India Gaming Market Size, Share, Trends and Forecast by Device Type, Platform, Revenue Type, Type, Age Group, and Region, 2026-2034

India Gaming Market Size, Share, Trends & Forecast (2026-2034)

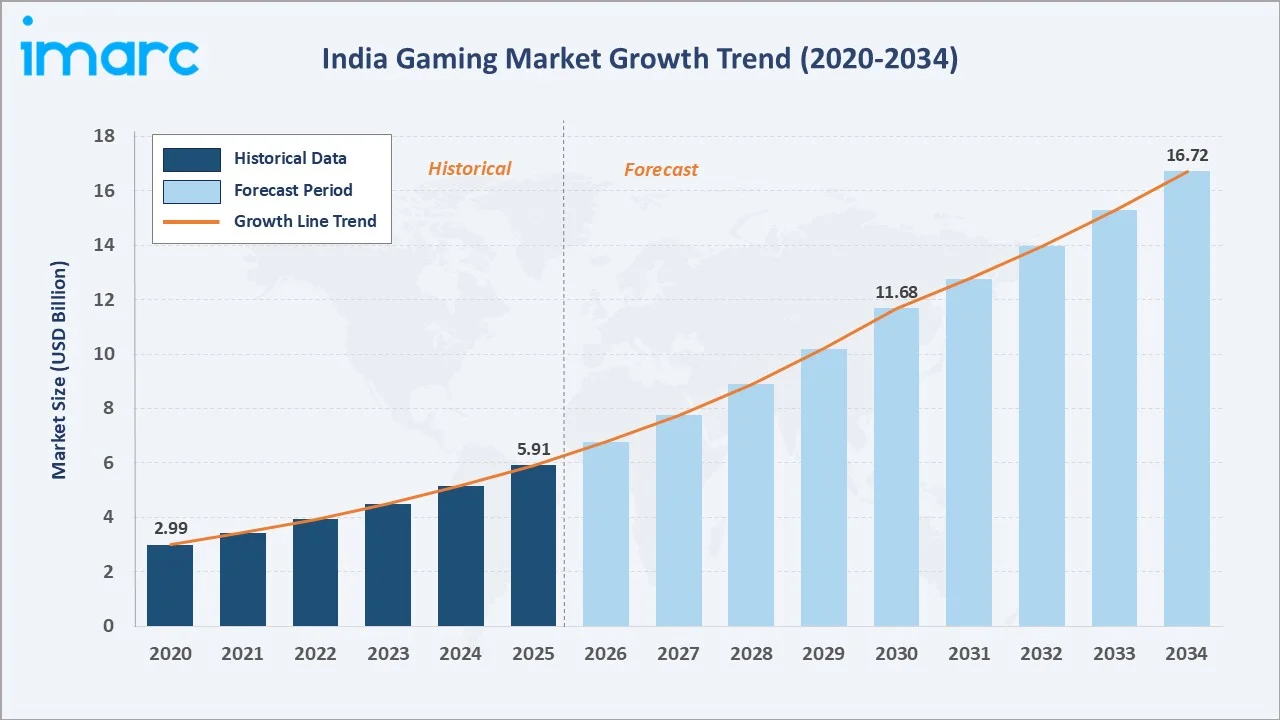

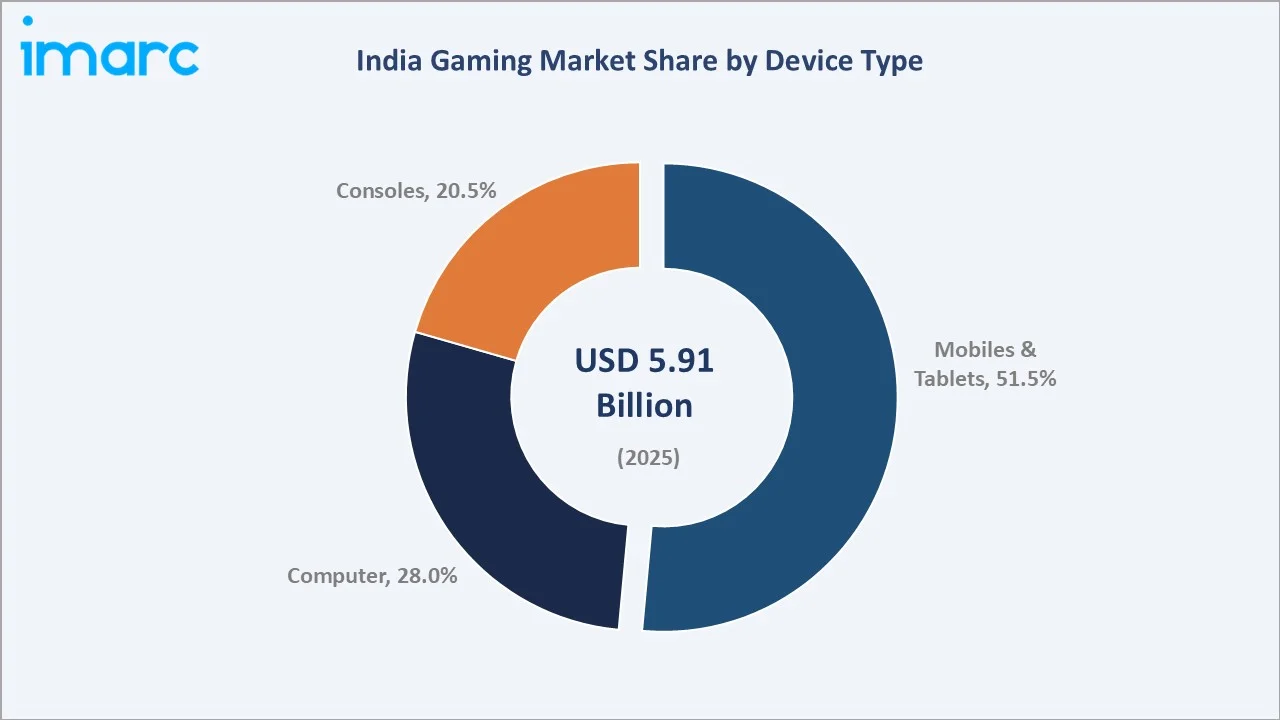

The India gaming market size was valued at USD 5.91 Billion in 2025 and is projected to reach USD 16.72 Billion by 2034, growing at a CAGR of 14.59% during 2026-2034. Rapid smartphone adoption, affordable mobile data plans, and a large, digitally native population are the primary catalysts reshaping India's gaming ecosystem.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.91 Billion |

