Insect Growth Regulators Market Size, Share, Trends and Forecast by Product, Form, Application, and Region, 2025-2033

Insect Growth Regulators Market Size and Share:

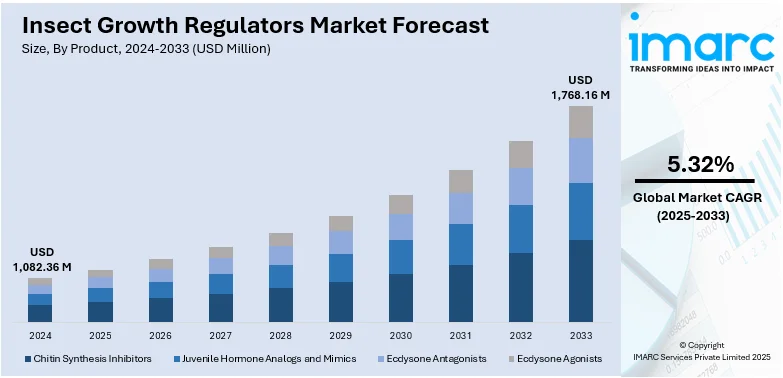

The global insect growth regulators market size was valued at USD 1,082.36 Million in 2024. Looking forward, IMARC Group estimates the market to reach USD 1,768.16 Million by 2033, exhibiting a CAGR of 5.32% during 2025-2033. North America currently dominates the market, holding a significant market share of over 39.6% in 2024. The strict pesticide regulations, rising integrated pest management (IPM) adoption, increasing insect resistance, growing organic farming, urban pest control demand, and technological advancements in eco-friendly biopesticides for agriculture and public health applications are some of the major factors fueling the insect growth regulators market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 1,082.36 Million |

|

Market Forecast in 2033

|

USD 1,768.16 Million |

| Market Growth Rate (2025-2033) | 5.32% |

The insect growth regulators (IGR) market is driven by increasing demand for sustainable and eco-friendly pest control solutions across agriculture, public health, and commercial sectors. Rising concerns over insect resistance to conventional pesticides and stricter regulations on chemical insecticides are boosting IGR adoption. The market finds additional support from increasing IPM program adoption along with growing organic farming trends. Bio-based insect growth regulators receive enhancements through technological development to improve efficiency at lower environmental costs. Additionally, rising urban pest control initiatives, particularly for mosquitoes, fleas, and cockroaches, contribute to demand. Increased awareness about sustainable pest control methods and government support for biopesticides are further driving market expansion worldwide.

The insect growth regulators (IGR) market in the United States is driven by stringent pesticide regulations, increasing insect resistance to conventional chemicals, and a growing demand for eco-friendly pest control solutions. The adoption of integrated pest management (IPM) programs in agriculture and public health sectors supports market expansion. Rising urban pest control efforts, particularly for mosquitoes, fleas, and cockroaches, further fuel demand. Additionally, the expansion of organic farming and biopesticide innovations enhance IGR adoption. Government support for sustainable pest control methods and technological advancements in bio-based formulations contribute to the market’s growth, making the U.S. a key player in IGR development. For instance, in September 2024, Syngenta Biologicals and Provivi announced a partnership to create and market innovative pheromone-based biological solutions aimed at efficiently and safely managing harmful pests in corn and rice—two crops that are a major food source for 3.5 billion people worldwide.

Insect Growth Regulators Market Trends:

Increasing Insect Resistance to Conventional Pesticides

Insect resistance to traditional chemical pesticides is a major driver of the insect growth regulators (IGR) market. Overuse of conventional insecticides has led to resistant pest populations, reducing the effectiveness of standard treatments. IGRs offer an alternative by disrupting insect development rather than targeting the nervous system, making them a vital tool in resistance management. This has encouraged farmers, pest control professionals, and regulatory bodies to adopt IGRs as part of integrated pest management (IPM) programs. As resistance issues continue to grow, the demand for IGR-based solutions is expected to rise significantly across agriculture, urban pest control, and forestry. For instance, in September 2024, the Horizon Europe pest management project, IPMorama, was inaugurated. This year, it will start testing and conducting scientific experiments for pest management. It will establish a comprehensive plan for the upcoming year and will explore the next generation of integrated pest management (IPM) in agriculture. It also seeks to transform this sector in European agriculture.

