LNG Bunkering Market Size, Share, Trends and Forecast by Product Type, Application, and Region, 2026-2034

LNG Bunkering Market Size and Share:

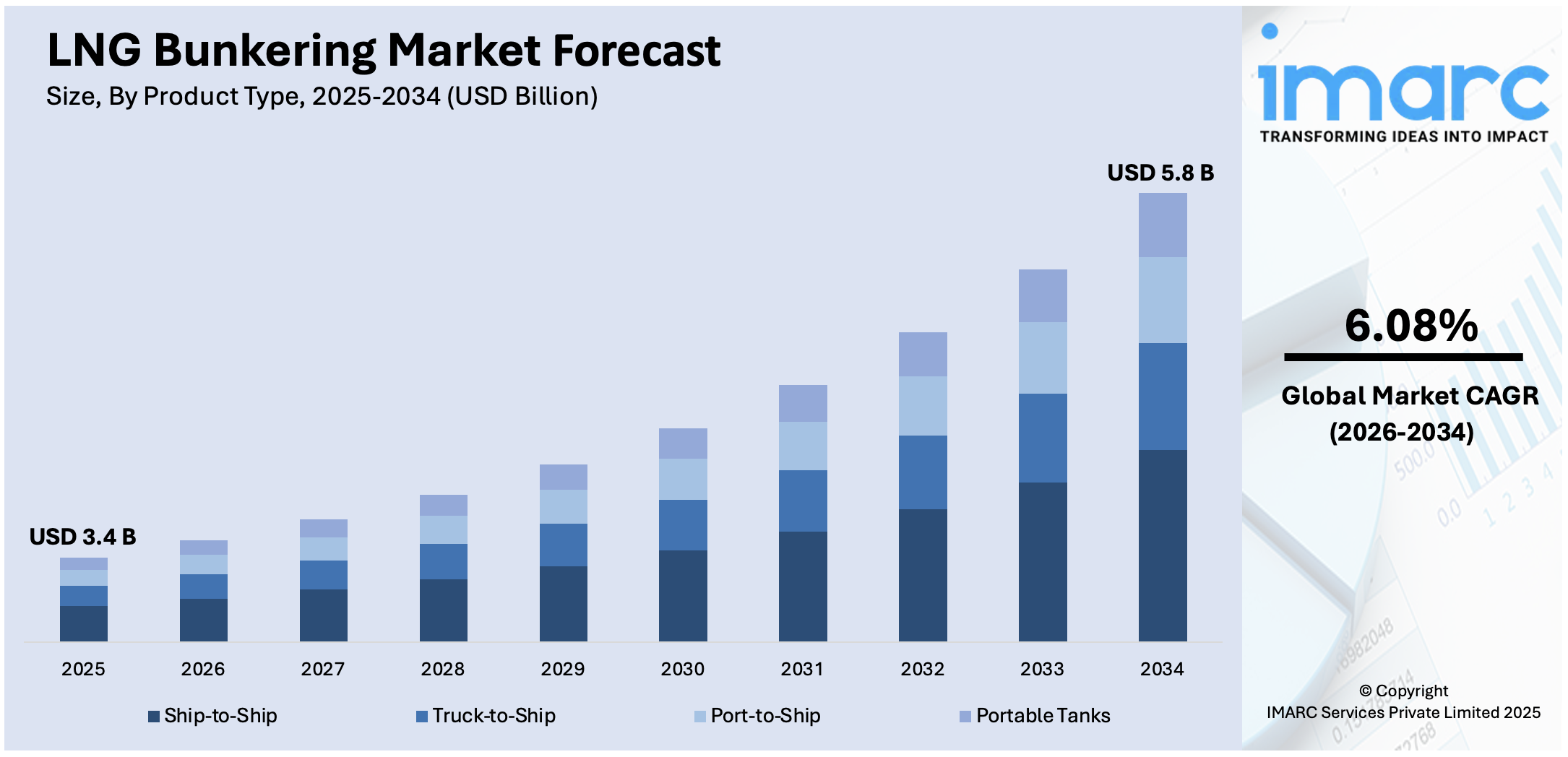

The global LNG bunkering market size was valued at USD 3.4 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 5.8 Billion by 2034, exhibiting a CAGR of 6.08% during 2026-2034. Europe currently dominates the market, holding a significant market share of over 78.6% in 2025, driven by strong economic performance, technological advancements, industry leadership, and a well-established regulatory framework.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3.4 Billion |

