India Sportswear Market Size, Share, Trends and Forecast by Product, Distribution Channel, End User, and Region, 2026-2034

India Sportswear Market Size, Share, Trends & Forecast (2026-2034)

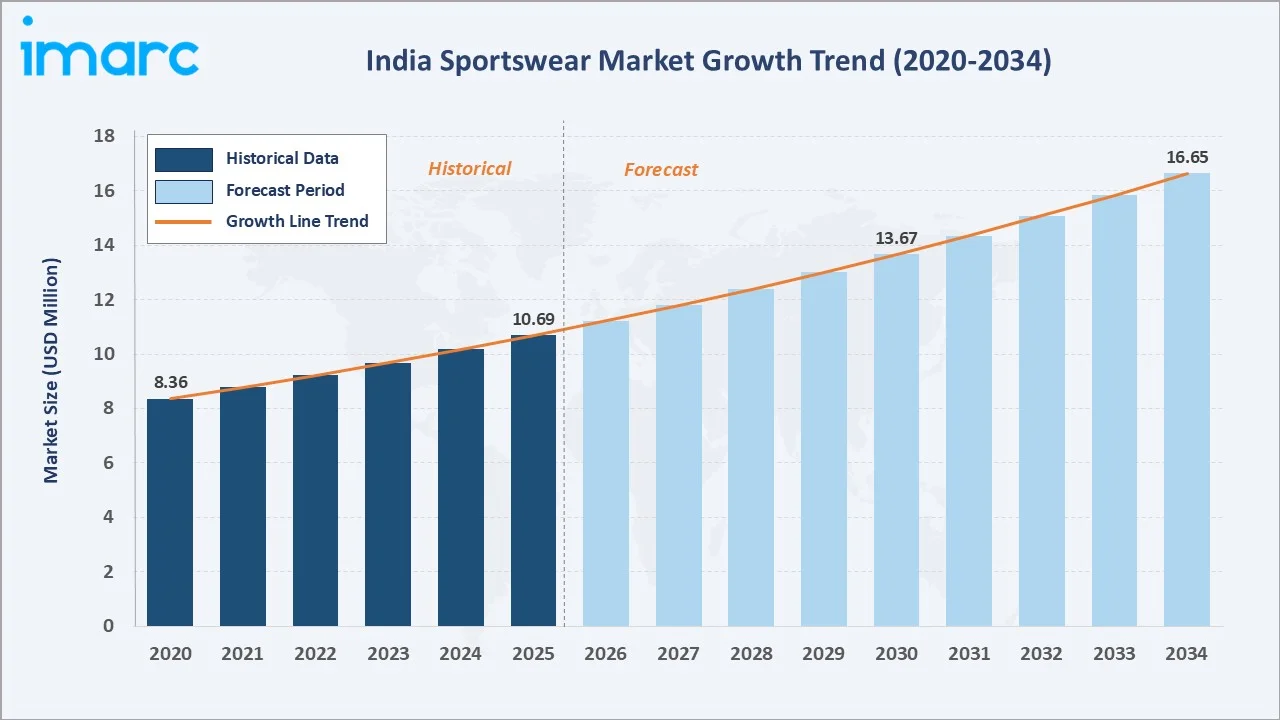

The India sportswear market reached USD 10.69 Million in 2025 and is projected to reach USD 16.65 Million by 2034, growing at a CAGR of 5.04% during 2026-2034. Rising health consciousness, the mainstream adoption of athleisure fashion, expanding e-commerce channels, and robust government investment in sports infrastructure are the key growth drivers propelling the market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.69 Million |

