Hyperlipidemia Drugs Market Size, Share, Trends and Forecast by Drug Type, End User, and Region, 2025-2033

Hyperlipidemia Drugs Market Size and Share:

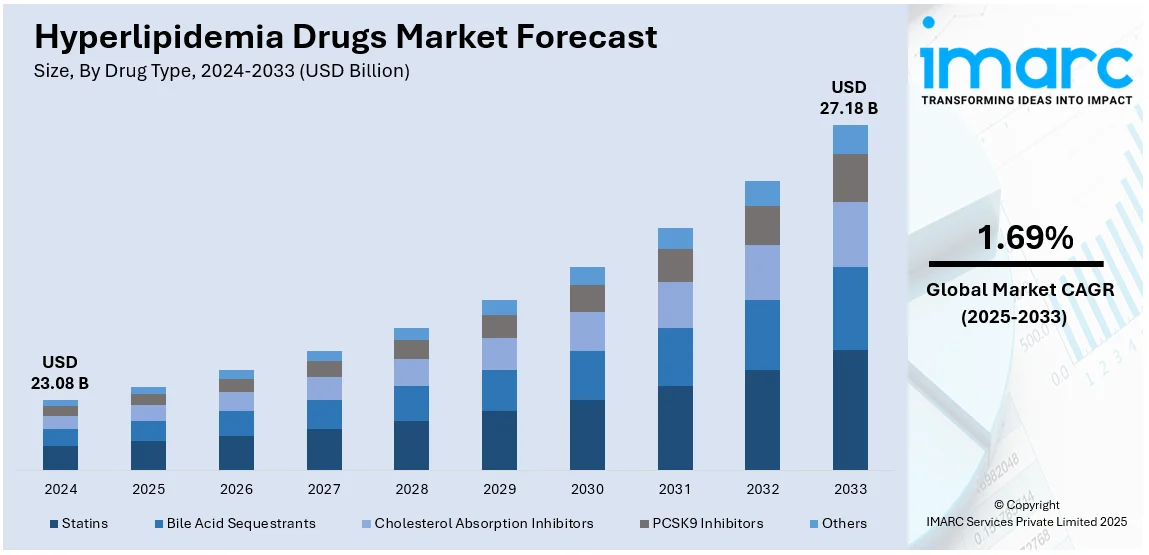

The global hyperlipidemia drugs market size was valued at USD 23.08 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 27.18 Billion by 2033, exhibiting a CAGR of 1.69% during 2025-2033. Europe currently dominates the market, holding a significant market share of over 39.0% in 2024. The growing adoption of novel lipid-lowering therapies, favorable government policies and regulatory approvals, rising medical expenditure, and increasing awareness regarding cardiovascular risk management among the masses are some of the factors positively impacting the hyperlipidemia drugs market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 23.08 Billion |

|

Market Forecast in 2033

|

USD 27.18 Billion |

| Market Growth Rate (2025-2033) | 1.69% |

The global market is majorly influenced by the increasing prevalence of hyperlipidemia due to sedentary lifestyles, poor dietary habits, and obesity. Additionally, continual advancements in lipid-lowering therapies are expanding treatment options. Also, expanding healthcare infrastructure and greater access to medical services in emerging economies are improving drug uptake, which is facilitating market expansion. The implementation of favorable regulatory policies supporting drug approvals and reimbursement policies for statins and combination therapies are also enhancing hyperlipidemia drug market growth. Moreover, pharmaceutical companies' strategic initiatives for novel drug development and lifecycle management are increasing market penetration. For example, on April 29, 2024, the University of Helsinki announced the establishment of Moncyte Oy, a spinout company focused on personalizing high cholesterol treatments. Moncyte has developed a patented technology that analyzes cellular mechanisms affecting the efficacy of cholesterol-lowering drugs, enabling tailored therapies for patients. This innovation aims to expedite the achievement of target cholesterol levels, thereby reducing the risk of cardiovascular diseases.