|

Forecast Market Size (2034) |

USD 16.72 Billion |

|

CAGR (2026-2034) |

14.59% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (32.0% share, 2025) |

|

Fastest Growing Region |

South India |

To get more information on this market, Request Sample

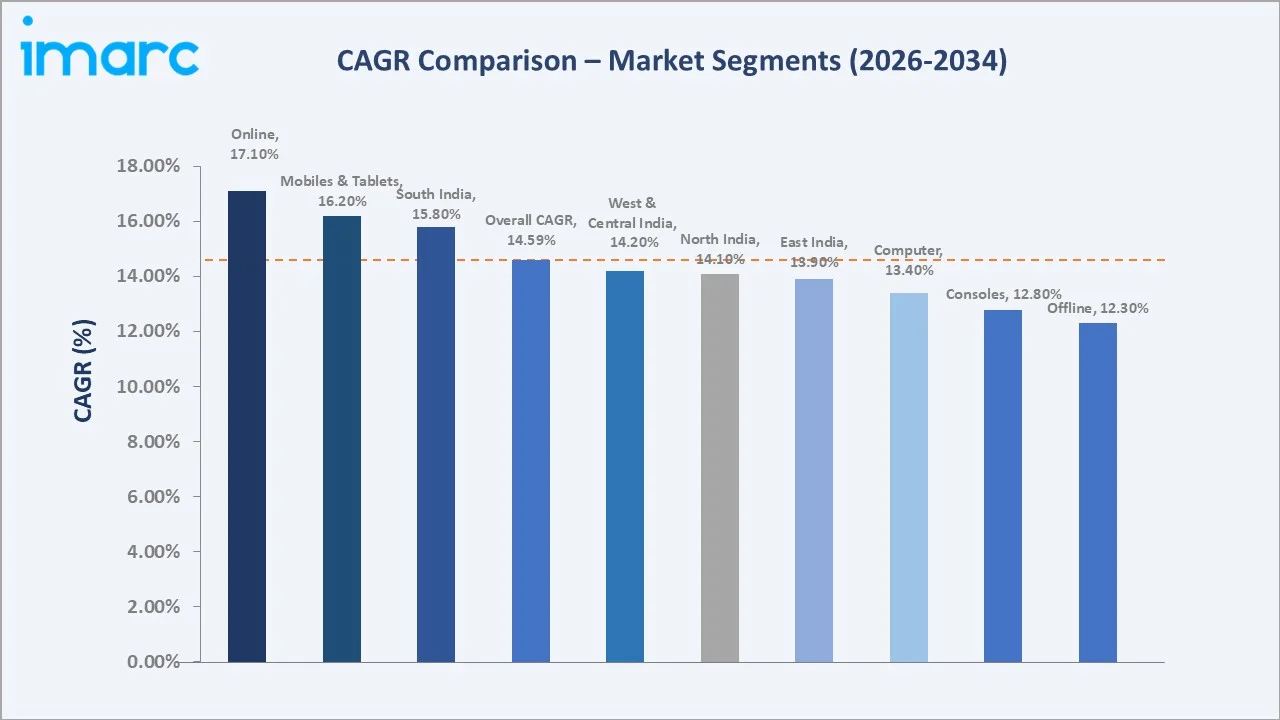

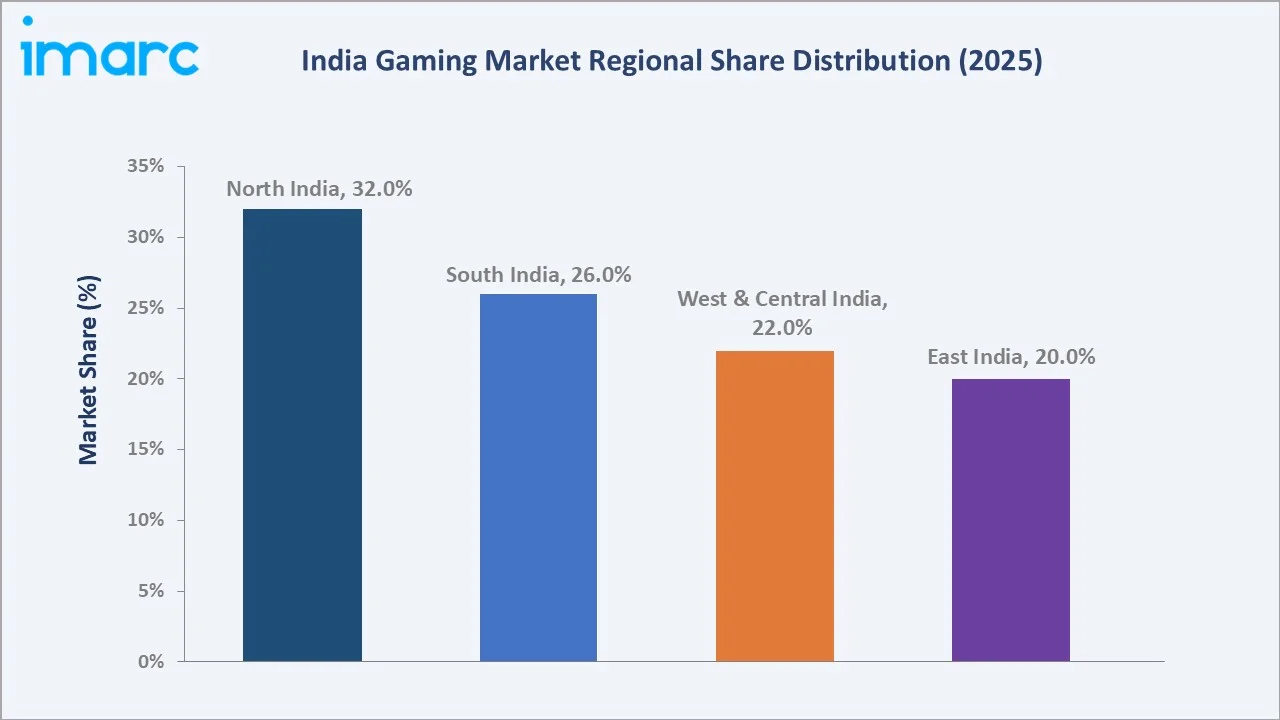

North India leads with a 32.0% market share in 2025, while mobiles and tablets command 51.46% of device-type demand. Offline gaming holds the leading platform share at 53.65%. India's gaming ecosystem benefits from one of the world's largest smartphone user bases, near-universal UPI payment adoption, and rapid 5G infrastructure deployment, making it a preferred destination for global gaming publishers and domestic developers alike.

With applications spanning mobile, PC, console, and cloud platforms, and a growing esports infrastructure, the India gaming market forecast reflects accelerating adoption across tier-two and tier-three cities through localized content, vernacular interfaces, and affordable subscription gaming models.

Executive Summary

The India gaming market is on a sustained growth path, underpinned by smartphone proliferation, 5G infrastructure expansion, and a youthful, digitally engaged consumer base. The market reached USD 5.91 Billion in 2025 and is forecast to reach USD 16.72 Billion by 2034, reflecting a robust CAGR of 14.59% over the forecast period.

North India dominates with a 32.0% revenue share in 2025, driven by high population density in the Delhi-NCR corridor, extensive esports event infrastructure, and wide UPI adoption, enabling seamless in-game transactions. South India, holding 26.0%, represents the fastest-growing opportunity, anchored by Bengaluru and Hyderabad's dense game-development ecosystems. West & Central India accounts for 22.0%, while East India holds 20.0%, with the latter emerging as a high-potential geography driven by vernacular content adoption.

