Industrial Insulation Market Report by Product (Blanket, Board, Pipe, and Others), Insulation Material (Mineral Wool, Fiber Glass, Foamed Plastics, Calcium Silicate, and Others), End Use Industry (Automotive, Chemical and Petrochemical, Construction, Electrical and Electronics, Oil and Gas, Power Generation, and Others), and Region 2026-2034

Industrial Insulation Market Size:

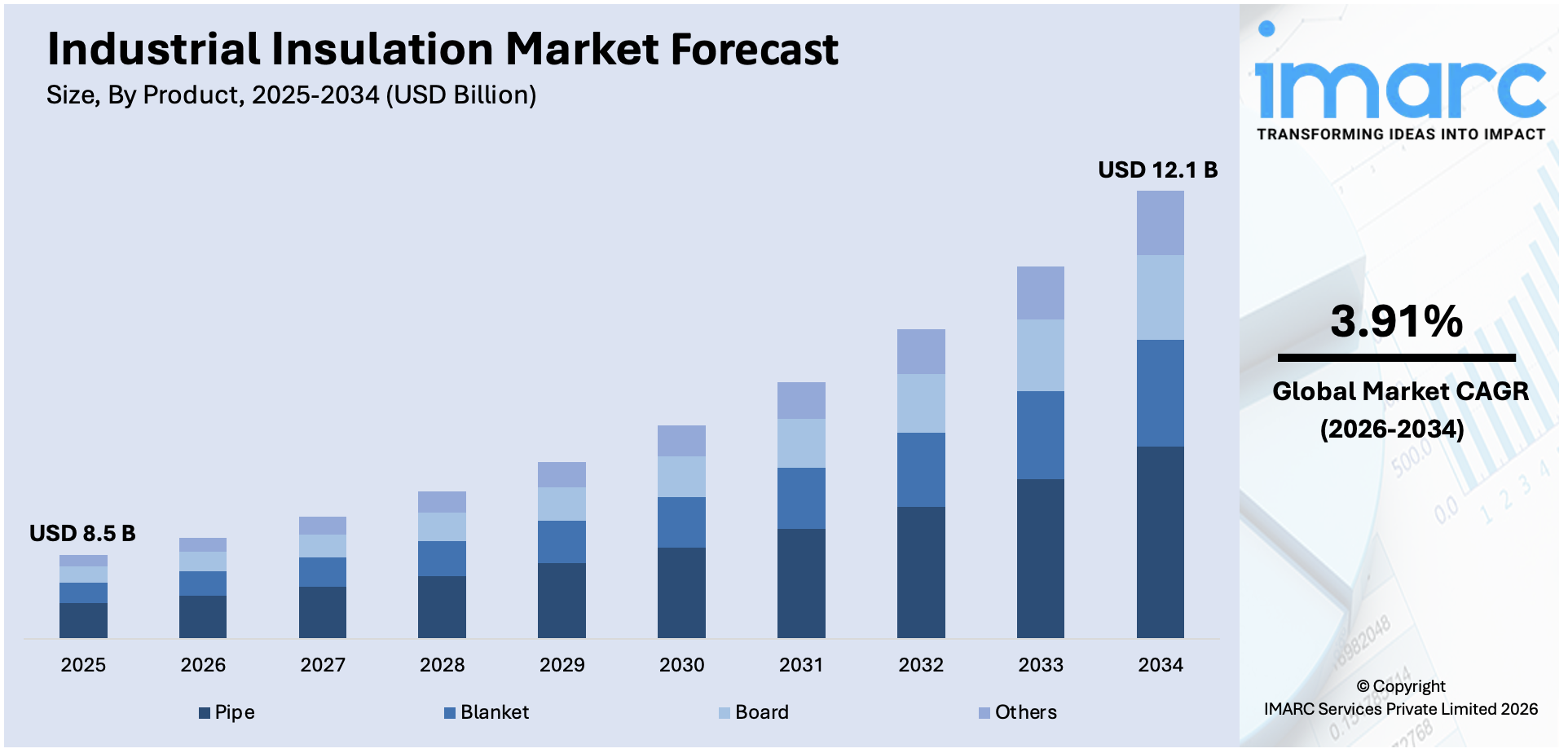

The global industrial insulation market size reached USD 8.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 12.1 Billion by 2034, exhibiting a growth rate (CAGR) of 3.91% during 2026-2034. The market is experiencing steady growth driven by the growing need for energy efficiency across different industry verticals, rising preferences of businesses for more efficient and environment-friendly alternatives, and the increasing construction of new refineries and chemical processing plants.

