Japan Medical Device Cleaning Market Size, Share, Trends and Forecast by Device, EPA Classification, Technique, End User, and Region, 2026-2034

Japan Medical Device Cleaning Market Size and Share:

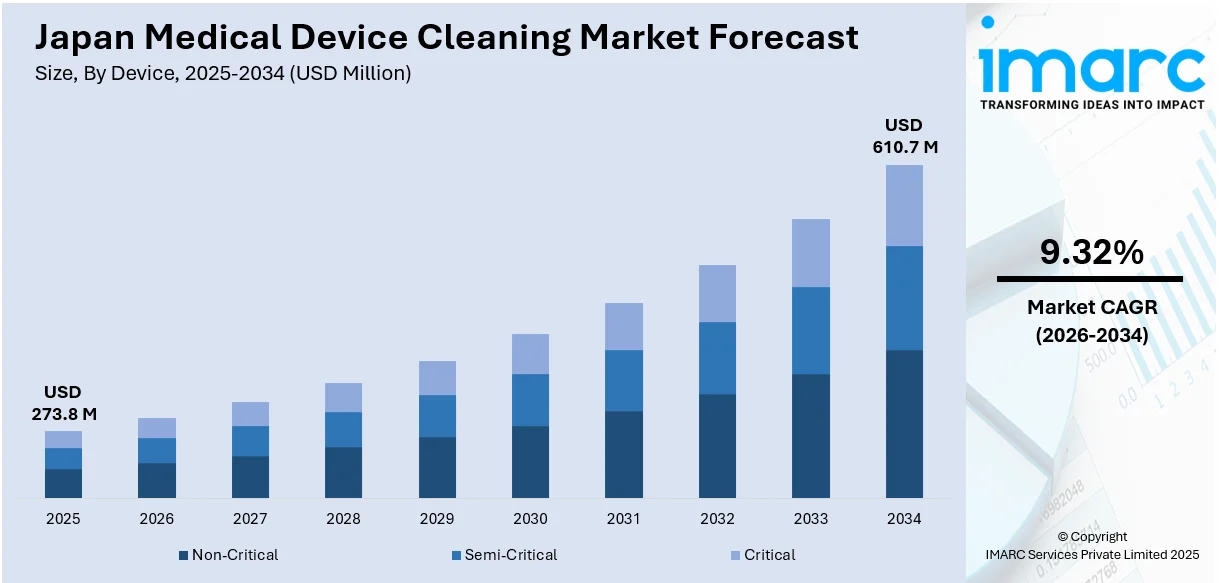

The Japan medical device cleaning market size was valued at USD 273.8 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 610.7 Million by 2034, exhibiting a CAGR of 9.32% from 2026-2034. The market is driven by the increasing need for infection control, rising adoption of reusable medical instruments, and stringent regulatory standards ensuring patient safety. Technological advancements in cleaning solutions, improved healthcare infrastructure, and the growing awareness about hygiene practices among healthcare professionals are offering a favorable market outlook in Japan.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034 |

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 273.8 Million |

| Market Forecast in 2034 | USD 610.7 Million |

| Market Growth Rate (2026-2034) | 9.32% |

The rising prevalence of healthcare-associated infections (HAIs) is driving the need for stringent cleaning protocols in medical facilities. Effective cleaning solutions are essential to minimize infection risks and ensure the safety of both patients and healthcare professionals. The growing aging population in Japan is driving the demand for medical services, leading to a higher usage of medical devices that require regular cleaning and maintenance. Furthermore, the increasing adoption of reusable medical instruments, such as endoscopes and surgical tools, is catalyzing the demand for efficient cleaning processes. Proper cleaning ensures these devices remain functional and contamination-free for repeated use. In addition, strict infection control regulations set by Japanese healthcare authorities emphasize the need for high-quality cleaning practices. Hospitals and clinics are adopting advanced cleaning methods to meet these compliance standards and improve patient outcomes.