|

Forecast Market Size (2034) |

USD 16.65 Million |

|

CAGR (2026-2034) |

5.04% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (32.0% share, 2025) |

|

Fastest Growing Region |

South India |

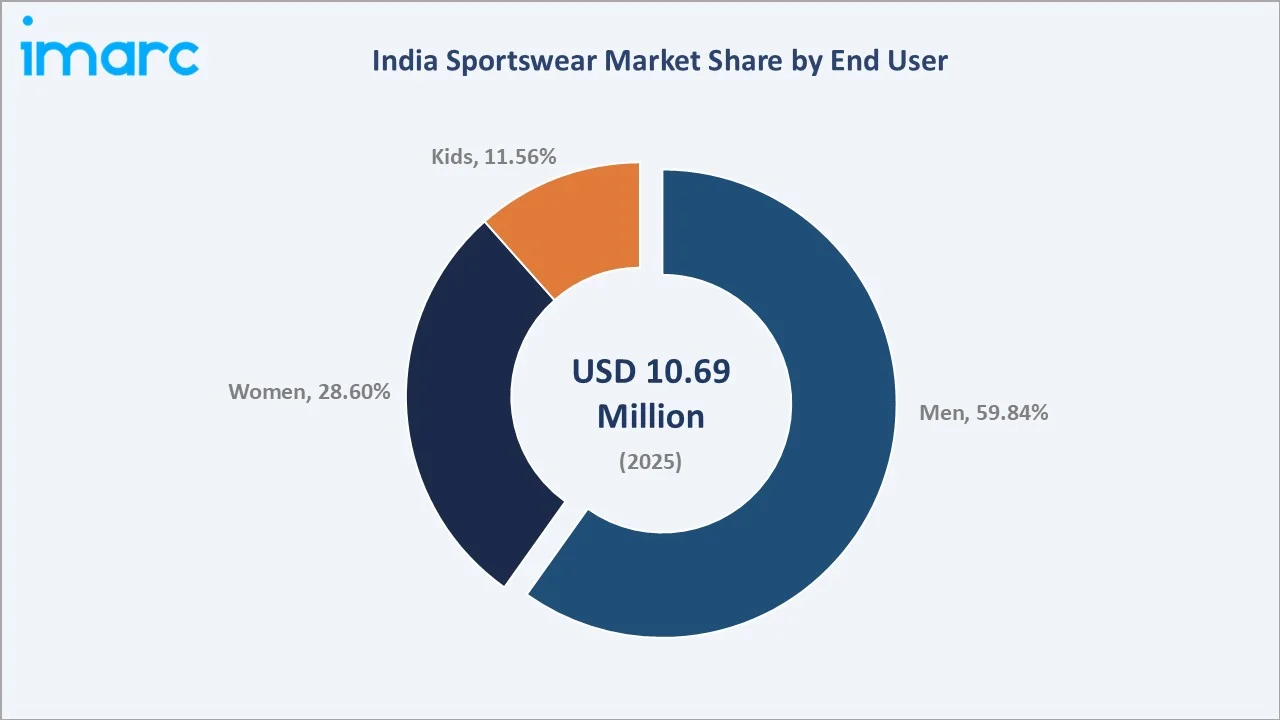

North India dominates, holding a 32.0% market share in 2025, while the men's segment leads end-user demand at 59.84%. Shoes remain the dominant product category with a 55.74% share. India's sportswear industry is benefitting from a dramatic transformation driven by the athleisure phenomenon, which has fundamentally redefined consumer wardrobe choices by seamlessly blending performance and casual aesthetics.

To get more information on this market, Request Sample

With applications spanning performance sports, fitness training, recreational athletics, and everyday athleisure, the market is expected to continue its steady expansion, supported by tier-two and tier-three city growth, where tier-three cities alone posted 21% year-on-year growth in e-commerce sportswear orders during 2025 summer sales, alongside increasing participation in organized sports and the proliferating influence of social media fitness culture across India's diverse consumer demographics.

Executive Summary

The India sportswear market is on a steady, consumer-driven growth path, underpinned by the confluence of rising health consciousness, mainstream athleisure adoption, digital commerce expansion, and increasing sports participation among India's large and young population. The market reached USD 10.69 Million in 2025 and is forecast to reach USD 16.65 Million by 2034, reflecting a CAGR of 5.04% over the forecast period.

North India commands the largest regional share at 32.0% in 2025, driven by high population density, strong retail infrastructure in metropolitan centers such as Delhi NCR, and a well-established sports culture. South India represents the fastest-growing regional opportunity, with Bengaluru's vibrant fitness culture and tech-affluent consumer base driving sportswear sales growth of 25% year-on-year.

Men dominate end-user demand at 59.84%, while the women's segment emerges as the fastest-growing demographic, driven by increasing female sports participation. Leading players, including Nike, Inc., Adidas, PUMA SE, Decathlon, and Under Armour Inc., are investing in celebrity partnerships and aggressive retail expansion to capture India's rapidly growing active lifestyle consumer base.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (End User) |

Men – 59.84% share (2025) |

|

Largest Segment (Product) |

Shoes – 55.74% share (2025) |

|

Fastest Growing End User |

Women (rising fitness participation) |

|

Leading Region |

North India – 32.0% revenue share (2025) |

|

Fastest Growing Region |

South India (Bengaluru fitness culture) |

|

Top Companies |

Nike, Inc., Adidas, PUMA SE, Decathlon, and Under Armour Inc. |

|

Market Opportunity |

Tier-2/tier-3 city expansion and women's sportswear segment |

Key Analytical Observations Supporting the Above Data:

- Men account for 59.84% of India's sportswear market in 2025, maintaining market leadership through higher participation rates in organized sports, gym memberships, and outdoor athletic activities.

- Shoes dominate the product segment at 55.74% (2025), driven by the rapid growth of athletic footwear demand across running, gym training, cricket, and basketball activities. Major brands, including Puma and Adidas, have signed major franchise agreements to expand sports footwear availability across tier-two and tier-three markets.

- North India holds 32.0% of the Indian sportswear market in 2025, benefitting from high urban concentration in Delhi NCR, Chandigarh, Jaipur, and Lucknow, supported by extensive modern retail infrastructure, metro-accessible brand stores, and strong sports event culture.

- South India is the fastest-growing region, with Bengaluru's technology sector creating a large base of fitness-conscious, high-disposable-income consumers, complemented by Decathlon's aggressive retail expansion into cities like Kochi and Raipur, bringing affordable activity-specific sportswear to previously underserved markets.