Mobiles and tablets command the device segment at 51.46%, reflecting India's mobile-first digital economy. The offline platform leads at 53.65%, preferred by consumers in markets with inconsistent connectivity. Key players, including Nazara Technologies, KRAFTON, Inc., Sporta Technologies Private Limited, Sea Limited, and nCore Games, continue to invest in localized content, esports infrastructure, and telecom partnerships to expand reach and monetization across India's diverse gamer demographic.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Device Type) |

Mobiles and Tablets – 51.46% share (2025) |

|

Largest Segment (Platform) |

Offline – 53.65% share (2025) |

|

Leading Region |

North India – 32.0% revenue share (2025) |

|

Fastest Growing Region |

South India (game-dev hub + regulatory clarity) |

|

Market Opportunity |

Cloud gaming projected at CAGR 46.2% through 2033 |

Key Analytical Observations Supporting The Above Data:

- Mobiles and tablets account for 51.46% of the India gaming market in 2025, preferred for their affordability, compatibility with 4G/5G networks, and an expansive library of free-to-play titles optimized for entry-level hardware, supported by India's 659 million smartphone owners as of 2025.

- Offline gaming maintains the leading platform share at 53.65% in 2025, driven by consumer preference for downloadable games that deliver uninterrupted gameplay independent of internet connectivity, particularly in tier-two and tier-three cities where network reliability remains inconsistent.

- North India holds 32.0% of the domestic gaming market in 2025, led by Delhi-NCR's concentration of esports venues, gaming cafes, and tournament infrastructure, underpinned by dense 5G coverage and near-universal UPI adoption for in-game payments.

- South India is the fastest-growing region, supported by Bengaluru and Hyderabad's concentration of game-development studios, with approximately 12 gaming-focused training centers in Karnataka.

- In-game purchase is the dominant revenue stream at 63.49%, reflecting growing acceptance of microtransactions and virtual goods purchases enabled by UPI's frictionless payment infrastructure across diverse demographic segments.