|

Report Attribute

|

Key Statistics |

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2034 | USD 12.1 Billion |

| Market Growth Rate 2026-2034 | 3.91% |

Industrial Insulation Market Analysis:

- Market Growth and Size: The global industrial insulation market growth is experiencing steady growth, driven by factors, such as energy efficiency regulations, sustainability initiatives, and the expansion of key end-use industries.

- Technological Advancements: There is a rise in the development of innovative insulation materials, including eco-friendly alternatives like aerogels. In addition, the emergence of smart insulation systems with monitoring capabilities provides real-time data for energy efficiency and facility management.

- Industry Applications: Industrial insulation finds widespread application in industries, such as petrochemical, power generation, oil and gas, and manufacturing. These sectors rely on insulation solutions to enhance energy efficiency, ensure safety compliance, and maintain process temperatures.

- Geographical Trends: Asia-Pacific leads the market, driven by the expansion of industries in the region. However, North America and Europe are emerging as one of the fast-growing markets on account of stringent energy regulations and sustainability goals.

- Competitive Landscape: The market features a competitive landscape with established manufacturers and suppliers offering a wide range of insulation solutions. Competition is driven by the need for specialized insulation materials catering to diverse industrial requirements.

- Challenges and Opportunities: While the market faces challenges, such as the need for constant innovation to meet evolving regulatory standards and sustainability demands, it also encounters opportunities by developing insulation solutions tailored to the specific needs of growing industries and exploring emerging markets for expansion.

- Future Outlook: The future outlook for the industrial insulation market remains positive, with continued growth prospects. Additionally, emerging technologies and materials, along with expanding end-use industries, are expected to drive market expansion.

To get more information on this market Request Sample

Industrial Insulation Market Trends:

Growing Concern for Energy Efficiency

The growing concerns for energy efficiency across different industry verticals represent one of the primary factors favoring the market growth. In addition, governing authorities and regulatory bodies of several countries are imposing stringent energy efficiency standards and regulations to reduce carbon emissions and combat climate change. This is encouraging industrial facilities to prioritize energy-efficient practices, driving the industrial insulation market demand. For instance, Energy Conservation Building Code (ECBC), Shunya Labeling for NZEBs and NPEBs, Star Rating of Commercial Buildings, TERI’s Green Rating for Integrated Habitat Assessment (GRIHA), National Mission for Enhanced Energy Efficiency (NMEEE), and National Building Code of India 2016 (NBC 2016) are some of the energy efficiency policies and programs in India. Proper insulation reduces heat transfer, which, in turn, lowers energy consumption for heating and cooling processes in industrial facilities. Along with this, several companies are increasingly adopting eco-friendly practices to reduce their carbon footprint and promote environmental health. In line with this, the development of innovative insulation materials made from recycled and renewable resources is attracting a wider consumer base, bolstering the market growth. Furthermore, the rising focus of businesses on meeting energy efficiency regulations is driving the market. Moreover, the escalating demand for advanced industrial insulation solutions across various industries is offering lucrative opportunities to manufacturers and suppliers. According to The Economic Times, nine in ten Indian business leaders (92.2%) are also concerned about the availability, reliability, and security of the energy supply. The most common concerns are further price increases (42%), power cuts or blackouts (40%), and energy rationing or supply interruptions (34%). This is further bolstering the industrial insulation market statistics.