- The women's sportswear segment is emerging as the fastest-growing end-user category, driven by rising female gym memberships, growing participation in yoga, running, and cricket, and the influence of women athletes and fitness influencers reshaping cultural attitudes toward women's sports engagement.

India Sportswear Market Overview

The India sportswear market encompasses clothing, footwear, and accessories specifically engineered for athletic performance, fitness activities, and the broader athleisure lifestyle category. The market has undergone a dramatic transformation, evolving from a product category primarily serving professional athletes and competitive sports participants to a mainstream consumer segment embedded in everyday Indian lifestyle choices.

Athleisure, the seamless blending of athletic performance and casual fashion aesthetics, has emerged as the defining market dynamic, fundamentally expanding the addressable consumer universe beyond traditional sportswear demographics.

India's young demographic profile, with approximately 65% of the population under 35, combined with rapidly growing urban middle-class aspirations, social media fitness influence, and increasing discretionary income, creates an exceptionally favorable structural backdrop for sportswear market expansion.

Government initiatives, including Khelo India National Programme for the Development of Sports, launched in 2016-17, aim to foster mass participation and sporting excellence in both rural and urban areas. In 2021, the scheme was extended for an additional five years with a funding allocation of ₹3,790.50 crore.

Market Dynamics

To evaluate market opportunities, Request Sample

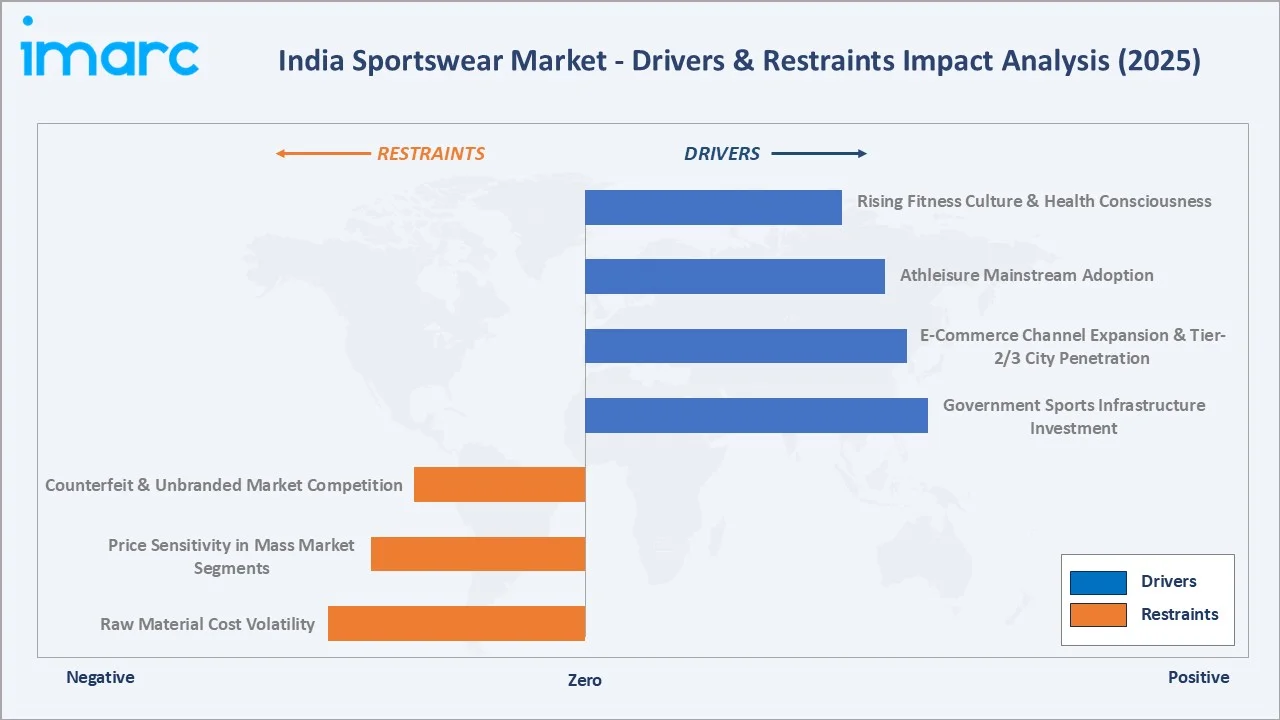

Market Drivers

- Rising Fitness Culture and Health Consciousness: As of 2024, India has around 12.3 million fitness facility members, representing a base with high sportswear purchase frequency. The growing prevalence of lifestyle diseases, including obesity and cardiovascular disorders, has catalyzed a nationwide shift toward preventive fitness.

- Athleisure Mainstream Adoption: Social media influencers and celebrity endorsements have normalized sportswear for office environments, social gatherings, and travel scenarios. The Indian athleisure market, valued at USD 13,879.7 Million in 2024, is projected to reach USD 22,367.3 Million by 2034, reflecting the magnitude of this lifestyle category expansion.

- E-Commerce Channel Expansion and Tier-2/3 City Penetration: Tier-three cities posted 21% year-on-year growth in e-commerce sportswear orders during 2025 summer sales, substantially outpacing the overall 8% market growth rate.

