India Lead Acid Battery Market Size, Share, Trends and Forecast by Product, Construction Method, Sales Channel, Application, and Region, 2026-2034

India Lead Acid Battery Market Summary:

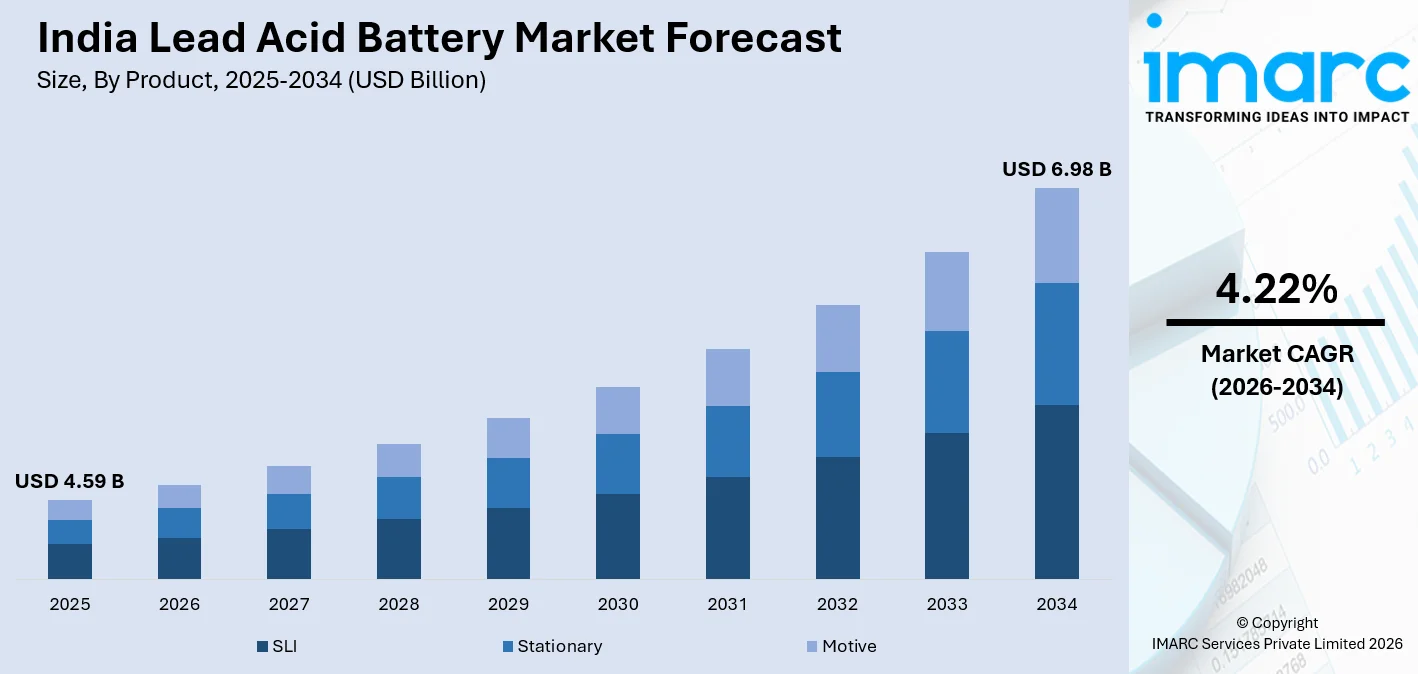

The India lead acid battery market size was valued at USD 4.59 Billion in 2025 and is projected to reach USD 6.98 Billion by 2034, growing at a compound annual growth rate of 4.22% from 2026-2034.

The India lead acid battery market is experiencing a robust market growth due to the rapid growth of the automotive industry, increasing investment in telecom infrastructure, and the ambitious plans to develop the renewable energy sector in the country. Increasing automobile ownership, rising demand for uninterrupted power supply systems in the commercial and industrial sectors, and increasing solar power capacity in the country are contributing to the robust market growth of the India lead acid battery market share.

