India Furniture Market Size, Share, Trends and Forecast by Material, Distribution Channel, End Use, and Region, 2026-2034

India Furniture Market Size, Share, Trends & Forecast (2026-2034)

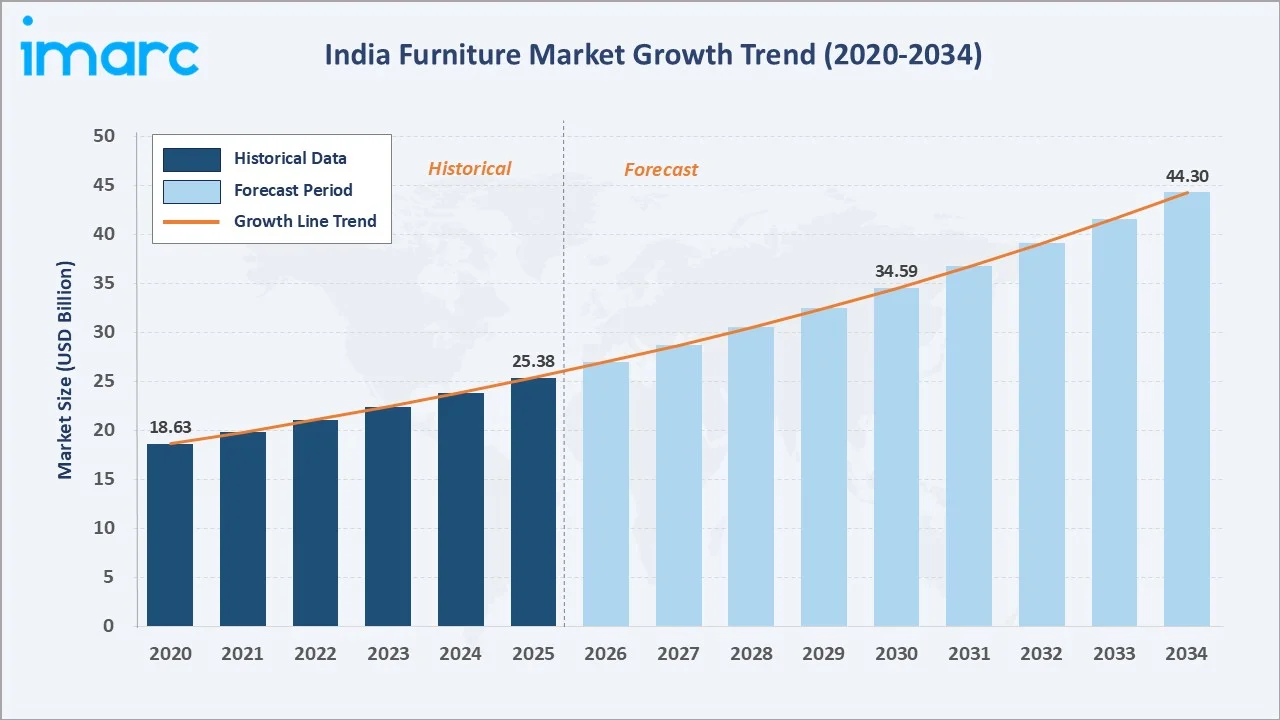

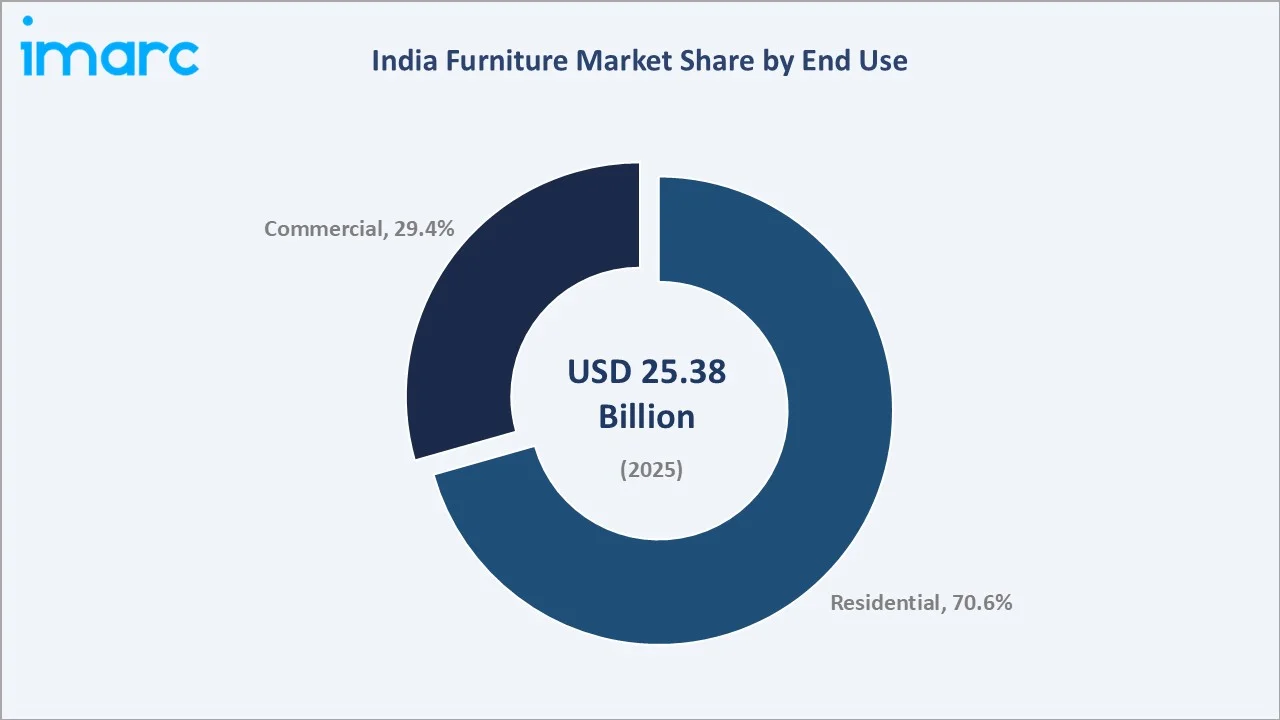

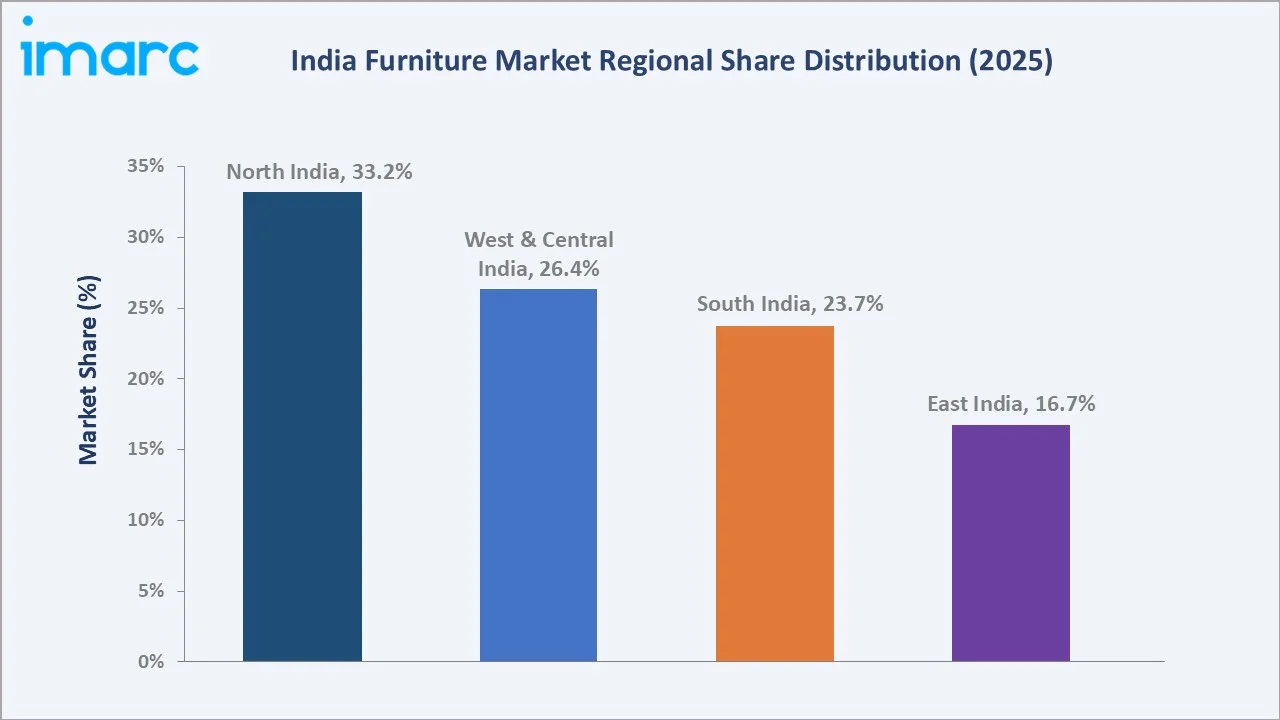

The India furniture market size was valued at USD 25.38 Billion in 2025 and is projected to reach USD 44.30 Billion by 2034, at a CAGR of 6.38% during 2026-2034. Rapid urbanization, a booming real estate sector, and rising disposable incomes are the primary growth catalysts. Wood furniture dominates with a 59.8% material share in 2025, while Residential end use accounts for 70.6% of total revenue. North India leads regional demand with a 33.2% share, driven by Delhi-NCR's real estate expansion and strong commercial infrastructure growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 25.38 Billion |

|

Forecast Market Size (2034) |

USD 44.30 Billion |

|

CAGR (2026-2034) |

6.38% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (33.2% share, 2025) |

|

Fastest Growing Region |

West & Central India |

|

Leading Material Segment |

Wood (59.8%, 2025) |

|

Leading End Use Segment |

Residential (70.6%, 2025) |

The chart below tracks India's furniture market growth from 2020–2034, illustrating post-pandemic demand recovery in the historical period and sustained CAGR-driven expansion across the forecast horizon