Technological Advancements and Material Innovations

Continuous technological advancements and material innovations are strengthening the growth of the market. Additionally, the rising preferences of businesses for more efficient and environment-friendly alternatives like aerogels due to their exceptional thermal insulation properties and lightweight nature, are facilitating the market growth. Furthermore, advancements in the manufacturing processes are leading to the development of insulation materials with enhanced fire resistance and durability. These materials are well-suited for industrial applications, for enhanced safety and longevity. Apart from this, the integration of nanotechnology into insulation materials is also contributing to improved performance characteristics. Similarly, Syneffex, a subsidiary of Industrial Nanotech Inc. specializing in nanotechnology-based solutions, proudly announced the strategic appointments of Pawel Cyniak as president of global business development and Wojciech Samilo as president of global strategy partnerships. Furthermore, the emergence of smart insulation systems with sensors and monitoring capabilities is offering a favorable market outlook. These systems provide real-time data on energy efficiency and insulation performance and allow facility managers to optimize energy consumption and address insulation issues promptly. Moreover, smart insulation improves energy conservation, reduces operational costs, and enhances the overall efficiency of industrial facilities. For instance, Recticel Group signed an agreement to acquire REX Panels & Profiles in Belgium, a move that allows it to accelerate its position in the growing insulated panels market.

Rapid Expansion of End-Use Industries

Rapid urbanization and the expansion of industries across the globe are creating a positive outlook for the market. In addition, the rising utilization of insulation materials across various end-use industries, including petrochemical, power generation, oil and gas, and manufacturing is strengthening the growth of the market. Along with this, the increasing construction of new refineries and chemical processing plants is influencing the market positively. For instance, companies in the Middle East announced petrochemical and hydrogen projects, including QatarEnergy and its partner Chevron Phillips Chemical, a joint venture between Chevron and Phillips 66, awarded a contract for early site works for a petrochemicals project in Ras Laffan that is expected to boost Qatar's polyethylene production capacity by more than 60%. This is further driving the future of industrial insulation market. These facilities require efficient insulation to maintain process temperatures, reduce energy costs, and ensure safety compliance. In line with this, the growing need for cleaner and more efficient energy sources in renewable energy installations is offering a favorable market outlook. Moreover, the increasing reliance of the oil and gas industry on insulation to mitigate heat loss in pipelines and equipment and ensure the integrity of operations in extreme environmental conditions is contributing to the market growth. Apart from this, the rising emphasis on precision and automation in the manufacturing sector is catalyzing the demand for insulation in industrial machinery and equipment.

Industrial Insulation Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product, insulation material, and end use industry.

Breakup by Product:

- Blanket

- Board

- Pipe

- Others

Pipe accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product. This includes blanket, board, pipe, and others. According to the report, pipe represented the largest segment.

Pipe insulation is specifically designed to insulate pipes and ducts in industrial facilities. It comes in various forms, including pre-formed sections, wraps, and jackets. Pipe insulation serves the critical purpose of preventing heat loss or gain, maintaining consistent temperatures within pipelines, and reducing energy consumption. It is widely used in industries such as oil and gas, chemical processing, and heating, ventilation, and air conditioning (HVAC) systems, where maintaining the temperature of fluids or gases is essential for operational efficiency and safety. For instance, high-performance insulation material SLENTEX® has been applied in industrial applications for the first time. The flexible, non-combustible construction solution was adopted in the interiors of close to 400 square meters of pipes, valves, and flanges in BASF’s manufacturing plant located in Ulsan, Korea. This is further fueling the industrial insulation market revenue.

Breakup by Insulation Material:

- Mineral Wool

- Fiber Glass

- Foamed Plastics

- Calcium Silicate

- Others

A detailed breakup and analysis of the market based on the insulation material have also been provided in the report. This includes mineral wool, fiber glass, foamed plastics, calcium silicate, and others.

Mineral wool insulation is made from natural or recycled materials, typically basalt, slag, or diabase rock. It offers excellent fire resistance, sound absorption, and thermal insulation properties. Mineral wool is widely used in industrial applications where safety and thermal performance are critical, such as in petrochemical plants and power generation facilities. For instance, Saint-Gobain announced that it has acquired the business assets of International Cellulose Corporation (ICC), a privately owned manufacturer of commercial specialty insulation products, including spray-on thermal and acoustical finishing systems.

Fiberglass insulation consists of fine glass fibers that are bonded together. It is known for its lightweight nature and cost-effectiveness. Fiberglass insulation provides effective thermal resistance and is commonly used in commercial and industrial buildings, HVAC systems, and manufacturing facilities. Fiberglass-based printed circuit boards (PCBs) are employed in electronics manufacturing to provide mechanical support and electrical insulation. According to The Economic Times, India's electronics manufacturing sector is set to grow 15 % to be worth USD 115 billion in 2024, with companies continuing to emphasize more on higher levels of value addition in terms of components and development of products. In line with this, the production of mobile phones is expected to exceed USD 50 billion by March 2024 from around USD 42 billion in the previous financial year.

