India Over the Top (OTT) Market Size, Share, Trends and Forecast by Component, Platform Type, Deployment Type, Content Type, Revenue Model, Service Type, Vertical, and Region, 2026-2034

Market Overview:

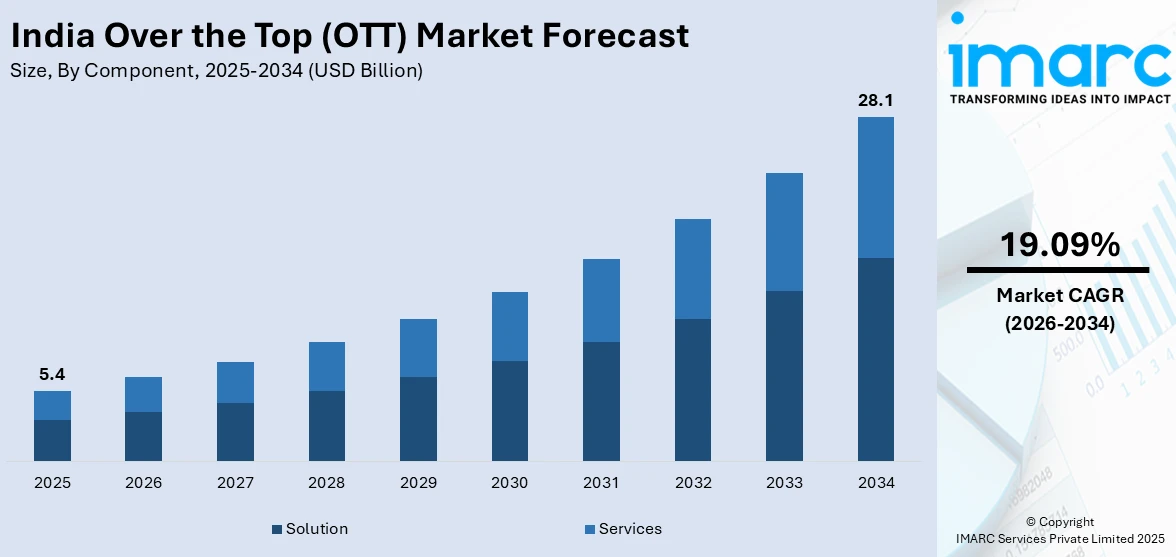

The India over the top (OTT) market size reached USD 5.4 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 28.1 Billion by 2034, exhibiting a growth rate (CAGR) of 19.09% during 2026-2034.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 5.4 Billion |

| Market Forecast in 2034 | USD 28.1 Billion |

| Market Growth Rate (2026-2034) | 19.09% |

Over-the-top (OTT) refers to a media streaming platform that delivers personalized television (TV), web series, and film content directly to users over the internet either free or on subscription basis. Unlike traditional broadcasting mediums, OTT content can be downloaded and viewed on users demand across various internet-connected devices, such as tablets, smartphones, consoles, and personal computers (PCs). Apart from this, it offers video, audio, Voice over Internet Protocol (VoIP) services, games, and communication, which can be accessed and watched easily at cost-effective rates. On account of these properties, it is extensively used for personal and commercial purposes.

To get more information on this market Request Sample

India Over the Top (OTT) Market Trends:

The increasing availability of internet connectivity, along with the rising demand for content within media and entertainment domain, especially during the consequent implementation of mandatory lockdowns due to the sudden outbreak of coronavirus disease (COVID-19) pandemic, are anticipated to drive the India OTT market growth. Additionally, the widespread adoption of OTT platforms across information technology (IT), telecom, government, and banking, financing, servicing, and insurance (BFSI) industries for advertising purposes is further propelling the market growth. In line with this, the introduction of subscription-video on demand (SVoD) and freemium viewing models by OTT platforms is acting as another growth-inducing factor. Additionally, significant technological advancements have enabled the easy streaming and viewing of content on internet-based communication applications and various other electronic gadgets, including smart TV, consoles, and mobiles, which is contributing to the market growth. Moreover, the emergence of various online OTT platforms with the list of subscription-based narrowed genre series, podcasts, videos, music films, and television programs are propelling the market growth. Apart from this, strategic collaborations of OTT operators with multi-channel video programming distributors (MVPDs) for providing viewers with live and linear feeds are creating a positive outlook for the market across India.

Key Market Segmentation:

IMARC Group provides an analysis of the key trends in each sub-segment of the India over the top (OTT) market report, along with forecasts at the country and regional level from 2026-2034. Our report has categorized the market based on component, platform type, deployment type, content type, revenue model, service type and vertical.

