Laser Technology Market Size, Share, Trends and Forecast by Type, Product, Application, End User, and Region, 2026-2034

Laser Technology Market Size and Share:

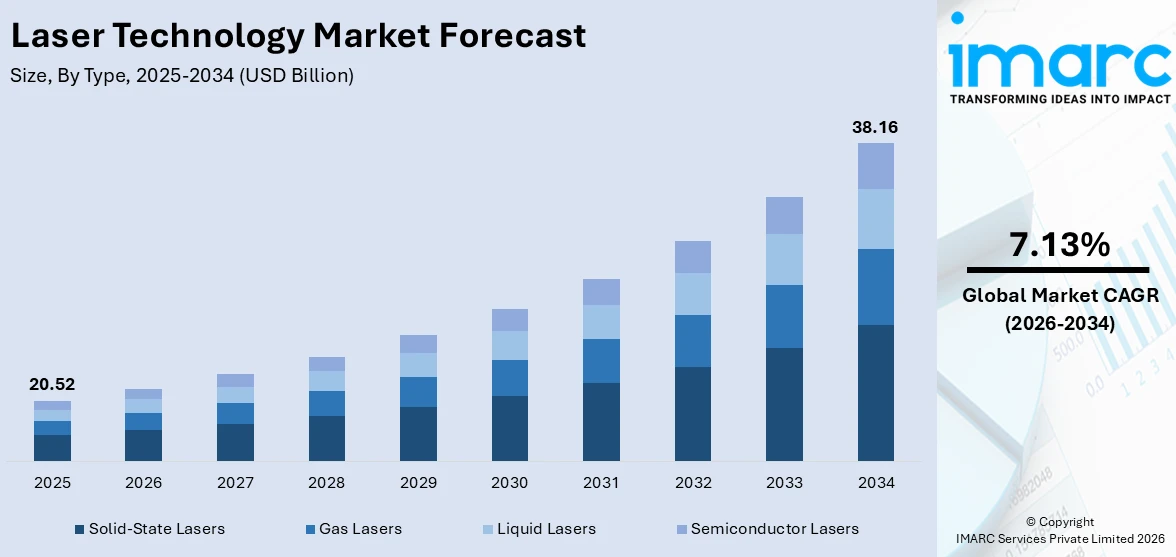

The global laser technology market size was valued at USD 20.52 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 38.16 Billion by 2034, exhibiting a CAGR of 7.13% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of 35% in 2025. The region benefits from extensive manufacturing infrastructure, government-backed smart manufacturing programs, such as China's industrial modernization initiatives, and robust demand from electronics, automotive, and semiconductor industries, all contributing to the laser technology market share.

The global laser technology market is being propelled by the rising emphasis on precision manufacturing and automation across industries, such as automotive, aerospace, electronics, and healthcare. The transition from traditional manufacturing processes to laser-based techniques is accelerating as companies seek higher productivity, reduced waste, and enhanced product quality. Furthermore, the increasing adoption of laser technology in optical communications and data transmission infrastructure is supporting the market growth. The proliferation of fiber-optic networks and the deployment of next-generation telecommunications systems are creating sustained demand for laser components. Additionally, the growing research and development (R&D) investments aimed at developing higher-efficiency laser sources, ultrafast laser systems, and compact laser modules for emerging applications, are offering a favorable laser technology market outlook.

The United States is becoming a major player in the laser technology market, driven by several key factors. The country's advanced industrial base, combined with substantial investments in defense and semiconductor technologies, is fueling the widespread adoption of laser systems across diverse sectors. Additionally, the presence of leading laser technology companies and renowned research institutions further strengthening the market growth. A prime example of this is Civan Lasers' 2024 announcement of opening two demonstration labs in the USA, located in Rexburg, Idaho, and Detroit, Michigan. These labs were designed to showcase Civan's innovative Dynamic Beam Laser technology, which aimed to revolutionize laser welding processes. This development underscores the United States' ongoing leadership in laser technology innovation and its critical role in shaping future industrial applications.

To get more information on this market Request Sample

Laser Technology Market Trends:

Innovation in Customization and Efficiency

The increasing demand for customization and efficient production processes across various industries is a crucial factor impelling the market growth. The rise of individual personalization, particularly in sectors like retail and promotional products, is driving the adoption of advanced laser systems. A notable example of this trend is the 2025, unveiling of the Tumbler Laser Engraving Machines by Laser Photonics and CMS. These machines utilized CO2 laser technology to create precise, permanent markings on drinkware, offering an innovative solution for high-volume customization. By enhancing brand visibility and consumer engagement, the technology not only meets the growing demand for personalized products but also improves operational efficiency. The system was designed to boost sustainability by reducing material waste and increasing resource management in industrial marking applications. As industries continue to embrace more sustainable, precise, and efficient manufacturing methods, such advancements play a pivotal role in supporting the laser technology market growth.