| Market Forecast in 2034 | USD 5.8 Billion |

| Market Growth Rate (2026-2034) | 6.08% |

One major driver of the LNG bunkering market growth is the implementation of stringent environmental regulations by the International Maritime Organization (IMO), particularly the IMO 2020 mandate limiting sulfur content in marine fuels to 0.5%. This regulation is accelerating the shift toward cleaner alternatives, with LNG emerging as a preferred fuel due to its lower sulfur oxide, nitrogen oxide, and carbon dioxide emissions compared to traditional marine fuels. For instance, in March 2025, The U.S. Department of Energy has eased restrictions on LNG bunkering, supporting growth as LNG-fueled vessels are projected to surpass 1,200 by 2028, per IEA’s January 2025 report. Shipowners and operators are increasingly investing in LNG-powered vessels and associated bunkering infrastructure to ensure compliance and reduce long-term operational costs, thereby driving demand for LNG bunkering solutions across global shipping routes.

To get more information on this market Request Sample

The United States is serving the LNG bunkering market through substantial investments in infrastructure development, particularly at key ports such as Jacksonville, Florida, and Port Fourchon, Louisiana. These ports are equipped with LNG bunkering terminals and storage facilities, supporting both domestic and international marine traffic. Additionally, U.S.-based companies are actively engaging in ship-to-ship and truck-to-ship LNG bunkering services, enhancing fuel availability for LNG-powered vessels while represents one of the key LNG bunkering market trends. Government support, including regulatory approvals and funding for LNG-related projects, is further accelerating market growth. For instance, in March 2025, EXIM’s board announced the approval of a $4.7 billion loan amendment to support U.S. exports for an LNG project in Mozambique, covering onshore plant construction, related infrastructure, and offshore operations. The U.S. is positioning itself as a strategic LNG bunkering hub, capitalizing on its abundant natural gas reserves and established export capabilities.

LNG Bunkering Market Trends:

Increasing Adoption of LNG as a Shipping Fuel

The market is majorly driven by the widespread adoption of LNG as a shipping fuel with an enhanced focus on sustainable development. This can be attributed to the stringent environmental regulations regarding sulfur content in marine fuel and pollution caused by ship transportation. According to UN Trade and Development (UNCTAD) shipments grew by an estimated 3.2% to reach 11 Billion tons. In line with this, continual advancements in the distribution infrastructure of LNG are providing an impetus to the market. Moreover, a significant increase in gas exploration and production activities across the globe is creating a positive outlook for the market. The market is further driven by a considerable rise in the uptake of truck-to-ship LNG bunkering practices across the globe.

Availability of LNG Bunker Fuel in Marine Industry

Apart from this, the easy availability of LNG bunker fuel in most of the major maritime hubs is impacting the market positively while facilitating the LNG bunkering fuel market demand. The launch of LNG-powered ships resulting in the rapid development of LNG manufacturing and storage facilities are also acting as a significant growth-inducing factor for the market. Some of the other factors contributing to the market include rapid urbanization and industrialization, the growing concerns over the depletion of fossil fuels and extensive research and development (R&D) activities conducted by key players. According to reports, in 2023, emissions from fossil fuels increased by 1.1% compared to the previous year.

Strategic Alliances and Long-Term Contracts

Market participants are entering into long-term bunkering agreements and forming strategic partnerships to secure fuel supply and strengthen market presence. Energy companies are working closely with shipping lines to provide reliable, scalable LNG and bio-LNG fueling solutions. These alliances are supporting fleet transitions toward cleaner fuels and enabling economies of scale in procurement and distribution. Contract-based supply models are becoming increasingly common, providing financial predictability and supporting the development of dedicated LNG bunkering assets. For instance, in March 2025, Titan Clean Fuels and MOL completed their first LNG and bio-LNG bunkering under a new contract, delivering 900 tons to Celeste Ace at Zeebrugge, using ISCC-EU-certified waste-based bio-LNG.

LNG Bunkering Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global LNG bunkering market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type and application.

