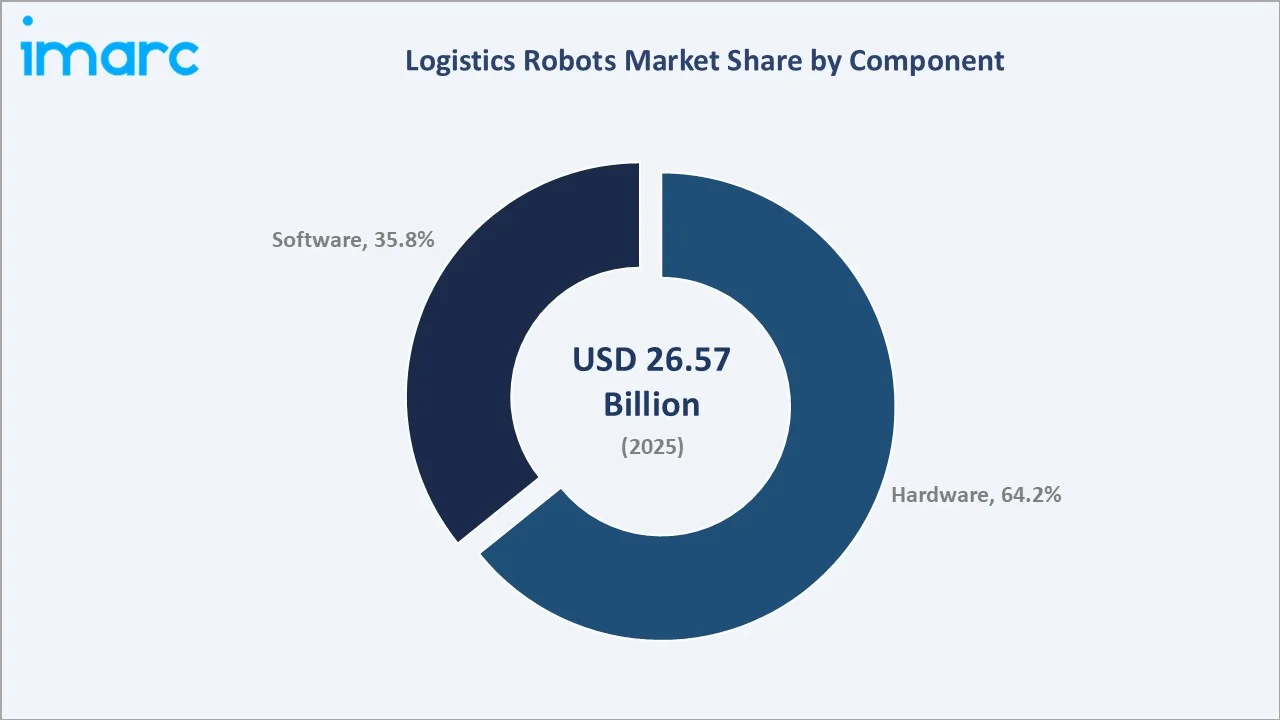

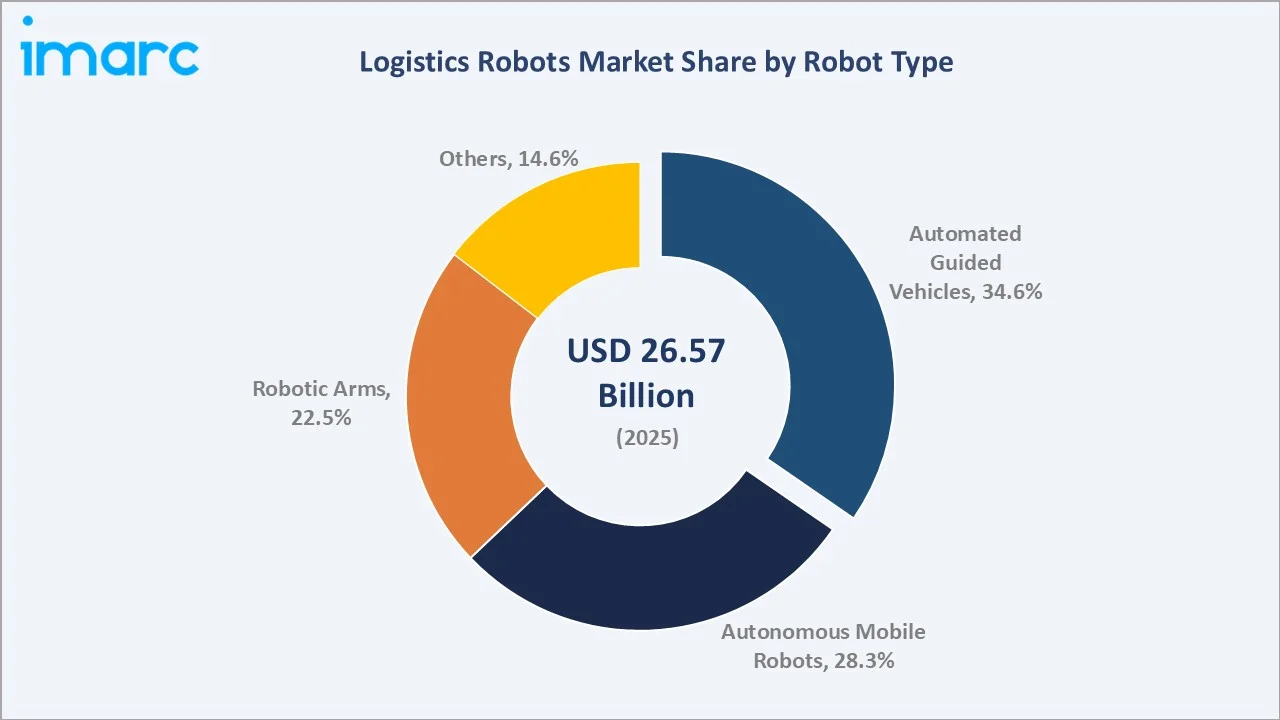

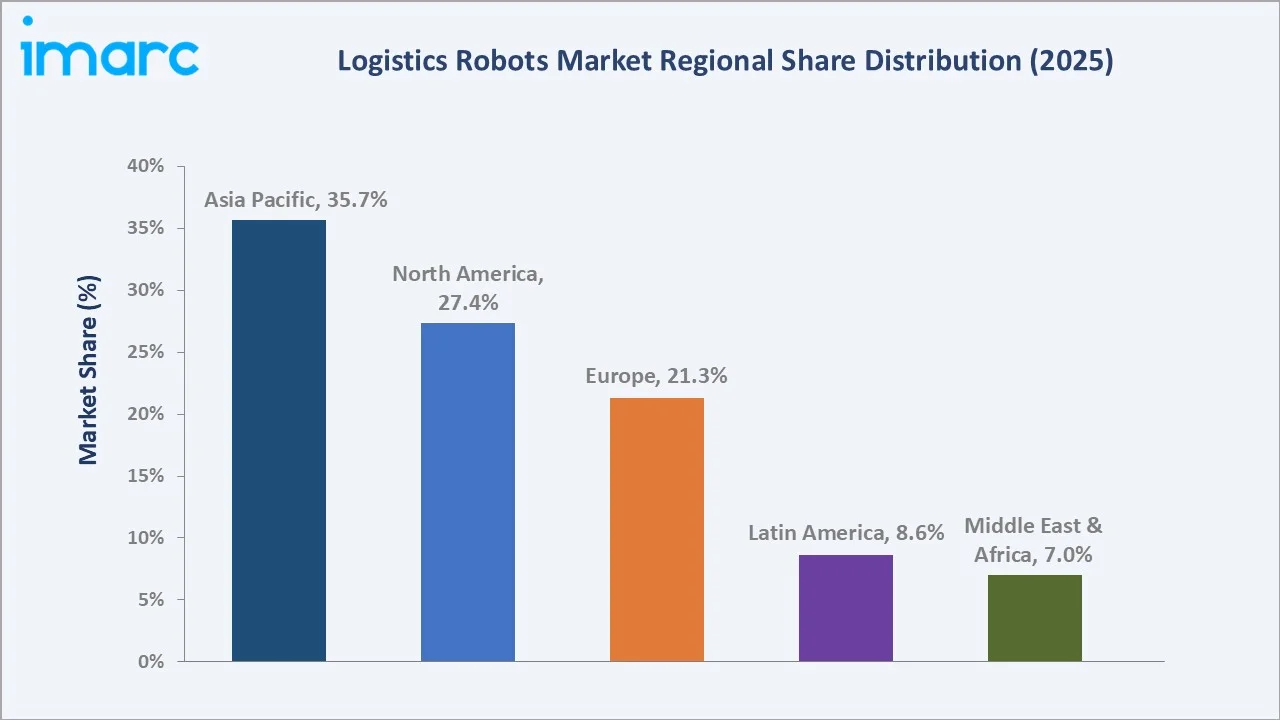

The global logistics robots market size was valued at USD 26.57 Billion in 2025 and is projected to reach USD 116.11 Billion by 2034, exhibiting a CAGR of 17.27% during 2026-2034. Rapid e-commerce expansion, rising warehouse automation investments, labour shortages across developed markets, and advancements in AI-driven navigation are collectively propelling the logistics robots market growth. Hardware leads with a 64.2% share in 2025, while Automated Guided Vehicles account for 34.6% of the global market. Asia Pacific dominates regional demand with a 35.7% share in 2025, supported by manufacturing scale in China and Japan.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 26.57 Billion |