To get more information on this market, Request Sample

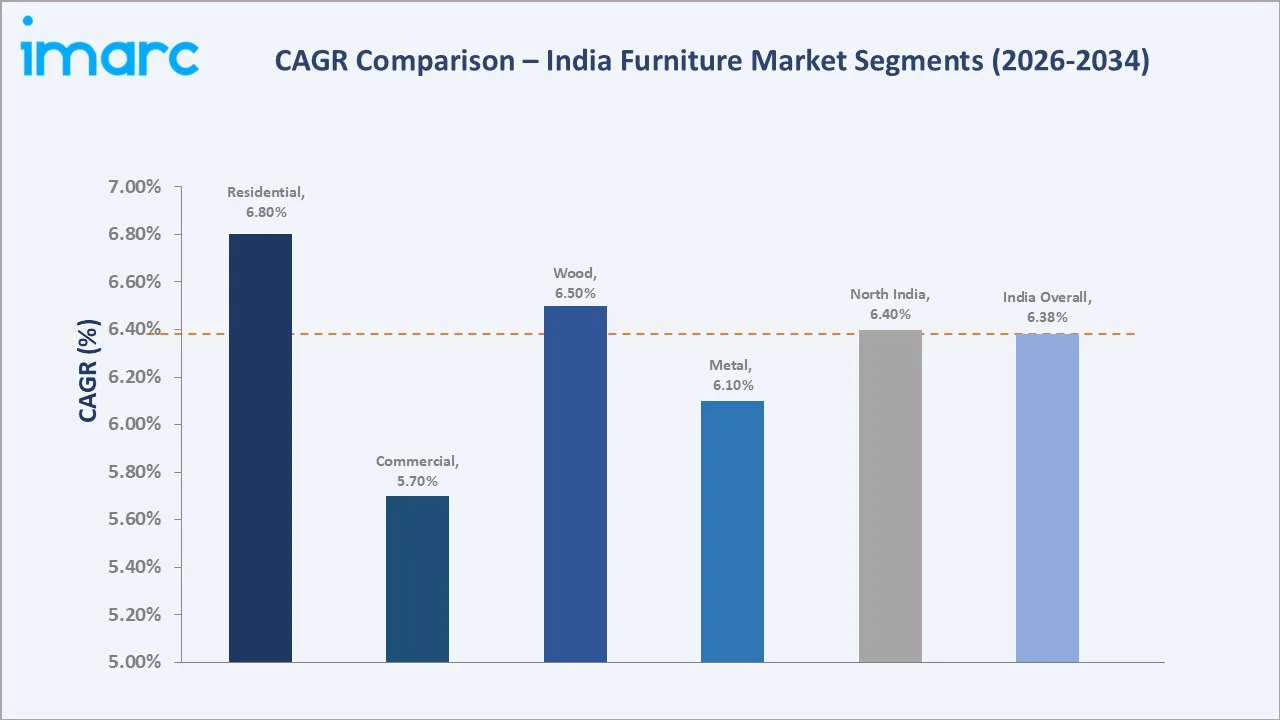

CAGR analysis across key segments reveals wood and metal as the fastest-growing product categories, with the Residential segment sustaining the highest application-level growth through 2034

Executive Summary

India’s furniture market is transforming due to real estate growth, rising digital retail adoption, and shifting consumer lifestyles. Valued at USD 25.38 Billion in 2025, it is projected to reach USD 44.30 Billion by 2034 at a CAGR of 6.38%. Expanding urban housing, supported by initiatives like the Pradhan Mantri Awas Yojana (PMAY), is driving steady demand across residential and commercial segments.

Wood furniture dominates with a 59.8% share in 2025, driven by demand for natural aesthetics, durability, and premium engineered wood. Metal and plastic segments hold 18.4% and 11.3%, gaining traction in commercial and institutional use. D2C e-commerce players like Wakefit and Pepperfry are reshaping distribution, while established regional players such as Godrej & Boyce and IKEA India are expanding omnichannel presence.

North India leads with a 33.2% share in 2025, driven by strong residential and corporate activity in Delhi NCR. South India and West & Central India hold 23.7% and 26.4%, supported by demand from Bengaluru’s IT sector and Mumbai’s premium housing market. Smart furniture, modular kitchens, and sustainable materials are key growth opportunities through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Material Segment |

Wood – 59.8% share (2025) |

|

Largest End Use Segment |

Residential – 70.6% share (2025) |

|

Second Material Segment |

Metal – 18.4% share (2025) |

|

Leading Region |

North India – 33.2% revenue share (2025) |

|

Second Region |

West & Central India – 26.4% revenue share (2025) |

|

Top Companies |

Godrej Enterprises, Inter IKEA Systems B.V., Nilkamal Furniture, Wakefit Innovations Limited, Durian Industries Ltd. |

|

Market Opportunity |

Smart & modular furniture demand rising across urban Tier-1 and Tier-2 cities |

Key Analytical Observations Supporting The Above Data:

- Wood's 59.8% dominance in 2025 reflects deep consumer preference for solid and engineered wood products, reinforced by the premiumization trend in urban housing and the growing interior design consultancy market.

- Residential furniture accounts for 70.6% in 2025, supported by India’s housing boom, with PMAY’s 11.2 million home target sustaining long-term demand.

- Metal furniture's 18.4% share serves primarily the B2B segment – corporate offices, hospitals, educational institutions, and government procurement – making it relatively insulated from consumer sentiment cycles.

- North India's 33.2% regional dominance is supported by Delhi-NCR's status as India's largest real estate market; residential project launches in Gurugram, Noida, and Faridabad drive continued demand for home furnishings.