To get more information on this market Request Sample

Moreover, continuous innovation in cleaning technologies, including ultrasonic cleaners and enzymatic detergents, enhances the efficiency and effectiveness of the cleaning process. These advancements support the growing demand for superior medical device cleaning solutions. The integration of automated cleaning systems, such as robotic washers and ultrasonic cleaners, is streamlining cleaning operations in hospitals and clinics. These systems offer greater precision and consistency, reducing human error and enhancing the overall efficiency of cleaning protocols. Apart from this, the rising number of surgical interventions across healthcare facilities are driving the demand for proper cleaning of surgical tools and equipment. Advanced cleaning solutions are necessary to prevent contamination, particularly with the rise in complex, minimally invasive, and robotic-assisted surgeries. Additionally, the increasing environmental concerns are promoting the adoption of eco-friendly cleaning agents and energy-efficient cleaning systems in healthcare settings. These sustainable practices are not only reducing the ecological impact of medical device cleaning but are also aligning with green healthcare initiatives.

Japan Medical Device Cleaning Market Trends:

Rising Demand for Hospital Supplies

The hospital supplies market in Japan is expected to exhibit a growth rate (CAGR) of 6.30% between 2024 and 2032, as per the IMARC Group. The increasing requirement for hospital supplies in Japan is driving the demand for cleaning solutions for medical devices. As healthcare facilities increase their inventory of medical devices to cater to rising patient volumes and advanced procedures, the requirement for effective cleaning systems intensifies. A wider variety of equipment, such as surgical tools, diagnostic apparatus, and patient care devices, requires thorough cleaning procedures to meet strict hygiene and safety regulations. Additionally, by incorporating reusable devices as a financially viable and eco-friendly option, healthcare providers are emphasizing the use of advanced cleaning technologies to preserve the effectiveness and cleanliness of these materials. This trend is reinforced by healthcare institutions prioritizing the implementation of innovative cleaning methods designed for various device types, guaranteeing peak performance while reducing infection risks.

Growing Geriatric Population

As stated by the United Nations Population Fund (UNFPA), Japan's total population in 2024 will be 122.6 million, with 30% of individuals being 65 years old or above. Japan's elderly population is leading to a greater demand for enhanced healthcare services, consequently raising the need for medical devices that require frequent cleaning. Elderly people frequently need continuous medical attention that includes different diagnostic equipment, surgical tools, and treatment devices. Such medical interactions require strict cleaning protocols to guarantee the safety and efficacy of devices employed in caring for at-risk patients. As the healthcare system adjusts to handle the rising need for geriatric care, there is a greater focus on reusable medical devices, which necessitate comprehensive cleaning to avoid infections and ensure functionality. Additionally, the increase in age-associated ailments like cardiovascular diseases, diabetes, and orthopedic problems is resulting in a higher frequency of medical interventions and hospital visits, which is driving the need for dependable cleaning and sterilization technologies. This demographic shift is greatly influencing the market, promoting innovation and the adoption of cleaning systems designed to address the demands of elder care in healthcare settings.

Increased Healthcare Expenditure

Rising healthcare expenditure in Japan, aligned with the "Japan Vision: Health Care 2035," is bolstering the market growth. This vision focuses on creating a sustainable and efficient healthcare system that prioritizes quality, innovation, and global health leadership. Increased investments in modernizing healthcare infrastructure are enabling the adoption of advanced cleaning technologies and practices, ensuring compliance with stringent infection prevention standards. The emphasis on value-based care and technology integration within the vision encourages the use of automated cleaning systems, innovative detergents, and eco-friendly solutions. Additionally, efforts to address regional disparities and promote health equity are fostering widespread implementation of robust cleaning protocols across various healthcare settings. These initiatives, coupled with higher budgets, are supporting training programs and awareness campaigns, reinforcing the importance of effective cleaning practices.

Japan Medical Device Cleaning Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Japan medical device cleaning market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on device, EPA classification, technique, and end user.

