In-Game Advertising Market Size, Share, Trends and Forecast by Type, Device Type, and Region, 2026-2034

In-Game Advertising Market Size, Share, Trends & Forecast (2026-2034)

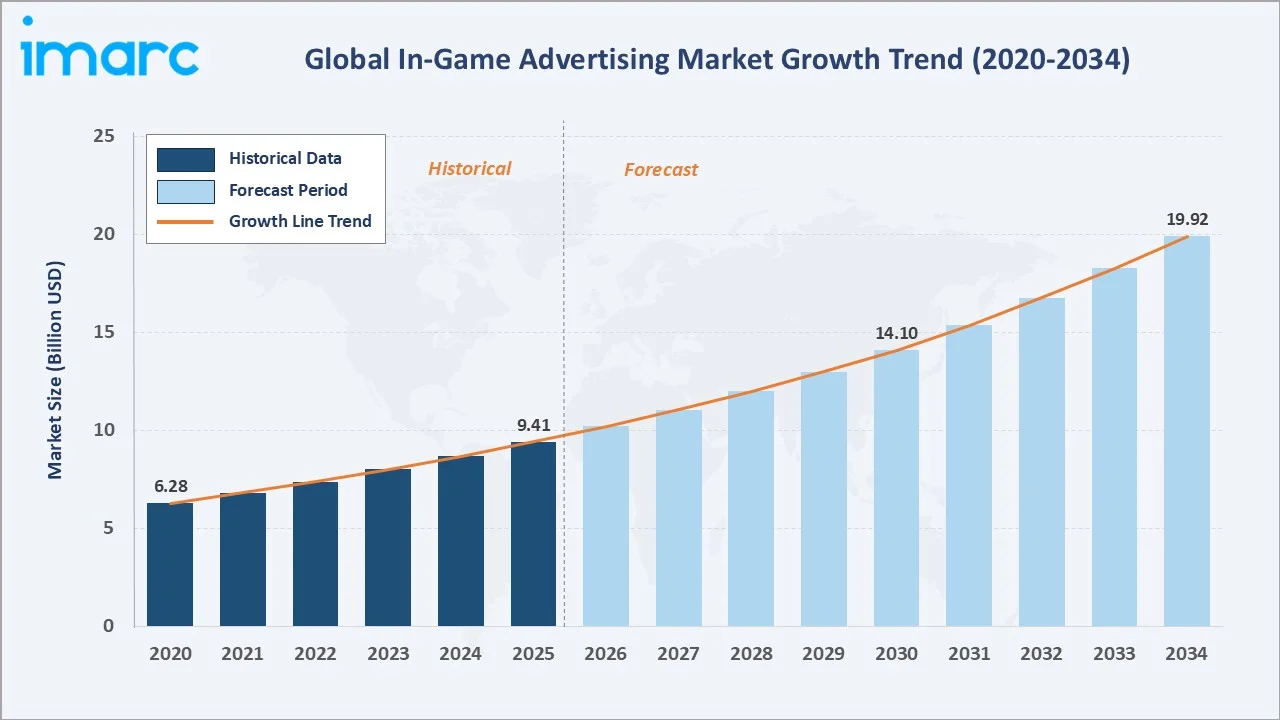

The in-game advertising market was valued at USD 9.41 Billion in 2025 and is projected to reach USD 19.92 Billion by 2034, exhibiting a CAGR of 8.43% during 2026-2034. Rising mobile gaming penetration, the expansion of programmatic ad delivery, brand demand for Gen Z and Gen Alpha audiences, and growing esports viewership are the primary drivers shaping the market. Esports popularity among younger audiences is increasing, with interest among individuals aged 18–29 rising from 27% in Q1 2021 to 31% in Q2 2024.