Key Takeaways and Insights:

- By Product: SLI dominates the market with a share of 56.0% in 2025, establishing their dominance as the essential starting, lighting, and ignition solution for India's rapidly expanding vehicle fleet.

- By Construction Method: Flooded leads the market with a share of 61.0% in 2025, driven by their cost-effectiveness and widespread availability across automotive and industrial applications in India.

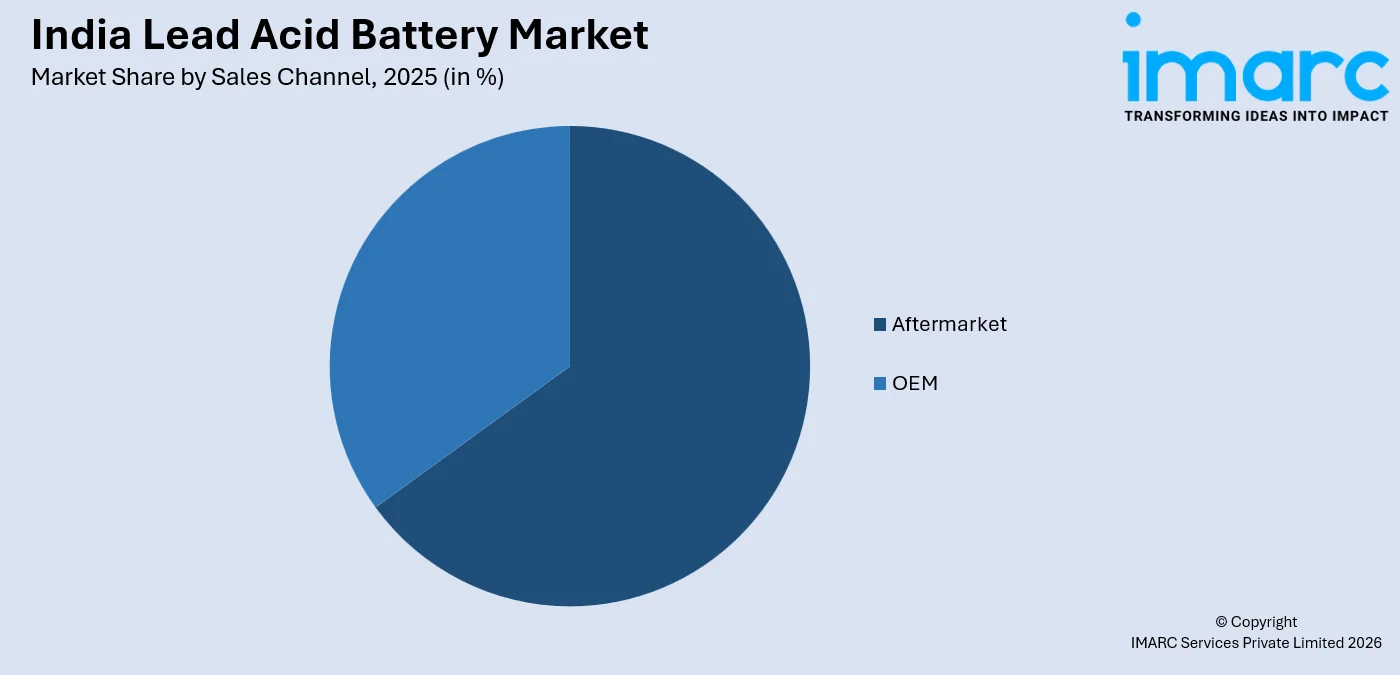

- By Sales Channel: Aftermarket leads the market with a share of 64.0% in 2025, reflecting the strong replacement demand generated by India's large and rapidly growing installed vehicle base.

- By Application: Automotive dominates the market with a share of 58.0% in 2025, underscoring the pivotal role of lead-acid batteries in supporting India's position as the world's third-largest and fastest-growing automobile market.

- By Region: South India leads the market with a share of 33.0% in 2025, fueled by robust automotive demand, high levels of industrial activity, and the concentration of major battery manufacturing facilities in the region

- Key Players: The India lead acid battery market features a mix of established domestic manufacturers and specialized players who compete through continuous product innovation, capacity expansion, strategic partnerships, and extensive nationwide distribution networks to strengthen their foothold across automotive and industrial segments.