|

Forecast Market Size (2034) |

USD 116.11 Billion |

|

CAGR (2026-2034) |

17.27% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (35.7% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Component |

Hardware (64.2%, 2025) |

|

Leading Robot Type |

Automated Guided Vehicles (34.6%, 2025) |

The chart below illustrates the logistics robots market growth trajectory from 2020 to 2034, reflecting robust expansion driven by e-commerce surges and warehouse automation mandates.

To get more information on this market, Request Sample

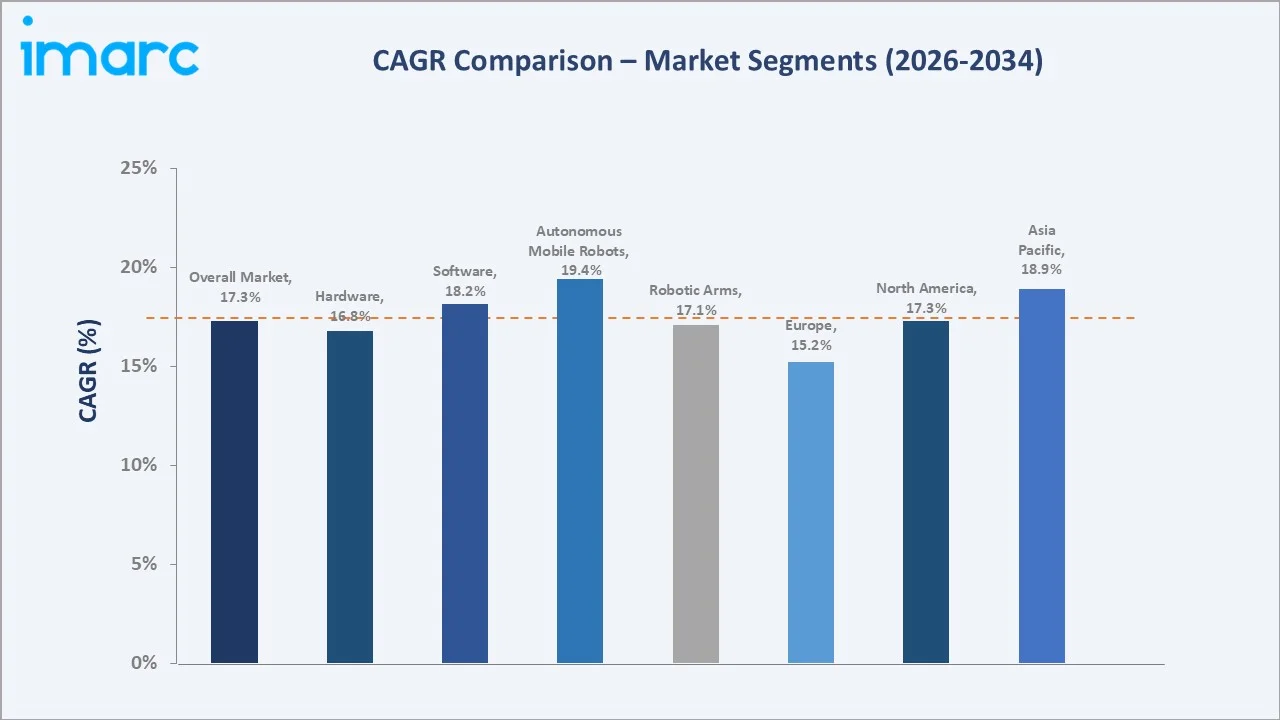

CAGR analysis highlights Autonomous Mobile Robots and Asia Pacific as the fastest-growing segments in the global logistics robots market through 2034.

