India Real Estate Market Size, Share, Trends and Forecast by Property, Business, Mode, and Region, 2026-2034

India Real Estate Market Summary:

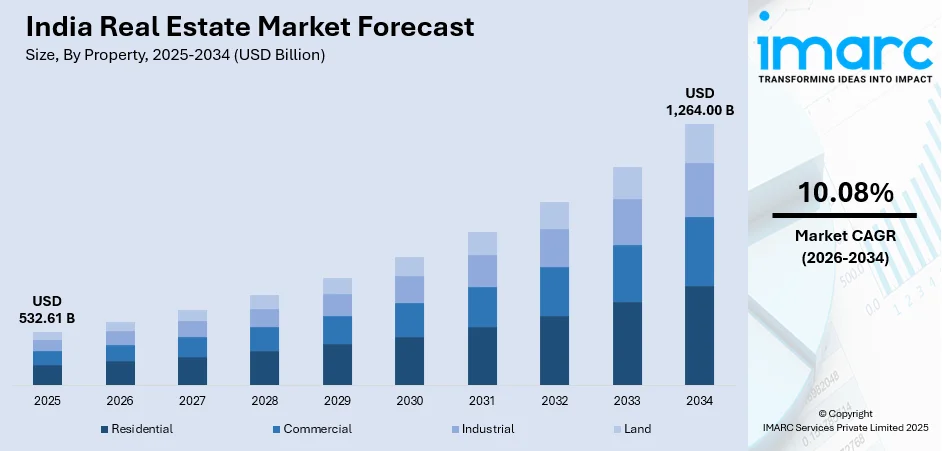

The India real estate market size was valued at USD 532.61 Billion in 2025 and is projected to reach USD 1,264.00 Billion by 2034, growing at a compound annual growth rate of 10.08% from 2026-2034.

The India real estate market is experiencing robust expansion driven by rapid urbanization, rising disposable incomes, and favorable government policies promoting affordable housing initiatives. Infrastructure development across metropolitan and tier II cities continues to fuel demand for residential and commercial spaces. Additionally, increasing foreign direct investments, expansion of IT and manufacturing sectors, and growing middle-class population are augmenting India real estate market share.

Key Takeaways and Insights:

- By Property: Residential segment dominates the market with a share of 78.8% in 2025, driven by rapid urbanization, government housing schemes, and growing demand for affordable and premium housing across metro and tier II cities.

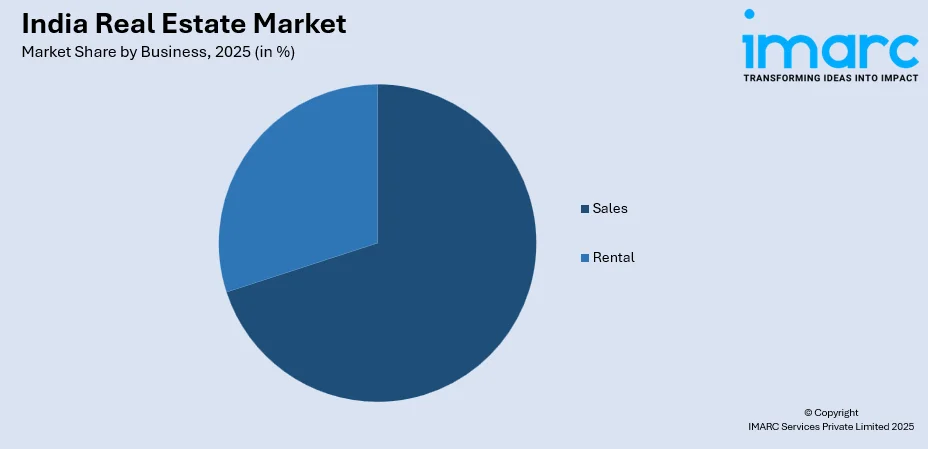

- By Business: Sales segment leads the market with a share of 70.0% in 2025, supported by strong end-user and investor demand seeking property ownership for long-term capital appreciation.

- By Mode: Offline mode represents the largest segment with a market share of 84.2% in 2025, attributed to buyer preference for physical site visits, direct dealer interactions, and traditional property transactions.

- By Region: West and Central India dominates with a 32.0% market share in 2025, driven by dominant urban centers including Mumbai, Pune, Ahmedabad, and robust economic activity.

