Hemostasis and Tissue Sealing Agents Market Size, Share, Trends and Forecast by Product Type, Material Type, Application, End User, and Region, 2026-2034

Hemostasis and Tissue Sealing Agents Market Size and Share:

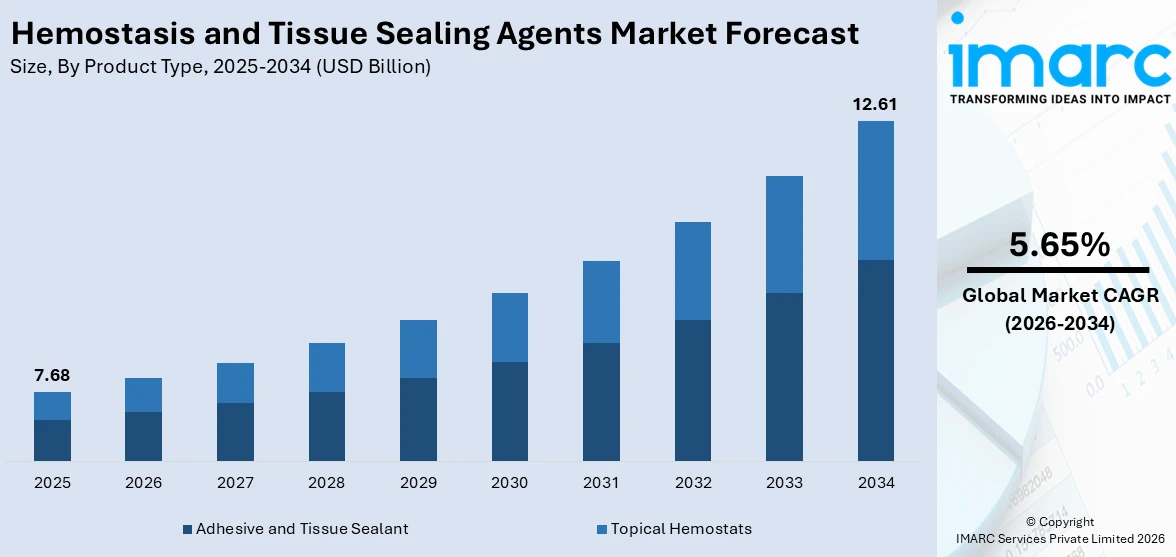

The global hemostasis and tissue sealing agents market size was valued at USD 7.68 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 12.61 Billion by 2034, exhibiting a CAGR of 5.65% from 2026-2034. North America currently dominates the market, holding a market share of 40% in 2025. The region benefits from well-established healthcare infrastructure, widespread adoption of advanced surgical technologies and hemostatic products, favorable reimbursement policies, and a high volume of surgical procedures driven by the rising prevalence of chronic diseases, all contributing to the hemostasis and tissue sealing agents market share.

The increasing number of surgical procedures being performed across the globe is one of the key drivers that are fueling the demand for hemostasis and tissue sealing agents. Cardiovascular, orthopedic, and general surgeries are increasingly adopting the use of effective hemostatic control and tissue sealing to ensure better patient outcomes and to prevent post-operative complications and blood loss. The increasing incidence of chronic diseases such as diabetes, cancer, and cardiovascular diseases is also contributing to the growing demand for surgical procedures that require the use of these specialized products. At the same time, the increasing adoption of minimally invasive surgical procedures is also influencing the demand for hemostats and tissue sealing agents. Additionally, the expanding geriatric population, which is more susceptible to chronic ailments and surgical complications, is supporting the hemostatic and tissue sealing agents market growth.

The United States has become a place for the market of things that help stop bleeding and seal tissues. The United States has a good healthcare system people are putting a lot of money into medical research and new developments and doctors are using the latest surgical tools. More people are getting sick with things like heart problems, diabetes and cancer so they need to have surgery. The doctors need to be able to stop the bleeding and seal the tissues well. As per information released by the CRT Group Foundation in August 2022, the count of people experiencing hypertension in the United States is expected to rise by 27.2%, reaching 162.5 million from 127.8 million between 2025 and 2060. In 2025, the American Heart Association (AHA) and the American College of Cardiology (ACC) established a specific goal for "healthy" blood pressure, below 130/80 mm Hg. Also, the United States has insurance plans that help pay for complicated illnesses, the population is getting older and more people want to have surgery that is not too invasive so the market for hemostasis and tissue sealing agents in the United States is growing rapidly.