Executive Summary

The global logistics robots’ market is undergoing rapid transformation driven by e-commerce expansion, persistent labour shortages, and accelerating warehouse automation. Valued at USD 26.57 Billion in 2025, the market is projected to reach USD 116.11 Billion by 2034, at a 17.27% CAGR. Rising operational complexity, same-day delivery expectations, and investments in smart factories are pushing operators across retail, automotive, healthcare, and food sectors toward robotic fulfilment systems.

Hardware leads the market with a 64.2% share in 2025, reflecting heavy demand for mobile bases, manipulator arms, and sensor suites. Automated Guided Vehicles capture 34.6% of global revenue, followed by Autonomous Mobile Robots at 28.3%, Robotic Arms at 22.5%, and Others at 14.6%. Key trends include AI-powered picking, humanoid robotics pilots, cloud fleet orchestration, and growing adoption of robotics-as-a-service (RaaS) financing models.

Asia Pacific leads the global logistics robots market with a 35.7% share in 2025, supported by large-scale warehouse buildouts in China, Japan, and South Korea. North America holds 27.4%, driven by e-commerce giants and third-party logistics automation. Europe accounts for 21.3%, followed by Latin America at 8.6% and Middle East and Africa at 7.0%. Asia Pacific is also the fastest-growing region through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Component Segment |

Hardware - 64.2% share (2025) |

|

Second Component Segment |

Software - 35.8% share (2025) |

|

Leading Robot Type |

Automated Guided Vehicles - 34.6% share (2025) |

|

Second Robot Type |

Autonomous Mobile Robots - 28.3% share (2025) |

|

Leading Region |

Asia Pacific - 35.7% revenue share (2025) |

|

Second Region |

North America - 27.4% revenue share (2025) |

|

Top Companies |

ABB, Fanuc Corporation, KUKA SE & Co. KGaA, Dematic, and Yaskawa America, Inc. |

Key Analytical Observations Supporting the Above Data:

- Hardware's 64.2% dominance in 2025 reflects heavy capital investment in robot chassis, actuators, grippers, LiDAR, and vision systems, which remain the largest cost component across AGV and AMR deployments.

- Software at 35.8% in 2025 is rising fast as operators adopt fleet management platforms, AI picking algorithms, and warehouse control systems, with cloud-native software-as-a-service (SaaS) models expanding recurring revenue streams.

- Automated Guided Vehicles holding 34.6% in 2025 reflects their maturity, lower unit cost, and predictable ROI in high-volume, fixed-route environments such as automotive plants and distribution hubs operating at scale.

- Autonomous Mobile Robots at 28.3% in 2025 represent the fastest-growing robot type, supported by dynamic navigation capabilities, short deployment cycles, and strong uptake across third-party logistics (3PL) and e-commerce fulfilment centres.

- Asia Pacific's 35.7% global dominance in 2025 is anchored by China's warehouse automation boom, Japan's deep robotics manufacturing base (Fanuc, Yaskawa), and government programs in South Korea and Singapore supporting smart logistics.

- Combined revenues of ABB, Fanuc, and KUKA exceeded USD 40 Billion in 2024, underscoring the scale advantages of incumbent industrial robotics leaders expanding into warehouse and last-mile logistics use cases.

Global Logistics Robots Market Overview

Logistics robots are automated machines that handle movement, picking, sorting, packaging, and delivery of goods across warehouses, factories, and outdoor environments. Core categories include Automated Guided Vehicles (AGVs), Autonomous Mobile Robots (AMRs), robotic arms, and delivery robots. The ecosystem spans component suppliers, OEMs, integrators, software providers, and end-user facilities across e-commerce, automotive, healthcare, and retail.

Applications span warehouse fulfilment, factory material handling, cold-chain logistics, last-mile delivery, airport baggage, and hospital supply. Growth is driven by e-commerce expansion, labour cost inflation, AI and sensor advances, and the shift toward same-day delivery. Macro factors including reshoring, supply chain resilience mandates, and Industry 4.0 investment further accelerate adoption.