- Key Players: The India real estate market exhibits moderate to high competitive intensity, with established developers competing alongside regional players across residential, commercial, and industrial segments. Major companies focus on portfolio diversification, sustainable construction practices, and strategic land acquisitions to strengthen market positioning.

To get more information on this market Request Sample

The India real estate sector continues to demonstrate resilience and growth potential, supported by favorable demographic trends and sustained economic expansion. Rising income levels, increasing nuclear families, and easier access to home loans are fueling residential demand across major metropolitan and tier II cities. The commercial segment benefits from expanding Global Capability Centers (GCCs), from 1,700 to 2,500 centers by 2030 operating nationwide contributing significantly to office space absorption. Strong private equity inflows reflect sustained investor confidence in the sector's long-term fundamentals. Government initiatives including RERA implementation, PMAY schemes, and infrastructure development under Smart Cities Mission continue to shape market dynamics, enhance regulatory transparency, and create favorable conditions for both developers and buyers across the industry.

India Real Estate Market Trends:

Rising Demand for Premium and Luxury Housing

The India real estate market is witnessing a significant shift toward premium and luxury housing segments, driven by high-net-worth individuals and NRI investments seeking exclusive residences with modern amenities. Luxury homes priced above Rs 4 Crore recorded 37.8% year-on-year sales growth in the first nine months of 2024, with buyers increasingly seeking smart homes featuring sustainable designs and premium amenities. This trend reflects evolving lifestyle preferences and growing appetite for sophisticated living experiences in prime urban locations.

PropTech Adoption and Digital Transformation

Technology adoption is revolutionizing how real estate is transacted and managed in India. The buyer experience and operational efficiency are being improved by PropTech technologies, such as AI-based property suggestions, virtual site tours, drone-based surveys, and automated CRM systems. In November 2024, when Magicbricks introduced its "Site Visit Product," more than 16,000 site visits and 1,000 reservations for more than 350 projects were made possible, demonstrating how digital platforms are streamlining property discovery and purchase decisions for both developers and homebuyers.

Sustainable and Green Building Development

Environmental sustainability is becoming integral to real estate development as developers increasingly focus on green buildings using eco-friendly materials and energy-efficient designs. Growing environmental awareness among buyers and regulatory emphasis on sustainable construction are driving widespread adoption of IGBC-certified projects nationwide. Developers are incorporating rainwater harvesting, solar energy systems, smart building technologies, and comprehensive waste management solutions to reduce carbon footprints. This shift reflects evolving consumer preferences for environmentally responsible living spaces while aligning with government initiatives promoting net-zero carbon emission targets.

Market Outlook 2026-2034:

The India real estate market outlook remains positive with sustained demand across residential and commercial segments, supported by favorable government policies and robust infrastructure development initiatives. Continued urbanization, rising incomes, and expanding middle-class population will drive housing demand across metropolitan and tier II cities, while GCC expansions, data center development, and flexible workspace adoption boost commercial spaces. Strategic investments in transportation networks, smart city projects, and industrial corridors are expected to further strengthen market fundamentals and create new growth opportunities. The market generated a revenue of USD 532.61 Billion in 2025 and is projected to reach a revenue of USD 1264.00 Billion by 2034, growing at a compound annual growth rate of 10.08% from 2026-2034.

India Real Estate Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Property | Residential | 78.8% |

| Business | Sales | 70.0% |

| Mode | Offline | 84.2% |

| Region | West and Central India | 32.0% |

Property Insights:

- Residential

- Commercial

- Industrial

- Land

The residential segment dominates with a market share of 78.8% of the total India real estate market in 2025.

The residential segment is driven by rapid urbanization, a growing middle class, and government assistance through programs like the Pradhan Mantri Awas Yojana (PMAY) and tax breaks on home loans. Consumers are drawn to cities like Mumbai, Bengaluru, Delhi NCR, and Pune because of their improved infrastructure and job prospects. Improved connectivity is also driving an increase in residential projects in Tier 2 and Tier 3 cities. Housing sales across top metros reached an 11-year high of 1.73 lakh units in H1 2024, underscoring strong demographic-driven demand.