Analysis by Product Type:

- Ship-to-Ship

- Truck-to-Ship

- Port-to-Ship

- Portable Tanks

Ship-to-ship stand as the largest component in 2025, holding around 51.6% of the market. This method involves the direct transfer of LNG fuel from a bunkering vessel to the receiving ship, offering flexibility, efficiency, and minimal port congestion. The rising number of LNG-fueled vessels and the demand for faster turnaround times at ports are contributing to the widespread adoption of ship-to-ship operations. It is particularly suitable for large vessels and container ships operating on fixed schedules. Additionally, advancements in LNG bunkering vessel design and increasing investments in port infrastructure are further supporting the growth of this segment. Its dominance is expected to continue as major ports enhance their capabilities for safe and efficient ship-to-ship transfers.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Cargo Fleet

- Container Fleet

- Tanker Fleet

- Ferries

- Inland Vessels

- Others

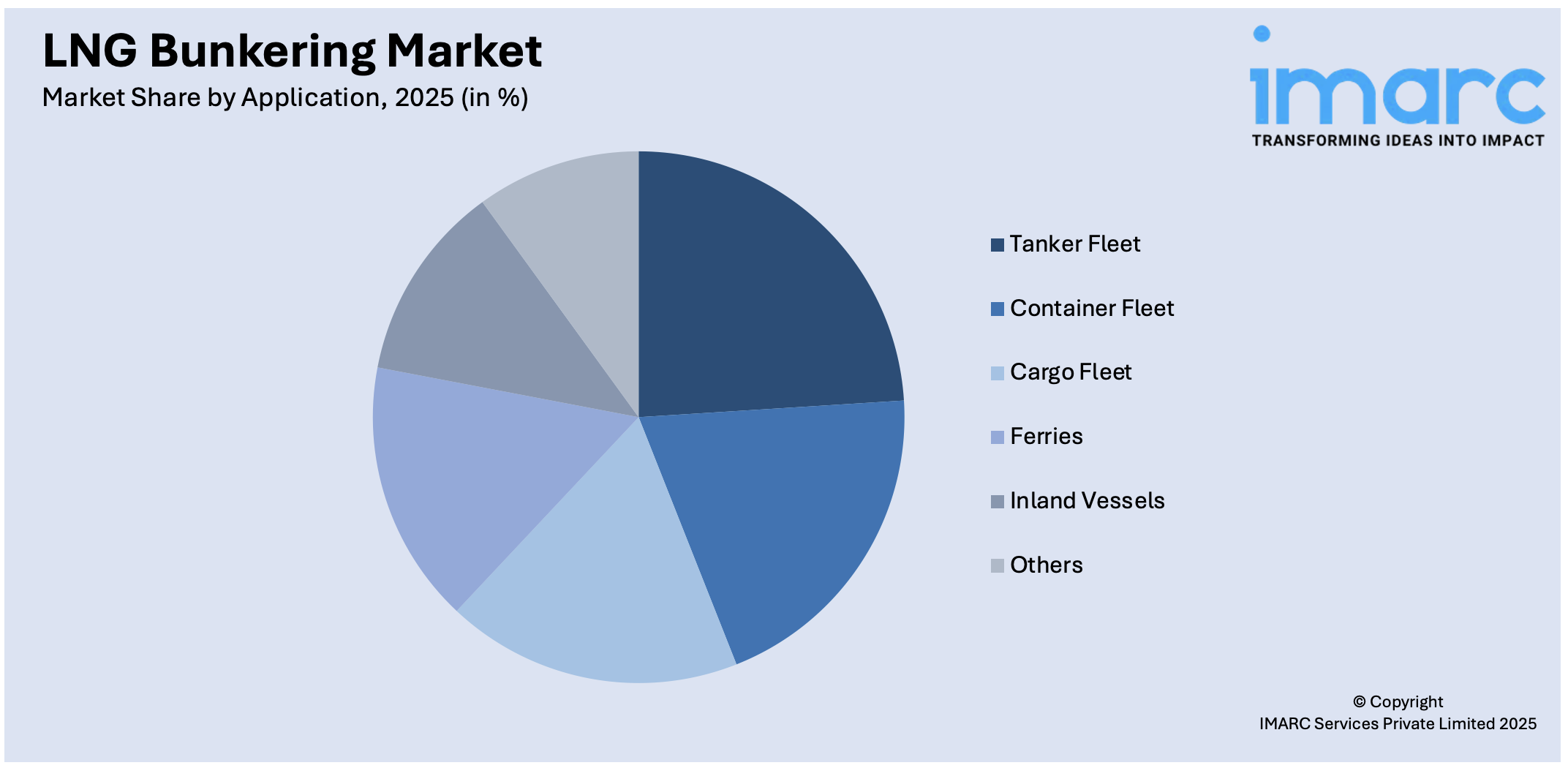

Tanker fleet leads the market with around 23.2% of the LNG bunkering market share in 2025. Tankers, particularly oil and chemical carriers, are increasingly shifting to LNG as a marine fuel to comply with strict international emission standards and reduce operational carbon footprints. These vessels typically operate on long-haul routes, making them suitable candidates for LNG adoption due to the fuel's high energy density and long-range efficiency. Shipping companies are retrofitting existing tankers and commissioning new LNG-powered vessels to align with decarbonization goals. The availability of LNG bunkering infrastructure at major ports and the development of long-term fuel supply agreements are further supporting the transition of tanker fleets toward cleaner propulsion solutions, reinforcing their market dominance.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, Europe accounted for the largest market share of over 78.6%. This dominance is driven by early regulatory adoption, strong policy support for decarbonization, and a well-established LNG bunkering infrastructure across key ports. Countries such as the Netherlands, Belgium, Norway, and Germany are at the forefront, offering multiple bunkering facilities and active support for alternative marine fuels. The Port of Rotterdam and Port of Zeebrugge remain major hubs, handling high volumes of LNG bunkering operations. Additionally, regional initiatives like the European Green Deal and funding under programs such as CEF Transport are encouraging investment in clean fuel logistics. The presence of leading energy firms and shipping companies further cements Europe’s leadership in the LNG bunkering space.