- Government Sports Infrastructure Investment: The Khelo India Programme has established 1,045 Khelo India Centres and approved 326 new sports infrastructure projects, creating direct demand for sports equipment and apparel at the grassroots level.

Market Restraints

- Counterfeit and Unbranded Market Competition: Over one in four sports apparel sales in smaller cities involves unbranded or imitation products, limiting market penetration for premium international brands and depressing average selling prices across the category.

- Price Sensitivity in Mass Market Segments: Despite rising incomes, price sensitivity remains a significant constraint on branded sportswear adoption among India's large middle-market consumer base. Premium brands, including Nike, Adidas, and Puma, face affordability barriers that restrict their penetration beyond urban upper-middle-class demographics.

- Raw Material Cost Volatility: Sportswear manufacturing is exposed to significant raw material price fluctuations, particularly in synthetic performance fabrics, rubber and foam for footwear, and specialty technical laminates. Global supply chain disruptions and commodity price cycles create margin pressure for both international brands and domestic manufacturers.

Market Opportunities

- Women's Sportswear Segment Expansion: In February 2025, Nike and SKIMS introduced NikeSKIMS, a new brand focused on empowering women athletes with innovative activewear, reflecting global brand recognition of women's athletic wear as a priority growth category. Increasing female gym memberships, yoga participation, and cricket engagement are creating a rapidly expanding addressable market.

- Tier-2 and Tier-3 City Market Development: Major retailers, including Decathlon, have accelerated store expansion in cities like Indore, Jaipur, Surat, Kochi, and Raipur, bringing activity-specific sportswear closer to previously underserved audiences.

- Sustainable and Technology-Integrated Sportswear: Adidas India gained momentum by expanding its sustainable sports apparel line, achieving a 20% sales increase in 2024. Smart fabric technologies incorporating moisture management, thermal regulation, compression science, and embedded biometric sensing represent a premium innovation frontier offering significant differentiation opportunity in India's increasingly sophisticated sportswear market.

Market Challenges

- Intense Competition from Global Premium Brands: India's sportswear market faces substantial competitive pressure from well-established international brands, Nike, Adidas, Puma, Reebok, and Under Armour, which dominate premium market segments through aspirational positioning, celebrity endorsements, and technologically advanced product innovation.

- Supply Chain Complexity and Local Manufacturing Gaps: India's domestic sportswear manufacturing ecosystem remains underdeveloped relative to global competitors, creating supply chain dependency on imports and limiting the ability to respond rapidly to shifting consumer demand.

Emerging Market Trends

1. Athleisure Mainstream Surge and Lifestyle Redefinition

In 2025, Lehar Footwear Limited unveiled its new sports and athleisure brand RANNR, marking its entry into performance footwear, reflecting the broader trend of consumer goods companies recognizing athleisure's mainstream consumer appeal. The India athleisure market is projected to reach USD 22,367.3 Million by 2034, growing at approximately 5.28% CAGR.

2. D2C Brand Proliferation and Digital Commerce Growth

Social media marketing, influencer partnerships, and personalized recommendation algorithms enable D2C brands to build engaged communities among fitness enthusiasts. E-commerce sportswear sales increased 32% in 2024, with Myntra, Amazon, and Flipkart becoming primary discovery and purchase channels for branded sportswear among India's digital-native consumer segment.

3. Sustainable Sportswear and Eco-Conscious Consumption

In April 2025, PUMA launched the Audacity Pack featuring performance-enhancing technologies while emphasizing inclusive, sustainable design. Adidas's commitment to sustainable sports apparel lines drove 20% sales growth in 2024. Recycled polyester fabrics, water-efficient manufacturing processes, and circular economy take-back programs are increasingly influencing premium sportswear purchase decisions.

4. Smart Fabric and Technology-Integrated Sportswear

Moisture-wicking technology, compression science for recovery, UV-protective fabrics, and thermal regulation systems are becoming expected features in mid-to-premium sportswear segments. In January 2025, Adidas replaced Puma as the official clothing partner of the Mercedes-AMG Petronas Formula 1 Team, reflecting sportswear brands' strategy of associating with elite athletic performance to reinforce technology and innovation credentials in consumer markets globally and in India.

Industry Value Chain Analysis

The India sportswear value chain spans raw material and fabric sourcing through manufacturing, quality certification, multi-channel distribution, and end-consumer delivery, each stage populated by specialized operators whose quality performance and regulatory compliance directly shape product performance, brand positioning, and market competitiveness.

|

Stage |

Key Players / Examples |

|

Raw Material & Fabric Sourcing |

Synthetic fiber manufacturers, cotton textile mills, rubber & foam suppliers, dye and finishing chemical companies |

|

Fabric & Component Manufacturing |

Technical fabric mills (polyester, nylon, spandex blends), foam sole producers, mesh and knit specialists |

|

Sportswear Production |

Nike India contract factories, Campus Activewear plants, Decathlon sourcing partners, and Puma India manufacturing |

|

Quality & Compliance Testing |

BIS certification labs, ISO-accredited testing agencies, performance-specific testing (sweat resistance, durability, colorfastness) |

|

Retail & Distribution Channels |

Exclusive brand outlets, multi-brand sports retailers, department stores, e-commerce (Amazon, Flipkart, Myntra), D2C platforms |

|

End Consumers |

Men's fitness/sports segment, women's athleisure, youth/kids’ sports, school and college athletes, recreational users |