India Gaming Market Overview

The India gaming market encompasses the development, distribution, and monetization of digital interactive entertainment across mobile, PC, console, and cloud platforms. Originally dominated by mobile casual games, the market has evolved into a sophisticated multi-segment ecosystem spanning casual and mid-core mobile titles, competitive PC and console gaming, organized esports leagues, fantasy sports platforms, and cloud-streamed premium content.

Macroeconomic drivers include India's status as the world's second-largest smartphone market with 659 million owners as of 2025, the proliferation of ultra-affordable 4G and 5G data plans driven by intense telecom competition, and a median population age of approximately 28 years, creating a structurally large addressable gamer base.

Market Dynamics

To evaluate market opportunities, Request Sample

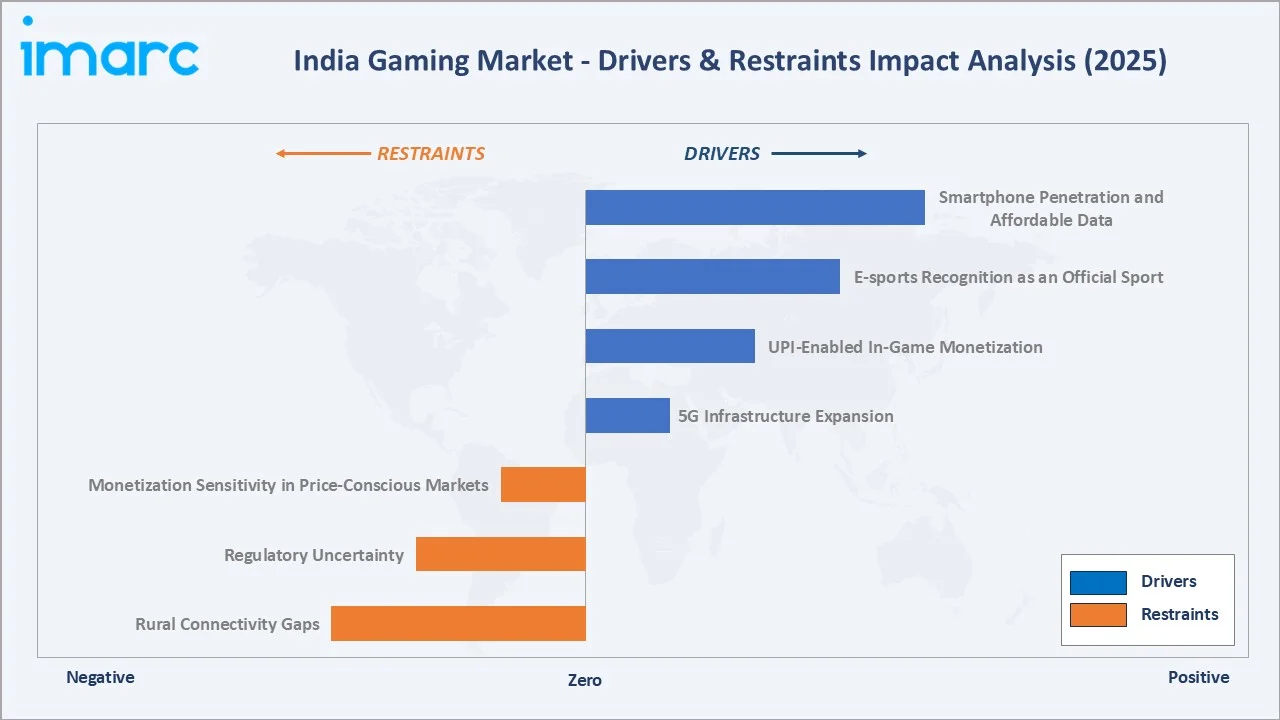

Market Drivers

- Smartphone Penetration and Affordable Data: India recorded 659 million smartphone owners in 2025, ranking second globally, with entry-level devices shipping with sufficient RAM for mid-core gameplay.

- E-sports Recognition as an Official Sport: The e-sports market is experiencing rapid growth and is projected to hit USD 1,088 million by 2033. Events such as BGIS 2025 are offering INR 2 crore, while streaming platforms are attracting millions of viewers.

- UPI-Enabled In-Game Monetization: The National Payments Corporation of India recorded 21.70 billion UPI transactions in January 2026 alone. Seamless in-app payment integration via UPI has accelerated the adoption of microtransactions, in-game purchases, and subscription-based gaming services.

- 5G Infrastructure Expansion: In December 2025, India added 4,112 new 5G base transceiver stations (BTS), bringing the national total to 518,854, as per DoT, reducing cloud gaming session latency to under 30 milliseconds in major metros and enabling telecom-bundled premium gaming subscriptions at scale.

These drivers reinforce a self-sustaining growth cycle, infrastructure investment drives new gamer cohorts, which attracts publisher content investment, which in turn drives deeper engagement and monetization that justifies further infrastructure and content spend across the ecosystem.

Market Restraints

- Rural Connectivity Gaps: Despite 5G reaching 99.9% of districts, consistent high-speed connectivity in rural tier-three markets remains limited, constraining online gaming adoption in underserved geographies and restricting the addressable market for bandwidth-intensive cloud gaming products.

- Regulatory Uncertainty: State-level divergence in classifying skill-based games versus games of chance has created compliance complexity for developers and publishers. Inconsistent regulatory frameworks across states impact investment decisions, content deployment timelines, and cross-market monetization strategies.