Advancements in Medical Laser Technology

The continuous innovation in medical laser systems, particularly those designed for precision, efficiency, and improved patient outcomes, is influencing the market. The healthcare sector’s growing demand for minimally invasive procedures is significantly contributing to this trend. In 2025, Coherent Corp. launched the ACE FL Series, a two-micron Thulium Fiber Laser designed specifically for medical applications, such as lithotripsy and Benign Prostatic Hyperplasia (BPH) treatment. This new laser technology offered enhanced precision, leading to more effective treatments and improved patient recovery times. Furthermore, the ACE FL Series demonstrated superior energy efficiency compared to older systems, making it more sustainable and cost-effective. The system was also designed for seamless integration into minimally invasive surgical tools, offering scalable, high-performance solutions for OEMs in the medical field. As such, innovations like these are propelling the market growth by meeting the rising demand for advanced, efficient, and precise medical treatments across a wide range of conditions.

Rise of Sustainable Packaging Solutions

As environmental concerns intensify, companies are seeking innovative ways to reduce waste, improve energy efficiency, and enhance the sustainability of their production processes. In 2025 , Sidel introduced its EvoBLOW laser technology at Drinktec 2025, a groundbreaking solution aimed at transforming lightweighting for PET and rPET packaging in the food and beverage sector. This laser-based system significantly reduced preform waste by 50% compared to traditional methods, offering precise control over material thickness to minimize material usage. Additionally, the EvoBLOW Laser incorporated advanced features like live speed modulation and cold oven technology, improving operational efficiency and stability. By enabling the production of stronger, more sustainable packaging with less environmental impact, the technology aligned with the industry’s shift toward greener, more resource-efficient practices. This trend underscores the growing role of laser technology in driving sustainability within manufacturing, ultimately contributing to the market demand.

Laser Technology Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global laser technology market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, product, application, and end user.

Analysis by Type:

- Solid-State Lasers

- Fiber Lasers

- Ruby Lasers

- YAG Lasers

- Thin-Disk Lasers

- Gas Lasers

- CO2 Lasers

- Excimer Lasers

- He-Ne Lasers

- Argon Lasers

- Chemical Lasers

- Liquid Lasers

- Semiconductor Lasers

Solid-state lasers account for 40% of the market share, making them a dominant force in the laser technology sector. These lasers encompass a wide variety of systems, including fiber, ruby, YAG, and thin-disk variants, which are extensively used across industrial, medical, scientific, and defense applications. Their popularity is driven by several key advantages, such as high-power efficiency, superior beam quality, exceptional durability, and their ability to support precision-driven tasks in demanding operational environments. The versatility of solid-state lasers allows for their seamless integration into various manufacturing processes, including cutting, welding, marking, and micro-machining. These attributes make solid-state lasers ideal for industries that require consistent performance and accuracy, including automotive, aerospace, electronics, and healthcare. As a result, solid-state lasers continue to play a crucial role in advancing modern production techniques, offering reliable and efficient solutions for both large-scale and intricate operations across multiple sectors.

Analysis by Product:

- Laser

- System

Laser leads the market with a commanding share of 65%, encompassing a wide range of standalone laser sources, including fiber lasers, solid-state lasers, gas lasers, and semiconductor lasers. This laser system serves as the core light-generating components for a variety of industrial and scientific applications, offering exceptional versatility and performance. The growing demand for standalone laser units is primarily driven by their integration into customized systems developed by original equipment manufacturers (OEMs) and system integrators. This entity requires lasers with specific wavelength, power, and beam characteristics to meet the precise needs of its applications, which span industries, such as manufacturing, aerospace, healthcare, and research. The ability to tailor this laser to unique operational requirements ensures its continued dominance in the market, with applications ranging from material processing and medical treatments to high-precision scientific experiments. The laser technology market forecast predicts continued growth driven by evolving industry demands and technological advancements.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Laser Processing