To get more information on this market Request Sample

The India lead acid battery market is advancing steadily, supported by the country's expanding vehicle fleet, growing telecommunications infrastructure, and rising renewable energy adoption. The automotive sector generates consistent replacement demand for SLI batteries, while telecom networks rely heavily on VRLA batteries to ensure uninterrupted backup power across urban and rural installations. Notably, in May 2025, Exide Industries announced plans to expand its lead-acid battery business revenue to ₹20,000 crore within the next two to three years, highlighting strong demand across automotive replacement, UPS, and solar backup segments in India. Government-led renewable energy initiatives are further driving energy storage requirements, particularly in off-grid and solar applications. The growing adoption of advanced battery technologies, including AGM and VRLA variants, is enhancing performance, extending service life, and broadening application scope. These converging dynamics position India as one of Asia's most dynamic lead acid battery markets.

India Lead Acid Battery Market Trends:

Rising Adoption of Advanced Battery Technologies Including AGM and VRLA

The India lead acid battery market is undergoing a notable technological transition, with manufacturers increasingly investing in advanced variants such as Absorbent Glass Mat (AGM) and Valve Regulated Lead-Acid (VRLA) batteries. For instance, in July 2025, Varroc Engineering Limited entered the Indian two-wheeler aftermarket battery segment with the launch of a new range of maintenance-free VRLA batteries, designed for motorcycles and scooters and distributed through its nationwide retail network. These technologies offer maintenance-free operation, superior deep-cycle performance, and longer service life compared to conventional flooded batteries, making them well-suited for automotive start-stop systems, telecom tower backup, and critical UPS applications, collectively elevating the market toward higher-performance energy storage solutions.

Expanding Telecom Infrastructure Driving VRLA Battery Demand

India's rapid telecommunications expansion, particularly the accelerated rollout of advanced network infrastructure across urban and rural areas, is generating substantial demand for VRLA batteries deployed in tower backup power systems. Operators increasingly favour VRLA variants for their sealed, spill-proof design, low maintenance requirements, and reliable performance under demanding outdoor conditions. For instance, in May 2025, the government confirmed that Bharat Sanchar Nigam Limited had installed about 93,450 4G towers across India as part of its nationwide network expansion program aimed at achieving nearly 100,000 sites, significantly strengthening mobile connectivity infrastructure across the country. The ongoing expansion of digital connectivity programs into underserved regions continues to amplify tower deployments, reinforcing VRLA battery demand as a critical component of India's telecommunications infrastructure.

Growing Lead Battery Integration into Renewable Energy and Solar Storage Systems

India's ambitious push toward expanding non-fossil fuel energy capacity is driving increasing deployment of lead-acid batteries in off-grid and solar storage applications. The proliferation of solar home systems, rural electrification programs, and community microgrids is broadening demand for cost-effective energy storage across underserved regions. In 2024, the Government of India launched the PM Surya Ghar: Muft Bijli Yojana, a nationwide rooftop solar initiative aimed at installing solar systems in one crore households by FY2026–27, with a government outlay of about ₹75,021 crore to accelerate distributed renewable energy adoption across residential areas. The affordability established supply chain, and high recyclability of lead-acid technology continue to make it a preferred storage solution for cost-sensitive renewable energy applications spanning residential, agricultural, and community-level installations throughout the country.

Market Outlook 2026-2034:

The India lead acid battery market is expected to sustain robust growth, driven by continuous expansion across the automotive, telecommunications, and renewable energy sectors. Rising vehicle production, growing replacement cycles, and accelerating network infrastructure deployment are anticipated to underpin steady demand. Government investments in national infrastructure, expanding data center development, and the proliferation of solar-powered off-grid systems will create additional opportunities. Technological innovations including graphene-enhanced batteries, advanced AGM systems, and improved VRLA designs will further elevate performance standards, strengthening the market's competitive positioning across diverse application segments. The market generated a revenue of USD 4.59 Billion in 2025 and is projected to reach a revenue of USD 6.98 Billion by 2034, growing at a compound annual growth rate of 4.22% from 2026-2034.