The United States is a significant region in the market, primarily driven by increased healthcare spending coupled with favorable insurance coverage for lipid-lowering agents. Expanding clinical research on next-generation lipid-modifying therapies, including bempedoic acid and gene-silencing treatments, is diversifying available treatment options. In line with this, the growing emphasis on preventive cardiology and the implementation of favorable initiatives across healthcare settings is supporting the market. On September 16, 2024, in order to prevent one Million heart attacks and strokes by 2027, the Centers for Medicare & Medicaid Services and the CDC renewed their dedication to the Million Hearts project. In addition to encouraging the ABCS of cardiovascular health and raising involvement in cardiac rehabilitation, the program places a high priority on lowering air pollution, tobacco use, and physical inactivity. Million Hearts 2027 incorporates strategies to address social determinants of health and enhance health outcomes across the country, acknowledging differences in the prevalence of heart disease.

Hyperlipidemia Drugs Market Trends:

Emergence of RNA-Based Therapies for LDL Reduction

The increased investment in RNA-based therapies, particularly small interfering RNA (siRNA) and antisense oligonucleotides (ASOs) is supporting the hyperlipidemia drugs market demand. These therapies target hepatic pathways involved in lipid metabolism, offering sustained LDL-C reduction with less frequent dosing. Major pharmaceutical companies are expanding pipelines with novel RNA-based candidates targeting apolipoprotein B (ApoB) and angiopoietin-like protein 3 (ANGPTL3), aiming for broader lipid management beyond LDL-C reduction. Regulatory agencies are increasingly approving these approaches, given their efficacy in reducing cardiovascular risk. Long-term safety and cost-effectiveness remain key considerations, shaping market adoption and driving competition among innovative lipid-lowering therapies. On May 29, 2024, Mount Sinai researchers announced that an investigational small interfering RNA (siRNA) therapy, zodasiran, effectively reduced various cholesterol and triglyceride levels in individuals with mixed hyperlipidemia. The phase 2b global trial demonstrated significant reductions in triglycerides (54–74%), LDL cholesterol (up to 20%), non-HDL cholesterol (up to 36%), and remnant cholesterol (73–82%) compared to placebo. These findings suggest that zodasiran could offer a promising alternative to conventional therapies for patients with persistent lipid elevations.

Shift Toward Fixed-Dose Combination Therapies

The market is shifting towards combination therapies with the integration of multiple lipid-lowering agents in a single formulation, which is enhancing the hyperlipidemia drugs market outlook. On March 22, 2024, Ezetimibe, bempedoic acid, and the fixed-dose combination tablet of the two were approved by the European Medicines Agency's Committee for Medicinal Products for Human Use (CHMP). Analysis from the Phase 3 CLEAR Outcomes trial, which showed notable decreases in cardiovascular events and low-density lipoprotein cholesterol (LDL-C), served as the basis for these recommendations. This market trend is due to the increased medication adherence, decreased treatment burden, and optimized treatment intensity account for the overall push for the administration of the lipid-lowest combination: statins/ezetimibe and PCSK9 inhibitors. Pharmaceutical companies are focusing on developing novel FDCs that incorporate RNA-based or bempedoic acid-based therapies in high-risk patients with statin intolerance or an insufficient response to monotherapy.

Expanding Market Penetration in Emerging Economies

One of the significant hyperlipidemia drugs market trends is the increasing awareness of cardiovascular risk factors, which is driving diagnosis rates. In the emerging economies. The drugs for hyperlipidemia are witnessing tremendous growth in emerging economies with the increase in health issues, obesity, and cardiovascular diseases. As per WHO, cholesterol contributes to 29.7 Million DALYS, or 2% of all DALYS, and 2.6 Million fatalities, or 4.5% of all deaths. The aging population, which is more prone to cardiovascular diseases and high cholesterol, is also driving the market. The adoption of government policies in preventive care is driving demand for lipid-lowering treatments. PCSK9 inhibitors and bempedoic acid are gradually being launched through tiered pricing strategies and local partnerships. Major pharmaceutical companies are now shifting focus towards regional collaborations to overcome the complexity of regulation and increase access. Digital health initiatives and telemedicine further enable the management of lipids by increasing patient involvement and adherence in regions where there is limited access to healthcare.

Hyperlipidemia Drugs Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global hyperlipidemia drugs market, along with forecasts at the global, regional, and country levels from 2025-2033. The market has been categorized based on drug type, and end user.