- Monetization Sensitivity in Price-Conscious Markets: A large proportion of India's gamer base remains in the free-to-play segment, requiring publishers to develop cost-effective engagement models to convert casual users to paying customers without eroding accessibility for lower-income demographics.

Market Opportunities

- Cloud Gaming Infrastructure Expansion: India's cloud gaming market is projected at a CAGR of 46.04% through 2034. NVIDIA announced plans to establish a GeForce RTX-powered data center in India in January 2025, extending its GeForce Now cloud gaming service and enabling premium title access without costly hardware investment for end consumers.

- AVGC Sector Government Initiative: The Ministry of Information and Broadcasting committed INR 250 crore to regional game studios under the AVGC sector task force, accelerating localized IP creation, regional-language content development, and domestic studio scaling capabilities.

Market Challenges

- Responsible Gaming and Addiction Concerns: Growing public awareness of gaming addiction among younger demographics has prompted regulatory discussion around screen-time limits and content age-gating.

- Talent Scarcity for Specialized Development Roles: India's rapid gaming sector expansion has created acute demand for game designers, narrative engineers, 3D artists, and esports infrastructure specialists that outpace domestic training capacity.

Emerging Market Trends

1. Rise of e-sports as Mainstream Entertainment

According to the latest FICCI–EY report, the Indian online gaming industry reached 488 million users in 2024, adding 33 million new gamers across casual and real-money segments on all devices. Major brands across consumer electronics, beverages, and telecommunications are actively sponsoring events, expanding prize pools, and elevating competitive gaming as a career pathway.

2. Vernacular Content Driving Regional Adoption

Maharashtra has proposed a ₹500 crore fund aimed at strengthening the gaming ecosystem by supporting innovation, skill development, and infrastructure creation, which is catalyzing this vernacular content shift. Downloads for regional-language titles more than doubled in 2025, with AppsFlyer reporting that users in Asia spend around 40% more on in-app purchases compared to users in other regions globally, validating the commercial viability of the vernacular gaming market and reinforcing India gaming market trends toward hyper-localization.

3. Cloud Gaming Expansion Through Telecom Partnerships

In April 2024, Vodafone Idea partnered with CareGame to launch a cloud gaming platform, exemplifying the sector's trajectory toward infrastructure-light gaming. NVIDIA's January 2025 announcement of a GeForce RTX-powered India data center further validates cloud gaming's strategic importance.

4. AI-Powered Personalization and Adaptive Gaming Experiences

AI-driven matchmaking systems in esports platforms are improving competitive balance and player retention. The convergence of AI with mobile gaming's massive data scale positions India as a laboratory for next-generation adaptive gaming experiences that can be deployed globally, aligning with the broader India gaming market trends toward technologically sophisticated, personalized entertainment.

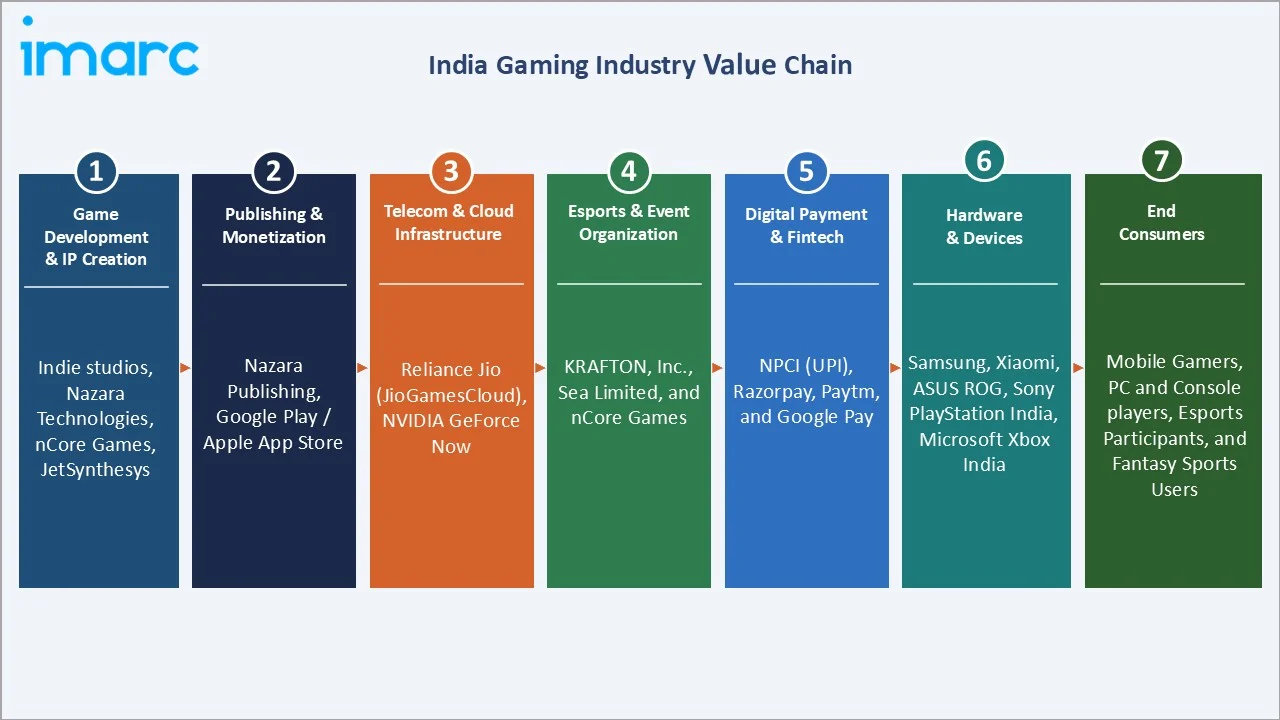

Industry Value Chain Analysis

The India gaming market value chain spans intellectual property creation through end-consumer engagement, with each stage supported by specialized operators whose capabilities directly influence content quality, reach, monetization efficiency, and player lifetime value.