Market Dynamics

To evaluate market opportunities, Request Sample

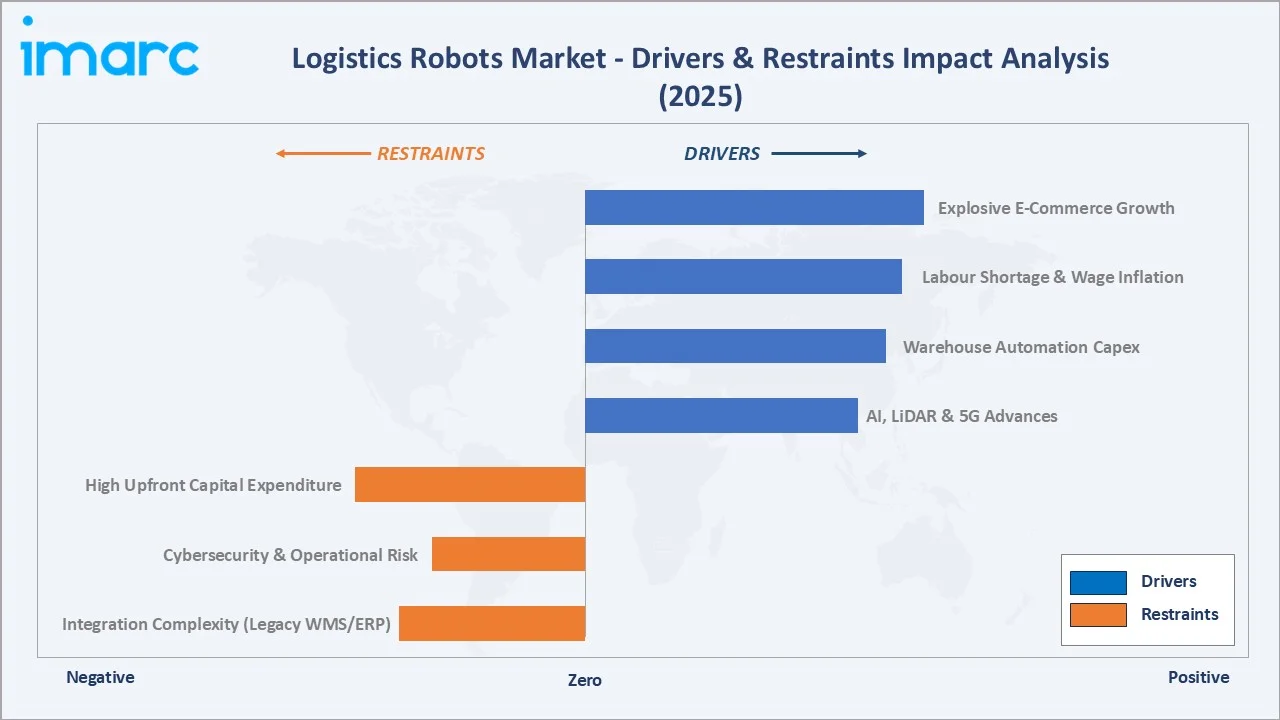

Market Drivers

- Explosive E-commerce Growth: Global e-commerce sales exceeded USD 6 trillion in 2024, as reported by eMarketer, increasing fulfilment complexity. This drives adoption of logistics robots to improve picking efficiency, scalability, and order accuracy in high-volume warehouse operations.

- Persistent Labour Shortages and Wage Inflation: Rising warehouse wages and persistent labor shortages in the U.S. and Europe, highlighted by U.S. Bureau of Labor Statistics and EU reports, are accelerating robotics adoption to reduce reliance on manual labor and improve operational continuity.

- Warehouse Automation Capital Expansion: Companies such as Amazon, Walmart, and JD.com are increasing investments in warehouse automation, though exact combined spending figures are not publicly disclosed, supporting rising demand for logistics robots.

- AI, LiDAR and 5G Advances: Advances in AI, LiDAR, and 5G technologies are enhancing robot navigation, real-time coordination, and deployment efficiency, reducing implementation complexity and enabling faster scaling of robotics solutions across warehouses and fulfilment centres.

Market Restraints

- High Upfront Capital Expenditure: High upfront costs for hardware, software, and integration, along with uncertain ROI timelines, limit adoption of logistics robots, particularly among small and mid-sized warehouse operators.

- Integration Complexity with Legacy WMS and ERP Systems: Older warehouse management platforms often lack standard APIs, requiring expensive middleware and extended commissioning cycles, which delay full-scale robot deployments across multi-site operators.

- Cybersecurity and Operational Risk: Connected robot fleets expand the enterprise attack surface, and a single ransomware incident can halt fulfilment operations, making IT-OT security investments a growing cost for adopters.

Market Opportunities

- Robotics-as-a-Service (RaaS) Models: RaaS adoption is expanding as subscription-based pricing reduces upfront investment barriers. Industry reports from International Federation of Robotics highlight growing interest in service-based robot deployment, enabling SMEs to adopt automation with lower financial risk and scalable usage models.

- Humanoid Robots in Warehouse Applications: Companies like Amazon and Agility Robotics are piloting humanoid robots for material handling tasks. Early trials indicate potential for flexible automation, though large-scale commercial deployment remains in early stages.

- Cold Chain and Pharmaceutical Logistics: Automation in pharmaceutical logistics is rising, with robots supporting temperature-sensitive handling and compliance with Good Distribution Practice (GDP) standards. Growth in pharma supply chains is creating niche opportunities for specialized robotics in controlled warehouse environments.

Market Challenges

- Interoperability Across Multi-Vendor Fleets: Most warehouses use robots from multiple OEMs, yet common standards like VDA 5050 are still maturing. This slows fleet coordination and elevates integration costs for enterprise buyers.

- Limited Skilled Workforce for Robotics Operations: Shortages of robotics technicians, maintenance engineers, and automation programmers delay rollouts in North America, Europe, and emerging markets, constraining deployment velocity for scaling operators.

- Regulatory Ambiguity Around Outdoor and Last-Mile Robots: Sidewalk delivery robots and drones face uneven permitting across US states and EU countries, slowing commercial rollouts despite strong operator interest and early pilot success stories.