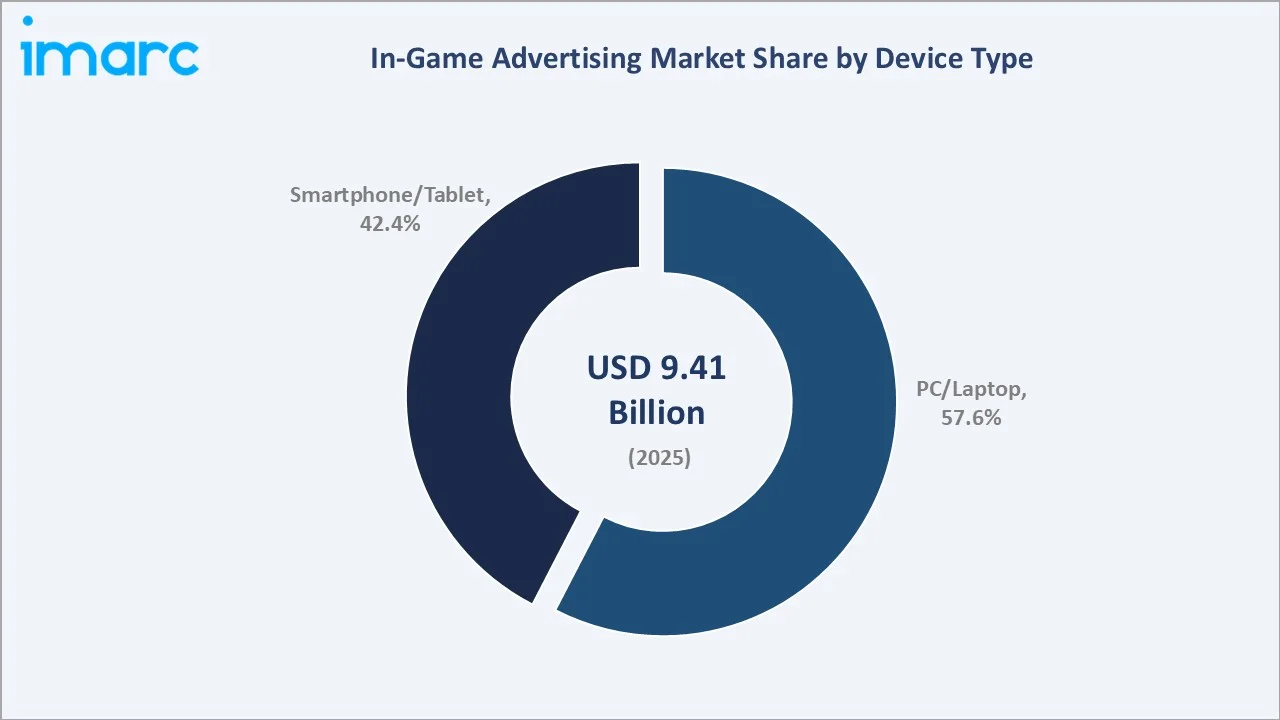

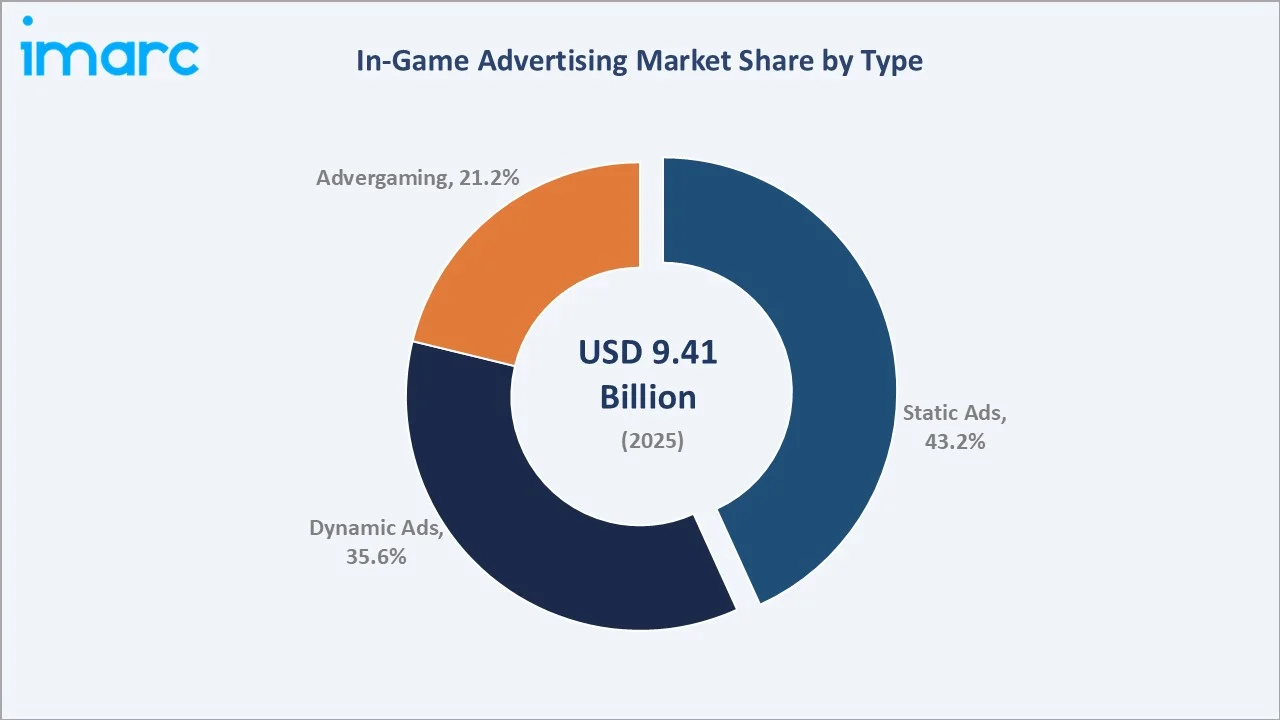

PC/laptop leads the device type segment at 57.6%, static ads dominate the type segment at 43.2%, and North America commands 36.8% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.41 Billion |