|

Stage |

Key Players / Examples |

|

Game Development & IP Creation |

Indie studios, Nazara Technologies, nCore Games, JetSynthesys |

|

Publishing & Monetization |

Nazara Publishing, Google Play / Apple App Store |

|

Telecom & Cloud Infrastructure |

Reliance Jio (JioGamesCloud), NVIDIA GeForce Now |

|

Esports & Event Organization |

KRAFTON, Inc., Sea Limited, and nCore Games. |

|

Digital Payment & Fintech |

NPCI (UPI), Razorpay, Paytm, and Google Pay are integrated into in-game payment rails |

|

Hardware & Devices |

Samsung, Xiaomi, ASUS ROG, Sony PlayStation India, Microsoft Xbox India |

|

End Consumers |

Mobile gamers, PC and console players, esports participants, and fantasy sports users |

Technology Landscape in the India Gaming Industry

5G and Edge Computing for Cloud Gaming

Microsoft Azure and Amazon Web Services have placed GPU compute stacks inside Airtel and Vodafone Idea facilities, reducing cloud gaming latency below 30 milliseconds in major metros. NVIDIA's planned GeForce RTX data center in India will further accelerate cloud-streamed AAA title access on mobile devices, enabling a fundamentally hardware-free premium gaming pathway.

UPI and Seamless In-Game Payment Technology

India's Unified Payments Interface processed 21.7 billion transactions in January 2026, providing the payment infrastructure backbone for in-game purchases, subscription billing, and real-money gaming transactions. Deep UPI SDK integration within mobile game applications has reduced payment drop-off rates to near zero, enabling even first-time spenders to complete microtransactions in under three seconds without leaving the gaming environment.

AI and Machine Learning in Game Development

Indian game studios are deploying AI for procedural level generation, adaptive difficulty calibration, and personalized content recommendation within mobile titles. AI-powered anti-cheat systems are being adopted by esports platforms to protect competitive integrity. Natural language processing is enabling multilingual customer support automation, reducing operational costs for publishers serving India's linguistically diverse gamer base across 22 official languages and hundreds of regional dialects.

AR/VR and Immersive Gaming Technology

In February 2025, Lothar MetaWorlds introduced next-generation VR gaming experiences integrating AI, AR, and spatial computing for immersive gameplay. AjnaLens showcased its high-performance spatial computing solution, AjnaHPSC, at GDC in March 2024, highlighting advanced XR innovations and reinforcing India’s presence in the global immersive technology ecosystem.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Device Type |

Mobile and Tablets |

51.46% |

2025 |

|

Platform |

Offline |

53.65% |

2025 |

|

Revenue Type |

In-Game Purchase |

63.49% |

2025 |

|

Type |

Adventure/Role Playing Games |

41.2% |

2025 |

|

Age Group |

Adult |

75.19% |

2025 |

|

Region |

North India |

32% |

2025 |

By Device Type

To access detailed market analysis, Request Sample

Mobiles and tablets dominate the device segment with a 51.5% share in 2025. India's mobile-first digital economy has established mobile as the de facto primary gaming platform. Entry-level devices with sufficient RAM for mid-core gameplay, combined with extensive 4G/5G network coverage, have democratized gaming access across income levels and geographies.

Computers account for 28.0% of the device segment, driven by the core gaming community and esports participants requiring high-performance hardware for competitive play. Consoles hold 20.54%, with adoption concentrated among urban, higher-income consumers and gaming enthusiasts attracted to console-exclusive franchises and premium gaming experiences on large-format displays.

By Platform

Offline gaming leads the platform segment with a 53.7% share in 2025, driven by Indian consumers' preference for downloadable titles that deliver uninterrupted gameplay independent of internet connectivity. This preference is especially pronounced in tier-two and tier-three cities, where network reliability remains inconsistent.

Online gaming commands 46.4% of the platform segment in 2025, propelled by the rapid expansion of 5G infrastructure, increasing broadband penetration, and the rising popularity of multiplayer battle royale titles, esports platforms, real-money gaming, and subscription-based cloud gaming services. The growth of JioGamesCloud, Vodafone's Cloud Play, and NVIDIA's GeForce Now expansion into India is progressively shifting the platform mix toward online and cloud-delivered formats through the forecast period.