Foamed plastics, including materials like expanded polystyrene (EPS) and polyurethane, are lightweight and have excellent insulation capabilities. They are used extensively in the construction of industrial refrigeration systems, cold storage, and thermal insulation for piping and equipment. Foamed plastics offer versatility and high insulating efficiency. The rising use of foamed plastics in medical devices and orthopedic supports for providing cushioning and support to injured or sensitive body parts. According to invest India, there are 750-800 domestic medical devices manufacturers in India, accounting for 65% of the market. In addition to this, the start-up ecosystem in India’s medical devices sector is diverse and vibrant, with 250+ organisations engaged in innovations for addressing important health issues.

Calcium silicate insulation is a non-combustible material known for its exceptional temperature resistance and moisture resistance. It is often used in high-temperature industrial applications, including furnace linings, steam and process pipe insulation, and fire protection. Calcium silicate insulation is valued for its durability in extreme conditions. Calcium silicate insulation is used in fireproofing applications due to its excellent fire-resistant properties. According to the National Safety Council, in 2022, 1,504,500 fires resulted in 3,790 civilian deaths and 13,250 injuries. In line with this, there were 96 on-duty firefighter deaths.

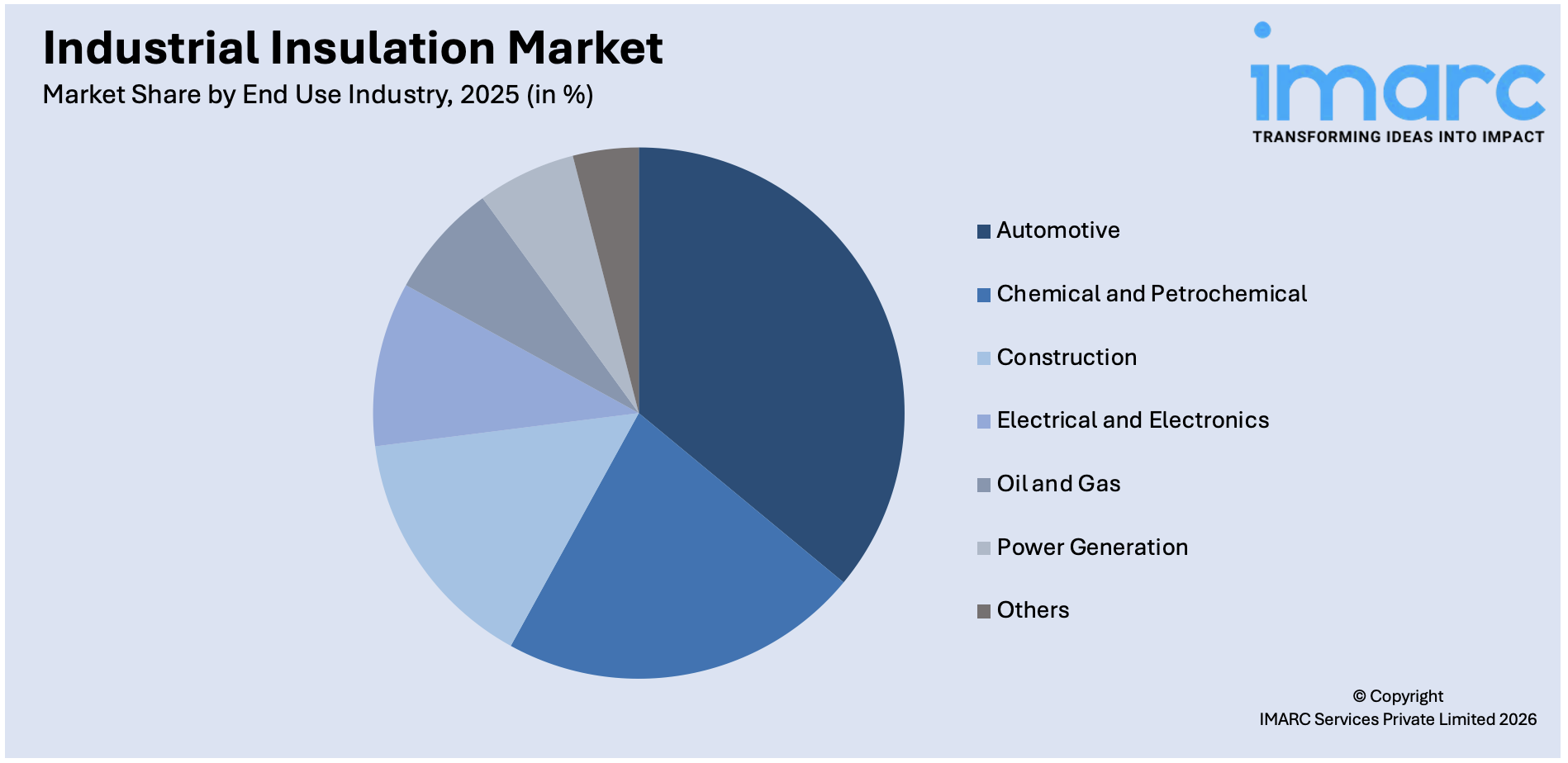

Breakup by End Use Industry:

Access the comprehensive market breakdown Request Sample

- Automotive

- Chemical and Petrochemical

- Construction

- Electrical and Electronics

- Oil and Gas

- Power Generation

- Others

The report has provided a detailed breakup and analysis of the market based on the end use industry. This includes automotive, chemical, and petrochemical, construction, electrical and electronics, oil and gas, power generation, and others.

Insulation materials are widely used in the automotive industry to reduce noise, vibration, and thermal fluctuations within vehicles. Automotive insulation helps enhance passenger comfort and improve fuel efficiency by minimizing heat transfer. It is commonly found in vehicle interiors, engine compartments, and exhaust systems. According to ESSI, to achieve energy security and climate protection targets, vehicles that are more efficient and run on fuels with lower carbon emissions are essential. EESI works to expedite the shift from petroleum-based fuels to alternate liquid and non-liquid "fuels" produced from renewable sources, all the while promoting advances in vehicle fuel economy.