Technology Landscape in the India Sportswear Industry

Advanced Performance Fabric Engineering

Moisture-wicking polyester blends, four-way stretch fabrics, DWR (durable water repellent) coatings, and compression knit technologies are progressively moving from premium international brands into mid-market accessible price points. Adidas's AEROREADY and Nike's Dri-FIT technology platforms have established consumer expectations for moisture management that are now influencing product development standards.

3D Printing and Customized Footwear Technology

Nike's Air Zoom technology platform and Adidas's BOOST midsole system represent the leading edge of footwear performance technology currently available in India's premium sportswear retail segment. These technologies drive consumer upgrade cycles as performance-oriented buyers invest in successive generations of technically superior athletic footwear, supporting premium category value growth.

Digital Retail and AI-Powered Personalization

AI-powered size recommendation algorithms on platforms like Myntra are reducing returns and improving customer satisfaction. Virtual try-on technologies and personalized product feed algorithms are increasing conversion rates for premium sportswear purchases. Brands including Nike and Adidas are deploying mobile apps with fitness tracking integration to create direct consumer engagement ecosystems.

Sustainable Material Innovation and Circular Economy

Recycled ocean plastic fabrics, bio-based polyester derived from sugarcane, and organic cotton blended with performance synthetics represent the frontier of sustainable sportswear material innovation entering India's market. PUMA's RE: FIBER initiative and Adidas's Parley Ocean Plastic collections are introducing circular economy principles to India's premium sportswear consumers.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Shoes | 55.74% | 2025 |

| Distribution Channel | Retail Stores | 35.28% | 2025 |

| End User | Men | 59.84% | 2025 |

| Region | North India | 32.0% | 2025 |

By End User

Men dominate the end-user segment with a 59.84% share in 2025. This dominance reflects higher male participation rates in organized sports, including cricket, football, kabaddi, and gym fitness activities, translating into stronger and more frequent sportswear purchasing patterns.

To access detailed market analysis, Request Sample

Women account for 28.60% and represent the fastest-growing end-user segment, driven by increasing female gym memberships, growing participation in yoga and running events, and the proliferating influence of women athletes and fitness influencers reshaping cultural attitudes toward women's sports and active lifestyle adoption.

By Product

Shoes dominate the product segment with a 55.74% share in 2025. Athletic footwear's dominance reflects the centrality of performance shoes across running, gym training, cricket, basketball, and everyday athleisure wear contexts.

Clothes account for the remaining 44.26%, encompassing athletic apparel, including track pants, sports T-shirts, compression wear, training shorts, and athleisure casual wear. The clothes segment is growing rapidly as the athleisure trend drives consumers to invest in purpose-designed athletic apparel beyond footwear.