- E-commerce channels are growing faster than offline retail, with platforms like Wakefit, Pepperfry, Urban Ladder, and Amazon India capturing a rising share of furniture sales by 2025.

- Godrej Interio, IKEA India, and Nilkamal are the three largest branded furniture players, highlighting the growing influence of the organized sector.

India Furniture Market Overview

The India furniture market covers the design, manufacturing, distribution, and retail of furniture across residential, commercial, hospitality, healthcare, and institutional segments, involving suppliers, component makers, OEMs, retailers, e-commerce platforms, and interior design services.

India is an emerging global furniture exporter, ranking around 16th worldwide and supplying to key markets such as the USA, UK, and GCC countries. Domestic demand is driven by rapid urbanization, evolving lifestyles, nuclear family growth, and increased home improvement and work-from-home spending. Government initiatives like Make in India and export promotion schemes are supporting manufacturing growth and sector formalization.

Market Dynamics

To evaluate market opportunities, Request Sample

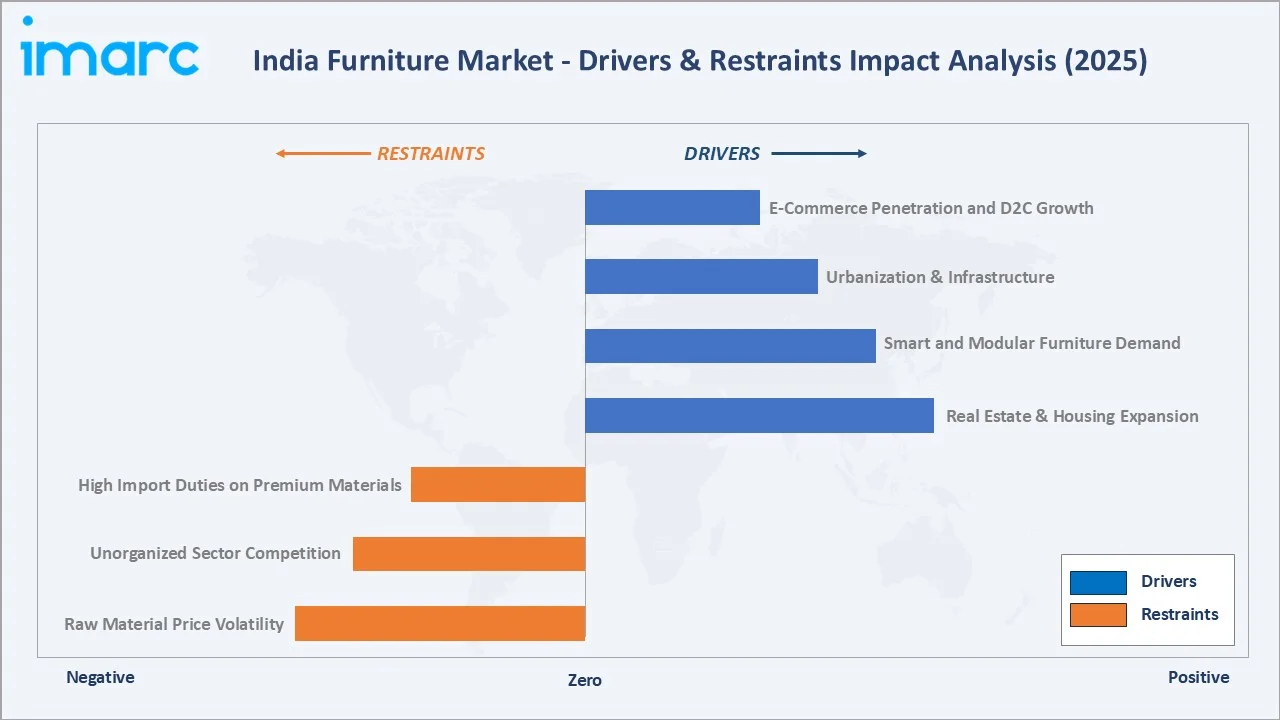

Market Drivers

- Real Estate and Housing Sector Expansion: India’s housing sector remains the primary demand driver, with strong residential activity across major cities, as 4,12,520 units were launched across the top seven cities in 2024, supporting steady furniture demand from rising homeownership.

- Rising Disposable Incomes and Middle-Class Consumption: India’s per capita income has steadily increased in recent years, boosting spending on home improvement and premium furniture among urban and semi-urban consumers.

- Urbanization and Commercial Infrastructure: Expanding urbanization and growth in office and commercial spaces across cities like Bengaluru, Hyderabad, Mumbai, and Delhi NCR are driving demand for office and institutional furniture, with India’s real estate industry projected to reach US$ 5.8 trillion by 2047.

- E-Commerce Penetration and D2C Growth: Online furniture retail is expanding rapidly, supported by platforms like Wakefit, Urban Ladder, Pepperfry, and Amazon India, improving accessibility and accelerating organized market growth.

Market Restraints

- Raw Material Price Volatility: Prices of key inputs like timber, steel, and polymers have shown significant volatility in recent years, with import dependence and supply disruptions (especially from Southeast Asia) increasing cost pressures for manufacturers.

- Competition from the Unorganized Sector: A large share of India’s furniture market remains unorganized, dominated by local carpenters and small workshops that compete aggressively on price, limiting organized sector penetration.

