Immunoglobulin Market Size, Share, Trends and Forecast by Product, Application, Mode of Delivery, and Region, 2025-2033

Immunoglobulin Market Size and Share:

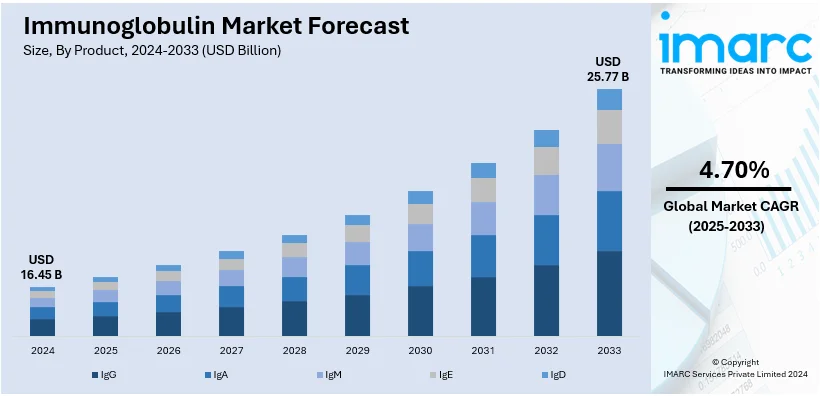

The global immunoglobulin market size was valued at USD 16.45 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 25.77 Billion by 2033, exhibiting a CAGR of 4.70% during 2025-2033. North America currently dominates the market with 46.5% of the share in 2024. The market is primarily driven by the rising incidences of immune disorders, increasing geriatric population, ongoing advancements in immunotherapy treatments, expanding product employment in neurology and hematology, and growing awareness about primary immunodeficiency disorders (PIDD) and other autoimmune diseases.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 16.45 Billion |

|

Market Forecast in 2033

|

USD 25.77 Billion |

| Market Growth Rate (2025-2033) | 4.70% |

The main driving factor of the market is the increased prevalence of immunodeficiency disorders, such as primary and secondary immunodeficiencies, raising the demand for immunoglobulin therapies. Moreover, ongoing clinical research, along with innovation in immunoglobulin formulations, such as subcutaneous and intravenous delivery methods, is providing an impetus to market growth. For instance, on October 22, 2024, Otsuka Pharmaceutical released promising interim results for their Phase 3 VISIONARY study regarding sibeprenlimab to treat adult patients with IgAN. The study met the primary endpoint after nine months by showing a clinically significant decrease in 24-hour uPCR compared with placebo, without compromising safety. Apart from this, rising awareness and diagnosis of autoimmune diseases have increased the usage of immunoglobulins as an effective treatment modality.

The market in the United States is experiencing significant growth due to the increasing incidence of rare neurological disorders, such as myasthenia gravis and multifocal motor neuropathy, which has fueled demand for immunoglobulin therapies. Apart from this, the presence of advanced healthcare infrastructure in the United States enabling better access to high-cost treatments, is positioning the country as a significant market for immunoglobulin products. Besides this, the implementation of favorable initiatives and tested approvals in the United States further enables wider access to immunoglobulin treatments, ensuring sustained market growth and innovation in this sector. On June 17, 2024, Grifols announced that its subsidiary, Biotest, secured U.S. FDA approval for Yimmugo, an intravenous immunoglobulin therapy for primary immunodeficiencies. This marks Biotest's first FDA-approved treatment, manufactured at its new "Next Level" facility in Dreieich, Germany. The U.S. launch of Yimmugo® in the latter half of 2024 is expected to significantly contribute to Grifols Group's sales and support its future growth strategy.

Immunoglobulin Market Trends:

Increasing prevalence of immune disorders

The rising incidence of immune disorders, such as PIDD, chronic inflammatory demyelinating polyneuropathy (CIDP), and Kawasaki disease, is one of the key trends driving the immunoglobulin market. For instance, the number of new cases per year of CIDP is about 1-2 per 100,000 people. These disorders weaken the body's immune system, making it more susceptible to infections. With a growing number of patients being diagnosed with immune-related conditions, the demand for immunoglobulin therapies is on the rise. PIDD, which comprises over 300 different rare conditions, is gaining increased attention in both developed and emerging economies. Early diagnosis and treatment are critical in managing these conditions, which is further increasing the immunoglobulin demand as the primary treatment option.