|

Forecast Market Size (2034) |

USD 19.92 Billion |

|

CAGR (2026-2034) |

8.43% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.8%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (28.4%, 2025) |

|

Leading Device Type |

PC/Laptop (57.6%, 2025) |

|

Leading Type |

Static Ads (43.2%, 2025) |

The in-game advertising market expanded from USD 6.28 Billion in 2020 to USD 9.41 Billion in 2025, supported by mobile gaming proliferation, programmatic ad-tech maturity, and intrinsic ad placements that respect player immersion. Anchored at USD 14.10 Billion in 2030, the forecast to USD 19.92 Billion by 2034 reflects continued migration of brand budgets toward gaming-native inventory and audiences.

To get more information on this market, Request Sample

CAGR trajectories across device type, type, and regional sub-segments show smartphone/tablet, dynamic ads, and Asia-Pacific expanding faster than the overall 8.43% market CAGR, driven by mobile gaming penetration, programmatic ad delivery economics, and emerging-market gaming uptake.

Executive Summary

The in-game advertising market is on a strong growth path from USD 6.28 Billion in 2020 to a projected USD 19.92 Billion by 2034. Advertising inside video games has matured from simple banner placements into intrinsic, programmatically delivered creatives that integrate naturally into game environments. Falling barriers to ad-tech adoption, brand budgets shifting toward gaming audiences, and rapid mobile gaming penetration are sustaining momentum across the industry.

PC/laptop dominates the device type segment at 57.6% in 2025, supported by deep engagement times and access to immersive, high-performance gaming environments that enable richer ad formats and brand integrations. Static ads lead the type segment at 43.2%, fueled by easy implementation and minimal disruption to gameplay. North America commands 36.8% regional share, led by mature ad ecosystems in the United States and Canada. The Entertainment Software Association (ESA) reported that in 2025, more than 205 Million Americans regularly played video games, giving brand advertisers in the United States access to one of the world's largest single-country gaming audiences.

Key Market Insights

|

Insight |

Data |

|

Leading Device Type |

PC/Laptop - 57.6% share (2025) |

|

Second Device Type |

Smartphone/Tablet - 42.4% share (2025) |

|

Leading Type |

Static Ads - 43.2% share (2025) |

|

Fastest Growing Type |

Dynamic Ads - 35.6% share (2025) |

|

Leading Region |

North America - 36.8% share (2025) |

|

Fastest Growing Region |

Asia-Pacific - 28.4% share (2025) |

|

Top Companies |

Amazon.com, Inc., Unity Technologies, Microsoft, AppLovin Corp, and Roblox Corporation |

Key Analytical Observations Supporting the Above Data:

- PC/laptop dominance at 57.6% reflects deep engagement times in complex, high-immersion game genres and competitive titles, where sustained gameplay sessions support premium, high-impact in-game advertising placements. Valve disclosed at GDC 2026 that Steam reached an all-time concurrent user peak of 42,042,778 simultaneous players on January 11, 2026, underscoring the depth and stickiness of the PC gaming audience that brand advertisers are increasingly seeking to reach.

- Smartphone/tablet share at 42.4% is driven by the scale of free-to-play mobile gaming, programmatic mediation through ad networks, and rewarded video formats that offer in-game incentives in exchange for ad views.

- Static ads at 43.2% lead due to lower integration cost, predictable performance, and minimal disruption, making them the default choice for publishers seeking stable monetization without complex pipelines.

- Dynamic ads at 35.6% benefit from real-time creative refresh, contextual relevance, and programmatic buying compatibility, allowing brands to update messaging without patching the underlying game build.

- North America at 36.8% dominates owing to mature programmatic ecosystems, deep advertiser networks across the United States and Canada, and well-established relationships with major console and PC game publishers.

In-Game Advertising Market Overview

In-game advertising refers to the practice of integrating brand messaging into video games through static placements, dynamic banner inventory, branded mini-games, sponsored content, and rewarded video formats. These ads can appear on virtual billboards, in-game objects, splash screens, or as native experiences that blend with gameplay narratives across PC, mobile, and console environments.