Stringent Regulations on Chemical Pesticides

Tighter environmental and health regulations on chemical pesticides are driving the demand for safer alternatives like IGRs which is creating a positive insect growth regulators market outlook. Regulatory agencies, such as the U.S. Environmental Protection Agency (EPA) and the European Food Safety Authority (EFSA), are imposing restrictions on hazardous insecticides due to their toxic effects on humans, wildlife, and pollinators. In response, pest control industries are increasingly shifting toward IGRs, which have a more targeted action and lower environmental impact. The push for sustainable agriculture and eco-friendly pest management solutions is further accelerating the adoption of IGRs as a preferred method for long-term insect control. For instance, in August 2024, the Union Government introduced the AI-driven National Pest Surveillance System (NPSS) that enables farmers to reach out to agricultural scientists and specialists for pest control assistance via their phones. Inaugurating the program, Agriculture Minister Shivraj Singh Chouhan stated that the purpose of NPSS is to lessen farmers' reliance on pesticide sellers and foster a scientific mindset among them regarding pest control. NPSS will utilize AI tools to examine the most recent data on pests to assist farmers and specialists in pest management and control.

Growth of Integrated Pest Management (IPM) Programs

The rising adoption of integrated pest management (IPM) strategies is a key factor driving the IGR market. IPM emphasizes the use of multiple pest control methods, including biological control, habitat modification, and chemical control with minimal environmental impact. IGRs play a crucial role in IPM programs due to their selective action against insect pests without harming beneficial organisms. Governments and agricultural organizations are actively promoting IPM practices to reduce reliance on chemical pesticides, thereby increasing insect growth regulators demand. As sustainable farming practices gain momentum, IGR usage is expected to grow across various agricultural and commercial applications. For instance, in September 2023, ADAS, NFU, SRUC, and Voluntary Initiative (VI) developed a free IPM Planning Tool to assist farmers in developing crop-specific IPM management plans, as IPM planning is now a paid activity under the Sustainable Farming Incentive (SFI).

Insect Growth Regulators Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global insect growth regulators market, along with forecasts at the global, regional, and country levels from 2025-2033. The market has been categorized based on product, form, and application.

Analysis by Product:

- Chitin Synthesis Inhibitors

- Juvenile Hormone Analogs and Mimics

- Ecdysone Antagonists

- Ecdysone Agonists

Chitin synthesis inhibitors stand as the largest product in 2024, holding around 41.2% of the market due to their high effectiveness in disrupting insect exoskeleton formation, leading to pest mortality. They are widely used in agriculture, forestry, and public health for controlling pests like mosquitoes, beetles, and caterpillars. Their selective mode of action ensures minimal impact on non-target organisms, making them environmentally friendly. Additionally, they help combat insect resistance to conventional pesticides. Regulatory support for safer pest control solutions and increasing demand for sustainable agricultural practices further drive their adoption. Their versatility and efficiency make them the dominant segment in the IGR market.

Analysis by Form:

- Aerosol

- Liquid

- Bait

Liquid leads the market with around 46.6% of market share in 2024 due to its ease of application, superior coverage, and effectiveness in pest control. They are widely used in agriculture, commercial pest control, and public health programs for treating large areas efficiently. Liquid IGRs can be applied as sprays, drenches, or mixed with other pesticides, enhancing their versatility. Their rapid absorption and consistent distribution improve pest management outcomes. Additionally, liquid formulations are preferred for mosquito control and stored product pest treatments. Growing demand for integrated pest management (IPM) and environmentally friendly solutions further boosts their dominance in the market.

Analysis by Application:

- Agriculture

- Residential

- Commercial

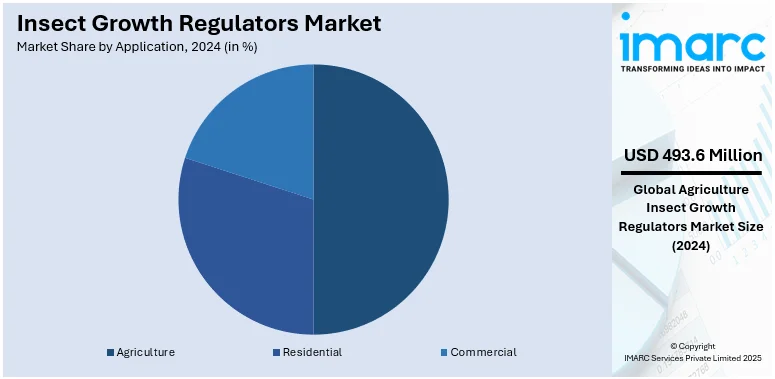

Agriculture leads the market with around 45.6% of the market share in 2024 due to the rising need for effective pest control in crop production. IGRs help manage destructive pests like aphids, whiteflies, and caterpillars while minimizing environmental impact and resistance issues associated with conventional insecticides. Farmers prefer IGRs for their targeted action, reducing harm to beneficial insects and promoting sustainable farming. Increasing global food demand, stringent pesticide regulations, and the adoption of integrated pest management (IPM) practices further drive their use. Additionally, advancements in bio-based IGR formulations and expanding agricultural activities, especially in developing regions, contribute to market growth.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 39.6%. The insect growth regulators (IGR) market in North America is driven by increasing demand for sustainable pest control solutions in agriculture, public health, and commercial pest management. Strict regulations on conventional pesticides and a growing preference for eco-friendly alternatives support IGR adoption. Expanding integrated pest management (IPM) programs and rising awareness of insect resistance drive market growth. The agricultural sector relies on IGRs for protecting high-value crops, while urban pest control programs use them against mosquitoes, fleas, and cockroaches. Technological advancements, rising organic farming practices, and government initiatives promoting biopesticides further fuel the demand for IGRs in the region.

Key Regional Takeaways:

United States Insect Growth Regulators Market Analysis

In 2024, the United States accounted for over 87.30% of the insect growth regulators market in North America. The United States insect growth regulators market is experiencing steady growth due to rising concerns over pest management in agricultural and urban settings. Increased adoption of integrated pest management (IPM) strategies and the demand for environmentally friendly pest control solutions are key drivers. Regulatory policies promoting safer alternatives to conventional pesticides further support market expansion. The agriculture sector remains a major consumer, with applications in stored product protection and crop protection. Additionally, increased use in residential, commercial, and industrial settings contributes to market growth. Government funding is also playing a crucial role in advancing pest management solutions. The National Institute of Food and Agriculture states that the amount available for the Crop Protection and Pest Management (CPPM) program’s ARDP grants in FY 2024 is approximately USD 4.8 Million. This funding supports research and innovation in pest control strategies, encouraging the development of safer and more effective insect growth regulators. Advancements in formulation technologies, including aerosol and bait-based products, further enhance product efficiency and adoption, driving overall market expansion.

Europe Insect Growth Regulators Market Analysis

The Europe insect growth regulators market is witnessing growth, driven by stringent regulations on chemical pesticides and a growing preference for biological pest control methods. Increased awareness regarding the harmful effects of synthetic pesticides has led to higher adoption in agriculture, horticulture, and urban pest management. The market benefits from ongoing research and development efforts aimed at improving product efficiency and safety. Expanding organic farming practices and sustainable pest control strategies further support demand. The European Court of Auditors states that the Commission has set a target of having 25% of the EU’s agricultural land organically farmed by 2030. This initiative is expected to boost the adoption of environmentally friendly pest management solutions, including insect growth regulators, as farmers seek alternatives to chemical pesticides. With regulatory frameworks encouraging reduced chemical pesticide use, market players are focusing on innovative solutions to cater to diverse applications, including stored grain protection and animal health.

Asia Pacific Insect Growth Regulators Market Analysis

The insect growth regulators market in Asia Pacific is expanding due to rising agricultural production and increasing pest-related challenges. The shift toward sustainable pest management practices and restrictions on chemical pesticides is driving demand. The agriculture sector remains a key consumer, particularly for crop protection and stored grain preservation. As projected by the Organization for Economic Co-operation and Development, India along with Southeast Asian nations is anticipated to contribute to 31% of the increase in global consumption by 2033. This significant rise in food demand is expected to accelerate the need for effective pest control solutions, further supporting the adoption of insect growth regulators. Growing urbanization has also boosted demand for residential and industrial pest control. Additionally, technological advancements and increased awareness about the benefits of insect growth regulators contribute to market expansion. Emerging economies in the region are witnessing increased adoption, driven by government initiatives promoting integrated pest management.

Latin America Insect Growth Regulators Market Analysis

The Latin America insect growth regulators market is growing due to increasing agricultural activities and pest management concerns. The demand for eco-friendly pest control solutions is rising, supported by regulatory efforts to limit chemical pesticide use. The market is driven by applications in crop protection, stored product management, and livestock care. As per the United States Department of Agriculture, the 2024 federal budget of Mexico for the Secretariat of Agriculture and Rural Development (SADER) stands at USD 4.3 Billion, showing a five percent rise from the 2023 budget. This rise in agricultural funding is expected to support advancements in pest management solutions, including the adoption of insect growth regulators. Expanding urban areas also contributes to the demand for commercial and residential pest control. Research and innovation in biological pest control methods are further enhancing market growth.