Regional Market Insights

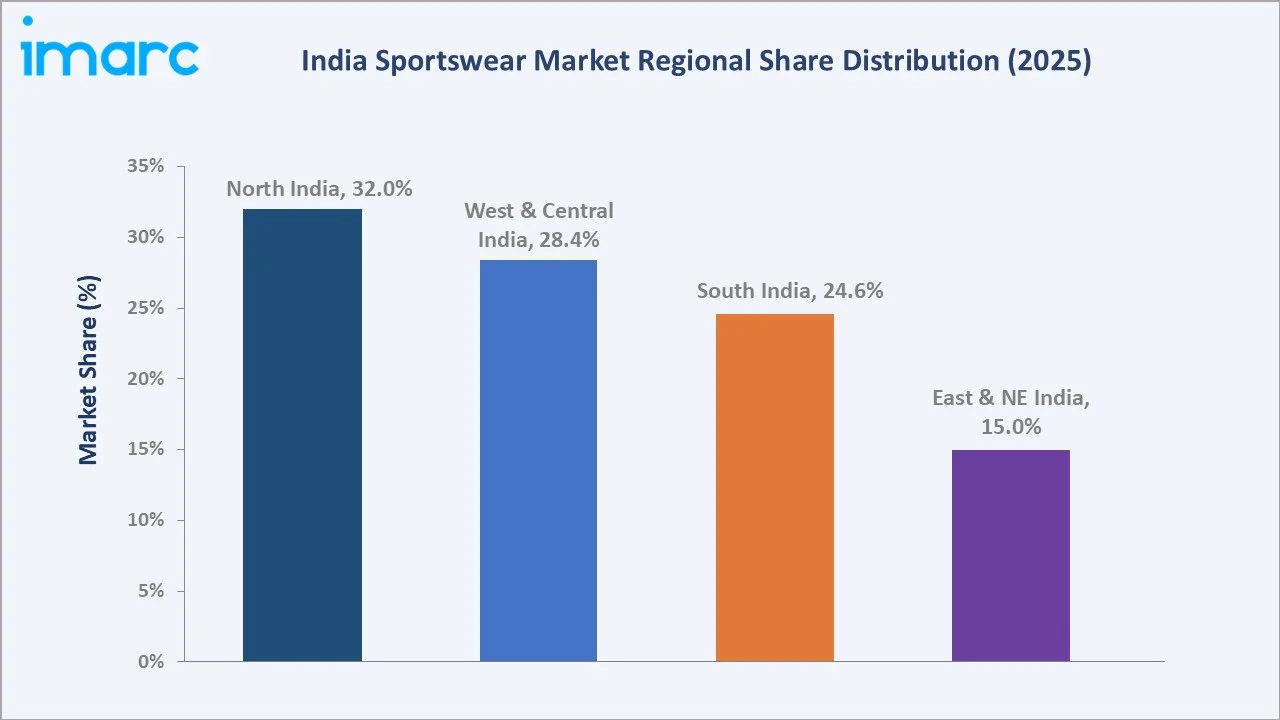

North India's market leadership (32.0%, 2025) reflects the region's high urban concentration, well-developed modern retail infrastructure across Delhi NCR, Chandigarh, Jaipur, and Lucknow, strong cricket culture generating consistent sportswear demand, and the presence of major brand flagship stores and multi-brand sports retailers serving an affluent and sports-engaged consumer base.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

32.0% |

Delhi NCR retail hub, cricket culture, strong brand store density, and high sports event frequency |

|

West & Central India |

28.4% |

Mumbai-Pune financial hub, fitness culture, premium segment preference, IPL fanbase concentration |

|

South India |

24.6% |

Bengaluru tech consumer base, Decathlon expansion, vibrant running culture, 25% YoY growth (2025) |

|

East & NE India |

15.0% |

Kolkata sports heritage, growing e-commerce adoption, rising middle class, online channel 15% YoY growth |

South India is the fastest-growing region, with sportswear sales in Bengaluru increasing by 25% year-on-year, particularly driven by the city's vibrant fitness culture among technology sector professionals. Decathlon's aggressive retail expansion into South Indian cities, including Kochi, Coimbatore, and Raipur, is making activity-specific sportswear accessible at competitive price points across the region.

Competitive Landscape

The India sportswear market exhibits intense competitive dynamics, with multinational corporations competing alongside strong domestic brands across multiple price segments and distribution channels. The top five players, Nike, Inc., Adidas, PUMA SE, Decathlon, and Under Armour Inc., collectively account for approximately 55–60% of total branded sportswear revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Nike, Inc. |

Nike, Jordan |

Market Leader |

Global premium positioning; Air Zoom technology; 15% sales growth in 2025 |

|

Adidas |

Adidas, Adidas Originals |

Market Leader |

Sustainable sportswear leader; Indian national cricket team partnership |

|

PUMA SE |

Puma |

Market Leader |

500+ stores nationwide; celebrity endorsements; affordable athleisure; 12% urban market growth in 2024 |

|

Decathlon |

Decathlon, Quechua, Kalenji |

Strong Challenger |

Value-driven product range; 25% sales growth; aggressive tier 2/3 expansion targeting 190 stores across 90+ cities by 2029 |

|

Under Armour Inc. |

Under Armour |

Challenger |

Premium performance technology; compression wear leadership; NFL footwear partnership (March 2025) |

Other domestic brands, including Campus Activewear, HRX, Shiv-Naresh Sports, and Nivia Sports, also cater effectively to mass-market and entry-level segments.

Key Company Profiles

Nike Inc.

Nike, Inc. (Beaverton, Oregon, USA), is one of the market leaders in India's premium sportswear segment. The company's technology platforms, Air Zoom footwear, and Dri-FIT performance apparel set the performance standard in India's premium athletic segment.

- Product Portfolio: Premium performance footwear (Air Zoom, React, Air Max), athletic apparel (Dri-FIT, Therma-FIT), training equipment, and Jordan brand lifestyle and basketball products targeting urban youth demographics.

- Recent Developments: In February 2025, Nike announced the launch of NikeSKIMS, a new women’s activewear brand created in partnership with Kim Kardashian’s SKIMS, combining Nike’s performance innovation with SKIMS’s inclusive, body‑sculpting design across training apparel, footwear, and accessories

- Strategic Focus: Digital consumer engagement through Nike Training Club and Nike Run Club apps; D2C channel development; women's segment expansion; premium brand positioning through elite athlete and sports event partnerships.

Adidas

Adidas (Herzogenaurach, Germany) is a prominent player in India's sportswear segment. The company has distinguished itself through sustainability leadership, signing with the Indian national cricket team, and committing to the expansion of sustainable sportswear lines.

- Product Portfolio: Adidas performance sportswear, Adidas Originals lifestyle, and Terrex outdoor apparel. Mercedes-AMG Petronas F1 Team official clothing partner.

- Recent Developments: In January 2025, Adidas announced as the new technical clothing partner for the Mercedes‑AMG Petronas Formula 1 Team, taking over from PUMA beginning in the 2025 season.