Analysis by Drug Type:

- Statins

- Bile Acid Sequestrants

- Cholesterol Absorption Inhibitors

- PCSK9 Inhibitors

- Others

Statins lead the market with around 45.9% of market share in 2024 due to their well-established efficacy in reducing levels of low-density lipoprotein (LDL) cholesterol. As first-line therapy, they are widely prescribed for managing hyperlipidemia, particularly in patients with high cholesterol and those at risk of atherosclerotic cardiovascular disease. It has been characterized extensively through the inhibition of HMG-CoA reductase, which builds confidence in it among physicians and enhances its wide clinical uptake. This remains the most cost-effective therapy given how high prescription rates are worldwide despite the competition that PCSK9 inhibitors and other new lipid-lowering therapies bring. Statins, atorvastatin, rosuvastatin, and simvastatin will maintain their market share largely due to generic availability, affordability, and widespread real-world data supporting long-term safety and efficacy.

Analysis by End User:

- Hospitals

- Clinics

- Others

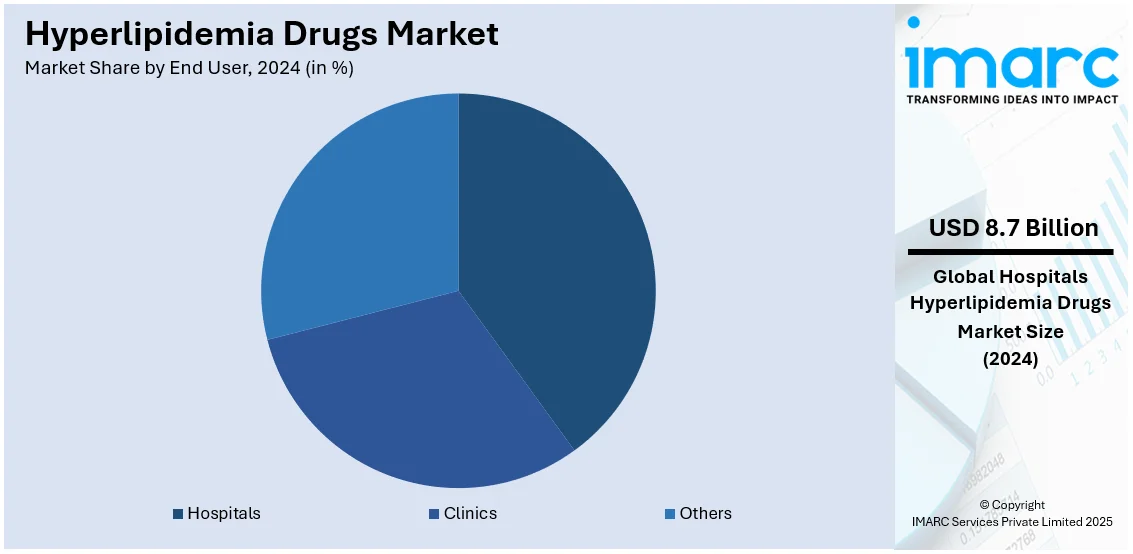

Hospitals lead the market with around 37.6% of market share in 2024 as are they are critical to the management of high-risk patients with severe lipid disorders and cardiovascular conditions. They serve as primary treatment centers for acute cardiovascular events, where lipid-lowering therapies, including statins and adjunctive drugs, are prescribed for both immediate intervention and long-term management. Hospitals also conduct lipid profile screenings, ensuring early diagnosis and treatment initiation. With access to specialized cardiologists and lipidologists, hospitals drive adherence to guideline-based therapies, including combination treatments for patients unresponsive to statins alone. They also promote newer lipid-lowering drugs like PCSK9 inhibitors and bempedoic acid, especially for high-risk or statin-intolerant patients.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