The chemical and petrochemical industry relies on insulation to maintain consistent temperatures in processing equipment and pipelines. Insulation materials prevent heat loss or gain, ensuring the safe and efficient operation of chemical processes and storage facilities. This sector values insulation for its role in safety, energy efficiency, and process optimization. According to Statista, the production capacity of petrochemicals worldwide reached almost 2.3 billion metric tons in 2021. By 2030, it is expected to grow significantly, with China, India, and Iran the countries with the largest petrochemical capacity additions announced or planned.

In construction, insulation materials are essential for energy-efficient buildings. They provide thermal insulation to regulate indoor temperatures and reduce heating and cooling costs. Insulation is used in walls, roofs, and floors to create comfortable and sustainable living and working environments. According to Deloitte, the construction industry entered 2023 marked by a 7% increase in nominal value added and a 6% increase in nominal gross output compared to the previous year.

Insulation materials find numerous applications in the electrical and electronics industry to prevent electrical shorts, protect components from overheating, and ensure the safe transmission of electricity. It is used in cables, wires, transformers, and electronic devices, for maintaining electrical integrity and safety. According to Edison Electric Institute, energy agency (IEA) In 2022, total U.S. electricity generation was 4,243,136 gigawatt-hours (GWh)—an increase of 3.5 percent over total generation in 2021.

The oil and gas sector relies on insulation to control temperatures in pipelines, storage tanks, and offshore platforms. Insulation materials help maintain the flow of oil and gas, prevent freezing, and reduce energy consumption. Insulation is crucial for ensuring the efficiency and safety of oil and gas operations. For example, in 2022, global crude oil production increased by a record 5.4% rate, much above its 2021 growth (+1.6%) and its 2010-2019 average (+1.3%/year), in a context of global economic growth and progressive OPEC+ crude oil production adjustment (+0.4 mb/d each month until phasing out the 5.8 mb/d production adjustment), according to enerdata.