Key Regional Takeaways:

United States LNG Bunkering Market Analysis

US accounts for 95.60% share of the market in North America. United States is experiencing increased LNG bunkering adoption as the depletion of fossil fuels accelerates, driving demand for cleaner maritime fuel alternatives. For instance, fossil fuels, oil, natural gas, and coal, made up approximately 84% of overall U.S. primary energy production in 2023. The growing shift away from conventional marine fuels has led to significant investments in LNG infrastructure, including bunkering terminals and refuelling vessels. As regulatory pressures mount to reduce emissions from shipping operations, LNG is becoming a viable solution for sustainability while ensuring compliance with evolving maritime standards. Technological advancements in LNG storage and distribution have further supported its integration into maritime supply chains. Ship operators are increasingly transitioning to LNG-powered fleets to enhance fuel efficiency and minimize carbon footprints. The depletion of fossil fuels is also influencing long-term strategies for fuel diversification, leading to expanded LNG bunkering networks. Major port authorities are collaborating with energy firms to scale up LNG infrastructure, ensuring seamless refuelling operations. The increasing depletion of fossil fuels has reinforced LNG bunkering adoption as a strategic move to ensure energy security, lower emissions, and enhance operational cost-effectiveness.

North America LNG Bunkering Market Analysis

The North America LNG bunkering market is expanding steadily, driven by environmental regulations, increasing LNG-fueled vessel orders, and supportive government policies. The United States leads the region with key bunkering hubs in Jacksonville, Port Fourchon, and the Port of Long Beach. Recent regulatory easing by the Department of Energy has further removed operational barriers. Companies such as Seaspan Energy and JAX LNG are strengthening regional capabilities through fleet expansion and port-based infrastructure. For instance, in February 2025, Seaspan Energy launched accredited LNG bunkering in Vancouver, following its first operation in Long Beach. Its three 112 m LNG bunkering vessels serve North America's West Coast, ready for global deployment. Canada is emerging as a strategic contributor with the Port of Vancouver entering the LNG bunkering landscape. Growth is further supported by rising adoption of bio-LNG and long-term fueling contracts with global shipping lines, positioning North America as a key player in alternative marine fuel supply.