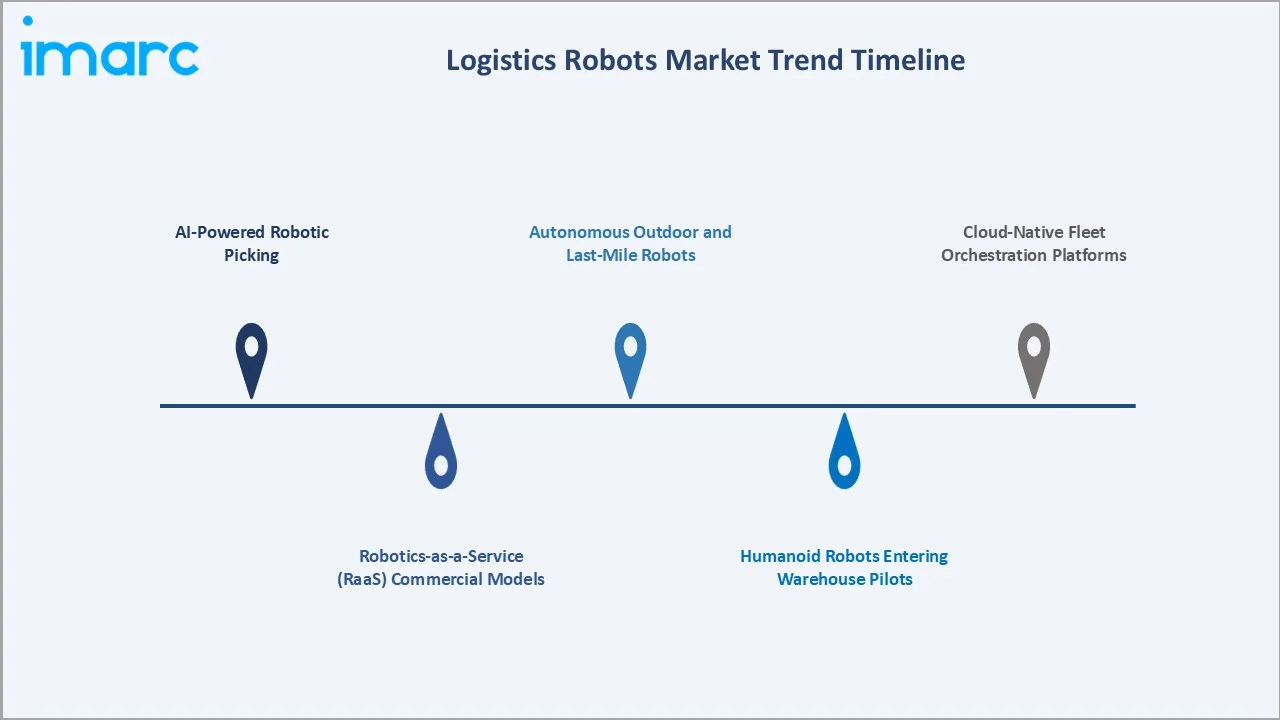

Emerging Market Trends

1. AI-Powered Robotic Picking

AI-enabled robotic picking using computer vision and deep learning is improving handling of diverse SKUs; however, widely cited 99% accuracy and 50% labor reduction vary by deployment and are not consistently validated across all warehouses.

2. Robotics-as-a-Service (RaaS) Commercial Models

Monthly subscription pricing, with no capital expenditure, is rapidly expanding access for mid-market warehouses. Locus Robotics and GreyOrange have reported strong RaaS revenue growth, broadening the addressable market significantly through 2030.

3. Humanoid Robots Entering Warehouse Pilots

Amazon began testing Agility Robotics' Digit in 2024. Figure AI raised USD 675 Million in 2024 to advance its humanoid platform, signalling that bipedal robots are nearing commercial viability in mixed-task logistics environments.

4. Autonomous Outdoor and Last-Mile Robots

Starship Technologies has completed over 6 million commercial deliveries globally by early 2024. Yard robots, autonomous trucks, and delivery drones are scaling, supported by improving sensors and decreasing per-mile operating costs.

5. Cloud-Native Fleet Orchestration Platforms

Cloud platforms are unifying AGV, AMR, and robotic arm fleets under a single control plane. This trend enables multi-vendor coordination, real-time optimisation, and analytics-driven performance improvements across distributed operations.

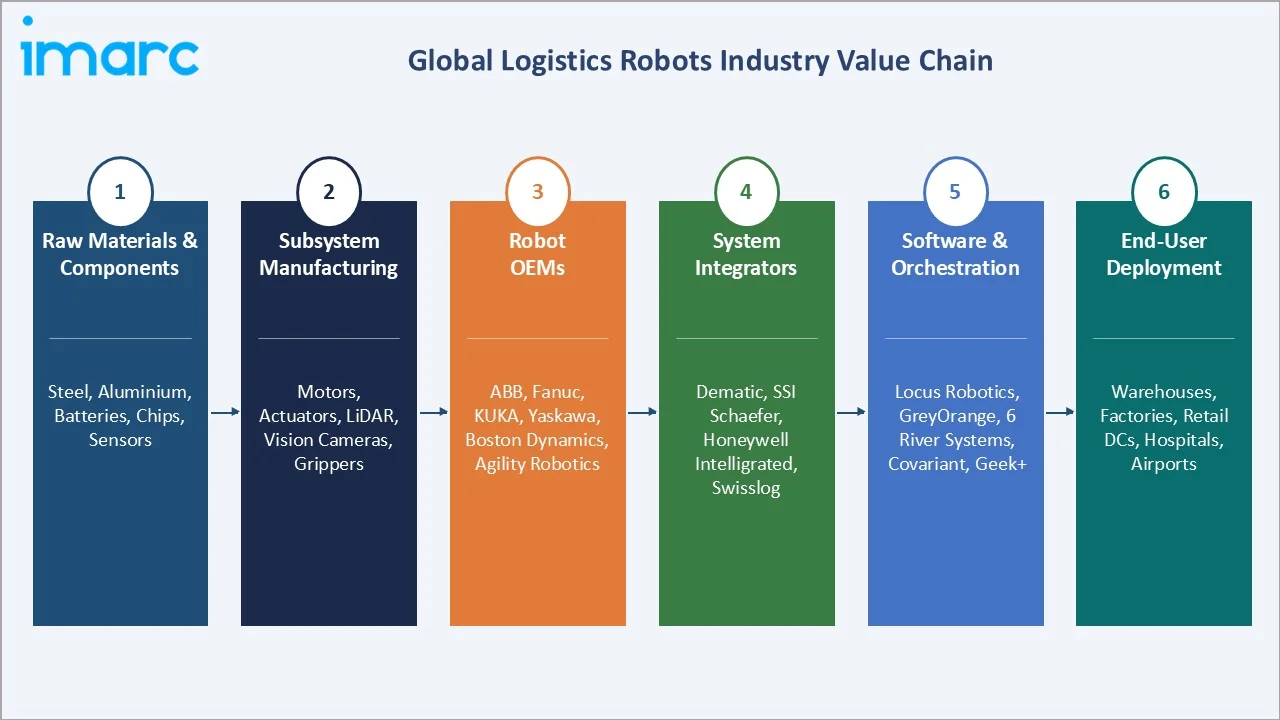

Industry Value Chain Analysis

The logistics robots value chain spans six interconnected stages, from raw semiconductor and metal inputs through OEM assembly, system integration, and end-user deployment across warehouses and factories.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Steel, aluminium, batteries, chips (Intel, NVIDIA, Qualcomm), sensors |

|

Subsystem Manufacturing |

Motors, actuators, LiDAR (Velodyne, Ouster), vision cameras, grippers |

|

Robot OEMs |

ABB, Fanuc, KUKA, Yaskawa, Boston Dynamics, Agility Robotics |

|

System Integrators |

Dematic (KION), SSI Schaefer, Honeywell Intelligrated, Swisslog |

|

Software & Orchestration |

Locus Robotics, GreyOrange, 6 River Systems, Covariant, Geek+ |

|

End-User Deployment |

Warehouses, factories, retail DCs, hospitals, airports |

Robot OEMs and system integrators capture the largest value share, as they combine hardware engineering with software capabilities and service contracts. Integrators increasingly bundle RaaS offerings, which is shifting value toward recurring revenue streams across the chain.