Analysis by Device:

- Non-Critical

- Semi-Critical

- Critical

The non-critical category comprises stethoscopes, blood pressure monitors, and thermometers, which necessitate surface cleaning and basic disinfection. These devices touch unbroken skin and carry a reduced risk of spreading infections. The emphasis on upholding fundamental hygiene in healthcare environments is increasing the need for efficient cleaning supplies and disinfection techniques designed for non-critical apparatus.

Semi-critical consists of endoscopes, dental instruments, and respiratory therapy equipment, which contact mucous membranes or non-intact skin. These devices require high-level disinfection to ensure safety and prevent cross-contamination. The increasing use of minimally invasive procedures and diagnostic tools is catalyzing the demand for advanced cleaning solutions designed for semi-critical devices.

The critical segment includes surgical tools, implants, and catheters that interact with sterile body tissues or blood, necessitating thorough cleaning and sterilization. If not cleaned properly, these devices present the greatest risk of infection. The strict regulatory standards for sterilization and the increasing volume of surgical procedures are driving the demand for specialized cleaning technologies and sterilization equipment for essential devices.

Analysis by EPA Classification:

- High Level

- Intermediate Level

- Low Level

High-level encompasses disinfectants formulated to eradicate all microorganisms, including bacterial spores, when applied correctly. It is primarily used for sterilizing critical and semi-critical devices like surgical instruments and endoscopes. The rising adoption of high-level disinfection in healthcare facilities reflects the need for advanced solutions to maintain sterility and comply with stringent infection control standards.

The intermediate-level segment is effective against a majority of bacteria, viruses, and fungi, but it does not eliminate bacterial spores. It is frequently utilized for non-critical and certain semi-critical devices, such as stethoscopes and non-invasive instruments. The growing focus on stopping surface-level contamination in patient care settings is increasing the need for these disinfectants in hospitals and clinics.

The low-level segment is intended for surfaces and equipment that touch unbroken skin, like hospital beds and furniture. It focuses on prevalent bacteria and viruses, rendering it fit for regular cleaning in healthcare environments. The need for low-level disinfection products is increasing as healthcare institutions emphasize sustaining fundamental cleanliness in non-critical zones.

Analysis by Technique:

- Cleaning

- Disinfection

- Sterilization

Cleaning entails the elimination of noticeable dirt, organic materials, and waste from medical instruments and surfaces. It is the initial stage in the decontamination procedure, confirming that devices are devoid of contaminants prior to additional processing. Manual cleaning, automatic washers, and ultrasonic cleaning systems are frequently employed, and the rising usage of reusable devices is heightening the use of effective cleaning solutions.

Disinfection removes the majority of microorganisms, except for bacterial spores, and is used on semi-critical and non-critical instruments like thermometers and respiratory devices. Disinfectants at both high and intermediate levels are commonly utilized in this procedure. The growing focus on avoiding cross-contamination in medical settings is encouraging the utilization of specialized disinfectants designed for various equipment types.

Sterilization guarantees the total elimination of all microorganisms, including bacterial spores, making it essential for instruments that contact sterile body areas, like surgical tools and implants. Methods such as autoclaving, ethylene oxide sterilization, and hydrogen peroxide plasma are commonly utilized. The increase in surgical operations and strict regulatory guidelines for infection control are driving the need for advanced sterilization technologies.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