- Optical Communications

- Optoelectronic Devices

- Others

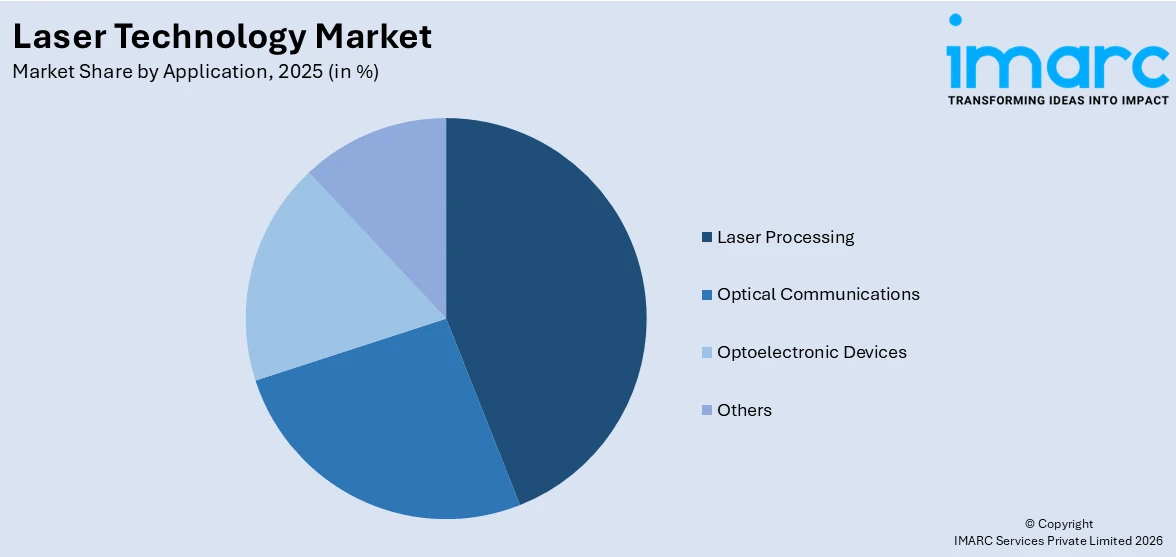

Laser processing dominates the market, with a share of 44%. This segment includes a range of essential applications like cutting, welding, drilling, marking, engraving, and additive manufacturing, all of which play a critical role in modern industrial production. Its leadership can be attributed to the widespread adoption of laser-based manufacturing techniques across industries, including automotive, aerospace, electronics, packaging, and metalworking. Laser processing offers distinct advantages over traditional methods, including greater precision, higher processing speeds, reduced material waste, and compatibility with a variety of materials. The increasing demand for lightweight vehicle construction, particularly for EVs, is further driving the need for laser welding of battery components and aluminum structures. In 2024, nLIGHT demonstrated this trend by launching two advanced laser technologies, nfinity™ and ProcessGUARD™, at FABTECH and EuroBLECH 2024. These innovations enhance cutting speed and accuracy for thick metal applications, optimize process monitoring, and boost productivity in industrial and aerospace sectors, reducing costs while increasing efficiency.

Analysis by End User:

- Telecommunications

- Industrial

- Semiconductor and Electronics

- Commercial

- Aerospace and Defence

- Automotive

- Healthcare

- Others

Industrial represents the leading segment, with a market share of 32%. This segment encompasses a wide range of applications, including manufacturing, metalworking, heavy machinery, textiles, and general industrial production. As industries continue to evolve, there is a rise in the demand for advanced laser systems in surface treatment, precision manufacturing, and material processing. A notable example of innovation in this space is the 2024 launch of Laser Photonics Corporation's CleanTech Industrial Roughening Laser 3060 (CTIR-3060). This pulsed fiber laser system was designed to minimize thermal impact, making it ideal for delicate materials. The CTIR-3060 can be used independently or integrated with the automated CleanTech Robotic Cell, and features like overheat protection and mobile connectivity for remote operation make it particularly suited for sectors like aerospace, automotive, and defense. This development highlights the increasing reliance on laser technology to meet the complex needs of modern industrial applications.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Other

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Other

- Latin America

- Brazil

- Mexico

- Other

- Middle East and Africa

Asia Pacific, accounting for 35% of the share, enjoys the leading position in the market. This dominance is primarily fueled by rapid industrialization, extensive manufacturing infrastructure, and strong demand from key industries, such as automotive, electronics, and semiconductors. A notable example of this trend is the growing adoption of "Make in India" laser solutions by clinics across India in 2025. Driven by affordability, localized support, and government incentives, these domestically produced systems, such as IMDSL's dental and proctology lasers, offer both high performance and cost-effectiveness. As a result, they are enhancing clinical efficiency and expanding service offerings in various medical fields. This shift towards locally manufactured, affordable laser technology not only supports the country’s healthcare sector but also strengthens the broader adoption of advanced laser systems within the region.