Regional Market Insights

North India's market leadership (32.0%, 2025) reflects the region's high metropolitan population density, well-developed digital infrastructure, and concentration of esports event venues in the Delhi-NCR corridor. UPI adoption is near-universal across North India's urban centers, enabling frictionless in-game monetization.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Landscape |

|

North India |

32.0% |

Metro density, esports infrastructure, and UPI adoption |

Conducive; central online gaming regulations applicable |

|

South India |

26.0% |

Game-dev ecosystem, 5G depth, regulatory clarity |

Karnataka reversed 2024 skill-gaming restrictions |

|

West & Central India |

22.0% |

Corporate esports leagues, VC inflow, real-money gaming |

Maharashtra and Gujarat regulatory frameworks stable |

|

East India |

20.0% |

Vernacular content, growing 5G rollout, youth demographics |

Evolving; Bengali-language titles driving mainstream adoption |

South India is the fastest-growing region, with Karnataka reversing its 2024 restrictions on skill-based gaming and Telangana positioning Hyderabad as a national gaming industry hub. The majority of India's national game-development workforce is concentrated in South India, enabling rapid content localization and IP creation. Global publishers, including KRAFTON and Garena, have established local headquarters in Bengaluru, partnering with telecom operators for device preload agreements.

Competitive Landscape

The Indian gaming market exhibits a dynamic, moderately fragmented competitive structure. Mobile-first market characteristics have lowered certain barriers to entry, resulting in a vibrant ecosystem of domestic independent studios competing alongside global technology giants.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Nazara Technologies |

Nodwin Gaming / WCC (World Cricket Championship) |

Market Leader |

Diversified portfolio; esports + edutainment; listed entity with acquisition strategy |

|

KRAFTON, Inc. |

BGMI (Battlegrounds Mobile India) |

Market Leader |

Battle royale franchise dominance; telecom and OEM device preload partnerships |

|

Sporta Technologies Private Limited |

Dream11 |

Strong Challenger |

Fantasy sports leadership; 200M+ registered users |

|

Sea Limited |

Free Fire |

Strong Challenger |

Tier-2/3 city penetration; relaunched as "Free Fire India" only in July 2025; mass-market battle royale IP |

|

nCore games |

FAU-G: Domination |

Niche Player |

Indigenous IP development; cultural resonance; domestic game publishing capabilities |

The top five players, Nazara Technologies, KRAFTON, Inc., Sporta Technologies Private Limited, Sea Limited, and nCore Games, collectively account for an estimated 40–45% of market revenue in 2025. Regional developers, independent mobile studios, and vernacular gaming platforms account for the remaining share, ensuring a diverse and competitive market landscape.

Key Company Profiles

Nazara Technologies

Nazara Technologies. is India's leading listed gaming and sports media company, headquartered in Mumbai. Nazara is recognized as the only publicly listed Indian gaming company with a multi-vertical gaming strategy spanning entertainment, education, and competitive sports.

- Product Portfolio: World Cricket Championship (WCC) series, esports platform Nodwin Gaming, edutainment brand Kiddopia, fantasy gaming investments.

- Recent Developments: In June 2024, Nazara Publishing partnered with nCore Games to become the global publishing partner for FAU-G Domination, expanding indigenous Indian IP into international markets.

- Strategic Focus: Vertical integration across gaming content, esports, and sports media; international expansion through acquisitions; edutainment segment growth in emerging markets.

KRAFTON, Inc.

KRAFTON, Inc., primarily operates BATTLEGROUNDS MOBILE INDIA (BGMI), India's largest mobile battle royale franchise. KRAFTON, Inc. is a South Korean gaming company headquartered in Seoul. Its India subsidiary, KRAFTON India Private Limited, is based in Bengaluru.

- Product Portfolio: BATTLEGROUNDS MOBILE INDIA (BGMI); India-exclusive esports events, creator economy programs, and branded in-game content integrations.

- Recent Developments: In January 2025, KRAFTON India partnered with Mahindra to introduce the Mahindra BE 6 within BGMI, demonstrating automotive brand integration capabilities.

- Strategic Focus: Localized tournament ecosystem development; creator economy engagement; hardware and automotive brand integration within gaming environments.

Sporta Technologies Private Limited

Sporta Technologies Private Limited. is the parent company of Dream11, India's largest fantasy sports platform with over 200 million registered users. Headquartered in Mumbai, the company has established dominance in skill-based fantasy formats across cricket, football, kabaddi, and basketball.

- Product Portfolio: Dream11, FanCode, DreamX (accelerator), DreamSetGo, DreamPay.

- Recent Developments: In November 2025, the company leased around 169,000 sq ft of office space in Mumbai’s Worli in a major long-term deal valued at over INR 300 crore.

- Strategic Focus: Fantasy sports platform leadership; sports media monetization through FanCode; international fantasy gaming expansion; live sports data integration.

Market Concentration Analysis

The India gaming market exhibits moderate fragmentation, with no single entity commanding an overwhelming revenue share. Mobile gaming's low barrier to entry has generated a large population of independent Indian studios, indie developers, and niche vertical specialists competing alongside global publishing giants. The top five companies collectively account for an estimated 40–45% of market revenue in 2025, with a long tail of 200+ active independent developers, regional platforms, and vertical gaming applications accounting for the balance.

Consolidation activity is accelerating, driven by competitive advantages in vernacular content scale, esports infrastructure, telecom partnership negotiation, and branded IP ownership. Between 2023 and 2025, notable transactions included Nazara's strategic acquisitions of complementary gaming assets and Nodwin Gaming's emergence as an independently valued esports entity. Private equity and venture capital interest in India gaming remains elevated, targeting companies with proprietary IP portfolios, established vernacular content libraries, and monetization-proven user bases in non-metropolitan geographies.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud gaming (CAGR 46.2% through 2033), esports infrastructure and media rights (CAGR ~25%), and vernacular mobile game publishing represent the three highest-growth investment vectors through 2034. Together, these segments address a total addressable market projected to exceed USD 3 Billion by 2030.