Advancements in plasma-derived therapies

Continual advancements in plasma-derived therapies are a significant growth-inducting factor for the market. Primarily, immunoglobulin is derived from human plasma. Technological advancements along the lines of plasma collection and purification further enhance production efficiency. These innovations contribute to a more reliable supply of immunoglobulin products. Additionally, innovations in manufacturing processes improve the quality, safety, and efficacy of these therapies. The development of SCIG products, which allow for self-administration at home, facilitates patient convenience and adherence to treatment. Furthermore, the emergence of recombinant immunoglobulin products, which do not rely on plasma donations, has the potential to alleviate supply constraints while offering an alternative therapeutic option, thereby supporting the immunoglobulin market growth.

Expanding applications in various medical fields

The expanding application of immunoglobulin therapies in various medical fields is providing an impetus to market growth. Beyond its traditional usage in immunology, immunoglobulin is widely employed in neurology, hematology, and even oncology. For instance, the United States spent USD 99 billion on oncology in 2023, up from USD 65 billion in 2019. For example, in neurology, immunoglobulin therapies are increasingly used to treat conditions like Guillain-Barré syndrome, multiple sclerosis, and myasthenia gravis. In hematology, immunoglobulins are used to manage autoimmune hemolytic anemia and idiopathic thrombocytopenic purpura (ITP). These expanding applications are supported by ongoing clinical trials and research efforts exploring the use of immunoglobulins for a wider range of diseases, thus positively impacting the immunoglobulin market outlook.

Immunoglobulin Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global immunoglobulin market, along with forecasts at the global, regional, and country levels from 2025-2033. The market has been categorized based on product, application, and mode of delivery.

Analysis by Product:

- IgG

- IgA

- IgM

- IgE

- IgD

IgG leads the market with 42.2% of the share in 2024 due to its widespread therapeutic use and central role in the proper functioning of the immune system. As the most abundant antibody circulating in the bloodstream, IgG is indispensable in neutralizing pathogens and mediating immune responses; therefore, it forms an important component in the treatment of primary immunodeficiency diseases, autoimmune diseases, and a variety of infections. Its increasing global prevalence has increased the demand for IgG therapies. Advancements in IgG technology also include enhancement of its purity by extraction, and methods of administration with better efficiency have increased patient safety and acceptance toward it, resulting in adoption.

Analysis by Application:

- Hypogammaglobulinemia

- Chronic Inflammatory Demyelinating Polyneuropathy (CIDP)

- Immunodeficiency Disease

- Myasthenia Gravis

- Others

In 2024, immunodeficiency diseases lead the market due to a high and increasingly large prevalence. Immunodeficiency diseases, which comprise primary immunodeficiency diseases, are characterized by a weakened immune system, with patients being very susceptible to infections. Immunoglobulin therapy has become a cornerstone in managing these conditions; it provides patients with essential antibodies that bolster their immune defense. The increase in the incidence of PIDs across the globe, in conjunction with improved diagnostics, raises demand for immunoglobulin products. Increased accessibility due to growth in healthcare infrastructure, as well as entry into specialty treatment centers, expands a patient's access for treatment.

Analysis by Mode of Delivery:

- Intravenous Mode of Delivery

- Subcutaneous Mode of Delivery

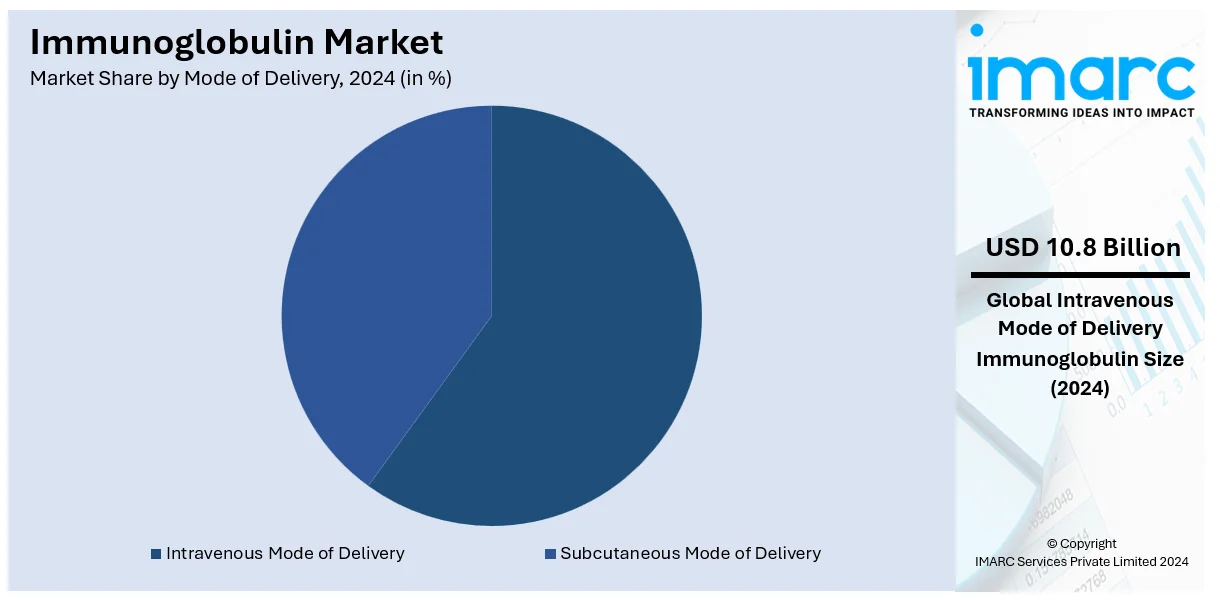

Intravenous mode of delivery leads the market with 46.5% of the share in 2024. The efficiency and application for treating numerous immune-related conditions provided by intravenous mode of delivery drives its usage in such treatments. Severe and acute conditions like primary immunodeficiency diseases (PIDs), Kawasaki disease, and some neurological disorders require the intravenous delivery of IVIG for its quick bioavailability and therapeutic impact. The growing incidence of these conditions, combined with improvements in the formulation of IVIG, which makes it safer and more convenient for patients, increases demand for this product. Healthcare providers and patients prefer the intravenous route, as it has been well-established to be effective in the treatment of life-threatening complications.

Analysis by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America leads the immunoglobulin market with 46.5% of the share, due to its advanced health care infrastructure, awareness regarding diseases, and significant expenditure towards research and development (R&D) activities. Its well-built diagnostic capabilities help to recognize the primary condition, that is, immune deficiencies and autoimmune disorders, and therefore create a regular demand for immunoglobulin therapies. Also, an increased older population at higher risk for immune-related disorders results in demand for immunoglobulin. The increasing incidence of primary immunodeficiency diseases, neurological disorders such as Guillain-Barré syndrome, and chronic inflammatory demyelinating polyneuropathy are driving growth in the market. The presence of key biopharmaceutical companies and facilitative regulatory environments make it easier for innovative immunoglobulin products to get through to the market. Positive recompense policies further boost market growth.

Key Regional Takeaways:

United States Immunoglobulin Market Analysis

The US accounted for 83.30% of the overall North America immunoglobulin market share in 2024. Massive growth in the adoption of immunoglobulin treatments is being encouraged in the region due to increasing emphasis on developing advanced healthcare systems. The need for better patient outcomes results in significant investment in healthcare services and biopharmaceutical inventions, which ensures the availability of therapies regarding immune deficiencies. For instance, U.S. healthcare companies are securing venture capital deals of USD 15 Million plus are driving robust investment growth, focusing on innovation in medical technology to meet rising market demands. Expanded access to immunoglobulin products via specialized centers and ongoing improvements in administration techniques streamline the treatment process. Support for rare disease management and comprehensive insurance coverage further supports the adoption of treatments. Improved diagnostics are also instrumental, allowing for earlier detection and more targeted therapeutic interventions. Interdisciplinary collaboration between healthcare providers and research institutes is fueling clinical development and optimizing patient care. Efforts to educate healthcare professionals about the most advanced treatments are empowering the wide usage of immunoglobulin therapies. As funding grows, healthcare systems are better equipped to integrate immunoglobulin into treatment protocols, reinforcing its role in addressing immune-related conditions.

Asia Pacific Immunoglobulin Market Analysis

The rise in immunoglobulin utilization in the region is due to the increase in conditions which require immune system modulation. According to National Library of Medicine, the estimated number of incident cases of cancer in India for the year 2022 was found to be 14,61,427. With more patients diagnosed at advanced stages, the demand for supportive therapies has increased. Expanding medical research focused on adjunctive treatments complements chemotherapy and radiotherapy. Enhanced clinical trial frameworks pave the way for innovations, ensuring tailored solutions for unique patient needs. Hospitals are incorporating cutting-edge biotherapeutic products into treatment guidelines, reflecting a commitment to comprehensive care. Strategic alliances among healthcare providers and educational institutions are fostering awareness regarding immunoglobulin therapies. Upgraded healthcare technologies facilitate the integration of these treatments into routine care. Such advancements, along with patient-centric models, are creating an environment conducive to greater therapeutic adoption. Increased accessibility to specialized medicines is empowering practitioners to incorporate them into a broader spectrum of treatment approaches.

