Kidney Cancer Therapeutics and Diagnostics Market Size, Share, Trends and Forecast by Component, Cancer Types, Application, and Region, 2025-2033

Kidney Cancer Therapeutics and Diagnostics Market Size and Share:

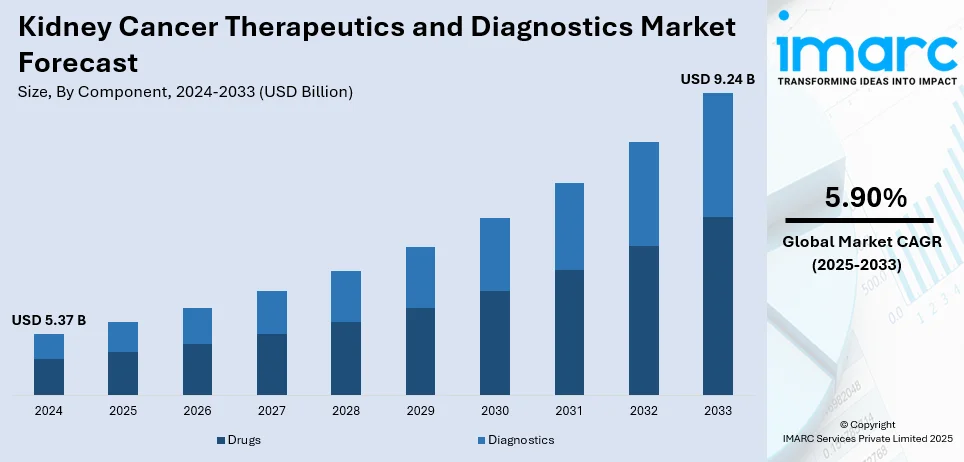

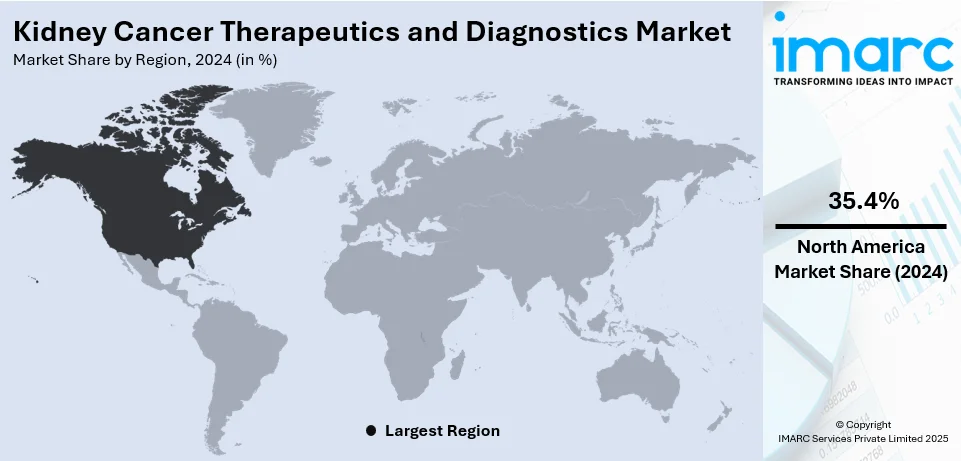

The global kidney cancer therapeutics and diagnostics market size was valued at USD 5.37 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 9.24 Billion by 2033, exhibiting a CAGR of 5.90% during 2025-2033. North America currently dominates the market, holding a market share of over 35.4% in 2024. The rising incidences of kidney cancer, increasing geriatric population, and favorable initiatives by several governments represent some of the key factors driving the kidney cancer therapeutics and diagnostics market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 5.37 Billion |

|

Market Forecast in 2033

|

USD 9.24 Billion |

| Market Growth Rate (2025-2033) | 5.90% |

Kidney cancer cases are increasing globally, creating a significant need for improved treatment and diagnostic options. Factors like aging populations and lifestyle habits such as smoking, obesity, and high blood pressure (BP) contribute to boosting the kidney cancer therapeutics and diagnostics market demand. In the United States alone, kidney cancer caused nearly 15,000 deaths in 2023 and over 90 percent of adult kidney cancers were renal cell carcinoma (RCC). This has created the need or early diagnosis to prevent deaths and spread of the disease. Early detection has also become more common due to increased awareness and routine health check-ups, but the growing number of cases highlights the need for innovation. For instance, advancements in imaging technology and biomarker testing are helping detect kidney cancer at earlier stages, which improves treatment outcomes. This demand for better diagnostic and therapeutic options drives market growth by encouraging research and development in this space. Kidney cancer therapeutics and diagnostics are employed to treat and diagnose renal cell carcinoma (RCC), benign tumors of the kidney, Wilms tumors, transitional cell carcinoma, renal sarcoma, medullary carcinoma, multilocular cystic RCC, and mucinous tubular and spindle cell carcinoma.