- Strategic Focus: Sustainable sportswear leadership via Made to Be Remade and Parley Ocean Plastic collections; franchise retail expansion into tier-two/three cities; Indian cricket and football partnership deepening; ESG-aligned brand positioning.

PUMA SE

PUMA SE (Herzogenaurach, Germany) operates one of India's most extensive sportswear retail networks with over 500 stores nationwide. Puma has successfully positioned itself as the affordable-premium athleisure leader in India, supported by aggressive celebrity endorsement campaigns.

- Product Portfolio: Puma performance footwear (Audacity Pack football boots), athleisure apparel, training gear, and the KING heritage collection. April 2025 launch of the Audacity Pack featuring FUZIONFIT3 uppers.

- Recent Developments: In November 2024, Accenture and PUMA SE partnered to transform PUMA India’s supply chain and distribution network using advanced analytics and digital‑twin technology, aiming to accelerate order fulfilment and enhance efficiency across e‑commerce and offline channels.

- Strategic Focus: Scale-driven retail expansion across tier-two and tier-three cities; celebrity endorsement to maintain aspirational brand positioning at accessible price points; athleisure segment leadership; football market growth capture.

Market Concentration Analysis

The India sportswear market exhibits moderate concentration at the branded product level. The top five players, Nike, Inc., Adidas, PUMA SE, Decathlon, and Under Armour Inc., account for approximately 55–60% of branded sportswear revenue in 2025.

The competitive landscape is undergoing rapid restructuring as international brands accelerate franchise-based retail expansion, domestic brands like Campus Activewear invest in manufacturing modernization, and new entrants, including celebrity-led D2C brands (HRX) and international lifestyle-sport crossover brands, gain ground.

Consolidation is emerging in the mid-market segment, where price competition between Decathlon, Campus, and emerging domestic performance brands is intensifying. Private equity investment in Indian sportswear manufacturing and retail platforms has increased, reflecting confidence in the market's long-term structural growth trajectory.

Investment & Growth Opportunities

Fastest Growing Segments

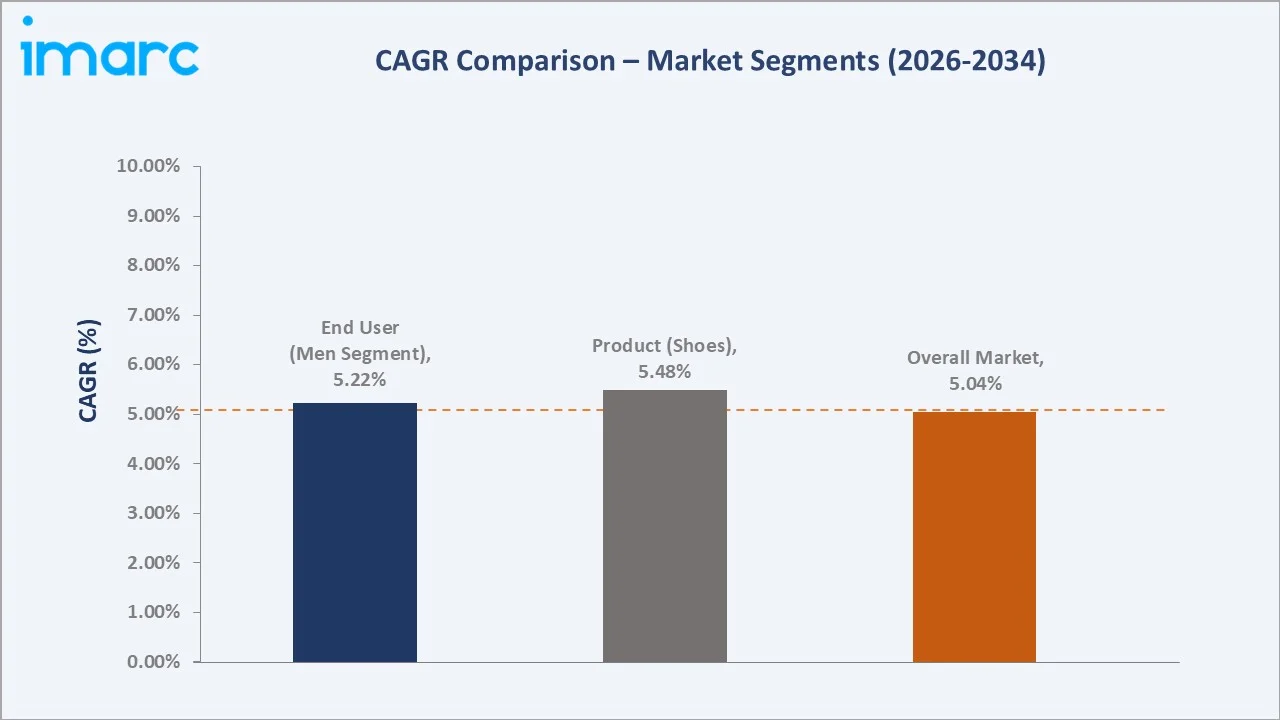

Women's sportswear (estimated CAGR approximately 7%), children's active lifestyle apparel, technology-integrated performance footwear, and sustainable sportswear collections represent the four highest-growth investment vectors through 2034. Together, these niches address a combined incremental opportunity of approximately USD 3.5 Million in additional market value by 2034, with premium per-unit margins significantly exceeding mass-market category benchmarks.