Technology Landscape in the Logistics Robots Industry

Battery and Power Technology

Lithium-ion battery adoption and fast-charging systems are extending robot uptime significantly. Advanced chemistries, including lithium-iron-phosphate (LFP), are improving safety and cycle life, enabling 20+ hour continuous operations across two-shift warehouse environments.

Sensors, LiDAR and Computer Vision

LiDAR costs have declined significantly over recent years, improving affordability. Combined with AI-enabled vision and depth sensing, these technologies enhance navigation and safety, enabling robots to operate reliably in dynamic, human-shared warehouse environments.

Smart Connectivity and 5G Fleet Coordination

Private 5G networks enable low-latency communication and real-time coordination of large robot fleets in warehouses. Deployments support scalable automation and dynamic routing, though fleet sizes and performance vary across operators and facility requirements.

AI, Machine Learning, and Autonomous Navigation

Advances in AI, including SLAM, reinforcement learning, and vision models, are improving robot autonomy. Platforms like NVIDIA Isaac and ROS 2 accelerate development and deployment of intelligent robotic systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Component | Hardware | 64.2% |

2025 |

| Robot Type | Automated Guided Vehicles | 34.6% |

2025 |

| Function | Pick and Place |

🔒 |

2025 |

| Operation Area | Factory Logistics Robots |

🔒 |

2025 |

| End Use Industry | E-Commerce |

🔒 |

2025 |

|

Region |

Asia Pacific | 35.7% |

2025 |

By Component

Hardware dominates the global logistics robots’ market with a 64.2% share in 2025, driven by high capital expenditure on chassis, motors, grippers, batteries, and sensor suites. Component inflation and supply constraints in semiconductors have sustained pricing power for core hardware providers across geographies.

To access detailed market analysis, Request Sample

Software holds 35.8% in 2025 and is growing faster than hardware, driven by fleet management platforms, AI-based picking systems, WMS integration middleware, and cloud-native orchestration software. Subscription and SaaS-based pricing models are steadily expanding recurring revenue pools.

By Robot Type

Automated Guided Vehicles lead with a 34.6% share in 2025, reflecting their maturity in predictable, high-volume environments such as automotive assembly plants. Fixed-path navigation, lower unit costs, and proven reliability continue to sustain AGV demand at enterprise scale.

Autonomous Mobile Robots hold 28.3% in 2025 and represent the fastest-growing segment, driven by dynamic navigation, short deployment timelines, and adoption in e-commerce fulfilment. Robotic Arms account for 22.5%, widely used in pick-and-place and palletizing. Others, including delivery and humanoid robots, capture 14.6% and are expanding rapidly as pilot deployments scale globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

35.7% |

China warehouse automation, Japan robotics OEMs (Fanuc, Yaskawa), South Korea smart factory push |

|

North America |

27.4% |

E-commerce giants (Amazon, Walmart), 3PL automation, tech labour shortages |

|

Europe |

21.3% |

Germany Industry 4.0, UK grocery automation (Ocado), Nordic sustainability mandates |

|

Latin America |

8.6% |

Brazil automotive automation, Mexico nearshoring-driven warehouse investment |

|

Middle East & Africa |

7.0% |

UAE logistics hubs, Saudi Vision 2030, port and oil & gas automation |

Asia Pacific commands a 35.7% global revenue share in 2025, anchored by China's mega-warehouse automation programs, Japan's dominance in industrial robotics manufacturing, and South Korea's government-backed smart factory initiatives. China alone added over 290,000 industrial robots in 2023, supporting broader logistics automation demand across Asia.

North America, at 27.4% in 2025, is driven by Amazon's fleet of over 750,000 robots, Walmart's automated distribution centres, and aggressive 3PL investment. Europe holds 21.3%, led by Germany's automotive automation and UK grocery robotics leadership. Latin America (8.6%) and Middle East & Africa (7.0%) are emerging markets where nearshoring, GCC mega-projects, and port automation programs are driving incremental growth through 2034.