The United States is a major market disruptor with 89.60% in North America. In the year 2024, 81,610 new cases of kidney and renal pelvis cancer in the U.S. were recorded with the majority occurring in individuals aged 65 and older. The increasing elderly population, with its susceptibility to renal cell carcinoma and other kidney cancer types, is helping drive demand for therapies and diagnostics that can treat tumors, extend survival, and preserve the noncancerous parts of the kidney in the country. Moreover, the implementation of various government initiatives to spread awareness regarding cancer is creating a positive kidney cancer therapeutics and diagnostics market outlook. Other factors that push the growth in the United Sates include major advancements in the healthcare sector, significant investment in R&D activities to explore potential treatment options, and the growing acceptance of high-tech methods of treatments like robotic surgery, telemedicine, and artificial intelligence.

Kidney Cancer Therapeutics and Diagnostics Market Trends:

Rising Prevalence of Kidney Cancer

A key growth driver for the kidney cancer therapeutics and diagnostics market share is the rising global incidence of kidney cancer. The International Kidney Cancer Coalition reported about 431,000 new cases every year. With the rising burden of the disease, the increasing demand for advanced diagnostic and effective therapeutic options will remain a crucial challenge. This surge is thus motivating the health care systems to seek some of the world's recent cutting-edge technologies in diagnosis imaging techniques and in molecular diagnostics intended for early and proper staging in kidney cancer cases. Growing demands for new and innovative therapies-such as targeted treatments and immunotherapies-in turn call for tremendous improvement in the formulation of more tailor-made and highly effective treatment protocols. With the increased incidence of kidney cancer worldwide, the market is therefore bound to continue growing, with innovation and solutions availed on the market to improve patient outcomes.

Advancements in Diagnostic and Therapeutic Technologies

Significant developments in biomarker-based diagnostics, liquid biopsies, and advanced imaging technologies such as PET/CT scans have improved early detection rates for kidney cancer. Accurate diagnosis and appropriate planning lead to better outcomes for patients. Targeted therapies, immunotherapies like immune checkpoint inhibitors, and personalized medicine approaches are now revolutionizing the treatment strategies that are boosting the kidney cancer therapeutics and diagnostics market growth. One in point includes the approval made by Health Canada in October 2022 to KEYTRUDA. This marks the significance as at that point, KEYTRUDA was deemed as a monotherapy for the adjuvant treatment of adults with RCC at intermediate-high or high risk of either recurrence after nephrectomy or after nephrectomy and resection of metastatic lesions. The approvals further add up to the rising use of immunotherapy for kidney cancer treatments, which has created a cycle of further increasing demand for the advanced forms of treatment and fueling growth in the market for therapeutics and diagnostics of kidney cancer.

Increasing Investments and Research Initiatives

As per the kidney cancer therapeutics and diagnostics market forecast, significant funding and research activities in oncology are driving new treatments for kidney cancer, thereby propelling the growth of the market. In this regard, the National Cancer Institute is a significant player that provides substantial funds for kidney cancer research, an aspect that drives innovation and the subsequent introduction of the next-generation diagnostic and therapeutic solutions. Public and private sector investment initiatives have also helped promote investments in research and development, which further promote market growth. For example, in September 2022, Weill Cornell Medicine received a USD 1 million three-year grant from the Department of Defense's Kidney Cancer Research Program. The body is researching the function of the ATF4 protein in clear cell renal cell carcinoma (ccRCC), especially about its possible revolutionary therapy. This type of funding will help recognize novel biomarkers, target new therapies, and refine diagnostic processes; all lead to better managements of the kidney cancer patients, which encourage continuous development within therapeutics and diagnostics in the market.

Kidney Cancer Therapeutics and Diagnostics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global kidney cancer therapeutics and diagnostics market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on component, cancer types, and application.