The segment encompasses affordable housing to luxury apartments, with heightened demand for gated communities and green buildings. Rising land costs have made vertical high-rises increasingly common in metropolitan areas, while plotted developments gain popularity in satellite towns benefiting from improved infrastructure and reduced commute times. Developers are progressively focusing on smart homes incorporating sustainable features, energy-efficient designs, and premium amenities to meet evolving buyer preferences for modern, environmentally conscious living spaces.

Business Insights:

Access the comprehensive market breakdown Request Sample

- Sales

- Rental

The sales segment leads with a share of 70.0% of the total India real estate market in 2025.

The sales segment maintains dominance in the India real estate market, driven by strong end-user demand and investor preference for property ownership offering long-term capital appreciation. Cities like Mumbai, Bengaluru, and Pune witness robust sales activity fueled by affordable housing schemes and growing urban populations. In FY23, home sales reached a record high of Rs 3.47 Lakh Crore (USD 42 Billion), representing a 48% increase from 2022, demonstrating sustained buyer confidence in property acquisition.

The segment benefits from favorable lending rates, government incentives, and increasing homeownership aspirations among the expanding middle class. Non-resident Indian investments have strengthened sales activity, motivated by attractive exchange rates and long-term asset diversification strategies. The introduction of RERA has significantly enhanced buyer confidence by ensuring timely project delivery, quality compliance, and greater transparency in transactions, creating a more secure environment for property purchases across residential and commercial categories.

Mode Insights:

- Online

- Offline

The offline mode holds the largest share at 84.2% of the total India real estate market in 2025.

Offline transactions continue to dominate the India real estate market, reflecting buyer preference for physical site visits, direct interactions with developers and agents, and traditional documentation processes. High-value property purchases typically require in-person due diligence, legal verification, and negotiations that consumers prefer conducting face-to-face. The offline channel benefits from established broker networks and developer sales offices that provide personalized service and immediate query resolution.

Despite growing digital adoption, the complexity and financial significance of real estate transactions maintain offline dominance. Mumbai's property registrations exceeded 105,608 from January to September 2024, a 12% year-on-year increase. However, the online segment is gradually gaining traction as PropTech platforms enhance property discovery, virtual tours, and digital documentation, particularly among younger demographics and NRI investors seeking remote transaction capabilities.

Regional Insights:

- North India

- West and Central India

- South India

- East India

The West and Central India dominates with a 32.0% share of the total India real estate market in 2025.

West and Central India witnesses high demand, driven by dominant urban centers including Mumbai, Pune, Ahmedabad, Indore, and Bhopal. The Mumbai Metropolitan Region and Pune serve as top drivers of residential and commercial real estate demand based on robust economic activity, strong industrial presence, and excellent connectivity. Gujarat has emerged as a hotbed of real estate activity with significant expansion in logistics and manufacturing sectors attracting developer interest and institutional investments.

Central India cities including Indore and Bhopal are gaining popularity with accelerating infrastructure development and increasing disposable incomes among growing middle-class populations. Mumbai continues witnessing strong demand in premium properties, reflecting sustained buyer confidence. Pune and Ahmedabad continue attracting substantial investments through manufacturing expansion and IT sector growth, while emerging micro-markets benefit from metro connectivity projects and improved social infrastructure driving residential absorption rates across affordable and mid-segment housing categories.

Market Dynamics:

Growth Drivers:

Why is the India Real Estate Market Growing?

Rapid Urbanization and Demographic Expansion

India's rapid urbanization serves as a fundamental driver of real estate market growth, with increasing migration to urban centers creating substantial demand for new housing across the country. The nation's young demographic profile drives unprecedented demand for both housing and commercial spaces. City households are fragmenting into nuclear families favoring compact apartment configurations, fundamentally reshaping residential demand patterns. Developers are increasingly focusing on developing tier II and tier III cities, drawn by attractive land prices and expedited regulatory procedures, while this urban growth drives the creation of mixed-use corridors that seamlessly integrate housing with retail and office spaces. Developers are increasingly targeting Tier-2 cities, which now represent 44% of recent land acquisitions, attracted by lower entry costs and faster approvals.

Government Policy Support and Regulatory Reforms

Supportive government policies continue to catalyze real estate sector growth through multiple initiatives targeting both demand and supply sides. Under PM Awas Yojana Urban 2.0, the government committed Rs. 10 Lakh Crore investment to address housing needs for one crore families. The Union Budget allocated significant funds to the Urban Challenge Fund for transforming cities through redevelopment and infrastructure projects. RERA implementation has enhanced transparency and accountability, ensuring timely project delivery and quality compliance. Recent Reserve Bank of India repo rate cuts have reduced home loan EMIs, boosting buyer confidence and affordability across market segments while stimulating housing demand nationwide.