Europe Immunoglobulin Market Analysis

The aging demographic in the region significantly influences the growing application of immunoglobulin therapies. For instance, Europe's ageing population is on the rise, with one in five Europeans now aged 65 or older, projected to approach 30% by 2050. Older adults are more prone to chronic and autoimmune diseases, necessitating comprehensive immune support. Healthcare services are adapting to meet the specific needs of this group, integrating therapies that address immune system vulnerabilities. Regulatory frameworks support the availability of treatments tailored for geriatric care. Continuous advancements in medical education highlight the critical role of immunoglobulin in enhancing life quality among the elderly. Hospitals are expanding immunotherapy units to cater to increased demand, supported by dedicated research programs exploring age-specific applications. The push for seamless patient care experiences includes access to therapies that improve immune function. Elderly-focused healthcare policies emphasize the importance of accessible and effective treatments, driving the systematic inclusion of immunoglobulin in therapeutic regimens.

Latin America Immunoglobulin Market Analysis

Enhanced private healthcare establishments in the region are driving the integration of immunoglobulin therapies. According to International Trade Administration, Brazil is the largest healthcare market in Latin America with 7,191 hospitals, 62% are private. Advanced medical facilities are offering treatments that cater to diverse patient needs. Investments in private sectors are enabling the establishment of state-of-the-art centers equipped with modern therapeutic solutions. Specialized healthcare providers are expanding their service portfolios to include immune-focused therapies. Increased collaboration with global institutions ensures that innovative solutions are implemented swiftly. Educational initiatives are informing professionals about the benefits of advanced treatment modalities, encouraging their inclusion in clinical practice. Such developments ensure that immunoglobulin adoption aligns with the growing expectations of quality care delivery.

Middle East and Africa Immunoglobulin Market Analysis

Upgraded healthcare facilities in the region are propelling immunoglobulin applications across various therapeutic areas. According to Dubai Healthcare City Authority report, Dubai's healthcare sector saw rapid growth, with 4,482 private medical facilities and 55,208 licensed professionals by 2022, projected to expand further by 3-6% in facilities and 10-15% in professionals in 2023. The establishment of well-equipped medical centers is creating opportunities to include cutting-edge treatments in standard care practices. Regional healthcare improvements emphasize addressing immune deficiencies with effective biotherapeutics. Specialized services within advanced facilities are incorporating immunoglobulin-based interventions to address a wide range of health conditions. Growing emphasis on patient-centric care and the alignment of health services with global standards are fostering widespread therapy utilization. Enhanced accessibility to immune-focused treatments is enabling healthcare providers to cater to broader patient demographics efficiently.

Competitive Landscape:

The competitive landscape of the market has key players capturing a significant part of the market share, especially with established networks of plasma collection, advanced manufacturing processes, and strong product portfolios. Intense competition is thus created around product formulations, particularly concerning the development of subcutaneous and IVIG therapies that can advance patient outcomes and convenience. In parallel, continuous efforts are placed on supply chains and increasing capacities to produce goods to meet a growing demand. With these considerations, plasma producers have huge entrance barriers mainly characterized by intricate requirements in the aspect of regulatory laws and rather stringent standards of quality. Companies make considerable mergers and acquisitions for strengthened market position along with strategic partnering. Furthermore, research and development (R&D) for recombinant immunoglobulins, as well as alternate forms of therapies, raise the dynamics of competition within this industry.

The report provides a comprehensive analysis of the competitive landscape in the immunoglobulin market with detailed profiles of all major companies, including:

- ADMA Biologics Inc.

- Baxter international Inc.

- Biotest AG

- CSL Limited

- Grifols S.A

- Kedrion S.p.A

- LFB SA

- Octapharma AG

- Sanquin Plasma Products B.V.