Analysis by Component:

- Drugs

- Drugs by Therapeutic Class

- Targeted Therapy

- Immunotherapy

- Others

- Drugs by Pharmacologic Class

- Angiogenesis Inhibitors

- mTOR Inhibitors

- Monoclonal Antibodies

- Cytokine Immunotherapy (II-2)

- Drugs by Therapeutic Class

- Diagnostics

- Imaging Test

- Biopsy

- Blood Test

- Others

Drugs lead the market with approximately 84.3% of market share in 2024. The supremacy of drugs in the market has developed primarily due to their high efficacy and potential side-effect-free aspects as demanded by the targeted therapies and immunotherapies. The relevant drugs, useful in targeted therapy are TKIs like sunitinib and pazopanib, while some examples of immunotherapy include immune checkpoint inhibitors pembrolizumab and nivolumab. The spreading consumption of these drugs is associated with their superior efficacy and reduced side effects as compared to conventional chemotherapies. The incessant introduction of new drugs and combination therapies through intensive R&D activities has fueled the segment's growth. The drugs segment is thus an important growth driver for the market given the increasing incidence of kidney cancer and the need for personalized and oriented medicines.

Analysis by Cancer Types:

- Clear Cell RCC

- Papillary RCC

- Chromophobe RCC

- Transitional Cell Carcinoma

- Others

Clear cell RCC leads the market with around 66.3% of market share in 2024. This cancer type is characterized by the presence of clear cells, which have a distinct appearance due to their high lipid and glycogen content. It is often diagnosed at an advanced stage and is associated with a poor prognosis if not treated promptly. The large share of the clear cell RCC segment in the market is driven by the increasing prevalence of this cancer type, advancements in targeted therapies and immunotherapy, and the growing focus on early detection and personalized treatment options.

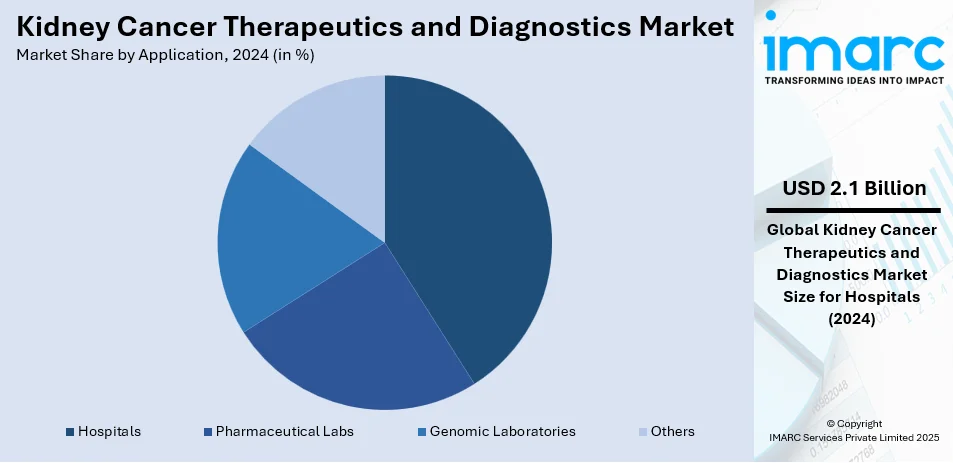

Analysis by Application:

- Hospitals

- Pharmaceutical Labs

- Genomic Laboratories

- Others

Hospital leads the market with a total market share of approximately 40.0% in 2024. The hospital-based market is dominated as they have the proper infrastructure facilities for the diagnosis and treatment processes of kidney cancer. They are well-equipped with extensive diagnostics, including imaging techniques and biopsies, which are mandatory for the proper staging and treatment of this cancer. Furthermore, the existence of specific oncology units in hospitals also implies a variety of treatments available, such as surgery, radiation therapy, targeted therapies, and immunotherapy among others. Multidisciplinary care teams consisting of oncologists, radiologists, and surgeons are present; such teams make a hospital's role in the management of kidney cancer more potent. With the increasing incidence of kidney cancer, hospitals are the primary healthcare setting for both initial diagnosis and ongoing treatment, thereby driving the largest share of this segment in the market.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America held the highest market share of 35.4%. The U.S. takes a lead in this market for a number of reasons that include the high prevalence of kidney cancer, cutting-edge infrastructural health facilities, and significant research development and manufacturing investments. The region is rich in healthcare infrastructural systems, advanced diagnostic technologies, and access to a variety of treatment modalities; some of them being targeted therapy and immunotherapy that provide value to patients. In light of this, North America has a strong pipeline for new therapies and diagnostic tools from various pharmaceutical companies and academic institutions to guarantee their place in the market. The huge awareness growth and initiative have made North America, with numerous early detection programs, to be the largest market for kidney cancer therapeutics and diagnostics.