Middle East and Africa Insect Growth Regulators Market Analysis

The insect growth regulators market in the Middle East and Africa is expanding, driven by growing concerns over pest control in agriculture and public health. The need for sustainable solutions has increased due to regulatory restrictions on chemical pesticides. Adoption is rising in stored grain protection, livestock care, and urban pest management. Saudi Arabia’s agriculture market size reached USD 130 Billion in 2024, and according to IMARC Group, it is expected to grow to USD 207 Billion by 2033, with a CAGR of 5.28% during 2025-2033. This rapid expansion in the agricultural sector is likely to drive the demand for effective pest management solutions, including insect growth regulators, as sustainable farming practices gain traction.

Competitive Landscape:

The insect growth regulators (IGR) market is highly competitive, driven by increasing demand for effective pest control in agriculture, public health, and commercial applications. Key players include Bayer AG, Syngenta, BASF SE, Corteva Agriscience, and Sumitomo Chemical. The market is divided into chitin synthesis blockers, juvenile hormone mimics, and anti-juvenile hormone substances, with significant application areas in agricultural and residential pest management. North America and Europe lead due to strict pest management regulations, while Asia-Pacific sees rapid growth with expanding agricultural activities. Growing concerns over insect resistance, environmental impact, and regulatory approvals shape market dynamics, fostering innovation in eco-friendly and biodegradable IGR formulations.

The report provides a comprehensive analysis of the competitive landscape in the insect growth regulators market with detailed profiles of all major companies, including:

- BASF SE

- Central Life Science (Central Garden & Pet Company)

- Control Solutions Inc (China National Chemical Corporation)

- Dow Inc

- Nufarm Limited

- OHP Inc. (AMVAC Chemical Corporation)

- Russell IPM Ltd

- Sumitomo Chemical Co. Ltd.

- Syngenta AG

Latest News and Developments:

- March 2024: Syngenta introduced the new Advion® Trio cockroach gel bait to assist pest management professionals (PMPs) in controlling cockroaches throughout all phases of their life cycle. Utilizing the synergistic effects of three active components with varying mechanisms, including two insect growth regulators (IGRs), Advion Trio aims to provide enhanced management of challenging cockroach infestations.

- February 2025: Control Solutions Inc. (CSI) introduced the Precision Delivery System (PDS) with Doxem Precise, a dry flowable bait for cockroach control. Designed for precision application, it provides long-lasting protection in extreme conditions. Effective for over six months, it reduced callbacks and was ideal for commercial kitchens and food-handling environments.

- January 2025: Sumitomo Chemical fully acquired Philagro in France and planned to acquire Kenogard in Spain by fiscal year 2024. The move aimed to expand its European crop protection business, integrate operations, and explore M&A opportunities. The company sought to enhance its biorationals portfolio and double its regional sales by 2030.

- March 2022: FMC India, a chemicals firm located in India, introduced Corprima, an insect growth regulator utilizing Rynaxypyr technology to provide enhanced crop protection.

Insect Growth Regulators Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Chitin Synthesis Inhibitors, Juvenile Hormone Analogs and Mimics, Ecdysone Antagonists, Ecdysone Agonists |

| Forms Covered | Aerosol, Liquid, Bait |

| Applications Covered | Agriculture, Residential, Commercial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BASF SE, Central Life Science (Central Garden & Pet Company), Control Solutions Inc (China National Chemical Corporation), Dow Inc, Nufarm Limited, OHP Inc. (AMVAC Chemical Corporation), Russell IPM Ltd, Sumitomo Chemical Co. Ltd. and Syngenta AG |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the insect growth regulators market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global insect growth regulators market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the insect growth regulators industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The insect growth regulators market was valued at USD 1,082.36 Million in 2024.

The insect growth regulators market is projected to exhibit a CAGR of 5.32% during 2025-2033, reaching a value of USD 1,768.16 Million by 2033.

The insect growth regulators market is driven by increasing insect resistance to conventional pesticides, stringent regulations on chemical insecticides, growing adoption of integrated pest management (IPM) programs, rising demand for eco-friendly pest control solutions, technological advancements in biopesticides, and expanding applications in agriculture, public health, and urban pest management.

North America currently dominates the insect growth regulators market due to stringent pesticide regulations, rising insect resistance, increasing IPM adoption, growing organic farming, urban pest control demand, and advancements in biopesticides.

Some of the major players in the insect growth regulators market include BASF SE, Central Life Science (Central Garden & Pet Company), Control Solutions Inc (China National Chemical Corporation), Dow Inc, Nufarm Limited, OHP Inc. (AMVAC Chemical Corporation), Russell IPM Ltd, Sumitomo Chemical Co. Ltd., Syngenta AG, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)