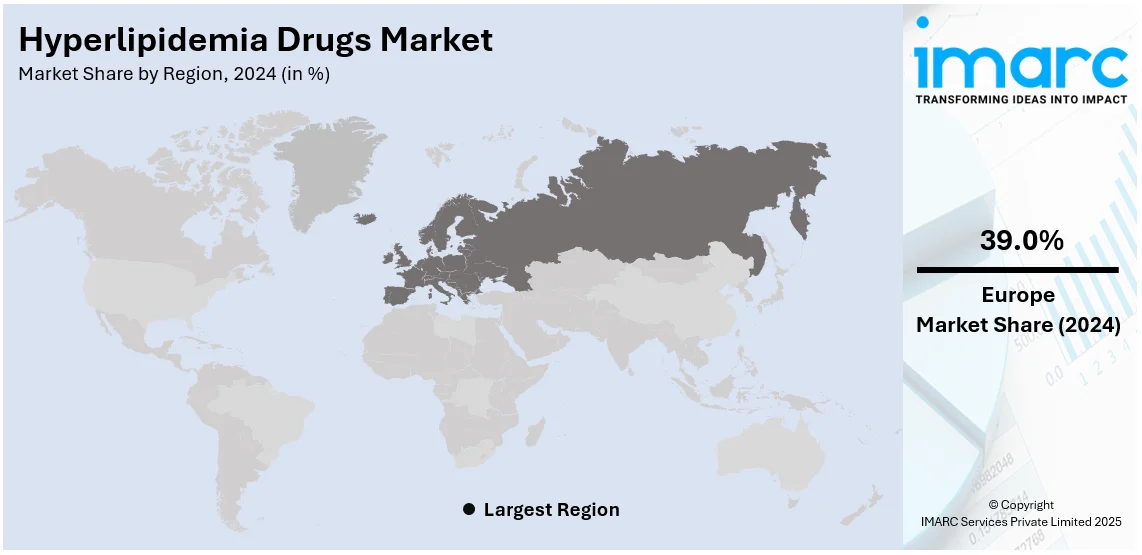

In 2024, Europe accounted for the largest market share of over 39.0% due to the presence of an aging population, high prevalence of cardiovascular diseases, and well-established healthcare infrastructure. The area also has a rising need for high-end lipid-lowering treatments, such as PCSK9 inhibitors and bempedoic acid, especially in high-risk patients with a certain intolerance to statin treatment. Strict regulatory standards and cost-containment measures influence drug pricing and market access, shaping competition among branded and generic products. The government-initiated preventive healthcare measures and cholesterol screening programs ensure early diagnosis and consequent treatment initiation. The increasing burden of obesity and sedentary lifestyles further accelerates demand for hyperlipidemia management. With continuous innovation and research in cardiovascular therapeutics, Europe remains a key market for lipid-lowering drugs, influencing global treatment trends and pharmaceutical investments.

Key Regional Takeaways:

United States Hyperlipidemia Drugs Market Analysis

The United States holds a substantial share of the North American hyperlipidemia drugs market at 82.00%. The rising levels of obesity lead to the increased demand for advanced treatments, which is driving the adoption of hyperlipidemia drugs. According to the Institute for Health Metrics and Evaluation, by 2050, it is anticipated that there will be 43.1 Million overweight and obese children and adolescents in the US (up 6.74 Million from 2021) and 213 Million adults (up 41.4 Million). The increased cholesterol levels are linked to changed dietary habits and sedentary lifestyles. Therefore, it is essential to control lipid-related disorders through timely medical interventions. Medical institutions have intensified the effort to sensitize people to the control of cholesterol, urging for earlier diagnosis and treatment. Advances in pharmacy present an innovative formulation targeting the effective treatment of obesity-related lipid imbalances. Furthermore, strong emphasis by healthcare providers on preventive care and treatment of individuals before the complication stage supports the market growth. Also, the widespread availability through well-established channels ensures the utilization of these drugs. In addition, increased interest in reducing obesity's long-term implications for public health creates opportunities for collaborations between research institutes and clinicians to enhance drug safety and efficacy, thereby increasing its uptake.

Asia Pacific Hyperlipidemia Drugs Market Analysis

Diabetes prevalence has emerged as a major concern, leading to a surge in the adoption of hyperlipidemia drugs across the region. The World Health Organization (WHO) estimates that 77 Million adults in India over the age of 18 have type 2 diabetes, and almost 25 Million are prediabetics, which denotes that they have a higher chance of getting the disease in the near future. Since diabetes often accompanies abnormal cholesterol levels, the demand for proper lipid management is on the rise. Healthcare systems in the region mainly focus on comprehensive strategies to prevent complications related to diabetes and incorporate cholesterol management into regular care. Increasing awareness among people regarding the relationship between diabetes and cardiovascular risks significantly promotes early intervention. In recent years, diagnostic efforts have increased in an attempt to identify lipid abnormalities so that timely treatment can be initiated. The increasing affordability of formulations for a wide range of populations has increased their availability further. In addition, campaigns aimed at disease management encourage regular medication use and, therefore, greater compliance. The establishment of modern healthcare infrastructure helps the widespread distribution of these treatments to ensure that they are available across all sections of society.