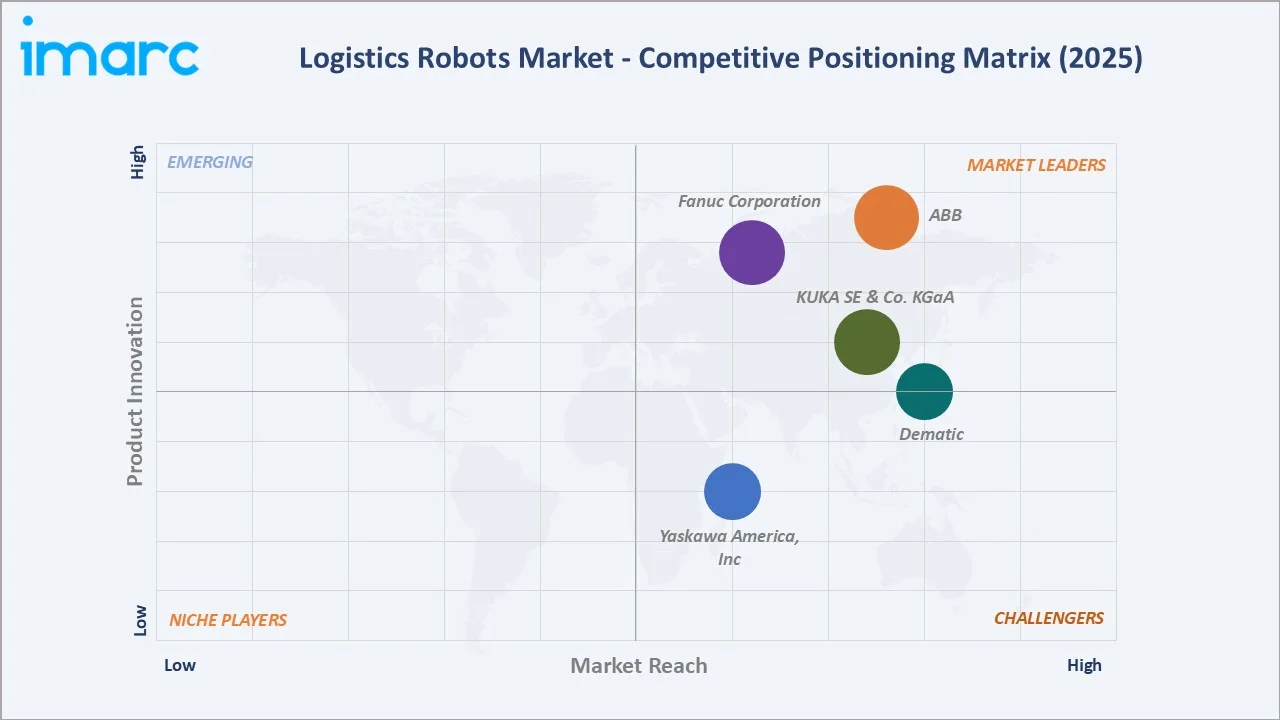

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

ABB |

ABB Robotics |

Leader |

Global scale, integrated automation, AI vision |

|

Fanuc Corporation |

FANUC |

Leader |

Industrial robot leader, Japan manufacturing base |

|

KUKA SE & Co. KGaA |

KUKA |

Leader |

Automotive automation, mobile platforms |

|

Dematic |

Dematic |

Leader |

Warehouse integration, goods-to-person systems |

|

Yaskawa America, Inc. |

Motoman |

Challenger |

Motion control, global service network |

The logistics robots’ market is led by a mix of industrial robotics giants and specialised warehouse automation firms. ABB reported USD 33.2 Billion in revenue in FY2025, while Fanuc generated approximately USD 5.3 Billion from its robotics segment, reflecting the deep resources incumbents bring to logistics automation expansion.

Key Company Profiles

ABB Ltd

ABB Ltd., headquartered in Zurich, is a global leader in electrification and automation, operating in over 100 countries. In FY2025, it generated about USD 33.2 billion revenue, with robotics and discrete automation supporting industrial and logistics automation growth.

- Product & Service Portfolio: ABB offers industrial robots (IRB series), collaborative robots (GoFa and SWIFTI), autonomous mobile robots (via ASTI acquisition), RobotStudio software, vision systems, and integrated solutions for warehouse automation, material handling, picking, palletizing, and intralogistics.

- Recent Developments: In 2024, ABB announced a strong push toward AI-driven robotics, highlighting how artificial intelligence, machine vision, and autonomous navigation are enabling smarter picking, sorting, and intralogistics automation solutions across new industry segments. ABB also showcased AI-powered robotic solutions at LogiMAT 2024, including advanced vision-enabled systems and AI-navigation technologies to improve flexibility and efficiency in warehouse and logistics automation.

- Strategic Focus: ABB is prioritizing AI-enabled robotics, AMR-led intralogistics expansion, and software-driven automation ecosystems to scale warehouse and supply chain automation globally.

Fanuc Corporation

Fanuc Corporation, headquartered in Oshino, Japan, is a leading global manufacturer of industrial robots and factory automation systems. In FY2025, it reported approximately JPY 830 billion revenue, with robotics forming a core business segment supporting manufacturing and logistics automation.

- Product & Service Portfolio: Fanuc offers industrial robots (LR Mate, M-series), SCARA robots, CRX collaborative robots, CNC systems, ROBOSHOT injection moulding machines, and automation solutions for material handling, picking, palletizing, machine tending, and warehouse logistics.

- Recent Developments: In February 2024, FANUC showcased CRX collaborative robots integrated with vision systems and autonomous mobile robots (AMRs) at MODEX 2024, demonstrating scalable solutions for order fulfillment, picking, and warehouse automation. FANUC highlighted that CRX cobots support applications such as palletizing, picking, and material handling, helping companies improve efficiency and address labour shortages in warehouse environments.

- Strategic Focus: Fanuc focuses on AI-integrated robotics, collaborative robot expansion, and digital manufacturing platforms to enhance flexible automation and scale logistics and warehouse robotics adoption globally.

KUKA SE & Co. KGaA

KUKA SE & Co. KGaA, headquartered in Augsburg, Germany, is a global automation and robotics provider majority-owned by Midea Group. In 2023, KUKA reported approximately EUR 4.1 billion revenue, with strong contributions from automotive and growing logistics automation segments.

- Product & Service Portfolio: KUKA offers industrial robots (KR series), collaborative robots (LBR iiwa), mobile platforms (KMR iiwa), AGVs/AMRs, software suites, and warehouse automation and intralogistics solutions through its subsidiary Swisslog.

- Recent Developments: In March 2024, KUKA presented advanced mobile robotics solutions at LogiMAT 2024, including the new KMP 3000P autonomous platform and integrated AMR systems designed to automate intralogistics with flexible navigation and real-time obstacle avoidance.

- Strategic Focus: KUKA focuses on mobile robotics, AI-driven automation, and end-to-end warehouse solutions via Swisslog, while leveraging Midea Group’s backing to accelerate expansion in Asia Pacific and global logistics automation markets.

Market Concentration Analysis

The global logistics robots market is moderately concentrated at the top tier, with the five largest players - ABB, Fanuc, KUKA, Dematic, and Yaskawa - collectively accounting for an estimated 38-42% of global revenue in 2025, driven by scale advantages, deep service networks, and vertically integrated hardware-software stacks required for large enterprise contracts.

Market fragmentation remains significant beyond leading global players, with numerous specialized AMR vendors, software providers, and system integrators competing. Fast-growing mid-market companies such as Locus Robotics, GreyOrange, Geek+, and Hai Robotics are gaining traction through focused, application-specific solutions and flexible deployment models, including Robotics-as-a-Service.

