Japan Semiconductor Device Market Size, Share, Trends and Forecast by Device Type, End Use Vertical, and Region, 2026-2034

Japan Semiconductor Device Market Size and Share:

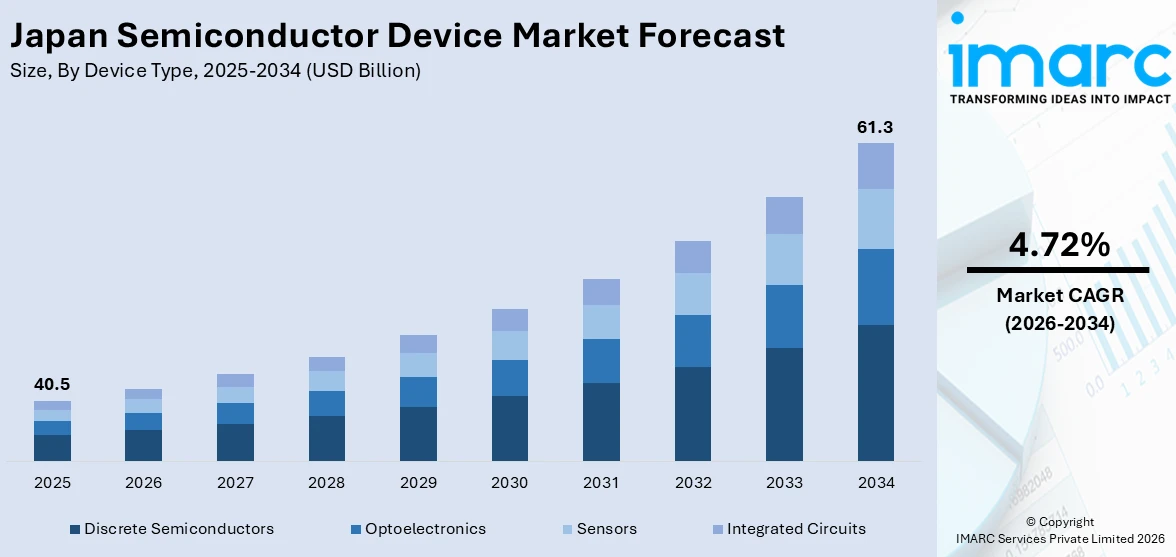

The Japan semiconductor device market size was valued at USD 40.5 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 61.3 Billion by 2034, exhibiting a CAGR of 4.72% from 2026-2034. The market is primarily driven by ongoing advancements in next-generation chip manufacturing, growing integration into automotive technologies, and rapid expansion into renewable energy systems, with increasing revenue and a commitment to carbon neutrality, solidifying its global leadership and supporting diverse applications in emerging industries.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034 |

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 40.5 Billion |

| Market Forecast in 2034 | USD 61.3 Billion |

| Market Growth Rate (2026-2034) | 4.72% |

As per the Japan semiconductor device market analysis, the region flourishes on continual advancements in manufacturing technologies, enabling efficient, miniaturized chip production. A strong focus on research and development (R&D) fosters innovation in design and fabrication, establishing Japan as a global industry leader. Government initiatives, including a USD 65 Billion plan announced by Prime Minister Shigeru Ishiba on November 11, 2024, aim to augment domestic chip and artificial intelligence (AI) industries through subsidies and financial incentives. Targeting chipmaker Rapidus and AI chip suppliers, the plan strengthens supply chain control and projects an economic impact of 160 Trillion yen. Additionally, growing demand for semiconductor devices in electric and autonomous vehicles drives the need for specialized chips for safety, connectivity, and energy efficiency.

To get more information on this market Request Sample

Besides this, the growing demand for semiconductors in artificial intelligence (AI), Internet of Things (IoT), and 5G networks is driving significant market growth. Japan's electronics and consumer device industries depend on advanced semiconductors to maintain global competitiveness. Strategic collaborations, such as the August 20, 2024, MOU between New York State and Hokkaido, strengthen semiconductor research and development (R&D) and workforce development through partnerships like NY CREATES and Rapidus. This collaboration enhances ties between Albany NanoTech Complex and Japan’s semiconductor initiatives, fostering innovation and economic growth. Moreover, semiconductors' critical role in renewable energy systems, including solar power and battery management, diversifies applications, further establishing Japan as a key player in the global semiconductor industry.