Key Regional Takeaways:

United States Laser Technology Market Analysis

The United States is a prominent and technologically advanced market for laser technology, driven by robust demand across key sectors, including industrial manufacturing, defense, healthcare, and semiconductors. The country's well-established industrial base, combined with its focus on precision manufacturing and automation, is significantly accelerating the adoption of advanced laser systems for applications, such as cutting, welding, marking, and additive manufacturing. The defense sector, in particular, represents a substantial driver of demand, with significant investments being directed toward directed-energy weapons, counter-drone systems, and advanced targeting technologies. In line with these advancements, in 2025 , Tescan acquired FemtoInnovations, a leader in ultrafast laser technology, and established a new laser technology Business Unit (LT BU) at the University of Connecticut Tech Park. This strategic acquisition enhanced Tescan’s capabilities in semiconductor, biomedical, and advanced manufacturing markets, allowing for the integration of ultrafast laser micromachining with their imaging and analysis platforms. The move underscores the growing importance of laser technology in driving innovation across multiple high-tech industries in the United States.

North America Laser Technology Market Analysis

The North America is a crucial player in the laser technology market, recognized for its technological advancements and strong demand across various sectors, such as industrial manufacturing, defense, healthcare, and semiconductors. The region’s well-established industrial base, coupled with its focus on precision manufacturing and automation, is driving the widespread adoption of advanced laser systems for applications like cutting, welding, marking, and additive manufacturing. A notable example of this technological progress occurred in 2024 , when nLIGHT unveiled two new laser technologies, WELDForm and Automatic Parameter Tuning (APT), at The Battery Show North America. These innovations are specifically designed to improve laser welding in advanced battery manufacturing, addressing the growing demand in the e-mobility sector. These improvements offer great potential for creating more efficient and dependable battery systems by improving weld quality and minimizing defects. This launch underscored the North America’s crucial life in laser technology innovation, especially in industries critical to the future of sustainable energy and advanced manufacturing.

Europe Laser Technology Market Analysis

Europe stands as a mature and innovation-driven market for laser technology, underpinned by a robust manufacturing base and a strong emphasis on R&D. The region is continuously advancing in diverse sectors, ranging from healthcare to aerospace, with laser technology playing a crucial role in this progress. In 2025, the UK government made a significant move by announcing a £500,000 investment in new laser detection technology aimed at safeguarding satellites from potential threats. The advanced sensors, developed by UK Space Command and the UK Space Agency, were designed to detect lasers that may disrupt communications or cause damage to satellite systems. This investment reflects Europe's commitment to leveraging cutting-edge laser technology for defense and security purposes, ensuring the continued protection and operational integrity of critical space infrastructure. It highlights the region's focus on both innovation and security in the evolving landscape of technological advancements.

Asia-Pacific Laser Technology Market Analysis

Asia Pacific stands as the largest and fastest-growing regional market for laser technology, fueled by rapid industrialization, expanding manufacturing capabilities, and government initiatives aimed at promoting advanced manufacturing. A key development in this growth occurred in 2024 when Sichuan Strongest laser technology renewed its agent contract in Korea, reinforcing its commitment to the region. This partnership aimed to introduce cutting-edge laser equipment to major industries, including global giants like Samsung and Hyundai. By focusing on enhancing technological capabilities, the renewal not only strengthens Sichuan Strongest laser technology's market presence but also supports the mutual growth of both companies, driving further advancements in laser technology across critical sectors in the region.

Latin America Laser Technology Market Analysis

Latin America is experiencing growth in the laser technology market, driven by expanding industrial activities and infrastructure development across the region. A significant milestone occurred in 2025, when LA&HA, in collaboration with Fotona and Zaneo/Odella, inaugurated two new training centers in Bogotá, Colombia, and Mexico City, Mexico. These centers, focused on medical laser education, offer workshops in aesthetics and gynecology. The events, which celebrated Fotona’s 60 years of innovation in laser technology, attracted large audiences of medical professionals, underscoring the growing interest and potential for laser technology in the region's healthcare sector. This development is a clear indication of the laser technology market growth in Latin America, with increasing adoption and innovation across various industries.