Consolidation is accelerating through M&A activity. KION's acquisition of Dematic for USD 2.1 Billion established its logistics leadership, while ABB's acquisition of ASTI Mobile Robotics in 2021 strengthened its AMR position. Further consolidation is expected as incumbents scale software capabilities and RaaS offerings across global markets through 2030.

Investment & Growth Opportunities

Fastest-Growing Segments

Autonomous Mobile Robots (AMRs) are among the fastest-growing segments, driven by e-commerce expansion, warehouse automation, and AI-enabled navigation. Industry estimates suggest global AMR deployments could reach millions of units by 2030, creating strong opportunities for OEMs and software providers.

Asia-Pacific, particularly China and India, represents a major growth hub. India’s warehouse automation and logistics technology market is expanding rapidly, driven by strong e-commerce demand, infrastructure development, and increasing investments in modern supply chain systems.

Emerging Market Expansion

The Middle East and Africa are emerging as high-growth regions for logistics automation, supported by large-scale infrastructure and smart logistics investments. Initiatives such as Saudi Vision 2030 and NEOM, along with the UAE’s logistics hub strategy and African port modernization, are driving long-term demand for automation technologies.

Venture & Strategic Investment Trends

Global venture funding in robotics remained strong in 2024, with significant capital flowing into AI-driven robotics and humanoid systems. Companies like Figure AI raised substantial funding rounds (reported $675M), while firms such as Agility Robotics, Covariant, and 1X Technologies secured major investments, highlighting growing interest in automation and intelligent robotics for logistics.

Future Market Outlook (2026-2034)

The global logistics robots market forecast projects sustained exponential expansion from USD 26.57 Billion in 2025 to USD 116.11 Billion by 2034 at a CAGR of 17.27%, representing a value increase of nearly USD 90 Billion across the forecast period. Growth will be driven by AI-enabled automation, humanoid robot adoption, RaaS expansion, and structural labour economics in developed markets.

Three transformational shifts will reshape the market through 2034. First, humanoid and general-purpose robots will move from pilots to commercial deployment in mixed-task warehouses. Second, AI foundation models will enable generalised manipulation capabilities. Third, cloud-native fleet orchestration will unify multi-vendor robot fleets under unified control planes and analytics systems.

By 2034, logistics robots are expected to evolve from task-specific automation to adaptive, general-purpose systems capable of operating across warehouses, factories, and outdoor environments. Operators investing early in AI, RaaS financing, and fleet orchestration platforms are likely to capture disproportionate value across the automation value chain.

Research Methodology

Primary Research

Primary research included structured interviews in 2024-2025 with robotics OEM executives, warehouse automation directors at Fortune 500 logistics operators, 3PL procurement leaders, venture capital investors active in robotics, and automation consultants. Over 80 interviews informed market sizing, segmentation, and competitive positioning.

Secondary Research

Secondary sources included company annual reports (ABB, Fanuc, KUKA, KION Group), International Federation of Robotics (IFR) World Robotics statistics, national robotics industry association publications (RIA, euRobotics, JARA), government filings, trade media (Modern Materials Handling, Robotics Business Review), and patent filings.

Forecasting Models

Market size and forecast projections were developed using a hybrid top-down and bottom-up approach, incorporating installed base models, unit shipment trajectories, average selling prices, RaaS subscription trends, GDP growth, and e-commerce penetration. Scenario analyses were built under base, optimistic, and conservative macroeconomic assumptions.

Logistics Robots Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Hardware, Software |

| Robot Types Covered | Autonomous Mobile Robots, Automated Guided Vehicles, Robotic Arms, Others |

| Functions Covered | Pick and Place, Loading and Unloading, Packing and Co-Packing, Shipment and Delivery, Others |

| Operation Areas Covered | Factory Logistics Robots, Warehouse Logistics Robots, Outdoor Logistics Robots, Others |

| End Use Industries Covered | E-Commerce, Healthcare, Retail, Food and Beverages, Automotive, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ABB, Fanuc Corporation, KUKA SE & Co. KGaA, Dematic, Yaskawa America, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the logistics robots market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global logistics robots market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the logistics robots industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Logistics Robots Market Report

The global logistics robots market was valued at USD 26.57 Billion in 2025, driven by e-commerce expansion, warehouse automation investments, labour shortages, and rapid advances in AI and sensor technologies.

The market is projected to reach USD 116.11 Billion by 2034, growing at a CAGR of 17.27% during 2026-2034, supported by AMR adoption, humanoid robot emergence, and global warehouse digitalisation.

Hardware leads with a 64.2% share in 2025, driven by heavy capital investment in chassis, motors, LiDAR sensors, vision systems, and grippers that remain core to every deployment.

Automated Guided Vehicles dominate with a 34.6% share in 2025, driven by maturity, predictable fixed-path operations, and cost-effectiveness across automotive plants, large distribution hubs, and factories.

Asia Pacific leads with a 35.7% share in 2025, anchored by China, Japan, and South Korea's large-scale warehouse automation, deep robotics OEM presence, and supportive government programs.

Key drivers include explosive e-commerce growth, persistent labour shortages, rising wage inflation, advances in AI and LiDAR, same-day delivery demands, and smart factory investments globally.

Asia Pacific is the fastest-growing region, driven by China's warehouse buildouts, India's e-commerce expansion, Japan's robotics exports, and aggressive smart factory initiatives across the region.

Leading companies include ABB, Fanuc Corporation, KUKA SE & Co. KGaA, Dematic, and Yaskawa America, Inc., spanning OEMs and integrators.

Autonomous Mobile Robots hold 28.3% in 2025, driven by dynamic navigation capabilities, rapid deployment cycles, and strong adoption across e-commerce and 3PL fulfilment operations.

Software growth (35.8% share) is driven by fleet management platforms, AI-enabled picking algorithms, cloud-based orchestration, WMS integration, and subscription-based commercial models expanding recurring revenue.

AI enables computer-vision picking above 99% accuracy, SLAM-based autonomous navigation, predictive maintenance, and multi-robot coordination, cutting warehouse operating costs by 30-50% for leading operators.

E-commerce represents the largest end-use segment, driven by rapid order volume growth, same-day delivery pressures, and heavy investment by Amazon, JD.com, and Walmart in automation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)