Europe Hyperlipidemia Drugs Market Analysis

The rising incidence of cardiovascular conditions has significantly impacted the adoption of hyperlipidemia drugs, as these conditions often stem from elevated cholesterol levels. According to WHO, cardiovascular diseases (CVDs) constitute the primary cause of mortality and disability. More than two out of five (42.5%) of all deaths in Europe in 2019 were attributed to CVDs, accounting for an estimated 4.2 Million deaths. Lifestyle shifts increase the prevalence of unhealthy lipid profiles, necessitating effective pharmaceutical solutions. The focus on reducing cardiovascular risks further drives healthcare providers to incorporate advanced lipid-lowering therapies into treatment protocols. Enhanced awareness campaigns underscore the role of cholesterol management in preventing heart-related complications, encouraging individuals to seek timely medical interventions. With better diagnostics, the medical setting has diagnosed cases of hyperlipidemia much earlier and implemented more directed treatment plans. Increasing cooperation between clinical research organizations and pharmaceutical companies also enables therapies with better safety profiles to enter the market. Healthcare professionals continue to emphasize personalized treatment regimens, ensuring that patients receive optimized care tailored to their specific risk factors and medical histories.

Latin America Hyperlipidemia Drugs Market Analysis

The expansion of private healthcare services has significantly boosted the utilization of hyperlipidemia drugs. According to the International Trade Administration, Brazil is the largest healthcare market in Latin America, with 7,191 hospitals, 62% are private. Enhanced accessibility of quality health results in patients having a better opportunity for diagnosis earlier and better management of lipid-related disorders. Private facilities progressively integrate specialized treatments, which leads to an increased uptake of advanced pharmaceutical products. Additionally, preventive care measures have also been strengthened through enlightening campaigns by healthcare providers, encouraging patients to correct cholesterol imbalances earlier. With state-of-the-art medical technology now introduced into private systems, proper and efficient diagnosis is possible, which in turn enhances the adoption of drugs. Investment in healthcare infrastructure further facilitates the accessibility and affordability of such treatments to a wider population, thereby providing an impetus to the market.

Middle East and Africa Hyperlipidemia Drugs Market Analysis

The rising number of healthcare facilities has accelerated the adoption of hyperlipidemia drugs by improving access to necessary treatments. There were 4,482 private medical facilities and 55,208 licensed professionals in Dubai's healthcare sector, which is expected to grow by another 3-6% in facilities and 10-15% in professionals in 2023, according to research by the Dubai Healthcare City Authority. Enhanced diagnostic services have enabled earlier identification of lipid-related conditions, promoting proactive management. New healthcare centers are increasingly incorporating specialized therapies into their services, offering tailored solutions for lipid abnormalities. Awareness campaigns spearheaded by medical professionals have encouraged individuals to seek timely interventions, further driving the use of advanced drug formulations. Improvements in healthcare delivery systems have ensured that more patients can benefit from comprehensive lipid management, reducing the overall burden of cholesterol-related complications.

Competitive Landscape:

The market is dynamic and highly competitive, with innovation in pharmaceuticals, patent expirations, and strategic collaborations. The main players expand their product portfolios by developing novel lipid-lowering therapies, such as PCSK9 inhibitors, bempedoic acid, and combination treatments. Generic drug manufacturers intensify competition by offering low-cost statins and fibrates, making these products more accessible in price-sensitive markets. New therapies, biosimilars, and reformulated drugs approved by the regulatory authority's impact market dynamics and pricing strategies. Advancements are further enhanced through mergers and acquisitions and research partnerships with other institutions. With increasing demand for personalized medicine and combination therapies, competition remains strong as firms seek to differentiate products based on safety, efficacy, and long-term cardiovascular benefits.

The report provides a comprehensive analysis of the competitive landscape in the hyperlipidemia drugs market with detailed profiles of all major companies, including:

- Amgen Inc.

- AstraZeneca PLC

- Daiichi Sankyo Company Limited

- Eli Lilly and Company

- Esperion Therapeutics Inc.

- GlaxoSmithKline Pharmaceuticals Limited (GlaxoSmithKline Plc)

- Immuron Limited

- Ionis Pharmaceuticals Inc.

- Merck & Co. Inc.

- Pfizer Inc.

- Sanofi S.A.