The ecosystem connects game developers and publishers, ad-tech platforms, in-game ad networks, mediation layers, brand advertisers and agencies, measurement vendors, and end gamers across PC/laptop, smartphone/tablet, and console formats. Cloud gaming expansion and 5G rollout are widening the addressable inventory base.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Mobile Gaming and 5G Connectivity: Smartphone and tablet penetration combined with low-latency 5G networks is widening the audience for free-to-play games, which rely heavily on ad monetization through interstitials, rewarded video, and intrinsic placements.

- Brand Demand for Gen Z and Gen Alpha: Younger audiences spend significant entertainment time inside games, prompting consumer brands across food and beverage, fashion, automotive, and entertainment to shift media budgets toward gaming-native ad placements. Roblox Corporation alone reached more than 151 Million daily active users as of late 2025, providing advertisers a single platform with audience scale comparable to major social networks.

- Programmatic and Intrinsic Ad Tech Maturity: Advances in programmatic mediation, server-side decisioning, and intrinsic ad placement allow real-time creative delivery and contextual targeting without disrupting gameplay, expanding inventory liquidity for both publishers and advertisers.

- Esports and Live-Streaming Audience Growth: Tournament viewership, streaming integrations, and influencer-driven gaming content are creating premium adjacent inventory, including sponsorships, branded overlays, and rewarded video during match intermissions.

Market Restraints

- Privacy Regulations and Tracking Limits: Tightening data-protection regimes are acting as a key restraint, limiting cross-app behavioral targeting and forcing a shift toward contextual and consent-driven approaches, which can reduce targeting precision and campaign efficiency.

- Player Pushback and Brand Safety Concerns: Forced or intrusive ad placements have triggered backlash within gaming communities, raising reputational risk for publishers and advertisers and forcing a shift toward consent-based, value-exchange formats.

- Measurement and Standardization Gaps: In-game ad viewability, attention metrics, and attribution standards remain less mature than display or CTV, complicating buy-side budget allocation and slowing the adoption of premium console inventory.

Market Opportunities

- Cloud Gaming Ad Inventory: Cloud-streamed gaming services are creating new server-side ad insertion opportunities that mirror CTV economics while reaching cross-device audiences without download or hardware constraints.

- Emerging Markets and Affordable Smartphones: Asia-Pacific, Latin America, and the Middle East and Africa are expanding their mobile gaming bases as smartphone affordability improves and data plans bundle with ad-supported gaming, opening new monetization frontiers for brands seeking incremental reach.

Market Challenges

- Ad Fraud and Invalid Traffic: SDK spoofing, click injection, and fake install attribution remain ongoing challenges, requiring continuous investment in fraud-detection systems by mediation platforms and verification vendors.

- Inventory Quality Variation: Premium AAA console and PC inventory remains scarce relative to mobile and free-to-play, while quality, viewability, and brand-safe context vary widely across publishers, complicating large-scale media planning for global brand campaigns.

Emerging Market Trends

1. Programmatic Intrinsic Advertising

Intrinsic ads, which are non-disruptive placements integrated directly into 3D game environments, such as virtual billboards, banners, and stadium signage, are scaling through programmatic delivery. Server-side decisioning and standardized ad formats now enable real-time bidding for inventory that was previously sold as bespoke, hard-coded integrations, expanding access for both small and global advertisers.

2. Rise of AI-Driven Dynamic Ad Insertion

AI-powered creative optimization and contextual targeting are reshaping dynamic ad placements. Algorithms match brand messaging with player profiles, in-game context, and time-of-day signals to refresh creative without code changes, improving relevance and lifting completion rates across mobile, PC, and emerging cloud gaming environments.

3. Rewarded Video and Value-Exchange Formats

Rewarded video, where players opt in to view ads in exchange for in-game rewards, is becoming the dominant performance-friendly format on mobile and increasingly on web-game platforms. As of early 2026, Roblox Corporation reported that more than 1,000 brands had used its rewarded video format, achieving completion rates above 90% and viewability over 95%, illustrating the strength of consent-based advertising in gaming environments.

4. AR/VR and Immersive Brand Experiences

AR and VR environments are unlocking deeper brand storytelling formats, including 3D virtual storefronts, branded mini-games, and immersive sponsored events. Cross-platform releases are increasingly designed with built-in immersive ad slots that translate brand campaigns from flat creative into interactive experiences.