- High Import Duties on Premium Materials: India imposes relatively high import duties on furniture and components, increasing costs for premium materials and limiting access to global designs for domestic manufacturers.

Market Opportunities

- Smart and Modular Furniture Demand: Rising space constraints in urban homes are driving demand for modular, multifunctional, and smart furniture, supported by evolving urban lifestyles and compact housing trends.

- Tier-2 and Tier-3 City Expansion: Low penetration of organized furniture retail in Tier-2 and Tier-3 cities presents a significant growth opportunity, with increasing income levels and e-commerce access expanding the addressable market.

- Export Growth to GCC and Global Markets: India’s furniture exports have shown steady growth in recent years, with key markets including the USA, UK, and GCC countries driving international demand.

Market Challenges

- Skilled Artisan and Labour Shortages: India's furniture manufacturing sector faces shortages of trained woodworkers, upholstery specialists, and CAD-based design operators, limiting production quality consistency.

- Last-Mile Logistics Complexity: Bulky furniture products lead to high delivery and installation costs, especially in Tier-2 and Tier-3 cities, affecting margins for organized and e-commerce players.

- Counterfeit Products and Quality Perception Gaps: Widespread availability of substandard imports and domestic copies undermine consumer confidence and brand equity, creating pricing pressure on legitimate organized-sector manufacturers.

Emerging Market Trends

1. Smart and Multifunctional Furniture Adoption

Shrinking urban apartment sizes – the average Mumbai flat fell to 645 sq. ft. in 2024 – are accelerating demand for convertible beds, fold-out tables, wall-mounted shelving, and modular storage systems. Smart furniture integrating USB charging ports and embedded sensor systems is emerging as a premium differentiation strategy.

2. Sustainable and Eco-Certified Material Sourcing

Environmental awareness is driving demand for sustainable materials such as certified wood, bamboo, and recycled inputs. IKEA India’s commitment to 100% renewable and recycled materials by 2030 is shaping consumer expectations and influencing industry practices.

3. D2C E-Commerce and Online Customization

India’s D2C furniture segment is growing at a strong double-digit pace, driven by digital adoption. Brands like Wakefit and Urban Ladder are leveraging 3D visualization, AR-based previews, and customization tools to improve online conversion and customer experience.

4. Premiumization in Urban Markets

India’s luxury furniture segment is growing faster than the overall market, driven by rising HNIs, premium residential developments, and demand from boutique hotels and hospitality projects.

5. Corporate Office Re-Design and Hybrid Workplace Transformation

India’s shift to hybrid work is driving office refurbishment, with companies replacing fixed desks with collaborative layouts, boosting demand for commercial furniture across major cities like Bengaluru, Hyderabad, Mumbai, and Delhi NCR.

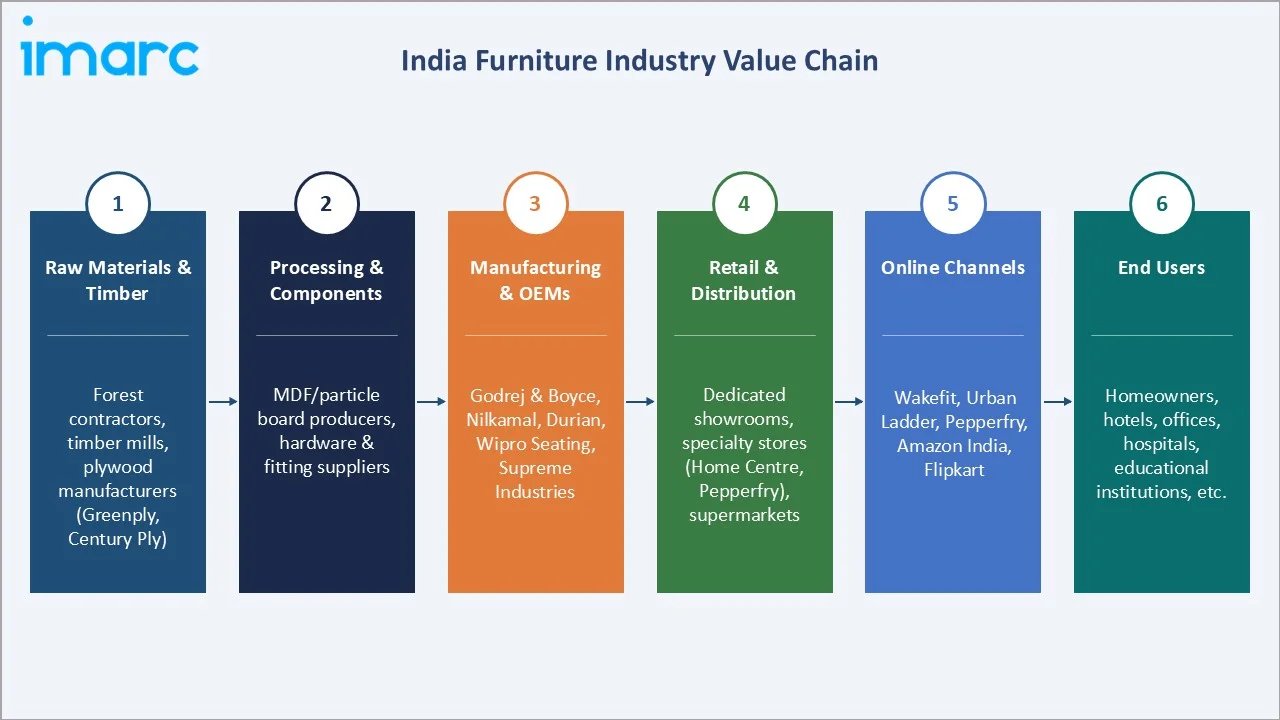

Industry Value Chain Analysis

The India furniture value chain spans six interconnected stages, from raw material procurement to end-consumer delivery, each driven by distinct competitive dynamics and margin structures.