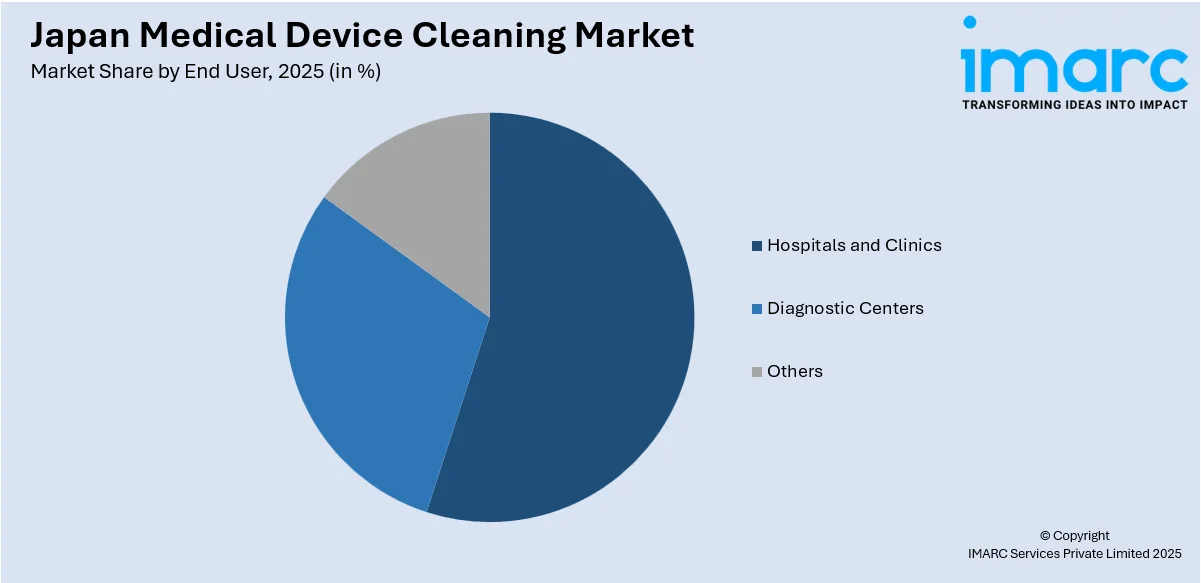

- Hospitals and Clinics

- Diagnostic Centers

- Others

Hospitals and clinics are crucial segment in the market due to the high volume of patient care and diverse range of medical devices used. Ranging from surgical tools to diagnostic equipment, maintaining stringent cleaning protocols is essential to prevent infections and ensure patient safety. This segment requires comprehensive cleaning, disinfection, and sterilization systems tailored to various device types.

Diagnostic centers depend significantly on clean and accurate equipment, including imaging devices and lab instruments, to obtain reliable results. Cleaning products created for diagnostic equipment are highly sought after to ensure proper operation and avoid contamination while testing. The growing application of advanced diagnostic technologies is intensifying the need for specialized cleaning techniques in this area.

Others include long-term care facilities, ambulatory surgical centers, and home healthcare settings. These environments require cleaning solutions suited for lower volumes of equipment but with equally rigorous standards. The rising focus on infection prevention in non-hospital settings is driving the adoption of compact and user-friendly cleaning and disinfection products in this segment.

Regional Analysis:

- Kanto Region

- Kansai/Kinki Region

- Central/ Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

The Kanto region, home to Tokyo and numerous major healthcare facilities, represents a significant share of the medical device cleaning market. Advanced hospitals and specialized clinics in this area drive the demand for high-quality cleaning solutions, particularly for critical devices used in surgeries and complex medical procedures.

With prominent medical hubs like Osaka and Kyoto, the Kansai region contributes substantially to the market. The region’s focus on cutting-edge medical research and healthcare services fosters the adoption of advanced cleaning, disinfection, and sterilization technologies for both critical and semi-critical devices.

The Central/Chubu region, known for its technological expertise and manufacturing excellence, supports the medical device cleaning market by promoting innovative solutions for healthcare facilities. The presence of leading medical institutions and diagnostic centers in cities like Nagoya increases the demand for reliable cleaning systems.

The Kyushu-Okinawa area is developing its healthcare infrastructure, emphasizing the delivery of extensive medical services to the elderly population. This fuels the need for efficient cleaning solutions in hospitals, clinics, and diagnostic centers within this area, maintaining high hygiene standards.

The Tohoku area, focusing on local healthcare services, demonstrates a consistent need for cleaning products for medical devices, especially for non-critical and semi-critical equipment. Healthcare facilities and diagnostic centers in this region need affordable and effective cleaning solutions to satisfy their requirements.

The Chugoku area, noted for its smaller yet vital healthcare establishments, depends on cleaning products that are effective and straightforward to use. The demand in this market is driven by the necessity for dependable disinfection and sterilization methods in general healthcare environments.