Emerging Market Expansion

India's tier-two and tier-three cities, including Jaipur, Indore, Surat, Kochi, Raipur, Coimbatore, and Visakhapatnam, collectively represent the largest structural expansion opportunity for sportswear market participants through 2034. These geographies offer growing middle-class populations with rising disposable incomes and higher customer loyalty rates that provide better long-term unit economics than saturated metropolitan markets.

Venture and Institutional Investment Trends

- Women's performance sportswear brands targeting India's growing female fitness consumer segment through digital-first D2C channels and social media community building.

- Technology-integrated athletic footwear platforms leveraging AI-powered customization and 3D manufacturing for premium personalized sportswear experiences.

- Sustainable sportswear manufacturing ventures developing India-sourced recycled performance fabrics and circular economy collection programs.

- Tier-two and tier-three city retail platforms combining omnichannel physical and digital distribution for branded sportswear across India's underserved regional markets.

Future Market Outlook (2026-2034)

The India sportswear market is positioned for sustained, consumer-driven growth through 2034. From a base of USD 10.69 Million in 2025, the market is projected to reach USD 16.65 Million by 2034, representing total incremental value creation of approximately USD 5.96 Million over the forecast decade at a CAGR of 5.04%.

Three structural macro-themes will define India's sportswear market trajectory through 2034: the continuing mainstreaming of athleisure as a permanent wardrobe category (expanding the addressable market beyond traditional sports consumers); the geographic democratization of branded sportswear through tier-two and tier-three city retail and e-commerce penetration; and the women's sportswear segment's emergence as the primary growth engine.

Government policy, particularly the Khelo India Programme's grassroots sports infrastructure investment and the broader Fit India Movement's promotion of physical activity, provides an enduring structural tailwind for sportswear demand creation. Brands that successfully navigate India's price sensitivity, counterfeiting challenges, and logistical complexity.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and consultations with over 120 industry stakeholders in 2024-2025, including sportswear brand managers, retail store operators, e-commerce category managers, sports federation procurement officers, footwear manufacturers, textile suppliers, and consumer focus group participants across North, South, West, and East India.

Secondary Research

Secondary research encompassed a systematic review of company annual reports and investor presentations, Ministry of Youth Affairs and Sports budget and program documentation, Bureau of Indian Standards (BIS) regulatory frameworks, IMARC Group proprietary market databases, e-commerce platform sales trend data, trade publications, and publicly available market transaction records.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating India's macroeconomic indicators (GDP growth, urban household income, e-commerce penetration), sports participation trend data, government investment program impacts, and brand-level reported revenue growth rates.

India Sportswear Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Shoes, Clothes |

| Distribution Channels Covered | Online Stores, Retail Stores |

| End Users Covered | Men, Women, Kids |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companie Covered | Nike, Inc., Adidas, PUMA SE, Decathlon, Under Armour Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Sportswear Market Report

The India sportswear market reached USD 10.69 Million in 2025 and is projected to reach USD 16.65 Million by 2034, growing at a CAGR of 5.04% during the forecast period 2026-2034.

The India sportswear market is projected to grow at a CAGR of 5.04% during the forecast period 2026-2034, driven by rising fitness culture, athleisure mainstream adoption, e-commerce channel expansion, and government sports infrastructure investment.

North India dominates the India sportswear market with a 32.0% revenue share in 2025, driven by high population density, Delhi NCR's strong retail infrastructure, cricket culture, and concentration of metropolitan consumers with active sports engagement. South India is the fastest-growing region.

Men are the dominant end-user segment with a 59.84% share in 2025, driven by higher participation rates in organized sports, gym memberships, and outdoor athletic activities, translating into stronger and more frequent sportswear purchasing patterns.

Shoes are the dominant product segment at 55.74% in 2025, driven by rapid growth in athletic footwear demand across running, gym training, cricket, basketball, and everyday athleisure contexts. Puma's 447+ store network and Adidas's franchise expansion reflect the footwear category's strategic priority in India.

Key players in the India sportswear market include Nike, Inc., adidas, PUMA SE, Decathlon, and Under Armour Inc.

E-commerce is a transformative distribution driver for India's sportswear market. Tier-three cities posted 21% year-on-year growth in e-commerce sportswear orders during 2025 summer sales, substantially outpacing overall market growth.

Key challenges include intense competition from counterfeit and unbranded alternatives (comprising over 25% of sales in tier-two and tier-three cities), price sensitivity limiting premium brand penetration, and supply chain complexity from limited domestic high-performance fabric manufacturing capacity.

Key investment opportunities include women's sportswear D2C brands targeting India's growing female fitness consumer, technology-integrated performance footwear platforms, and sustainable sportswear manufacturing using recycled and eco-friendly materials.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)