|

Stage |

Key Players / Examples |

|

Raw Materials & Timber |

Forest contractors, timber mills, plywood manufacturers |

|

Processing & Components |

MDF/particle board producers, hardware & fitting suppliers |

|

Manufacturing & OEMs |

Godrej & Boyce, Nilkamal, Durian, Wipro Seating Solutions, Supreme Industries |

|

Retail & Distribution |

Dedicated showrooms, specialty stores (Home Centre, Pepperfry), supermarkets |

|

Online Channels |

Wakefit, Urban Ladder, Pepperfry, Amazon India, Flipkart |

|

End Users |

Homeowners, hotels, offices, hospitals, educational institutions |

Organized players like Godrej Interio and Nilkamal lead the value chain through integrated operations, while e-commerce platforms are disrupting traditional distribution with direct-to-consumer delivery.

Technology Landscape in the Furniture Industry

Digital Manufacturing and CAD/CAM Automation

Technologies like CNC machines, laser cutting, and CAD/CAM are improving production precision and reducing material wastage, while leading manufacturers are investing in automation to enhance efficiency and ensure consistent quality in high-volume production.

Augmented Reality (AR) and 3D Room Visualization

AR-enabled room planning tools offered by IKEA India, Wakefit, and Pepperfry allow customers to visualize furniture in their homes, enhancing engagement and improving online conversion rates.

Engineered Wood and Material Innovation

Medium-density fibreboard (MDF), high-density fibreboard (HDF), and particle board are displacing solid timber in mid-price segments, offering dimensional stability and lower cost. Nano-coating technologies for scratch and moisture resistance are extending product lifespans and supporting premiumization.

E-Commerce Platform Integration and Supply Chain Digitalization

Real-time inventory systems, AI-driven demand forecasting, and supplier integration are helping organized furniture brands improve delivery speed and supply chain efficiency, enhancing customer satisfaction and reducing return rates.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material |

Wood |

59.8% |

2025 |

|

Distribution Channel |

Speciality Stores |

46.5% |

2025 |

|

End Use |

Residential |

70.6% |

2025 |

|

Region |

North India |

33.2% |

2025 |

By End Use

To access detailed market analysis, Request Sample

Residential furniture dominates the India furniture market with a 70.6% share in 2025, driven by sustained housing construction and government initiatives like Pradhan Mantri Awas Yojana, supporting strong demand for home furniture across key categories.

Commercial furniture accounts for 29.4% of the market in 2025, driven by office fit-outs, hospitality, healthcare, and institutional demand. Expanding commercial real estate and corporate activity across India continue to support steady growth in this segment.

By Material

Wood furniture commands a 59.8% share in 2025, underpinned by strong consumer preference for natural aesthetics, structural durability, and aspirational value. Engineered wood products including MDF, plywood, and particle board variants are gaining share within the wood category due to lower costs, design versatility, and reduced reliance on scarce natural timber.

Metal furniture holds an 18.4% share in 2025, mainly serving B2B applications such as office, healthcare, and institutional use. Plastic furniture accounts for 11.3%, driven by low-cost and outdoor segments, while glass furniture at 6.7% caters to premium residential and retail needs. The Others category, at 3.8%, includes rattan, cane, bamboo, and composite materials.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

33.2% |

Real estate boom in Delhi-NCR, Haryana, Punjab; rising middle-class home ownership; strong commercial furniture demand |

|

West & Central India |

26.4% |

Mumbai's premium residential market; Pune & Ahmedabad corporate demand; Maharashtra's hospitality sector growth |

|

South India |

23.7% |

Bengaluru tech sector corporate offices; Chennai export-oriented manufacturing; Kerala's tourism & hospitality furniture demand |

|

East India |

16.7% |

Kolkata's growing urban housing market; Odisha & Jharkhand infrastructure investment; rising disposable incomes in Tier-2 cities |

North India commands a 33.2% revenue share in 2025, driven by its position as a leading real estate hub. The housing market in Delhi NCR saw strong momentum, with 23,265 units launched in H1 2024, while expanding corporate office space in Gurugram and Noida continues to support demand for residential and institutional furniture.

