India Home Healthcare Market Size, Share, Trends and Forecast by Product and Service, Indication, and Region, 2026-2034

India Home Healthcare Market Summary:

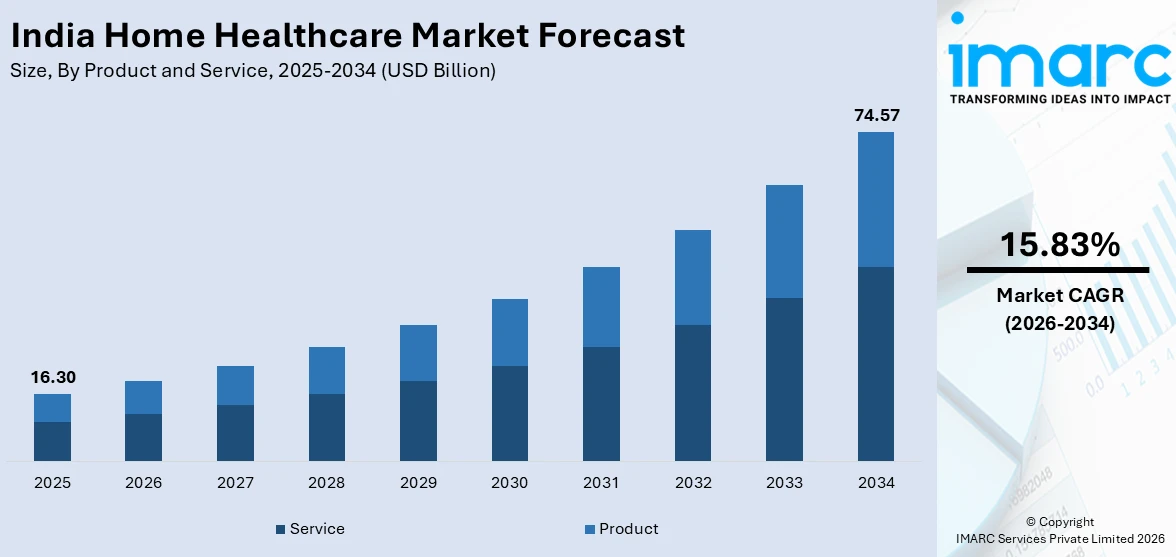

The India home healthcare market size was valued at USD 16.30 Billion in 2025 and is projected to reach USD 74.57 Billion by 2034, growing at a compound annual growth rate of 15.83% from 2026-2034.

The India home healthcare market is experiencing robust expansion fueled by a rapidly aging population, increasing prevalence of chronic diseases, and a growing preference for patient-centric care delivered in familiar home settings. Advances in telemedicine, remote monitoring technologies, and digital health platforms are enabling high-quality clinical services outside traditional hospital environments. Rising healthcare costs, limited hospital bed availability, and the need for cost-effective alternatives are further accelerating the shift toward home-based care models, strengthening India home healthcare market share.

Key Takeaways and Insights:

- By Product and Service: Service dominates the market with a share of 62.0% in 2025, driven by rising demand for skilled nursing, rehabilitation therapy, and chronic disease management delivered at patients’ doorsteps.