India Lead Acid Battery Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

SLI |

56.0% |

|

Construction Method |

Flooded |

61.0% |

|

Sales Channel |

Aftermarket |

64.0% |

|

Application |

Automotive |

58.0% |

|

Region |

South India |

33.0% |

Product Insights:

- SLI

- Stationary

- Motive

The SLI dominates with a market share of 56.0% of the total India lead acid battery market in 2025.

SLI (Starting, Lighting, and Ignition) batteries represent the dominant product category in India's lead acid battery market, primarily due to their indispensable role in powering the nation's expansive and continuously growing vehicle fleet. These batteries are engineered to deliver reliable cranking power, consistent electrical supply, and ignition support across a wide range of vehicle types, including two-wheelers, passenger cars, and commercial vehicles. Their cost-effectiveness, widespread availability, and compatibility with existing vehicle architectures make them the preferred choice for both OEM supply and aftermarket replacement.

Replacement demand for vehicles driven by a strong base in India ensures a predictable and consistent pattern of consumption for SLI batteries in all regions. With rising ownership in urban and semi-urban areas, the pace of battery replacement continues to ensure consistent market activity. Players are also working on improving SLI battery technology by developing better plate materials, advanced grid materials, and calcium-based technologies, thereby increasing product life and strengthening consumer confidence in lead-acid battery technology for mainstream automotive applications in the country.

Construction Method Insights:

- Flooded

- Valve Regulated Sealed Lead-acid Battery (VRLA)

The flooded leads with a share of 61.0% of the total India lead acid battery market in 2025.

Flooded lead-acid batteries maintain their market leadership in India due to their affordability, proven reliability, and well-established manufacturing and distribution ecosystem. These batteries remain the preferred choice across a broad spectrum of applications, including conventional passenger vehicles, two-wheelers, commercial transport, and entry-level industrial equipment. Their straightforward construction, ease of maintenance, and compatibility with India's existing vehicle service infrastructure make them particularly attractive in price-sensitive market segments where total cost of ownership is a primary purchasing consideration.

The extensive dealer and retailer network supporting flooded battery distribution across urban, semi-urban, and rural markets further reinforces their dominant position. Manufacturers continue to invest in improving flooded battery formulations through enhanced electrolyte compositions, optimized plate structures, and improved separator materials, extending operational life while maintaining competitive pricing. These incremental advancements, combined with the deep-rooted familiarity of mechanics and consumers with flooded battery maintenance practices, ensure their continued dominance across India's large and diverse battery replacement market.

Sales Channel Insights:

Access the comprehensive market breakdown Request Sample

- OEM

- Aftermarket

The aftermarket dominates with a market share of 64.0% of the total India lead acid battery market in 2025.

The aftermarket segment commands the dominant position in India's lead acid battery distribution landscape, driven by the substantial replacement demand generated by the country's extensive installed base of vehicles, industrial equipment, and backup power systems. With battery service life typically spanning a few years under Indian operating conditions, the large and continuously growing vehicle fleet creates a consistent and recurring replacement cycle across both organized and unorganized retail channels. Authorized service centers, independent battery retailers, and multi-brand outlets collectively serve this demand across geographies.

Consumer accessibility and price competitiveness are key factors shaping aftermarket dynamics in India. Leading manufacturers maintain extensive retail networks spanning metropolitan cities, tier-two towns, and rural markets, ensuring broad geographic coverage and prompt availability during replacement cycles. The growing proliferation of online retail platforms has further expanded aftermarket reach, enabling consumers to compare products, access warranties, and arrange doorstep installation. These distribution strengths, combined with strong brand loyalty built over decades, allow established players to sustain their aftermarket dominance effectively.

Application Insights:

- Automotive

- UPS

- Telecom

- Others

The automotive leads with a share of 58.0% of the total India lead acid battery market in 2025.