Japan Semiconductor Device Market Trends:

Advancement in Next-Generation Chip Manufacturing

Japan's semiconductor device market is advancing with next-generation technologies like extreme ultraviolet (EUV) lithography, enabling smaller, efficient, high-performance chips for applications in artificial intelligence (AI) and quantum computing. On October 29, 2024, FUJIFILM launched advanced EUV resist and developer, leveraging NTI technology to enhance semiconductor miniaturization and meet growing demand in 5G, AI, and autonomous driving. Production capabilities have been bolstered at facilities in Japan and South Korea, driving innovation and precision in chip manufacturing. Japan’s robust research and development (R&D) capabilities, coupled with collaborations with global semiconductor firms, refine processes and boost efficiency. These advancements solidify Japan’s global leadership, enabling the production of cutting-edge devices that meet stringent performance and energy efficiency standards for emerging applications.

Rapid Integration in Automotive Technologies

Advanced automotive technologies are impacting the Japan semiconductor device market outlook due to its increasing adoption of semiconductors. Semiconductors will play a key role in electric vehicles and autonomous driving systems as their rise contributes to safety, connectivity, and energy efficiency for the vehicle. Increasingly, Japanese automobile companies rely on domestic semiconductor companies for custom chips to cater to these applications, hence increasing the growth of the industry. The demand for power management solutions, sensor integration, and high-performance computing chips in EVs and smart vehicles is further expanding the market. This integration highlights the critical role of semiconductors in the development of Japan's automotive sector and its broader impact on global transportation trends.

Expansion into Renewable Energy Systems

According to the Japan semiconductor device market forecast, the region is increasingly focusing on renewable energy applications, including solar power systems and energy storage solutions. Semiconductors play a critical role in managing energy conversion and storage, particularly in battery systems and power inverters. The commitment to achieving carbon neutrality by 2050 is driving significant investments in renewable energy infrastructure, strengthening demand for high-performance, durable chips. On July 11, 2024, eight Japanese companies, including Sony and Mitsubishi Electric, announced a 5 Trillion yen investment by 2029 to expand semiconductor production for AI, EVs, and carbon reduction markets. These investments, supported by government funding, target image sensors, SiC power semiconductors, and advanced logic chips to revitalize Japan's industry and regain global competitiveness. Japan’s expertise in power semiconductors further aligns with global decarbonization efforts, diversifying applications and solidifying its role in the clean energy transition.

Japan Semiconductor Device Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Japan semiconductor device market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on device type and end use vertical.

Analysis by Device Type:

- Discrete Semiconductors

- Optoelectronics

- Sensors

- Integrated Circuits

- Analog

- Logic

- Memory

- Micro

Semiconductors are one of the most critical components in the market, leading to progress in different sectors. The country is also famous for its quality production of memory chips, microcontrollers, and power devices. Japanese companies, such as Toshiba and Renesas, are leaders in the global semiconductor market and focus on innovation in automotive, consumer electronics, and telecommunications sectors. This has been fueled by the increased adoption of technologies such as 5G, AI, and IoT, and is likely to further position Japan as a hub in semiconductor manufacturing.

Optoelectronics play a crucial role in Japan’s semiconductor device market, with products like LEDs, laser diodes, and optical sensors being integral to modern technologies. Japan's expertise in optoelectronics is evident in industries such as consumer electronics, automotive lighting, and communications. With companies like Sony and Sharp leading the way, Japan continues to drive innovation in display technologies, including OLEDs and quantum dot displays. The demand for energy-efficient lighting and high-performance displays fuels the growth of the optoelectronics sector, enhancing Japan's global competitiveness.

Sensors are another important segment in Japan's market, supporting diverse applications in automotive, robotics, healthcare, and industrial automation. Japan is famous for the precision and reliability of its sensors, products like image sensors, motion sensors, and environmental sensors are playing decisive roles in modern systems. The companies that have made significant contributions in this regard include Sony and Panasonic, which continue to benefit the growth of the sensor market, caused by growing applications in autonomous vehicles, wearable devices, and smart factories. Fast paced development of sensor technology also cements Japan's position at the top in the international semiconductor landscape.