- Takeda Pharmaceutical Company Limited

Latest News and Developments:

- January 2025: Innovent Biologics announced a collaboration with Roche to advance IBI3009, a DLL3-targeted antibody-drug conjugate for small cell lung cancer. IND approvals were secured in Australia, China, and the U.S., with Phase 1 dosing initiated in December 2024. This partnership enhances innovative treatment access for oncology patients globally.

- December 2024: Epsilogen has launched a Phase Ib trial to evaluate MOv18 IgE, an IgE antibody targeting folate receptor alpha, in platinum-resistant ovarian cancer (PROC). This open-label trial (NCT06547840) will enroll 45 PROC patients and assess safety, tolerability, and efficacy. MOv18 IgE, the first IgE antibody therapeutic, has shown safety and anti-tumor activity in earlier studies, promising insights into its mechanism of action.

- December 2024: Annexon, Inc. announced positive topline results from a real-world study comparing ANX005 to intravenous immunoglobulin (IVIg) or plasma exchange (PE) in treating Guillain-Barré Syndrome (GBS). The study, using a matched cohort of 79 patients, supports ANX005 as a promising immunotherapy targeting C1q to halt disease progression. GBS remains without FDA-approved treatments, highlighting ANX005's potential impact in addressing this acute neuromuscular disease.

- December 2024: Merck announced the FDA's acceptance of its Biologics License Application for clesrovimab, a long-acting monoclonal antibody designed to protect infants against RSV during their first season. If approved by June 2025, it would become the first single-dose immunization for this purpose. This milestone reflects progress in addressing unmet RSV prevention needs. Merck aims for availability by the 2025-26 RSV season.

- February 2024, AbbVie Inc. and OSE Immunotherapeutics SA announced a strategic partnership to advance OSE-230, a novel monoclonal antibody targeting ChemR23, currently in pre-clinical development. This collaboration aims to explore OSE-230's potential in resolving chronic inflammation by modulating macrophages and neutrophils. AbbVie's Jonathon Sedgwick and OSE's Nicolas Poirier highlighted the partnership's significance in enhancing treatment options for inflammatory diseases and advancing both companies' R&D efforts.

Immunoglobulin Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | IgG, IgA, IgM, IgE, IgD |

| Applications Covered | Hypogammaglobulinemia, Chronic Inflammatory Demyelinating Polyneuropathy (CIDP), Immunodeficiency Disease, Myasthenia Gravis, Others |

| Mode of Deliveries Covered | Intravenous Mode of Delivery, Subcutaneous Mode of Delivery |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ADMA Biologics Inc., Baxter international Inc., Biotest AG, CSL Limited, Grifols S.A, Kedrion S.p.A, LFB SA, Octapharma AG, Sanquin Plasma Products B.V., Takeda Pharmaceutical Company Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the immunoglobulin market from 2019-2033.

- The immunoglobulin market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the immunoglobulin industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

Immunoglobulin, commonly known as antibodies, are specialized proteins produced by plasma cells in response to foreign substances like bacteria, viruses, and toxins. They play a crucial role in the immune system by identifying and neutralizing harmful invaders, aiding in maintaining health and immunity. These proteins are essential in diagnosing and treating immune deficiencies and autoimmune diseases.

The Immunoglobulin market was valued at USD 16.45 Billion in 2024.

IMARC estimates the global Immunoglobulin market to exhibit a CAGR of 4.70% during 2025-2033.

The global immunoglobulin market is driven by increasing prevalence of autoimmune and immunodeficiency diseases, advancements in plasma-derived therapies, rising geriatric population, and growing awareness regarding early diagnosis and treatment of immune-related conditions.

According to the report, IgG represented the largest segment by product, driven by its widespread usage in treating immunodeficiency disorders, autoimmune diseases, and increasing demand for plasma-derived immunoglobulin therapies worldwide.

According to the report, immunodeficiency diseases represented the largest segment by component, driven by rising cases of primary and secondary immunodeficiency disorders, increased diagnostic capabilities, and greater availability of effective immunoglobulin-based treatments.

According to the report, intravenous mode represented the largest segment by component, driven by its effectiveness in providing rapid systemic distribution, established use in clinical settings, and ongoing advancements in intravenous immunoglobulin formulations.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein North America currently dominates the global market.

Some of the major players in the global Immunoglobulin market include ADMA Biologics Inc., Baxter international Inc., Biotest AG, CSL Limited, Grifols S.A, Kedrion S.p.A, LFB SA, Octapharma AG, Sanquin Plasma Products B.V., and Takeda Pharmaceutical Company Limited, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)