To get more information on this market Request Sample

Hemostasis and Tissue Sealing Agents Market Trends:

Surging Demand for Minimally Invasive Surgeries

The way doctors do surgery is changing fast because they are using methods that do not cut the body as much. This is changing what doctors need to stop bleeding and fix tissues. When doctors do surgery with machines and tiny cuts they need special helpers that can be used in small spaces. These new ways of doing surgery are beneficial for patients because they hurt less after the surgery they can go home from the hospital sooner. These procedures offer significant patient benefits, including faster recovery times, which have driven their widespread acceptance among both clinicians and patients. The growing preference for these techniques is compelling manufacturers to develop advanced hemostatic products with superior applicability in minimally invasive settings. Moreover, continuous improvements in surgical instrumentation, high-definition imaging, and robotic systems are further expanding the scope of minimally invasive procedures across multiple specialties, sustaining demand for effective hemostatic solutions. In 2025, a novel, minimally invasive technique for addressing haemorrhoids, permitting patients to evade the discomfort of extensive surgery and quickly return to their usual routines, was introduced at a city hospital. The Rafaelo procedure, which involves radiofrequency ablation of hemorrhoids with local anesthesia, was developed in Poland and is being performed at Apollo Spectra.

Technological Advancements in Product Formulations

Technological innovations in hemostasis and tissue sealing agents are significantly enhancing product efficacy, safety, and ease of use, thereby propelling the hemostasis and tissue sealing agents market outlook. These new developments include the production of biomaterials, better delivery systems, and enhanced hemostatic aspects making sure they help blood clot and wounds heal better. Biodegradable and biocompatible agents can be broken down which helps with concerns about how well they work with the body and if they are safe to use. This means the body can slowly get rid of these materials over six to eight weeks without needing to take them out. For instance, in April 2025, Baxter International introduced the Hemopatch sealing hemostat with room-temperature storage in Europe, eliminating the need for refrigeration and offering a three-year shelf life. These innovations enhance surgical efficiency, minimize product wastage, and improve overall hemostatic performance during both open and minimally invasive procedures.

Rising Prevalence of Chronic Diseases Worldwide

The rising incidence of chronic diseases, such as cardiovascular diseases, cancer, and diabetes, is a major driver fueling the demand for hemostasis and tissue sealing agents, thus contributing to the hemostasis and tissue sealing agents market forecast. Chronic diseases often require surgical procedures for diagnosis, treatment, or management, thus ensuring a constant demand for efficient hemostatic and tissue sealing agents. Chronic wounds such as diabetic foot, pressure sores, and venous ulcers are frequent complications that often require surgical debridement, closure, or management, where these agents are crucial in ensuring hemostasis and facilitating faster healing. Furthermore, patients with chronic diseases often have comorbid conditions that raise the risk of surgical bleeding complications. For example, new national and state statistics released by the Partnership to Fight Chronic Disease (PFCD) indicate that chronic disease could result in costs of up to $47 trillion for the United States from 2024 to 2039, contributing $2.2 trillion annually in medical expenses and nearly $900 billion annually in lost productivity by 2039. The rising burden of diseases worldwide, driven by lifestyle changes, environmental conditions, and the growing elderly population, continues to create a vast market for hemostatic agents.

Hemostasis and Tissue Sealing Agents Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global hemostasis and tissue sealing agents market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type, material type, application, and end user.

Analysis by Product Type:

- Topical Hemostats

- Adhesive and Tissue Sealant

Adhesive and tissue sealant holds 54% of the market share. Adhesive and tissue sealant products encompass solutions designed to seal tissues, close wounds, or bond tissues together during surgical procedures. Available in liquid, gel, or film forms, these products are applied directly to the tissue surface, creating a biocompatible barrier that promotes wound healing and prevents leakage or further bleeding. The segment benefits from increasing preference for products that offer faster wound closure, reduced operating times, and lower post-operative infection risks compared to traditional suturing methods. The growing adoption of minimally invasive surgical procedures, where precise tissue sealing through small incisions is essential, is further amplifying demand for advanced sealant solutions. For instance, in November 2023, Ethicon, a part of Johnson and Johnson, gained European approval for its ETHIZIA hemostatic sealing patch, which provides effective results on both sides of the wound and stops bleeding in 30 seconds for 80% of patients.