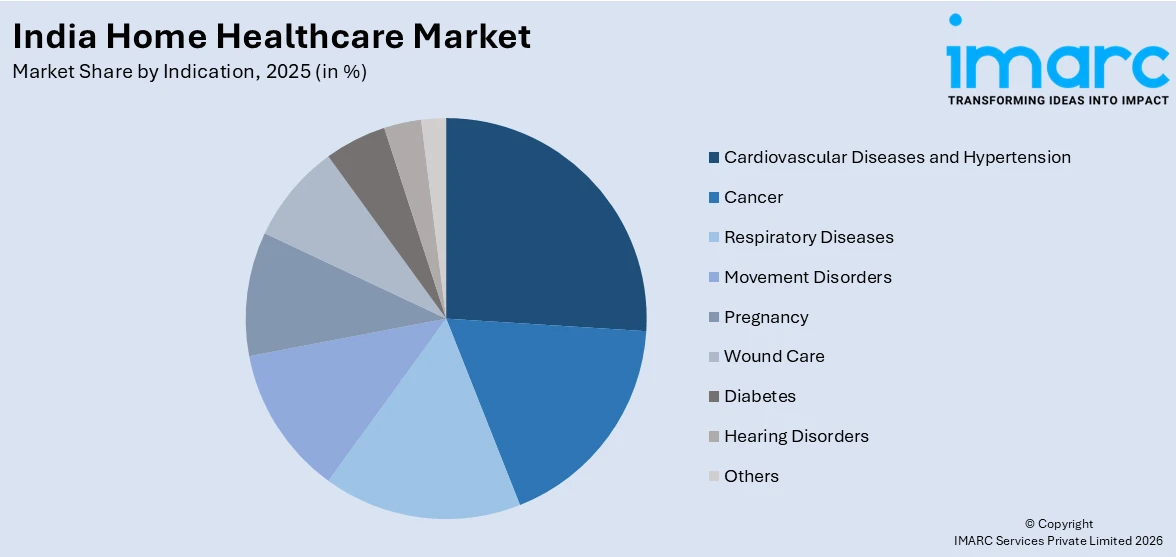

- By Indication: Cardiovascular diseases and hypertension lead the market with a share of 24.0% in 2025, reflecting the high prevalence of heart conditions requiring continuous home-based monitoring and management.

- By Region: South India represents the largest region with a market share of 35.0% in 2025, supported by advanced healthcare infrastructure, higher digital literacy, and a larger aging population in states like Kerala and Tamil Nadu.

- Key Players: The India home healthcare market is moderately fragmented, with established hospital networks, specialized home care providers, and technology-enabled startups competing to expand service portfolios, geographic reach, and digital care capabilities across urban and semi-urban regions.

To get more information on this market Request Sample

The India home healthcare market is undergoing a transformative phase, driven by the convergence of demographic shifts, technological innovation, and evolving consumer expectations. India’s elderly population is projected to reach approximately 230 million by 2036, creating unprecedented demand for geriatric care, post-operative support, and chronic disease management delivered in home settings. The expansion of the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana in October 2024 to provide free treatment benefits of up to ₹5 lakh per year to all senior citizens aged 70 and above has further catalyzed demand for accessible home-based healthcare services. The growing integration of telehealth platforms, AI-powered diagnostics, and wearable health monitoring devices is transforming service delivery, enabling real-time patient surveillance and timely clinical interventions while reducing hospital readmissions and healthcare costs.

India Home Healthcare Market Trends:

Digital Health Integration and Telehealth Expansion

The integration of digital health solutions and telehealth platforms is rapidly reshaping India’s home healthcare landscape. Providers are leveraging video consultations, electronic health records, and AI-driven triage tools to deliver seamless remote care. For instance, in February 2025, Star Health and Allied Insurance expanded its Home Health Care initiative to 100 locations across India, becoming the country’s largest home healthcare provider by offering cashless doorstep medical care within three hours to over 85% of its customer base. This trend is enabling broader access to quality care, particularly in underserved regions, supporting India home healthcare market growth.

Rise of Hospital-at-Home and Virtual ICU Models

Hospital-at-home programs and virtual intensive care unit models are gaining significant traction as healthcare providers seek to optimize bed capacity while maintaining clinical oversight. For instance, in September 2023, Apollo Hospitals launched India’s first Comprehensive Connected Care Services, integrating real-time patient monitoring systems that route vitals to centralized command centers for remote triage and clinical decision-making. These models enable stable patients to receive hospital-grade care at home, reducing hospitalization costs and improving patient comfort while maintaining continuous medical vigilance through connected monitoring technologies.

Growing Adoption of Wearable Health Monitoring Devices

Wearable health monitoring devices, including smart blood pressure monitors, glucose meters, and ECG-enabled smartwatches, are increasingly being integrated into home healthcare delivery models. For instance, in June 2023, OMRON Healthcare announced plans to construct a production facility in India at ORIGINS by Mahindra, with blood pressure monitor manufacturing commencing in March 2025. The proliferation of affordable, user-friendly monitoring devices enables continuous vital signs tracking, empowering patients and healthcare professionals to manage chronic conditions proactively and detect complications early.

Market Outlook 2026-2034:

India’s home healthcare market is set for steady growth as aging demographics, evolving patient expectations, and supportive healthcare reforms reshape service delivery models. Broader insurance inclusion for home-based treatments and the strengthening of digital health ecosystems under the Ayushman Bharat Digital Mission are improving accessibility and care coordination. Additionally, increasing preference for convenient, personalized medical support at home is encouraging providers to expand service networks across metropolitan centers as well as underserved rural areas, reinforcing long-term market expansion prospects. The market generated a revenue of USD 16.30 Billion in 2025 and is projected to reach a revenue of USD 74.57 Billion by 2034, growing at a compound annual growth rate of 15.83% from 2026-2034.

India Home Healthcare Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product and Service |

Service |

62.0% |

|

Indication |

Cardiovascular Diseases and Hypertension |

24.0% |

|

Region |

South India |

35.0% |

Product and Service Insights:

- Product

- Therapeutic Products

- Testing, Screening, and Monitoring Products

- Mobility Care Products

- Service

- Skilled Nursing

- Rehabilitation Therapy

- Hospice and Palliative Care

- Unskilled Care

- Respiratory Therapy

- Infusion Therapy

- Pregnancy Care

Service dominates with a market share of 62.0% of the total India home healthcare market in 2025.