Analysis by End Use Vertical:

Access the comprehensive market breakdown Request Sample

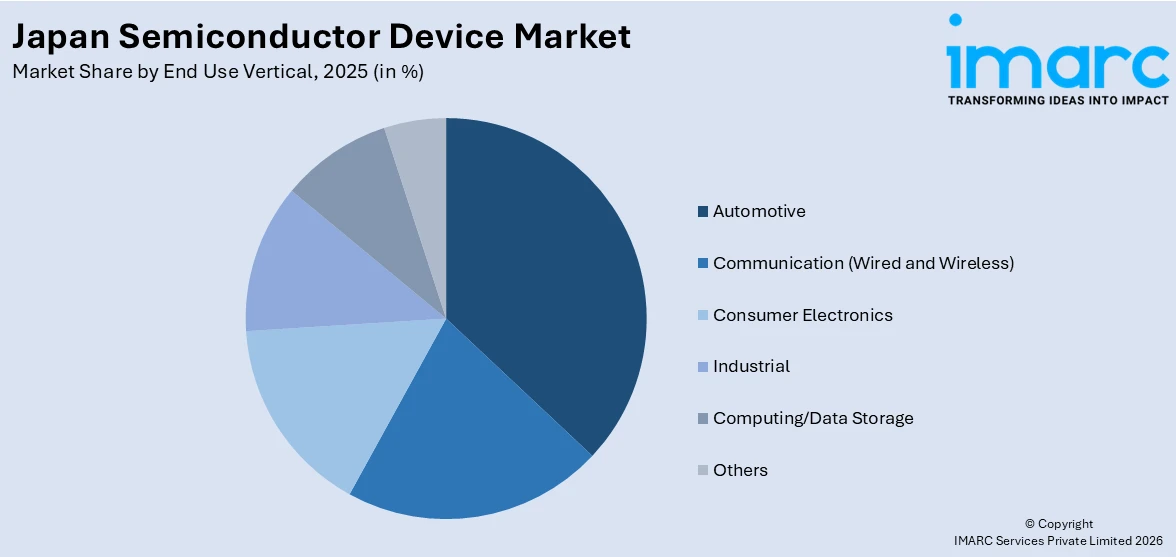

- Automotive

- Communication (Wired and Wireless)

- Consumer Electronics

- Industrial

- Computing/Data Storage

- Others

In the Japan market, the automotive sector plays a significant role, with semiconductors used in advanced driver assistance systems (ADAS), powertrain management, and electric vehicle (EV) technologies. Japanese companies like Renesas and Toyota are at the forefront of integrating semiconductors in automotive systems. The growing demand for electric vehicles and autonomous driving technologies is fueling the need for specialized chips, making Japan a key player in automotive semiconductor development and innovation.

The communication sector, both wired and wireless, is a major driver of Japan's semiconductor market. With the rise of 5G and data-intensive applications, semiconductor demand is growing for both wired infrastructure and wireless communication devices. Japanese companies such as Mitsubishi Electric and NTT are crucial suppliers, providing chips for telecom networks and devices like smartphones. Additionally, Japan's expertise in high-speed data transmission and network equipment supports its global competitiveness in communication technology.

Consumer electronics is a vital segment in the Japan Semiconductor Device Market, with semiconductors powering devices like gaming consoles, smartphones, tablets, and home appliances. Companies like Sony, Panasonic, and Sharp lead the development of advanced semiconductor technologies, including image sensors, processors, and memory chips. The increasing demand for smart devices, wearable tech, and high-definition displays drives the need for innovative semiconductor solutions, reinforcing Japan's position as a key hub for consumer electronics and semiconductor production.

Regional Analysis:

- Kanto Region

- Kansai/Kinki Region

- Central/ Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

The Kanto region houses Tokyo and its outskirts, accounting for the majority share of the Japanese semiconductor device market. The region is house to giants like Toshiba, Sony, and Renesas. Such high-end research institutions and robust supply chains further strengthen the region's power over the semiconductor business in the production and development of chips. Strong innovation in the region over electronics and communication helps further propel the regions forward and over the other competitors of semiconductor manufacturing.

The Kansai/Kinki region, consisting of Osaka, Kyoto, and Kobe, is another strategic area in Japan's semiconductor market. This region is well known for its high-end manufacturing capabilities and is home to large companies like Panasonic and Sharp. The Kansai region specializes in industrial electronics, consumer products, and energy-efficient solutions. Its strong emphasis on both semiconductor manufacturing and research, especially in optoelectronics and sensor technologies, drives the development of high-tech devices and innovation in consumer electronics.

The Central/Chubu region, which includes Nagoya, plays a significant role in the Japanese semiconductor market, particularly due to its strength in automotive and industrial manufacturing. Mitsubishi Electric and Denso are two companies that are leading the way in using semiconductors in automotive systems. The region also emphasizes robotics and industrial automation, making it important for the semiconductor demand in these sectors. Its manufacturing expertise and innovation make up a significant portion of Japan's overall semiconductor industry.

Kyushu-Okinawa plays an important role in Japan's semiconductor market for its strong manufacturing base and established technology clusters. Also known as the "Silicon Island," Kyushu hosts hundreds of semiconductor fabrication facilities and research centers, and innovation is nurtured through this concentration of advanced manufacturing technologies, with frequent interaction between academia and industry. In addition, its highly developed infrastructure and proximity to the global markets make it more crucial as a semiconductor hub for technological advancement and production efficiency in the Japanese semiconductor sector.