Automotive applications represent the largest and most consistent demand driver for lead acid batteries in India, underpinned by the country's expansive vehicle fleet and the inevitable replacement cycles it generates. Lead acid batteries serve as the primary energy source for starting, lighting, and ignition functions across the full spectrum of automotive categories, including two-wheelers, three-wheelers, passenger cars, and heavy commercial vehicles. Their affordability, established supply chains, and broad compatibility with conventional internal combustion engine vehicles make them the preferred choice across price-sensitive segments that constitute the majority of India's automobile market.

The automobile segment will also gain from the rising demand for advanced battery types in premium and semi-premium vehicles. This is due to the fact that automobile manufacturers are increasingly launching AGM and improved flooded battery types that are optimized for advanced start-stop engine types, micro-hybrid configurations, and vehicles with high electrical accessory requirements. With Indian automobile users increasingly adopting feature-rich vehicles that have more complex power requirements, the overall market for high-performance automobile lead-acid batteries is also set to grow in tandem with the conventional replacement market, thereby expanding the overall market for this segment.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

South India exhibits a clear dominance with a 33.0% share of the total India lead acid battery market in 2025.

South India leads the India lead acid battery market, driven by a combination of strong automotive demand, significant industrial activity, and the presence of major battery manufacturing operations within the region. The southern states, including Tamil Nadu, Karnataka, Andhra Pradesh, and Telangana, are home to prominent automotive clusters, technology parks, and industrial corridors that generate consistent demand for both automotive and industrial batteries. The region's high vehicle ownership rates, particularly in major metropolitan areas, create robust replacement demand through an extensive network of authorized dealers and independent retailers.

South India's rapidly expanding information technology and data center ecosystem further drives demand for UPS and stationary lead acid batteries, as companies invest in reliable power backup infrastructure to support uninterrupted operations. The region's growing renewable energy installations, including rooftop solar systems and community solar projects, are also contributing to off-grid battery storage demand. These combined demand drivers across automotive, industrial, telecommunications, and renewable energy segments collectively reinforce South India's position as the most significant regional contributor to the overall India lead acid battery market.

Market Dynamics:

Growth Drivers:

Why is the India Lead Acid Battery Market Growing?

Rapid Expansion of India's Automotive Sector and Replacement Demand

India's position as one of the fastest-growing automobile markets globally is a primary driver sustaining lead acid battery demand. The continuous addition of two-wheelers, passenger cars, and commercial vehicles creates an expanding installed fleet that generates a predictable and growing replacement cycle. In January 2024, the Society of Indian Automobile Manufacturers reported that India’s total passenger vehicle sales crossed 4 million units in 2023, marking the highest annual sales ever recorded in the country and reflecting the rapid expansion of the national vehicle fleet. The enduring affordability, reliability, and broad compatibility of lead acid batteries across conventional and emerging mobility segments further reinforce their indispensable role in supporting India's dynamic and rapidly evolving automotive landscape.

Growing Telecommunications Infrastructure and Digital Connectivity Investment

India's expansive and rapidly growing telecommunications network represents a substantial demand driver for lead acid batteries, particularly VRLA variants deployed in tower backup power systems. Accelerating network densification programs and national digitalization initiatives are expanding infrastructure into remote and underserved areas that depend on reliable battery-backed systems for uninterrupted connectivity. In January 2026, telecom infrastructure companies reported increasing deployment of high-temperature VRLA batteries for telecom tower power systems to improve backup performance and reliability at network sites operating under challenging environmental conditions. GTL Infrastructure has been rolling out such VRLA-based battery solutions across its tower network to support stable power supply for telecom infrastructure. The sealed, low-maintenance characteristics of VRLA batteries make them the preferred choice for outdoor tower installations, ensuring consistent performance across diverse climatic and geographic conditions throughout the country.

Government-Led Renewable Energy and National Infrastructure Development

India's ambitious clean energy transition and large-scale infrastructure development programs are creating significant new demand for lead acid batteries across off-grid solar systems, microgrids, and backup power installations. The proliferation of solar home systems and rural electrification programs is broadening storage requirements in cost-sensitive communities. In September 2024, Honeywell commissioned a battery energy storage system integrated with a solar microgrid in Lakshadweep for the Solar Energy Corporation of India, enabling renewable power distribution across remote islands and supporting reliable electricity supply through energy storage solutions. Simultaneously, government investments spanning transport and energy infrastructure generate sustained demand for UPS and backup power solutions across construction, industrial, and municipal applications, where lead acid batteries remain preferred for their cost competitiveness and proven operational reliability.