West & Central India accounts for 26.4%, driven by residential and commercial demand in Mumbai, Pune, and Ahmedabad. South India, at 23.7%, benefits from strong demand led by Bengaluru’s technology sector, while East India at 16.7% is an emerging market supported by urban growth in Kolkata and infrastructure development in Odisha.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Godrej Enterprises |

Godrej Interio |

Leader |

Operating as Godrej & Boyce Mfg. Co. Ltd. in India. Widest product range, pan-India distribution, strong corporate & institutional base |

|

Inter IKEA Systems B.V. |

IKEA |

Leader |

Functional as IKEA India Private Limited (Ingka Group). Flat-pack innovation, global design appeal, omnichannel retail, value-for-money positioning |

|

Nilkamal Furniture |

Nilkamal / @home |

Leader |

Plastic furniture dominance, nationwide retail network, growing lifestyle segment |

|

Wakefit Innovations Limited |

Wakefit |

Leader |

D2C digital-first model, sleep & home solutions, strong brand loyalty among millennials |

|

Durian Industries Ltd. |

Durian |

Challenger |

Premium wood & upholstered furniture, strong West India presence, luxury segment focus |

The India furniture market is characterized by a dual structure: a growing organized sector led by Godrej, IKEA India, Nilkamal, and Wakefit; and a large unorganized segment comprising local carpenters and regional manufacturers. Organized brands collectively account for an estimated 15–20% of total market value in 2025. The entry of Cello World and Supreme Industries into the branded furniture space signals accelerating formalization in the mass-market plastic and institutional furniture segments.

Key Company Profiles

Godrej Enterprises

Godrej Enterprises, operating as Godrej & Boyce Mfg. Co. Ltd. in India, the furniture division of Godrej & Boyce, is a leading organized furniture brand in India, offering comprehensive home and institutional solutions through an extensive omnichannel network, strong manufacturing base, and design-led portfolio across residential, commercial, and healthcare segments.

- Product & Service Portfolio: Living room furniture, bedroom sets, office desks and chairs, storage solutions, hospital furniture, laboratory furniture, modular kitchens, and customized institutional furniture.

- Recent Developments: In September 2025, Godrej Interio has announced a ₹300 crore investment to accelerate its expansion strategy, focusing on retail growth, digital capabilities, and product innovation, with a target of achieving ₹10,000 crore in revenue by FY2029. The company also unveiled a refreshed brand identity and plans to expand its retail footprint to around 1,500 outlets nationwide, with a strong emphasis on Tier-II and Tier-III cities to drive future growth.

- Strategic Focus: Godrej Interio focuses on scaling omnichannel retail, expanding in Tier-II/III markets, strengthening B2B institutional business, and driving growth through design innovation, sustainability, and digital customer experience.

Inter IKEA Systems B.V.

Inter IKEA Systems B.V. (IKEA India Private Limited), the Indian arm of Ingka Group, operates large-format and city stores alongside a growing omnichannel platform, offering affordable Scandinavian-designed furniture and home solutions, supported by significant long-term investments, local sourcing initiatives, and rapid retail expansion across major Indian cities.

- Product & Service Portfolio: IKEA India provides ready-to-assemble furniture across home and office segments, modular kitchens, décor and furnishings, storage solutions, and digital-enabled services including planning, delivery, installation, and omnichannel retail experiences.

- Recent Developments: In January 2026, IKEA announced plans to more than double its investment in India to approximately $2.2 Billion over the next five years, aimed at accelerating store expansion, strengthening digital capabilities, and increasing local sourcing. In March 2026, company reaffirmed its aggressive expansion roadmap, with plans to open around 25 new stores across formats over the next 4–5 years, reinforcing its omnichannel strategy and deeper penetration into key urban and emerging markets.

- Strategic Focus: IKEA India focuses on aggressive omnichannel expansion, small-format store penetration, affordability through local sourcing, and long-term market growth driven by digital integration and large-scale investment commitments.

Nilkamal Furniture

Nilkamal Furniture is a leading Indian furniture manufacturer specializing in moulded plastic and lifestyle furniture, supported by a wide distribution network, strong manufacturing capabilities, and a growing retail presence through its @home brand targeting mass and mid-premium segments.

- Product & Service Portfolio: Nilkamal offers moulded plastic furniture, mattresses, modular and institutional furniture, storage and material handling solutions, and lifestyle furniture through @home, along with retail, e-commerce, and B2B supply services.

- Recent Developments: In November 2025, Nilkamal Furniture reported strong Q2 FY26 performance, with revenue rising 18% year-on-year to around ₹948–968 crore and profit increasing to ₹33 crore, driven by robust B2B demand and a ~23% surge in e-commerce sales; the company also expanded its retail footprint to approximately 96 stores, strengthening its @home and omnichannel growth strategy.

- Strategic Focus: Nilkamal focuses on expanding its lifestyle furniture segment through @home, strengthening omnichannel retail, and leveraging its leadership in plastic furniture to drive growth across mass and mid-premium segments.

Market Concentration Analysis

The India furniture market is highly fragmented, with the top 5 organized players – Godrej, IKEA, Nilkamal, Wakefit, and Durian Industries Limited – collectively accounting for an estimated 10–14% of total market revenue in 2025. The market continues to be dominated by the unorganized segment, which contributes approximately 80–85% of total production volume, comprising tens of thousands of small-scale manufacturing units, along with a vast base of local carpenters, workshops, and fabricators across the country

Market fragmentation is highest in the mass-market wood and custom carpenter segment, where regional preferences and price sensitivity limit the scale of organized brands. In contrast, the commercial and institutional segment is relatively more consolidated, with organized manufacturers accounting for a higher share of procurement due to their ability to meet quality standards, offer warranties, and ensure regulatory compliance.

Consolidation in India’s furniture market is accelerating, driven by increasing PE/VC investments in D2C brands, expansion of IKEA India, and organized retailers’ growing presence in Tier-2 cities. As a result, the organized segment’s share is expected to increase steadily over the next decade as formal retail penetration deepens.