Breakup by Component:

- Solution

- Services

Breakup by Platform Type:

- Smartphones

- Smart TV's

- Laptops, Desktops and Tablets

- Gaming Consoles

- Set-Top Boxes

- Others

Breakup by Deployment Type:

- Cloud

- On-Premise

Breakup by Content Type:

- Voice Over IP

- Text and Images

- Video

- Others

Breakup by Revenue Model:

- Subscription

- Procurement

- Rental

- Others

Breakup by Service Type:

- Consulting

- Installation and Maintenance

- Training and Support

- Managed Services

Breakup by Vertical:

Access the comprehensive market breakdown Request Sample

- Media & Entertainment

- Education & Training

- Health & Fitness

- IT & Telecom

- E-Commerce

- BFSI

- Government

- Others

Breakup by Region:

- North India

- West and Central India

- South India

- East India

Competitive Landscape:

The competitive landscape of the industry has also been examined along with the profiles of the key players.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage | Component, Platform Type, Deployment Type, Content Type, Revenue Model, Service Type, Vertical, Region |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

We expect the India over the top (OTT) market to exhibit a CAGR of 19.09% during 2026-2034.

The expanding media and entertainment sector, along with the widespread adoption of OTT services and high-quality streaming content, is primarily driving the India over the top (OTT) market.

The sudden outbreak of the COVID-19 pandemic has led to the increasing popularity of over-the-top (OTT) platforms for numerous entertainment purposes, such as streaming music, live broadcasting, watching movies and series, etc., during the lockdown scenario across the nation.

Based on the component, the India over the top (OTT) market can be segmented into solution and services. Currently, solution holds the majority of the total market share.

Based on the platform type, the India over the top (OTT) market has been divided into smartphones, Smart TV’s, laptops, desktops and tablets, gaming consoles, set-top boxes, and others. Among these, smartphones exhibit a clear dominance in the market.

Based on the deployment type, the India over the top (OTT) market can be segregated into cloud and on-premise, where on-premise currently holds the largest market share.

Based on the content type, the India over the top (OTT) market has been categorized into voice over IP, text and images, video, and others. Currently, text and images account for the majority of the total market share.

Based on the revenue model, the India over the top (OTT) market can be bifurcated into subscription, procurement, rental, and others. Among these, subscription currently exhibits a clear dominance in the market.

Based on the service type, the India over the top (OTT) market has been segmented into consulting, installation and maintenance, training and support, and managed services. Currently, managed services hold the majority of the total market share.

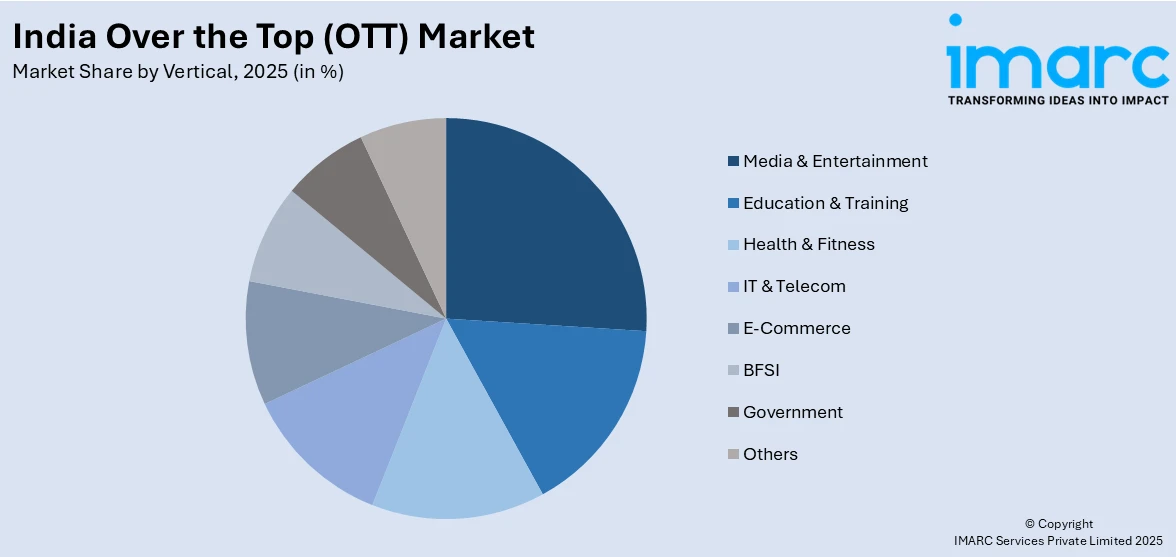

Based on the vertical, the India over the top (OTT) market can be divided into media & entertainment, education & training, health & fitness, IT & telecom, e-commerce, BFSI, government, and others. Among these, the media & entertainment sector exhibits a clear dominance in the market.

On a regional level, the market has been classified into North India, West and Central India, South India and East India, where South India currently dominates the India over the top (OTT) market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)