The Hokkaido region, with its unique geographic and climatic challenges, requires specialized cleaning solutions suited for healthcare facilities operating in colder environments. Demand is particularly strong for durable and efficient cleaning systems that can handle diverse medical devices.

The Shikoku area, featuring its smaller healthcare systems, emphasizes providing accessible and sanitary medical services. There is a significant demand for efficient and adaptable cleaning solutions, serving the requirements of hospitals, clinics, and smaller diagnostic centers in the area.

Competitive Landscape:

Major players in the market are prioritizing the creation of innovative cleaning solutions to address the increasing need for effective decontamination methods. They are dedicating resources to research operations to generate innovative products that serve multiple device types, including critical, semi-critical, and non-critical instruments. Companies are also enhancing their distribution networks to ensure the availability of cleaning solutions across healthcare facilities. Collaborations with hospitals and diagnostic centers allow them to understand particular needs and customize their offerings. Additionally, they are aiming for strategic purchases to improve their technological skills and expand their range of products. By acquiring innovative companies specializing in advanced reprocessing solutions, these players aim to enhance their market position, drive innovation, and improve infection control standards. In November 2023, HOYA Corporation, a prominent Japanese medical technology firm, purchased the remaining 49% of shares in WASSENBURG Medical B.V., a Dutch expert in endoscope reprocessing solutions. The goal of the acquisition is to improve innovation in endoscope cleaning, promoting standards for infection-free patient care.

The report provides a comprehensive analysis of the competitive landscape in the Japan medical device cleaning market with detailed profiles of all major companies, including:

- ASP Japan

- Belimed AG (Metall Zug)

- Getinge

- STERIS Japan Inc.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News and Developments:

- July 2024: Medical Bear, a sterilization service provider in Japan, partnered with Getinge to integrate the T-DOC sterile supply management system, boosting workflow efficiency by 9% and reducing process steps by 27%. This digital transformation supports over 100 hospitals and clinics, setting a new standard for sterilization management in Japan's healthcare sector.

- May 2024: ASP Japan secured an exclusive sales contract with PENTAX Medical to distribute the PlasmaTYPHOON™+ and AquaTYPHOON™ systems in Japan. These innovative solutions enhance endoscope reprocessing by improving drying, storage, and pre-cleaning efficiency, reducing infection risks and consumable usage. This collaboration aims to elevate Japan's medical cleaning standards through advanced technology.

Japan Medical Device Cleaning Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Devices Covered | Non-Critical, Semi-Critical, Critical |

| EPA Classifications Covered | High Level, Intermediate Level, Low Level |

| Techniques Covered | Cleaning, Disinfection, Sterilization |

| End Users Covered | Hospitals and Clinics, Diagnostic Centers, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | ASP Japan, Belimed AG (Metall Zug), Getinge, STERIS Japan Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan medical device cleaning market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan medical device cleaning market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan medical device cleaning industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

Medical device cleaning involves removing contaminants like blood, tissue, and microorganisms from instruments to ensure safety and functionality. It is a crucial step before sterilization or disinfection, employing methods, such as manual scrubbing, ultrasonic cleaners, and enzymatic detergents. Proper cleaning minimizes infection risks and adheres to regulatory standards, safeguarding patient health and maintaining device integrity.

The Japan medical device cleaning market was valued at USD 273.8 Million in 2025.

IMARC estimates the Japan medical device cleaning market to exhibit a CAGR of 9.32% during 2026-2034.

The Japan medical device cleaning market is driven by the rising prevalence of healthcare-associated infections, stringent regulatory requirements for infection control, and the growing use of advanced reusable medical devices. Increased healthcare spending, advancements in cleaning technologies, and the emphasis on patient safety further encourage adoption, making cleaning solutions essential for maintaining hygiene and compliance in healthcare settings.

Some of the major players in the Japan medical device cleaning market include ASP Japan, Belimed AG (Metall Zug), Getinge, STERIS Japan Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)