Key Regional Takeaways:

United States Kidney Cancer Therapeutics and Diagnostics Market Analysis

The United States is leading the market with 89.60% share in North America. The increasing prevalence of kidney cancer in America is a significant cause of the kidney cancer therapeutics and diagnostics market growth. The American Cancer Society's 2022 update reports approximately 79,000 new diagnoses of kidney cancer in the U.S. by the end of 2022. This growing incident rate has increased the demand for efficient diagnosis and better treatment options, such as targeted therapies and immunotherapies. An additional number of patient diagnostics increases the demands for early diagnostic techniques, molecular diagnostics, and imaging technologies. Furthermore, in light of developing personalized medicine as well as implementing new treatments is fueling rapid growth in this market. Moving forward, expanding research, alongside increased awareness over kidney cancer will provide an impetus to the overall market for both therapeutics as well as diagnostics. This trend is further supported by ongoing investments in healthcare infrastructure and oncology services across the country.

Europe Kidney Cancer Therapeutics and Diagnostics Market Analysis

One of the main growth drivers of the kidney cancer therapeutics and diagnostics market in Europe is the rising incidence of renal cell carcinoma (RCC). The world witnessed an estimated 431,288 new cases of RCC in 2020, while in the European region, there were an estimated 138,611 cases, according to Euroweb. Therefore, the rising number of diagnoses is driving the demand for early detection as well as effective treatment options. The diagnostic tools in Europe are experiencing great leap ahead in terms of imaging technologies and biomarkers-assisted testing to achieve a better early diagnosis of RCC. Moreover, the heightened interest in personal therapies such as targeted medicines and immunotherapy has driven the market since healthcare providers have a preference for such treatments, which can more effectively impact patients suffering from RCC. Additionally, a strong health care infrastructure in Europe and continued investments in cancer research and clinical trials also help support the growth of the therapeutics and diagnostics market. With the increasing incidence of RCC, there will be a steady demand for innovative treatment options and diagnostic solutions.

Asia Pacific Kidney Cancer Therapeutics and Diagnostics Market Analysis

The rapidly increasing incidence of kidney cancer in China has been an important growth factor driving the Asia-Pacific market of kidney cancer therapeutics and diagnostics. According to the NIH, in 2019, there were 59,827 new cases, 23,954 deaths, and 642,799 DALYs for kidney cancer in China. This is indicative of the increasing burden of kidney cancer and thus the increasing need for better diagnostic tools and treatment options. China is currently coming to terms with a rapidly increasing number of people being diagnosed with kidney cancer, for which early detection and targeted treatment and immunotherapy are highly in demand. Furthermore, the development of healthcare infrastructure and investments by the government for cancer treatment at a rapid scale are augmenting the market. Driven by the growing need to address the rising prevalence of kidney cancer in the region, the Asia-Pacific kidney cancer therapeutics and diagnostics market has focused increasingly on improving access to treatment and enhancing treatment outcomes.

Latin America Kidney Cancer Therapeutics and Diagnostics Market Analysis

The aging population is a growth driver for the therapeutics and diagnostics market for kidney cancer in the region of Latin America and the Caribbean. There were 88.6 million people aged 60 years and more living in the region in 2022. This proportion comprised 13.4% of the total population, as cited by CEPAL. Such a proportion would increase to 16.5% by 2030. Age being one of the primary risk factors for kidney cancer, the geriatric population rising in Latin America also increases cases of kidney cancer. This population necessitates not only early detection but also treatment; it is putting further pressure on adopting advanced diagnostics and novel treatments like targeted and immunotherapies in Latin America. As healthcare organizations adjust to the population shift of increasingly aged citizens, this Latin America market for the therapy and diagnosis of kidney cancer can look forward to explosive growth over time, where such patients should improve.