Market Restraints:

What Challenges the India Lead Acid Battery Market is Facing?

Intensifying Competition from Lithium-Ion Battery Technology

Lead acid batteries face growing competitive pressure from lithium-ion alternatives, which offer higher energy density, longer cycle life, and lower weight advantages in EV and portable electronics applications. As India's electric vehicle ecosystem matures and lithium-ion production costs decline, premium applications are gradually shifting away from lead-acid technology. This trend threatens to erode the India lead acid battery market share in higher-value segments over the forecast period, particularly as government incentives support domestic lithium-ion cell manufacturing.

Environmental Regulations and Lead Toxicity Concerns

Increasing regulatory scrutiny over lead handling, battery disposal, and recycling processes presents operational challenges for manufacturers and informal sector recyclers. India's Battery Waste Management Rules require compliance with collection, channelization, and recycling obligations, raising operational costs for market participants. Improper disposal of lead acid batteries poses significant environmental and public health risks, prompting stricter enforcement that increases compliance burdens across the value chain and may disadvantage smaller operators lacking formal recycling infrastructure.

Raw Material Price Volatility and Lead Supply Chain Constraints

The lead acid battery market is exposed to significant volatility in global lead prices, as lead constitutes approximately 60-70% of battery manufacturing costs. Fluctuations in lead commodity prices directly impact production costs, profit margins, and end-user pricing. Disruptions in secondary lead supply from recycled sources and dependence on imports for virgin lead can further compound cost pressures, particularly during periods of heightened global demand or supply chain disruptions affecting key raw material flows to India's manufacturing sector.

Competitive Landscape:

The India lead acid battery market is moderately consolidated, with a few dominant manufacturers collectively commanding significant positions across both automotive and industrial segments. Market leaders leverage extensive manufacturing infrastructure, established OEM partnerships, and broad aftermarket distribution networks to maintain competitive advantage. Specialized players complement the competitive field by focusing on niche segments including defense, inverter batteries, and industrial applications. Competition is intensifying with the entry of technology-focused manufacturers introducing advanced AGM and graphene-enhanced battery products, compelling established players to accelerate their own innovation pipelines. Strategic capacity expansions, product diversification, and strengthened distribution reach remain the primary competitive differentiators shaping market dynamics.

Recent Developments:

- In March 2026, battery recycler NavPrakriti partnered with NASH Energy to develop a circular battery ecosystem in India. The partnership focuses on sustainable battery manufacturing and recycling to ensure responsible end-of-life management for batteries used in energy storage and industrial applications, including legacy chemistries like lead-acid.

India Lead Acid Battery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | SLI, Stationary, Motive |

| Construction Methods Covered | Flooded, Valve Regulated Sealed Lead-Acid Battery (VRLA) |

| Sales Channels Covered | OEM, Aftermarket |

| Applications Covered | Automotive, UPS, Telecom, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The India lead acid battery market size was valued at USD 4.59 Billion in 2025.

The India lead acid battery market is expected to grow at a compound annual growth rate of 4.22% from 2026-2034 to reach USD 6.98 Billion by 2034.

SLI batteries, holding a 56.0% share, lead the market as the essential starting, lighting, and ignition solution for India's expanding automotive fleet, benefiting from the country's consistently growing vehicle ownership and robust replacement cycle demand.

Key factors driving the India lead acid battery market include India's rapid automotive sector expansion, extensive telecommunications infrastructure development supporting VRLA battery demand, and government-led renewable energy investments driving off-grid solar storage requirements across rural and semi-urban areas.

Major challenges include intensifying competition from lithium-ion battery technology in premium applications, regulatory pressures related to lead toxicity and disposal compliance, and raw material price volatility affecting manufacturing cost structures across the supply chain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)