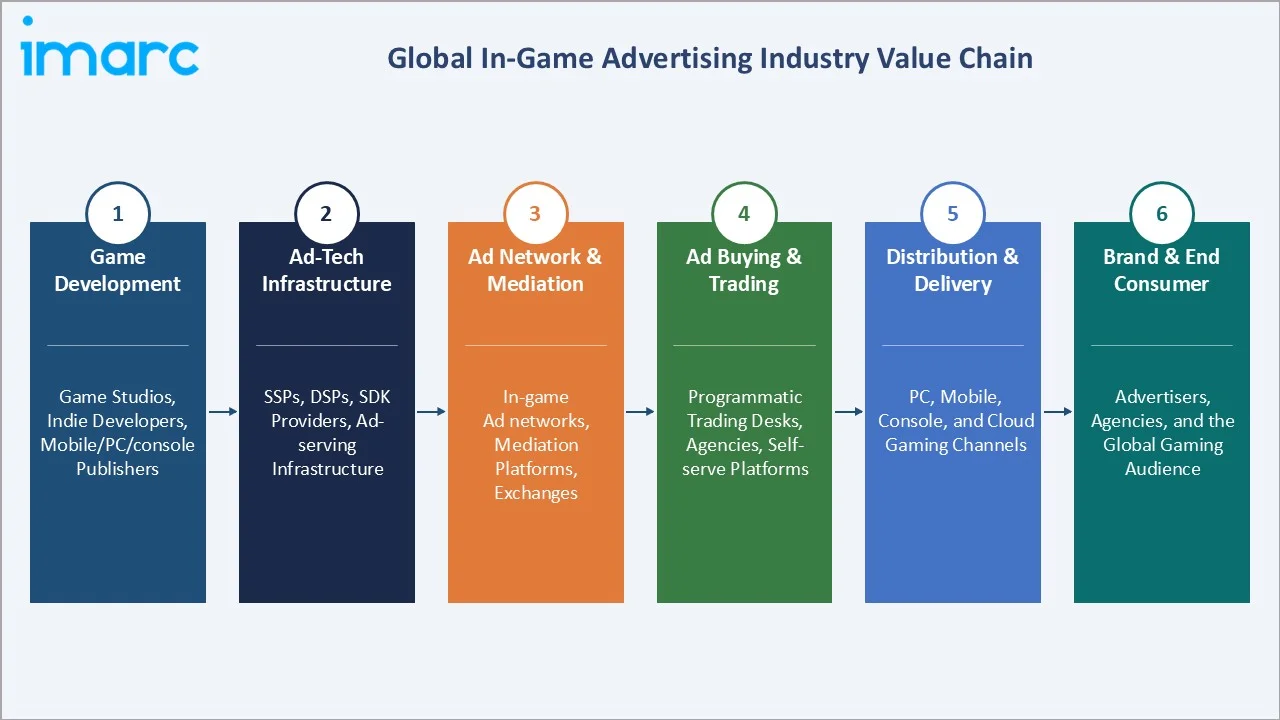

Industry Value Chain Analysis

The in-game advertising value chain spans six interconnected stages from game development to end-user delivery. Ad-tech infrastructure providers and ad network/mediation layers capture much of the technology value-add, while game publishers and gamers drive demand at both ends of the chain.

|

Stage |

Key Players / Examples |

|

Game Development |

Game studios, independent developers, and publishers building titles across mobile, PC, and console formats |

|

Ad-Tech Infrastructure |

Providers of supply-side platforms, demand-side platforms, software development kits, and ad-serving infrastructure |

|

Ad Network & Mediation |

In-game ad networks, mediation platforms, and exchanges aggregating publisher inventory and advertiser demand |

|

Ad Buying & Trading |

Programmatic trading desks, agency holding companies, and self-serve buying platforms |

|

Distribution & Delivery |

PC, mobile, console, and cloud gaming distribution channels enabling end-user playback of ads |

|

Brand & End Consumer |

Advertisers, agencies, and the global gaming audience consuming branded creative |

Vertically integrated platforms that combine engine-level ad insertion, mediation, and demand aggregation tend to capture the most value across the chain, supported by deeper data signals and direct publisher relationships.

Technology Landscape in the In-Game Advertising Industry

Programmatic Ad Delivery and Mediation

Real-time bidding, header bidding adapters, and unified auction frameworks are becoming standard for in-game ad placement, allowing publishers to access multiple demand sources simultaneously. Server-side mediation reduces latency and improves fill rates, especially in mobile gaming.

Intrinsic Ad Placement and Engine Integration

Modern game engines increasingly support native ad-placement modules that allow brands to render inside 3D environments without disrupting gameplay. Engine-level integration also enables dynamic creative swaps without requiring a game patch or update.

AI-Driven Targeting and Contextual Signals

Machine learning models analyze gameplay patterns, contextual cues, and aggregated player profiles to deliver more relevant creative. AI is also enabling automated brand-safety classification of in-game contexts and content.