Latest News and Developments:

- January 17, 2025: Arrowhead Pharmaceuticals announced that the FDA has approved the New Drug Application (NDA) for plozasiran, a medication used to treat familial chylomicronemia syndrome. This rare genetic condition raises the risk of severe pancreatitis and causes abnormally high triglyceride levels. Positive findings from the Phase 3 PALISADE research served as the foundation for the application. If authorized, plozasiran could help treat unmet medical needs in cases with mixed hyperlipidemia and severe hypertriglyceridemia.

- November 20, 2024: NewAmsterdam Pharma revealed positive topline results from its Phase 3 TANDEM trial, with the fixed-dose combination of anacetrapib 10 mg plus ezetimibe 10 mg significantly lowering LDL-C in patients with ASCVD, ASCVD risk factors, or HeFH. The treatment reduced LDL-C by about 50% at day 84, with over 70% of patients obtaining LDL-C values below 55 mg/dL. The treatment was tolerated well and achieved all co-primary endpoints with statistical significance. The data support global regulatory filings for combination therapy.

- November 26, 2024: Otsuka Pharmaceutical submitted a New Drug Application (NDA) for bempedoic acid, which is directed against hypercholesterolemia and familial hypercholesterolemia, to Japan's Ministry of Health. Bempedoic acid has already been marketed in the U.S. and Europe. It recently showed positive results in Phase 3 trials conducted in Japan. The drug lowered LDL cholesterol considerably. There were no significant side effects, and the drug was well tolerated. Otsuka has exclusive rights for the development and commercialization of bempedoic acid in Japan.

- May 28, 2024: Baylor College of Medicine conducted a study that proved the efficacy of Plozasiran, a drug therapy that targets ApoC3 to treat hyperlipidemia. Plozasiran controls lipoprotein particles that carry triglycerides and cholesterol; it is a new treatment option for patients with high cholesterol levels. The impact of the railway system on accessibility to healthcare facilities can help in enhancing patient access to such treatments.

- March 11, 2024: FDA-approved injections of Prauluent (Alirocumab) for the pediatric market in children with high cholesterol. It helps decrease and manage levels of LDL-C earlier in life, thereby providing one important tool for managing early-onset cholesterol. Timely access to the railway system would be supportive in this regard for children needing this early intervention in managing high cholesterol.

Hyperlipidemia Drugs Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Drug Types Covered | Statins, Bile Acid Sequestrants, Cholesterol Absorption Inhibitors, PCSK9 Inhibitors, and Others |

| End Users Covered | Hospitals, Clinics, and Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Amgen Inc., AstraZeneca PLC, Daiichi Sankyo Company Limited, Eli Lilly and Company, Esperion Therapeutics Inc., GlaxoSmithKline Pharmaceuticals Limited (GlaxoSmithKline Plc), Immuron Limited, Ionis Pharmaceuticals Inc., Merck & Co. Inc., Pfizer Inc., Sanofi S.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the hyperlipidemia drugs market from 2019-2033.

- The hyperlipidemia drugs market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the hyperlipidemia drugs industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The hyperlipidemia drugs market was valued at USD 23.08 Billion in 2024.

The hyperlipidemia drugs market is projected to exhibit a CAGR of 1.69% during 2025-2033, reaching a value of USD 27.18 Billion by 2033.

The market is driven by the rising prevalence of hyperlipidemia due to sedentary lifestyles, obesity, and aging populations. Increased awareness improved diagnostic rates, and expanded healthcare access boost demand. Favorable reimbursement policies and growing adoption of statins in preventive cardiovascular care further accelerate market growth.

Europe currently dominates the hyperlipidemia drugs market, accounting for a share of 39.0% in 2024. The dominance is fueled by high disease prevalence, strong healthcare infrastructure, and widespread adoption of lipid-lowering therapies. Government initiatives, extensive research and development (R&D) investments, and favorable reimbursement frameworks support market expansion in the region.

Some of the major players in the hyperlipidemia drugs market include Amgen Inc., AstraZeneca PLC, Daiichi Sankyo Company Limited, Eli Lilly and Company, Esperion Therapeutics Inc., GlaxoSmithKline Pharmaceuticals Limited (GlaxoSmithKline Plc), Immuron Limited, Ionis Pharmaceuticals Inc., Merck & Co. Inc., Pfizer Inc. and Sanofi S.A., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)