The service segment’s leadership reflects the growing demand for professional clinical care delivered directly to patients’ homes. Skilled nursing, rehabilitation therapy, and chronic disease management services are increasingly preferred by families seeking personalized attention for elderly members and patients recovering from surgeries or managing long-term conditions. For instance, in June 2024, Indiana Hospital and Heart Institute partnered with Critical Care Unified to launch home care services covering ICU-at-home, specialized cancer care, cardiac care, and medical equipment supply across northern Kerala, demonstrating the expanding scope of home-based clinical services.

The preference for home healthcare services is further reinforced by the cost advantages over hospitalization. Home-based ICU care typically costs approximately one-third of traditional hospital ICU services, making it a financially viable alternative for extended treatment regimens. The integration of telehealth consultations with in-person skilled nursing visits is creating comprehensive hybrid care models that enhance patient outcomes while reducing the burden on overcrowded hospital facilities across India’s metropolitan and tier-two cities.

Indication Insights:

Access the comprehensive market breakdown Request Sample

- Cancer

- Respiratory Diseases

- Movement Disorders

- Cardiovascular Diseases and Hypertension

- Pregnancy

- Wound Care

- Diabetes

- Hearing Disorders

- Others

Cardiovascular diseases and hypertension lead the market with a 24.0% share of the total India home healthcare market in 2025.

The dominance of cardiovascular diseases and hypertension as the leading indication segment underscores the immense burden of heart-related conditions in India. According to the World Health Organization, approximately 220 million people in India live with hypertension, yet only 12% have their blood pressure under control. Cardiovascular diseases account for nearly 27% of total deaths in the country, creating urgent demand for continuous home-based monitoring, medication adherence support, and lifestyle management programs that reduce hospital readmission rates and improve long-term patient outcomes.

The India Hypertension Control Initiative, implemented in collaboration with the Indian Council of Medical Research and the World Health Organization, highlights the growing emphasis on structured blood pressure management across the country. The initiative underscores the importance of continuous monitoring and long-term cardiovascular care. Home healthcare providers are well positioned to support these goals through routine nurse visits, remote blood pressure tracking, medication adherence support, and individualized care plans that improve patient outcomes and reduce complications.

Regional Insights:

- North India

- West and Central India

- South India

- East India

South India represents the largest share at 35.0% of the total India home healthcare market in 2025.

South India’s market leadership is driven by its advanced healthcare infrastructure, higher digital literacy rates, and a larger proportion of aging populations concentrated in states such as Kerala, Tamil Nadu, and Karnataka. These states have pioneered family medicine training programs and established extensive networks of private hospitals that increasingly offer home healthcare extensions. Kerala and Tamil Nadu are among the oldest states demographically in India, with the United Nations reporting that the southern and western regions have the highest shares of elderly residents, intensifying demand for geriatric home care services.

The region also benefits from a proactive telemedicine ecosystem, with cities like Bengaluru, Chennai, and Hyderabad serving as innovation hubs for digital healthcare solutions. South India’s dominance in the telemedicine market, supported by widespread smartphone penetration and government-backed digital health initiatives, has enabled seamless integration of remote consultations with home-based care delivery, establishing a strong foundation for sustained home healthcare market expansion across the region.

Market Dynamics:

Growth Drivers:

Why is the India Home Healthcare Market Growing?

Rapidly Aging Population and Expanding Geriatric Care Needs

India’s demographic transition is creating unprecedented demand for home healthcare services as the elderly population grows at an accelerating pace. The United Nations Population Fund projects that India’s elderly population will constitute approximately 20% of the total population by 2050, with the population aged 80 and above expected to grow by approximately 279% between 2022 and 2050. By January 2025, over 40 lakh senior citizens had successfully enrolled in the expanded scheme. The rise in nuclear family structures, coupled with urban migration of working-age adults, is weakening traditional intergenerational care systems, further driving demand for professional home healthcare services for the elderly.

Rising Prevalence of Chronic Diseases Requiring Long-Term Care

The escalating burden of non-communicable diseases in India is a primary catalyst for home healthcare adoption. Cardiovascular diseases, diabetes, respiratory illnesses, and hypertension collectively account for nearly 63% of total deaths in the country. The World Health Organization highlights the significant burden of hypertension and type 2 diabetes in India, underscoring the widespread need for continuous disease management. These chronic conditions demand consistent monitoring, medication supervision, and lifestyle support, which are effectively delivered through structured home-based care models. A large share of the elderly population also lives with at least one long-term illness, reinforcing the importance of ongoing medical engagement beyond occasional hospital visits and accelerating the growth of comprehensive home-based chronic care programs nationwide.