Emerging Market Expansion

East India and Central India collectively represent the most under-penetrated domestic geographies, with progressive 5G rollout and rising smartphone ownership creating a multi-year market activation opportunity. Regional-language content strategies, telecom bundling agreements, and affordable subscription gaming models are the preferred investment modalities for capturing incremental users.

Venture and Institutional Investment Trends

- Key investment themes include cloud gaming edge infrastructure, indigenous IP development with cultural resonance, esports media rights and broadcast monetization, and AI-powered game personalization technologies targeting India's multilingual user base.

- The government's AVGC sector initiative, backed by INR 500 crore, is creating co-investment opportunities for institutional investors seeking exposure to India's rapidly scaling gaming content creation ecosystem.

- Global gaming publishers are actively pursuing acquisition targets with established vernacular gaming libraries, proven tier-two/three city user bases, and UPI-integrated monetization frameworks to accelerate India market penetration without building from scratch.

Future Market Outlook (2026-2034)

The India gaming market is positioned for sustained, broad-based growth through 2034. From a base of USD 5.91 Billion in 2025, the market is projected to reach USD 16.72 Billion by 2034, representing total incremental value creation of approximately USD 10.81 Billion over the forecast decade.

Regulatory will drive significant platform development and publisher expansion. Telecom operators and cloud hyperscalers co-locating edge compute infrastructure within 5G networks will progressively eliminate hardware barriers to premium gaming, enabling cloud-streamed console-quality titles on mid-range smartphones at mass market price points.

Long-term, the India gaming market trends are tied to three structural macro themes: the continued democratization of smartphone and data access, driving new gamer cohorts from non-metro and rural geographies, the maturation of the esports ecosystem, creating professional career infrastructure and media viewership scale, and the vernacular content revolution extending gaming's cultural relevance to India's 900+ million non-English-speaking population.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with industry participants in 2024–2025, including mobile game publishers, esports tournament organizers, telecom operators, digital payment processors, hardware manufacturers, gaming hardware distributors, and end consumers across North, South, West, and East India.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, regulatory filings, government databases, and industry publications. Key sources included the Telecom Regulatory Authority of India, Ministry of Information and Broadcasting AVGC Task Force reports, National Payments Corporation of India data, and leading gaming analytics platforms covering India's mobile, PC, and esports segments.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating smartphone penetration rates, per-capita digital entertainment spending indices, gamer population cohort data, and historical segment-level revenue evolution. A base-case CAGR of 14.59% reflects consensus analyst estimates validated against reported publisher and platform revenue trajectories.

India Gaming Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Device Types Covered | Consoles, Mobiles and Tablets, Computers |

| Platforms Covered | Online, Offline |

| Revenue Types Covered | In-Game Purchase, Game Purchase, Advertising |

| Types Covered | Adventure/Role Playing Games, Puzzles, Social Games, Strategy, Simulation, Others |

| Age Groups Covered | Adult, Children |

| Regions Covered | South India, North India, West & Central India, East India |

| Companies Covered | Nazara Technologies, KRAFTON, Inc., Sporta Technologies Private Limited, Sea Limited, nCore games, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Gaming Market Report

The India gaming market size was valued at USD 5.91 Billion in 2025. It is projected to reach USD 16.72 Billion by 2034, growing at a CAGR of 14.59% during the forecast period of 2026-2034.

The India gaming market is expected to grow at a CAGR of 14.59% during the forecast period from 2026 to 2034, supported by smartphone penetration, 5G infrastructure expansion, esports growth, and government investment in the AVGC sector.

North India leads the market with a 32.0% revenue share in 2025, driven by high population density in the Delhi-NCR metropolitan corridor, well-developed digital infrastructure, and a thriving esports event ecosystem attracting consumer participation and brand sponsorship investment.

Mobiles and tablets dominate the device-type segment with a 51.46% share in 2025, driven by India's mobile-first digital ecosystem, widespread availability of affordable smartphones, and extensive 4G/5G network coverage enabling seamless gaming experiences across diverse demographic and income segments.

Offline gaming leads the platform segment at 53.65% in 2025, preferred by consumers seeking uninterrupted gameplay without internet dependency, particularly in tier-two and tier-three cities where network reliability remains inconsistent.

Key drivers include rapid smartphone penetration, ultra-affordable mobile data plans, a young digitally native population, formal esports recognition as an official sport, UPI-enabled frictionless in-game monetization, 5G infrastructure expansion, and government investment through the AVGC sector initiative.

Key players in the India gaming market include Nazara Technologies, KRAFTON, Inc., Sporta Technologies Private Limited, Sea Limited, and nCore Games.

Key challenges include rural connectivity gaps constraining online gaming adoption, state-level regulatory divergence on skill-based game classification, monetization sensitivity in price-conscious markets, gaming addiction concerns prompting content regulation discussions, and talent scarcity for specialized game development roles.

Significant opportunities exist in cloud gaming edge infrastructure, vernacular mobile game publishing, esports media rights and broadcast monetization, AI-powered game personalization, and indigenous IP development. The AVGC sector government initiative and the growing tier-two/three city user base represent additional high-potential investment themes through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)