Measurement, Verification, and Brand Safety

Third-party verification vendors are expanding viewability, attention, and brand-safety measurement frameworks specifically designed for 3D environments. Industry-standard measurement is gradually closing the gap with display and CTV ecosystems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Static Ads |

43.2% |

2025 |

| Device Type | PC/Laptop |

57.6% |

2025 |

|

Region |

North America |

36.8% |

2025 |

By Device Type

PC/laptop commands 57.6% share in 2025, supported by high-performance gaming environments and sustained player engagement that enable immersive ad formats, deeper brand integration, and more effective campaign delivery. Multi-platform publishers and ad-tech integrations further enable unified campaign execution across PC and other gaming environments with robust targeting and measurement capabilities.

To access detailed market analysis, Request Sample

Smartphone/tablet at 42.4% in 2025 captures most free-to-play and casual gaming inventory, where rewarded video, interstitial, and playable ad formats dominate the monetization model. Mobile expansion is accelerating in Asia-Pacific and Latin America as smartphone penetration deepens.

By Type

Static ads at 43.2% lead the type segment in 2025 due to ease of integration, low complexity, and stable monetization economics for publishers. They are the default option for AAA sports games featuring in-stadium signage and persistent in-world placements.

Dynamic ads at 35.6% offer real-time creative refresh, contextual relevance, and seamless programmatic buying, making them increasingly preferred by brand advertisers seeking measurable in-game performance. Their ability to update campaigns instantly based on user behavior and in-game context enhances targeting precision and campaign effectiveness.

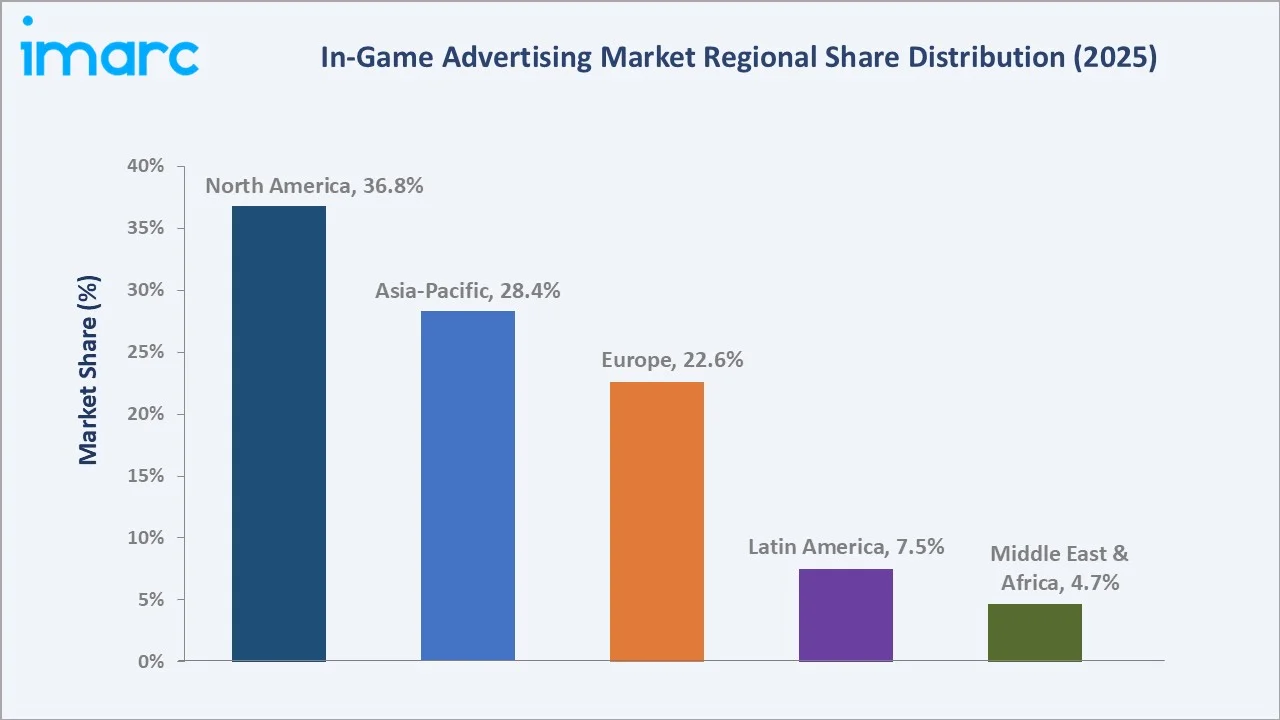

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.8% |

Mature programmatic ad ecosystems, deep advertiser networks, strong console and PC gaming culture, and high digital ad spend |

|

Asia-Pacific |

28.4% |

Large gaming user base globally, rapid mobile gaming adoption, expanding smartphone penetration, and growing esports audiences |

|

Europe |

22.6% |

Sophisticated digital advertising market, strong privacy frameworks driving contextual ad innovation, and active brand demand for gaming reach |

|

Latin America |

7.5% |

Rising smartphone affordability, expanding mobile-first gaming bases, and growing brand interest in younger digital audiences |

|

Middle East and Africa |

4.7% |

High mobile gaming uptake among younger demographics, increasing 4G/5G connectivity, and growing investments in regional gaming and esports infrastructure |

North America at 36.8% in 2025 leads the global in-game advertising market, driven by deep advertiser ecosystems, mature programmatic infrastructure, and strong AAA gaming culture across the United States and Canada. Brand budgets shifting from traditional digital channels toward gaming-native placements continue to anchor regional dominance.