Middle East and Africa Kidney Cancer Therapeutics and Diagnostics Market Analysis

One of the biggest growth drivers of the market for kidney cancer therapeutics and diagnostics remains the increasing incidence of kidney cancer in the Middle East and North Africa region. Industry reports indicate the rise of age-standardized incidence rate of kidney cancer in 17 countries of MENA in the period from 1990 to 2019. The high increase was noted in Saudi Arabia, Oman, and Lebanon-which are the most significant burdens faced by the region. Several factors have influenced the increase in cases of kidney cancer. These include changed lifestyle activities and rapid urbanization, which can be associated with increased risk factors in recent times, for example, smoking, obesity, and hypertension. Such an increase in incidence in cases of kidney cancer stimulates both early diagnosis and advanced treatments. This has led to increased adoption of high-end diagnostic technologies, including molecular imaging and biopsy techniques, as well as new therapies, such as targeted and immunotherapies, by healthcare systems within the region.

Competitive Landscape:

As per the kidney cancer therapeutics and diagnostics market trends, key players in the market are actively engaged in advancing treatments, enhancing diagnostics, and expanding their product portfolios to cater to the growing demand. Pharmaceutical companies are focusing on the development of targeted therapies and immunotherapies, such as immune checkpoint inhibitors and tyrosine kinase inhibitors, to improve patient outcomes in advanced stages of kidney cancer. These companies are also involved in conducting clinical trials to introduce novel drugs that target specific molecular pathways associated with renal cell carcinoma. Additionally, diagnostics companies are enhancing imaging technologies and introducing non-invasive diagnostic tools for early detection, which can significantly improve prognosis and treatment success. Strategic collaborations, partnerships, and acquisitions are common in the market, as companies aim to leverage each other’s expertise in cancer research and technological innovation. With the rising demand for personalized medicine, these players are also focusing on biomarkers and genetic profiling to provide tailored treatment plans for kidney cancer patients.

The report provides a comprehensive analysis of the competitive landscape in the kidney cancer therapeutics and diagnostics market with detailed profiles of all major companies, including:

- Bristol-Myers Squibb Company

- Exelixis Inc.

- Genentech Inc. (Roche Holding AG)

- Novartis AG

- Pfizer Inc

Latest News and Developments:

- September 2023: A leading global diagnostics company partnered with one of the largest South African companies to accelerate early diagnosis of kidney cancer. The partnership hopes to increase the usage of liquid biopsy and biomarker testing technologies among African countries to improve the rate of accuracy and speed of diagnosis of early kidney cancer, mainly in underserved areas.

- August 2023: A multinational pharmaceutical company launched a new immunotherapy medication for renal cell carcinoma (RCC) in the UAE. This is the first sign of increasing precision therapies in the Middle East for cancer, reflecting the evolution of treatments for RCC patients in the region.

- June 2023: A leading health technology company announced the successful installation of an innovative AI-based imaging technology for enhanced diagnosis of kidney cancer across the Middle East. This uses deep learning algorithms with an image system to make precise tumor detection for quicker and accurate diagnosis in various hospitals in the region.

Kidney Cancer Therapeutics and Diagnostics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Cancer Types Covered | Clear Cell RCC, Papillary RCC, Chromophobe RCC, Transitional Cell Carcinoma, Others |

| Applications Covered | Hospitals, Pharmaceutical Labs, Genomic Laboratories, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bristol-Myers Squibb Company, Exelixis Inc., Genentech Inc. (Roche Holding AG), Novartis AG, Pfizer Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the kidney cancer therapeutics and diagnostics market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global kidney cancer therapeutics and diagnostics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the kidney cancer therapeutics and diagnostics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The kidney cancer therapeutics and diagnostics market were valued at USD 5.37 Billion in 2024.

IMARC Group estimates the market to reach USD 9.24 Billion by 2033, exhibiting a CAGR of 5.90% during 2025-2033.

The key factors driving the kidney cancer therapeutics and diagnostics market include the rising incidence of kidney cancer, rapid advancements in targeted therapies and immunotherapies, growing demand for early detection through improved diagnostic technologies, increasing awareness about kidney cancer, and the development of personalized medicine for more effective treatments.

North America currently dominates the global market, driven by the increasing incidences of kidney cancer, rising research and development (R&D) expenditure, and growing geriatric population.

Some of the major players in the kidney cancer therapeutics and diagnostics market include Bristol-Myers Squibb Company, Exelixis Inc., Genentech Inc. (Roche Holding AG), Novartis AG, Pfizer Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)