Asia Pacific LNG bunkering Market Analysis

Asia-Pacific is witnessing accelerated LNG bunkering adoption due to rapid industrialization, which is driving higher maritime trade volumes and the need for efficient fuelling solutions. As per the India Brand Equity Foundation, foreign direct investment in India's manufacturing industry has hit USD 165.1 billion, marking a 69% rise over the last ten years. Expanding industrial activities have intensified cargo shipping, increasing demand for LNG as a lower-emission fuel alternative. With industries seeking sustainable logistics solutions, LNG bunkering is gaining prominence as a cleaner maritime energy source that aligns with environmental goals. The region’s shipbuilding sector is actively investing in LNG-powered vessels, while ports are expanding LNG refuelling infrastructure to accommodate rising industrial shipping needs. As industrialization progresses, logistical hubs are modernizing fuel supply chains, incorporating LNG bunkering to support growing maritime activities. Increased economic output from industrial operations is further accelerating demand for LNG as a reliable and cost-effective fuel option. LNG bunkering adoption continues to rise with supportive government policies encouraging sustainable industrial transport solutions.

Europe LNG bunkering Market Analysis

Europe is experiencing a significant rise in LNG bunkering adoption, driven by an increasing focus on carbon emission reduction across the maritime sector. For example, the EU has established a goal for 2030 of achieving a 55% net decrease in greenhouse gas emissions. Stricter environmental regulations are compelling shipping companies to shift towards cleaner fuel alternatives, making LNG a preferred option for reducing carbon footprints. As emission control areas expand, LNG bunkering infrastructure is rapidly growing to meet the demand for sustainable fuel solutions. Ports and energy firms are collaborating to enhance LNG supply chains, ensuring reliable refuelling capabilities for LNG-powered vessels. The region’s commitment to reducing greenhouse gas emissions has also encouraged shipowners to transition towards LNG propulsion. Advancements in LNG storage and distribution technology are supporting the seamless adoption of LNG bunkering as part of broader decarbonization strategies. The shipping industry’s shift towards environmentally responsible practices is accelerating LNG bunkering expansion.

Latin America LNG bunkering Market Analysis

Latin America is witnessing growing LNG bunkering adoption as urbanization drives higher demand for efficient maritime transport solutions. For instance, 85.2 % of the Latin America population is urban (565,084,260 people in 2024). Expanding urban centres are fuelling an increase in trade volumes, necessitating sustainable fuel alternatives for shipping operations. Ports are integrating LNG refuelling facilities to accommodate rising vessel traffic while aligning with sustainability initiatives. The shift towards LNG bunkering is further supported by urban development policies that emphasize cleaner energy adoption. As cities expand, logistical infrastructure is adapting to support LNG-fuelled shipping for commercial and cargo transport.

Middle East and Africa LNG bunkering Market Analysis

Middle East and Africa is experiencing increased LNG bunkering adoption due to the rapid expansion of the logistics sector, which is driving maritime trade and shipping activities. As per reports, the logistics sector in the Middle East is thriving as GCC nations capitalize on their strategic position, with 30% of worldwide trade flowing through the Red Sea and Gulf of Aden, fueling additional growth and diversification within the industry. The need for efficient fuelling solutions is prompting investments in LNG refuelling facilities at major ports. As logistics operations scale up, LNG is emerging as a preferred alternative to conventional marine fuels, ensuring cost-effective and sustainable shipping. LNG bunkering infrastructure is expanding to support growing logistics networks, facilitating seamless refuelling for LNG-powered vessels.

Competitive Landscape:

The LNG bunkering market is characterized by the presence of key global players competing through strategic partnerships, fleet expansion, and infrastructure investments. Companies are actively expanding their LNG bunkering capabilities to secure long-term contracts with shipping operators. For instance, in February 2025, TotalEnergies Marine Fuels completed Asia Pacific’s first LNG bunkering for a cruise ship at Singapore Cruise Centre, fueling Silver Nova via Brassavola while maintaining smooth passenger and ship operations. Collaboration between port authorities and energy firms is fostering the development of bunkering hubs in Europe, Asia, and North America. Technological innovation and compliance with environmental regulations remain critical differentiators. Market participants are also focusing on enhancing operational efficiency and supply chain integration to strengthen their competitive positions and meet the growing demand for cleaner marine fuel solutions.