Investment & Growth Opportunities

Fastest-Growing Segments

Smart, modular, and space-saving furniture is among the fastest-growing categories in India, driven by urbanization, smaller homes, and rising demand from millennials and nuclear families. Premium residential furniture is expanding faster than the overall market due to increasing disposable income and lifestyle upgrades.

The commercial furniture segment especially office, hospitality, and healthcare continues to grow steadily, supported by expansion in Grade-A office spaces, a strong hotel development pipeline, and increased public healthcare investments.

Emerging Market Expansion

Tier-2 and Tier-3 cities are key growth frontiers, driven by rising urbanization, improving infrastructure, and increasing consumer spending. Organized furniture retail penetration remains significantly lower than in Tier-1 cities, indicating strong headroom for expansion.

Venture & Strategic Investment Trends

India’s D2C furniture market has attracted notable venture capital and private equity investments in recent years, with leading players securing funding to expand omnichannel presence. Investments in technologies such as AR-based visualization, AI-led demand planning, and supply chain optimization are increasing. Additionally, export-oriented furniture manufacturing is gaining traction under government initiatives like Make in India, creating long-term investment opportunities.

Future Market Outlook (2026-2034)

India’s furniture market is projected to grow from USD 25.38 Billion in 2025 to USD 44.30 Billion by 2034, at a CAGR of 6.38%, creating over USD 18.9 Billion in incremental value. Growth is supported by real estate expansion, urbanization, and increasing organized retail penetration, with premium and smart furniture segments outpacing the overall market.

Three transformational forces will reshape India’s furniture market through 2034. First, the maturity of e-commerce and AR-enabled shopping will extend organized retail to Tier-3 consumers, significantly expanding the addressable market. Second, sustainable and certified sourcing will become a standard requirement rather than a differentiator. Third, modular and smart furniture innovation will redefine the residential segment, with multifunctional, space-efficient designs capturing a larger share of new household spending.

By 2034, India is expected to emerge as a leading furniture market in Asia, driven by a growing middle class, expanding urban infrastructure, and a strengthening domestic manufacturing base that is increasingly competitive with global imports.

Research Methodology

Primary Research

Primary research was conducted in 2024–2025 through structured interviews and surveys with India furniture market stakeholders including retail chain procurement managers, furniture brand marketing directors, interior design consultants, e-commerce platform operations teams, and real estate developer fit-out coordinators. Consumer surveys covering 500+ households across 8 cities captured purchase behaviour, channel preference, and product category priorities.

Secondary Research

Secondary sources include Ministry of Commerce furniture export data, Registrar of Companies financial filings for listed furniture manufacturers, NSSO housing surveys, Knight Frank and JLL commercial real estate reports, Retailers Association of India trade data, National Action Plan for furniture implementation reports, Bureau of Indian Standards quality norms, and sector-specific analyst publications.

Forecasting Models

Market size estimates and growth projections are derived using a combination of bottom-up and top-down approaches. The base-case CAGR of 6.38% is supported by India’s steady economic growth, expanding housing demand, and the increasing role of e-commerce in furniture sales.

India Furniture Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Materials Covered | Metal, Wood, Plastic, Glass, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online Stores, Others |

| End Uses Covered | Residential, Commercial |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Godrej Enterprises, Inter IKEA Systems B.V., Nilkamal Furniture, Wakefit Innovations Limited, Durian Industries Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Furniture Market Report

The India furniture market was valued at USD 25.38 Billion in 2025, driven by urbanization, real estate growth, rising incomes, and expanding commercial infrastructure.

The market is projected to reach USD 44.30 Billion by 2034, growing at a CAGR of 6.38% during 2026-2034, driven by e-commerce, smart furniture, and housing sector expansion.

Wood leads with a 59.8% share in 2025, owing to consumer preference for natural aesthetics, durability, and the premium positioning of solid wood and engineered wood products.

Residential furniture dominates with a 70.6% share in 2025, supported by rapid housing construction, home renovation trends, and rising urban middle-class spending.

North India leads with a 33.2% share in 2025, driven by Delhi-NCR's real estate expansion, strong retail penetration, and high commercial furniture demand from corporate parks.

Key drivers include real estate sector expansion, rising disposable incomes, urbanization, growing e-commerce penetration, and increasing interior design awareness among homeowners.

West & Central India is among the fastest-growing regions, fuelled by Mumbai's luxury housing projects, Pune's IT corridor expansion, and Ahmedabad's commercial real estate surge.

Leading companies include Godrej Enterprises, Inter IKEA Systems B.V., Nilkamal Furniture, Wakefit Innovations Limited, and Durian Industries Ltd., among others.

Metal furniture accounts for 18.4% of the India furniture market in 2025, primarily used in commercial and institutional settings due to its durability and lower maintenance requirements.

E-commerce platforms such as Wakefit, Pepperfry, and Urban Ladder are disrupting traditional channels, enabling price comparison, home delivery, and D2C brand growth across Tier-2 cities.

Rising homeownership rates, PMAY housing schemes, growing nuclear family trends, and urban migration are collectively driving residential furniture demand across India.

The India furniture market was valued at USD 18.63 Billion in 2020, growing at ~6.4% CAGR from 2020 to 2025 to reach USD 25.38 Billion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)