Asia-Pacific at 28.4% is the highest-growth region through 2034. Strong mobile gaming penetration, expanding smartphone adoption, and rapidly growing esports audiences are driving regional momentum, particularly in China, Japan, India, and South Korea.

Competitive Landscape

The in-game advertising market is moderately fragmented, with global ad-platform leaders dominating mediation and demand aggregation while gaming-native platforms increasingly build their own first-party ad businesses. Programmatic infrastructure depth, brand-safety capabilities, and measurement integration form the key competitive moats in the category.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Amazon.com, Inc. |

Amazon DSP / Twitch ads |

Leader |

Programmatic ad delivery; gaming streaming inventory; cross-platform demand aggregation |

|

Unity Technologies |

Unity Ads |

Leader |

Engine-level ad integration; mobile gaming mediation; end-to-end developer monetization |

|

Microsoft |

Xbox Media Solutions / Activision Blizzard |

Leader |

Premium console inventory; first-party gaming reach; integrated ad-tech stack |

|

AppLovin Corp |

MAX |

Challenger |

Mobile-first ad mediation; programmatic optimization; performance marketing |

|

Roblox Corporation |

Roblox Immersive Ads/ Rewarded Video Ads |

Emerging |

First-party platform monetization; immersive ad formats; Gen Z audience reach |

Key players include Amazon.com, Inc., Unity Technologies, Microsoft, AppLovin Corp, and Roblox Corporation, among others.

Key Company Profiles

Amazon.com, Inc.

Amazon.com, Inc. operates one of the world's largest digital advertising businesses through Amazon Ads and the Amazon DSP programmatic buying platform, alongside the Twitch livestreaming platform that hosts the world's largest live gaming audience. Its reach across mobile, gaming-streaming inventory, and connected TV positions it as a central programmatic demand source for in-game advertising worldwide.

- Product Portfolio: Amazon DSP; the Twitch livestreaming platform, with cross-platform programmatic buying tools spanning mobile, gaming, and connected TV inventory.

- Recent Developments: The company is expanding programmatic advertising partnerships and enhancing access to premium gaming and streaming inventory, enabling broader advertiser reach and improved monetization across integrated digital ecosystems.

- Strategic Focus: Programmatic ad delivery at global scale, gaming streaming inventory through Twitch, and cross-platform demand aggregation across mobile, console, and CTV environments.

Microsoft

Microsoft is one of the largest gaming companies globally through its Xbox Media Solutions advertising platform and the Activision Blizzard publishing portfolio. Its first-party gaming reach gives it direct control over premium console and PC ad inventory.

- Product Portfolio: Xbox Media Solutions advertising platform, Activision Blizzard franchises, and Microsoft Advertising for cross-channel demand.

- Recent Developments: In March 2025, During Microsoft Advertising Accelerate, Microsoft unveiled AI-powered solutions to enhance its offerings, such as its advertising platform. App Campaigns were launched to expand advertisement reach throughout King and Microsoft Casual Games, along with the Windows Start Menu.

- Strategic Focus: Premium first-party console inventory, integration of advertising with free-to-play titles, and leveraging Activision Blizzard's mobile gaming franchises through King.

AppLovin Corp

AppLovin Corp is a leading mobile marketing software company that operates MAX, a programmatic mediation platform, and the MoPub-acquired exchange business, serving thousands of mobile game developers globally.

- Product Portfolio: MAX mediation platform, MoPub mobile exchange.

- Recent Developments: The company has expanded its platform capabilities into connected TV, enabling a more unified advertising ecosystem across mobile gaming and CTV environments. It is also strengthening its programmatic optimization tools and data-driven targeting capabilities to enhance advertiser performance and monetization outcomes.

- Strategic Focus: Mobile-first ad mediation at global scale, performance marketing for game developers, and expansion into adjacent CTV and cloud gaming inventory pools.

Market Concentration Analysis

The in-game advertising market is moderately concentrated, with Amazon.com, Inc., Unity Technologies, Microsoft, AppLovin Corp, and Roblox Corporation collectively shaping a significant share of programmatic in-game inventory and demand aggregation in 2025.