The report provides a comprehensive analysis of the competitive landscape in the LNG bunkering market with detailed profiles of all major companies, including:

- Broadview Energy Solutions B.V.

- Crowley

- Gasum Ltd

- Harvey Gulf International Marine LLC

- Korea Gas Corporation

- Petroliam Nasional Berhad (PETRONAS)

- Shell plc

- SHV Energy

- TotalEnergies SE

- Trelleborg Marine and Infrastructure

Latest News and Developments:

- March 2025: Anglo-Eastern launched a cutting-edge LNG Bunkering and Ammonia station skid at its Maritime Academy in Karjat, Mumbai. During the 2025 Mumbai Conference, the facility was inaugurated to further increase maritime training in advanced handling systems for fuels. The bunkering station is a very strong proof of Anglo-Eastern's commitment to sustainable shipping. The main objective of the bunkering station will be to train and fill seafarers with LNG Bunkering and ammonia handling skills.

- December 2024: Wärtsilä Gas Solutions widened its LNG bunkering leadership by signing a new contract with Vitol for its 12,500 cbm vessel. Under construction in Nantong, China, at CIMC Sinopacific Offshore & Engineering, this vessel will come equipped with Wärtsilä's Cargo Handling and Fuel Gas Supply systems. This deal, however, was booked in the final quarter of 2024, a record that adds to the well-established reputation of Wärtsilä in small-scale LNG applications. The collaboration also supports the increasing demand worldwide for effective LNG bunkering solutions.

- October 2024: This July, it comprised a charter agreement with Ibaizabal for an 18,600m³ LNG bunker vessel, thereby extending yet further its LNG Bunkering footprint. The ship would probably operate in Oman and support the Marsa LNG project for Gulf shipping. It will also serve various ships at selected bunkering hubs under high environmental criteria. As compared to the most general marine fuels, LNG can reduces GHG emissions by more than 20% and at the same time makes impressive progress in reducing other pollutants released into the air.

- April 2024: With a delivery of LNG fuel to Daisy Leader at Hiroshima Port, KEYS Azalea completed the first ship-to-ship LNG bunkering in western Japan. It was conducted by KEYS Bunkering West Japan Ltd., and the vessel promotes the use of LNG as a marine fuel for reduction of GHG emissions. The LNG was sourced from the Tobata LNG terminal of Kitakyushu LNG Co., Inc. This is a breakthrough in the adoption of a sustainable maritime fuel.

LNG Bunkering Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Ship-to-Ship, Truck-to-Ship, Port-to-Ship, Portable Tanks |

| Applications Covered | Cargo Fleet, Container Fleet, Tanker Fleet, Ferries, Inland Vessels, and Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Broadview Energy Solutions B.V., Crowley, Gasum Ltd, Harvey Gulf International Marine LLC, Korea Gas Corporation, Petroliam Nasional Berhad (PETRONAS), Shell plc, SHV Energy, TotalEnergies SE, Trelleborg Marine and Infrastructure, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the LNG bunkering market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global LNG bunkering market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the LNG bunkering industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The LNG bunkering market size reached USD 3.4 Billion in 2025.

IMARC estimates the LNG bunkering market to reach USD 5.8 Billion by 2034, exhibiting a CAGR of 6.08% during 2026-2034.

Key factors driving the LNG bunkering market include stringent emission regulations, rising adoption of LNG-fueled vessels, and expansion of port-based infrastructure. Additionally, increasing availability of bio-LNG, government support for clean marine fuel initiatives, and growing investments by shipping and energy companies are further accelerating market growth worldwide.

Europe currently dominates the market with a 78.6% share, due to its advanced technological infrastructure, established industry leaders, and strong demand across various sectors. This dominance is supported by continuous innovation, investment in research and development, and a favorable regulatory environment, making Europe a global market leader.

Some of the major players in the LNG bunkering market include Broadview Energy Solutions B.V., Crowley, Gasum Ltd, Harvey Gulf International Marine LLC, Korea Gas Corporation, Petroliam Nasional Berhad (PETRONAS), Shell plc, SHV Energy, TotalEnergies SE, Trelleborg Marine and Infrastructure, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)