Middle East and Africa Laser Technology Market Analysis

The Middle East and Africa region is witnessing adoption of laser technology, fueled by rising investments in infrastructure, oil and gas operations, and robust manufacturing sectors. A notable example of this progress is the UAE's advancement in laser technology for rainfall stimulation. In 2026, successful laboratory tests conducted under the UAE Research Program for Rain Enhancement Science at the Technology Innovation Institute (TII) demonstrated that laser beams can effectively induce water vapor condensation. This breakthrough offers a promising solution to water scarcity, with future field trials planned to enhance precipitation and bolster water security in arid regions. These developments align with emerging laser technology market trends, highlighting the growing role of lasers in addressing critical environmental challenges.

Competitive Landscape:

The global laser technology market is characterized by the presence of established multinational corporations and specialized technology providers competing on the basis of innovation, product performance, and global reach. Leading companies are investing heavily in research operations to advance fiber laser capabilities, ultrafast laser systems, and AI-integrated manufacturing platforms. Strategic partnerships, acquisitions, and geographic expansion are key strategies employed by market participants to strengthen their competitive positions. Companies are increasingly focusing on vertical integration to secure supply chains for critical components such as pump diodes, nonlinear crystals, and precision optics. The development of application-specific laser solutions tailored to emerging sectors including electric vehicle manufacturing, semiconductor fabrication, and directed-energy defense systems represents a significant area of competitive differentiation.

The report provides a comprehensive analysis of the competitive landscape in the laser technology market with detailed profiles of all major companies, including:

- Bystronic Laser India Pvt. Ltd.

- Coherent Inc. (Coherent Corp.)

- Epilog Laser

- Eurolaser GmbH

- Gravotech Engineering PVT. Ltd.

- Han's Laser Technology Industry Group Co. Ltd.

- IPG Photonics Corporation

- Jenoptik AG

- LaserStar Technologies Corporation

- Lumibird Group

- Novanta Inc.

- Trumpf Group

Latest News and Developments:

- In January 2026, Laser Technologies launched a 5-axis CNC tube bending machine and Smart Weld Pro at IMTEX Forming & MOLDEX INDIA 2026 in Bangalore. These innovations aim to enhance precision, flexibility, and efficiency in forming and welding processes. The company also showcased a comprehensive laser fabrication ecosystem, reaffirming its role as a leader in India's evolving manufacturing sector.

- In November 2025, Exail launched the IXF-2CF-EY-10-130-SMX, a new erbium/ytterbium (Er:Yb) co-doped optical fiber for next-gen fiber lasers. This innovation improved power scalability, offering 30W output with exceptional beam quality, efficiency, and immunity to photodarkening. It enhanced free-space communication, LiDAR, and quantum technologies, enabling compact, reliable, and high-performance systems.

Laser Technology Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Products Covered | Laser, System |

| Applications Covered | Laser Processing, Optical Communications, Optoelectronic Devices, Others |

| End Users Covered | Telecommunications, Industrial, Semiconductor and Electronics, Commercial, Aerospace and Defence, Automotive, Healthcare, Others |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Saudi Arabia, United Arab Emirates |

| Companies Covered | Bystronic Laser India Pvt. Ltd., Coherent Inc. (Coherent Corp.), Epilog Laser, Eurolaser GmbH, Gravotech Engineering PVT. Ltd., Han's Laser Technology Industry Group Co. Ltd., IPG Photonics Corporation, Jenoptik AG, LaserStar Technologies Corporation, Lumibird Group, Novanta Inc., Trumpf Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the laser technology market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global laser technology market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the laser technology industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The laser technology market was valued at USD 20.52 Billion in 2025.

The laser technology market is projected to exhibit a CAGR of 7.13% during 2026-2034, reaching a value of USD 38.16 Billion by 2034.

The laser technology market is driven by trends in customization, medical advancements, and sustainability. The demand for personalized products boosts customization efficiency, while innovations in medical lasers enhance precision and patient outcomes. Additionally, the focus on sustainable packaging solutions accelerates adoption, supporting the market growth.

Asia Pacific currently dominates the laser technology market, accounting for a share of 35%. The region benefits from extensive manufacturing infrastructure in China, Japan, and South Korea, government-backed smart manufacturing initiatives, and strong demand from automotive, electronics, and semiconductor industries.

Some of the major players in the laser technology market include Bystronic Laser India Pvt. Ltd., Coherent Inc. (Coherent Corp.), Epilog Laser, Eurolaser GmbH, Gravotech Engineering PVT. Ltd., Han's Laser Technology Industry Group Co. Ltd., IPG Photonics Corporation, Jenoptik AG, LaserStar Technologies Corporation, Lumibird Group, Novanta Inc., Trumpf Group, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)