In power generation, insulation is used in various equipment, including turbines, boilers, and generators. It is essential for optimizing energy production, preventing heat loss, and maintaining equipment reliability. Insulation materials play a critical role in reducing energy consumption and greenhouse gas emissions in the power generation sector. According to enerdata, coal is the top energy source in India with a share of 46% in 2022, followed by oil (24%) and biomass (21%). Natural gas covers 5% and primary electricity (hydro, nuclear, solar, and wind) 4% which is driving the power generation industry.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia-Pacific leads the market, accounting for the largest industrial insulation market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia-Pacific accounted for the largest market share.

Asia Pacific stands as a key region for the industrial insulation market due to rapid industrialization, urbanization, and infrastructure development. Additionally, countries like China and India are experiencing substantial growth in construction, manufacturing, and energy sectors, driving demand for insulation materials. Along with this, energy efficiency initiatives, coupled with government regulations, promote the use of industrial insulation in this region. Moreover, Asia Pacific is a major consumer of insulation materials in applications ranging from commercial buildings to heavy industries. According to Economic and Social Commission for Asia and the Pacific (ESCAP) every day an estimated 120,000 people are migrating to cities in the Asia Pacific region and by 2050, the proportion of people living in urban areas is likely to rise to 63% when the urban population could be 3.3 billion.

Leading Key Players in the Industrial Insulation Industry:

The key players in the market are consistently investing in research and development (R&D) activities to introduce innovative insulation materials and solutions. This includes the development of eco-friendly and energy-efficient insulation materials, aligning with global sustainability trends. Additionally, many major players are expanding their geographical footprint to tap into emerging markets with a growing industrial sector. This includes establishing new manufacturing facilities and distribution networks. They are also forming partnerships with other industry stakeholders, such as construction companies and energy management firms to offer comprehensive insulation solutions and services to clients. Apart from this, they are embracing digital technologies for better project management and client engagement. This includes the use of digital tools for project estimation, monitoring, and maintenance.

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Armacell

- Aspen Aerogels, Inc.

- BNZ Materials

- Cabot Corporation

- Kingspan Group

- Knauf Insulation

- Morgan Advanced Materials

- Paroc Group Oy (Owens Corning)

- Rath-Group

- Rockwool A/S

- Temati B.V.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News:

- December 09, 2022: Rockwool A/S announced the launch of a new plant in Qingyuan, Guangdong Province, China. The new plant adopts the most advanced electric furnace production line and centrifuge equipment to achieve the production process upgrade and product quality improvement.

- January 15, 2020: Owens Corning, an inventor and a leading global producer of fiberglass insulation, announced the launch of a next-generation insulation product made by PureFiber Technology. The product is soft to the touch, has less dust, is easy to use, cut, and split, and is non-combustible as per BS476-part 4.

Industrial Insulation Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Blanket, Board, Pipe, Others |

| Insulation Materials Covered | Mineral Wool, Fiber Glass, Foamed Plastics, Calcium Silicate, Others |

| End Use Industries Covered | Automotive, Chemical and Petrochemical. Construction, Electrical and Electronics, Oil and Gas, Power Generation, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Armacell, Aspen Aerogels, Inc., BNZ Materials, Cabot Corporation, Kingspan Group, Knauf Insulation, Morgan Advanced Materials, Paroc Group Oy (Owens Corning), Rath-Group, Rockwool A/S, Temati B.V., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the industrial insulation market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global industrial insulation market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the industrial insulation industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global industrial insulation market was valued at USD 8.5 Billion in 2025.

We expect the global industrial insulation market to exhibit a CAGR of 3.91% during 2026-2034.

The rising demand for industrial insulation across various end-use industries, such as automotive, petrochemicals, electronic, etc., as it ensures energy conservation and process optimization, eliminates condensation of moisture, reduces the risks of accidents and fire hazards, etc., is primarily driving the global industrial insulation market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary halt of numerous production activities for industrial insulation.

Based on the product, the global industrial insulation market can be bifurcated into blanket, board, pipe, and others. Currently, pipe exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where Asia-Pacific currently dominates the global market.

Some of the major players in the global industrial insulation market include Armacell, Aspen Aerogels, Inc., BNZ Materials, Cabot Corporation, Kingspan Group, Knauf Insulation, Morgan Advanced Materials, Paroc Group Oy (Owens Corning), Rath-Group, Rockwool A/S, and Temati B.V.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)