The Tohoku region promotes the growth of Japan's semiconductor industry, with a focus on cutting-edge research and manufacturing. It is also known for clean energy initiatives that support sustainable semiconductor production. Tohoku’s universities and research institutes are integral to developing innovative technologies, while its growing industrial parks host key players in the semiconductor value chain. The region's resilience and ongoing investments in infrastructure have positioned it as a critical area for Japan’s semiconductor production, especially in the wake of natural disasters.

The Chugoku region is gradually becoming a crucial player in the Japanese semiconductor market through the increasing number of small- and medium-sized enterprises specializing in electronic components. The region also enjoys its location, which aids in trading and exporting semiconductor products to international markets. Its interest in improving the supply chain for semiconductors and developing industry collaboration also indicates a role in supporting Japan's broader interests in technological self-sufficiency and international competitiveness in semiconductors.

Hokkaido promotes the semiconductor industry through its leading-edge research facilities and sustainability focus. The region is able to support the development of high-performance semiconductors, especially for renewable energy applications and automotive technologies. Furthermore, its cold climate is an additional advantage for energy-efficient data centers, which are part and parcel of semiconductor manufacturing. A commitment to innovation and its strategic focus on fostering partnerships between industry and academia reinforce Hokkaido's position in Japan's semiconductor ecosystem.

Specialized in the production of necessary material and components for chip making, Shikoku finds an important role in the market of semiconductors. It houses several major players involved in the production of substrates and other related semiconductor materials. Its focus on the R&D of future technologies, further supported by the government towards innovations, enhances its contribution towards the value chain of semiconductors. Shikoku's geographical advantages and its proximity to the major industrial regions in Japan make it a significant hub for semiconductor logistics and supply chain management.

Competitive Landscape:

The Japan semiconductor device market is highly competitive, featuring a blend of established global leaders and strong domestic players. Major international companies are significant competitors, while local firms hold substantial market shares. These companies are primarily driven by constant innovation in microchips, sensors, and memory devices. The competition is fueled by technological advancements in 5G, artificial intelligence (AI), and Internet of Things (IoT) applications. Japan's growing focus on high-quality manufacturing, precision, and automation is also strengthening its position in the market. Apart from this, challenges such as supply chain disruptions and geopolitical tensions impact market dynamics, prompting firms to adopt strategies like collaboration and strategic acquisitions.

The report provides a comprehensive analysis of the competitive landscape in the Japan semiconductor device market with detailed profiles of all major companies.

Latest News and Developments:

- November 20, 2024: Mitsubishi Electric announced a 10 Billion yen investment to build a new facility in Fukuoka Prefecture for assembling and inspecting power semiconductor modules, scheduled to begin operations in October 2026. The plant will streamline production and improve productivity with automation. It aims to meet increasing market demand for power semiconductors, supporting applications in electric vehicles, renewable energy, and industrial equipment.

- June 27, 2024: Axcelis Technologies announced the opening of two new service offices in Chitose, Hokkaido, and Kumamoto, Kyushu, in June 2024, to support its growing customer base in Japan. The company aims to expand its market share by providing innovative ion implantation solutions for semiconductor applications. The new offices will offer localized support for Purion ion implant equipment, serving Silicon Carbide (SiC) as well as both Silicon (Si) semiconductor power device customers. This expansion strengthens Axcelis' position in Japan's advanced logic production market.

Japan Semiconductor Device Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Device Types Covered |

|

| End Use Verticals Covered | Automotive, Communication (Wired and Wireless), Consumer Electronics, Industrial, Computing/Data Storage, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan semiconductor device market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan semiconductor device market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan semiconductor device industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

A semiconductor device refers to an electronic component made from semiconductor materials, such as silicon or gallium arsenide, that control electrical current. Applications include microprocessors, memory chips, sensors, and power devices used in computers, smartphones, automotive systems, renewable energy solutions, and advanced technologies like artificial intelligence and 5G networks.

The Japan semiconductor device market was valued at USD 40.5 Billion in 2025.

IMARC estimates the Japan semiconductor device market to exhibit a CAGR of 4.72% during 2026-2034.

Key drivers of the Japan market include rapid advancements in chip manufacturing technologies, rising demand in AI, IoT, 5G, and EV applications, and significant government investments. Expanding use in renewable energy systems and strategic industry collaborations is further fueling innovation and market expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)