Barriers to entry include established advertiser-and-agency relationships, scale of mediation infrastructure, brand-safety verification capabilities, and access to premium first-party game inventory. Independent players specialize in intrinsic ad placement, while platform-native businesses build first-party ad capabilities to capture more of the value chain.

Consolidation continues through strategic acquisitions, mediation-platform mergers, and partnerships between game publishers and ad-tech specialists, reinforcing the competitive position of well-capitalized incumbents with cross-platform reach.

Investment & Growth Opportunities

Fastest-Growing Segments

Dynamic ads and advergaming are the highest-momentum sub-categories, growing faster than the overall 8.43% market CAGR through 2034 due to programmatic delivery economics and brand demand for immersive experiences. Smartphone/tablet inventory continues to expand rapidly, fueled by mobile gaming penetration in emerging markets.

Emerging Markets

Asia-Pacific at 28.4% is the highest-growth region, with rapid mobile gaming adoption in India, Southeast Asia, and Japan unlocking new audiences. Latin America and the Middle East and Africa together represent significant untapped opportunity as smartphone affordability and 4G/5G expansion accelerate.

Venture & Investment Trends

Investment is concentrating on programmatic in-game ad networks, AI-driven creative optimization, intrinsic ad placement engines, and rewarded video infrastructure. Cross-platform measurement vendors and brand-safety verification specialists are also attracting capital as advertisers demand parity with display and CTV measurement standards.

Future Market Outlook (2026-2034)

The in-game advertising market is forecast to expand from USD 9.41 Billion in 2025 to USD 19.92 Billion by 2034 at a CAGR of 8.43%, adding approximately USD 10.51 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: AI-driven dynamic ad insertion becoming the default delivery mode, the rise of cloud gaming inventory delivering CTV-like ad economics, growing in-game ad spend on console and AAA PC titles, and continued expansion of rewarded video and value-exchange formats across mobile.

By 2034, in-game advertising is expected to be a mainstream brand-budget channel rather than a niche experiment. Publishers, ad-tech providers, and platform-native businesses will collectively transform how brands engage with the global gaming audience.

Research Methodology

Primary Research

Primary research included interviews with senior product managers at leading ad-tech platforms, game publishers, agency trading-desk leaders, and brand-side media buyers, validating market sizing, regional demand, device-type splits, and ad-format share evolution.

Secondary Research

Secondary sources included annual reports, regulatory filings, investor presentations from listed ad-tech and gaming companies, industry trade publications, government statistical agencies, and academic literature on digital advertising and consumer behavior.

Forecasting Models

Market forecasts used top-down and bottom-up models combining gaming user growth, ad-load and CPM evolution by device type, mobile gaming penetration, and macroeconomic ad-spend indicators. Scenario analysis addressed regulatory and tracking-restriction sensitivity.

In-Game Advertising Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Static Ads, Dynamic Ads, Advergaming |

| Device Types Covered | PC/Laptop, Smartphone/Tablet |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Amazon.com, Inc., Unity Technologies, Microsoft, AppLovin Corp, Roblox Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the in-game advertising market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global in-game advertising market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the in-game advertising industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the In-Game Advertising Market Report

The in-game advertising market was valued at USD 9.41 Billion in 2025, driven by mobile gaming penetration, programmatic ad delivery expansion, and growing brand demand for gaming audiences.

The market is projected to grow at 8.43% CAGR from 2026 to 2034, reaching USD 19.92 Billion, supported by intrinsic ad formats, rewarded video adoption, and esports.

PC/laptop leads at 57.6% in 2025, driven by long session lengths and AAA inventory. Smartphone/tablet at 42.4% expands rapidly through mobile gaming growth.

Static ads dominate at 43.2% in 2025, driven by ease of integration, lower implementation costs, and widespread adoption across casual and mobile gaming environments. Dynamic ads at 35.6% are growing through programmatic delivery.

North America commands 36.8% in 2025, led by the United States, supported by advanced digital advertising ecosystems, strong brand participation, and early adoption of in-game monetization strategies. Asia-Pacific at 28.4% is the fastest-growing region through 2034.

Leading parent companies include Amazon.com, Inc., Unity Technologies, Microsoft, AppLovin Corp, and Roblox Corporation.

Intrinsic ads are favored for non-disruptive integration, programmatic delivery efficiency, brand-safety alignment, and measurable ad performance, enabling brands to reach gaming audiences without breaking immersion.

Rewarded video offers consent-based viewing where players opt in for in-game incentives, delivering high completion rates, strong viewability, and strong brand recall across mobile and web games.

AI powers dynamic creative optimization, contextual targeting, brand-safety classification, and audience segmentation, enabling real-time creative swaps without code changes across mobile, PC, and console environments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)