Rising Foreign Direct Investment and Institutional Capital

Increasing foreign direct investment and institutional capital flows are strengthening the India real estate market's growth trajectory. Private equity inflows into the sector have witnessed substantial year-on-year growth, reflecting sustained investor confidence in the market's long-term potential. India has positioned itself as a leading GCC hub with numerous centers operating nationwide, contributing significantly to overall office leasing activity. The growing REIT ecosystem and fractional ownership platforms are further diversifying investment channels, democratizing real estate access, and attracting retail investors seeking exposure to commercial and residential property markets through structured investment vehicles.

Market Restraints:

What Challenges the India Real Estate Market is Facing?

Rising Construction Costs and Material Price Volatility

Developer profit margins have been severely impacted by the steady increase in construction prices. Material and labor expenses have surged considerably in recent years, with wage inflation creating additional financial burden. Steel price fluctuations and volatile diesel costs create budgeting challenges, particularly for mid-tier firms lacking scale procurement capabilities and strategic supplier partnerships.

Land Availability and Acquisition Challenges

Land availability remains a critical constraint, especially in urban areas experiencing rapid growth in residential and commercial demand. Complex land acquisition processes, prolonged disputes, and elevated costs in prime locations limit development opportunities. Developers are increasingly forming joint-development alliances with landowners to share risks and navigate acquisition challenges more effectively.

Regulatory Complexity and Approval Delays

Despite RERA implementation, regulatory complexities and delays in project approvals continue to hinder market progress. Inconsistent enforcement across states, multiple clearance requirements, and extended approval timelines adversely impact project viability and developer confidence. The industry requires streamlined processes and single-window clearance mechanisms to accelerate construction timelines and improve delivery efficiency.

Competitive Landscape:

The India real estate market exhibits moderate to high competitive intensity, with national developers competing alongside regional players across residential, commercial, and industrial segments. Market fragmentation persists, yet scale advantages accrue to large developers capable of navigating approvals, digitizing sales processes, and meeting green-building standards. Key players are pursuing strategic acquisitions, portfolio diversification, and sustainable construction practices to strengthen positioning. Joint-development agreements and partnerships are becoming increasingly common as developers seek to optimize land acquisition costs and share development risks effectively.

Recent Developments:

- In June 2025, Adani Cement and CREDAI (Confederation of Real Estate Developers' Associations of India) formed a strategic alliance to advance sustainable and superior building methods across the country. To change business practices, the partnership will establish a Green India Council and a Skilling Council.

- In January 2025, Equinox India Developments and NAM Estates combined to establish Embassy Developments Limited, one of the biggest publicly traded real estate companies in India. The deal strengthens the company's position in Tier-2 cities in South India while broadening its residential and commercial portfolios.

India Real Estate Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Properties Covered | Residential, Commercial, Industrial, Land |

| Businesses Covered | Sales, Rental |

| Modes Covered | Online, Offline |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Brigade Enterprises Limited, DLF Limited, Experion Developers Pvt Ltd., Godrej Properties, Jaypee Infratech Ltd. (Jaiprakash Associates Limited), Larsen & Toubro Limited, Lodha Group, Merlin Group, Oberoi Realty Limited, Prestige Estates Projects Ltd., SOBHA Limited, Sunteck Realty, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The India real estate market size was valued at USD 532.61 Billion in 2025.

The India real estate market is expected to grow at a compound annual growth rate of 10.08% from 2026-2034 to reach USD 1,264.00 Billion by 2034.

The residential segment dominated the market with a 78.8% share in 2025, driven by rapid urbanization, government housing initiatives like PMAY, expanding middle class, and growing demand for affordable and premium housing across metropolitan and tier II cities.

Key factors driving the India real estate market include rapid urbanization, rising disposable incomes, favorable government policies including RERA and PMAY, increasing foreign direct investments, infrastructure development, and expanding IT and manufacturing sectors fueling residential and commercial demand.

Major challenges include rising construction costs with material and labor expenses, land availability constraints especially in urban areas, regulatory complexities causing project approval delays, and high property prices impacting affordability for certain buyer segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)