Technological Advancements in Remote Monitoring and Digital Health

Rapid progress in telemedicine, remote patient monitoring, and digital health infrastructure is reshaping home healthcare delivery across India. The Ayushman Bharat Digital Mission has strengthened the foundation for interoperable health records and digital identities, enabling better care coordination. Several states are also exploring reimbursement models for remote monitoring under public insurance schemes, supporting wider adoption of home-based services. Additionally, the eSanjeevani platform has enhanced virtual consultation access. Together, these advancements support real-time vital tracking, predictive analytics, and improved collaboration between home care professionals and hospital-based specialists.

Market Restraints:

What Challenges the India Home Healthcare Market is Facing?

Shortage of Trained Healthcare Professionals for Home-Based Settings

India faces a significant deficit of qualified healthcare professionals trained specifically for home-based care delivery. The limited availability of skilled nurses, physiotherapists, and geriatric care specialists constrains the capacity of home healthcare providers to scale operations. Training programs tailored to home care environments remain underdeveloped compared to hospital-based education, creating quality and consistency challenges in service delivery.

Limited Insurance Coverage and Reimbursement Frameworks

Despite growing demand, comprehensive insurance coverage for home healthcare services remains limited in India. Most health insurance policies primarily cover hospitalization expenses, leaving home-based treatments, skilled nursing, and rehabilitation services inadequately reimbursed. The absence of standardized reimbursement frameworks discourages both providers and consumers from fully embracing home healthcare as a mainstream alternative to institutional care.

Inadequate Digital Infrastructure in Rural and Semi-Urban Areas

While urban centers benefit from robust internet connectivity and digital health platforms, rural and semi-urban regions continue to face significant infrastructure gaps. Limited broadband access, inconsistent network reliability, and low digital literacy levels hinder the deployment of telehealth and remote monitoring solutions in these areas. This digital divide restricts the equitable expansion of technology-enabled home healthcare services beyond metropolitan regions.

Competitive Landscape:

The India home healthcare market exhibits a moderately fragmented competitive landscape characterized by the presence of established hospital chains, specialized home care providers, and technology-driven startups. Market participants are pursuing strategies centered on geographic expansion, service portfolio diversification, and integration of digital health technologies to differentiate their offerings. Strategic partnerships between healthcare providers and insurance companies are creating cashless home care delivery models that enhance accessibility. Competition is intensifying as providers invest in AI-powered platforms, remote monitoring capabilities, and specialized clinical programs to capture growing demand for personalized, convenient, and cost-effective home-based healthcare solutions.

Recent Developments:

- July 2025: Apollo Home Healthcare introduced its ‘Integrated Palliative Care at Home’ initiative in Delhi in collaboration with Apollo Indraprastha Hospital. The programme focuses on providing comprehensive palliative care services within patients’ homes. It will also be expanded to Apollo Athenaa, a specialized center dedicated to women’s oncology care. The company has outlined plans to further extend the service model to additional metropolitan markets across India in the coming phase.

- July 2024: Star Health Insurance launched comprehensive Home Health Care services across more than 50 cities in partnership with leading providers including Care24, Portea, CallHealth, and Athulya Homecare, offering 100% cashless treatment for infectious ailments directly at customers’ doorsteps.

India Home Healthcare Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product and Services Covered |

|

| Indications Covered | Cancer, Respiratory Diseases, Movement Disorders, Cardiovascular Diseases and Hypertension, Pregnancy, Wound Care, Diabetes, Hearing Disorders, Others |

| Regions Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Home Healthcare Market Research Report and Industry Forecast Report

The India home healthcare market size was valued at USD 16.30 Billion in 2025.

The India home healthcare market is expected to grow at a compound annual growth rate of 15.83% from 2026-2034 to reach USD 74.57 Billion by 2034.

Service held the largest share at 62.0% in 2025, driven by the growing demand for skilled nursing, rehabilitation therapy, hospice care, and chronic disease management services delivered at patients’ homes across India.

Key factors driving the India home healthcare market include the rapidly aging population, rising prevalence of chronic diseases, advances in telemedicine and remote monitoring technologies, expanding insurance coverage, and growing consumer preference for cost-effective, personalized home-based care.

Major challenges include a shortage of trained home healthcare professionals, limited insurance reimbursement for home-based services, inadequate digital infrastructure in rural areas, lack of standardized quality benchmarks, and low consumer awareness in semi-urban and rural regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)