Analysis by Material Type:

- Collagen-based

- Oxidized Regenerated Cellulose (ORC) based

- Gelatin-based

- Polysaccharide-based

- Others

Gelatin-based leads the market with a share of 33%. Gelatin-based hemostats are derived from collagen obtained from animal sources, predominantly bovine or porcine, and possess intrinsic hemostatic properties that are often enhanced through combination with thrombin or other clotting factors. These hemostats are available in various forms, including sponges, powders, and sheets, offering versatility across diverse surgical applications. The segment benefits from the material’s proven biocompatibility, cost-effectiveness, and ability to promote both platelet aggregation and wound healing simultaneously. Gelatin-based products are widely used across cardiovascular, orthopedic, and general surgical procedures to control bleeding and facilitate tissue repair. For instance, in 2025, GELITA, a producer of collagen and gelatin, has revealed the introduction of its Endotoxin Controlled Excipients (ECE) range. This product range, including VACCIPRO and MEDELLAPRO, satisfies the rigorous requirements of contemporary biomedical and pharmaceutical uses, such as vaccine stabilization, medical equipment, and 3D bioprinting. The growing demand for reliable and affordable hemostatic solutions in both developed and emerging healthcare systems continues to reinforce the segment’s leading position.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

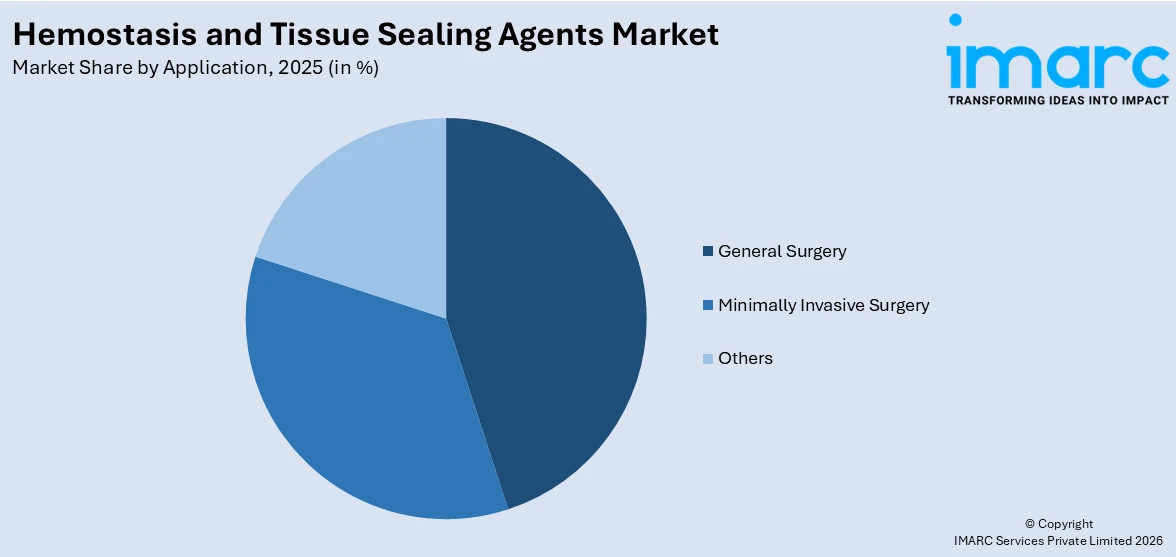

- General Surgery

- Minimally Invasive Surgery

- Others

General surgery dominates the market, with a share of 36%. General surgery encompasses a broad spectrum of surgical procedures involving various organs and tissues within the body, including appendectomies, hernia repairs, gallbladder removals, and bowel surgeries. Hemostasis and tissue sealing agents play a crucial role in these procedures by controlling bleeding from incisions, dissected tissues, and damaged vessels, thereby ensuring optimal surgical outcomes and patient recovery. The segment’s dominance is underpinned by the sheer volume of general surgical procedures performed annually across healthcare systems worldwide. As surgical complexity increases and patients present with more comorbidities, the need for effective hemostatic control during general surgical interventions continues to expand. For instance, according to the International Journal of Surgery, approximately 310 million major surgeries are carried out annually worldwide, with 40 to 50 million taking place in the United States. The growing emphasis on reducing post-operative complications and improving patient outcomes further supports the segment’s leading market position.

Analysis by End User:

- Hospitals

- Ambulatory Surgical Centers

- Home Care Settings

- Others

Hospitals represent the leading segment, with a market share of 56%. Hospitals serve as the primary settings for a wide range of medical interventions, including complex surgical procedures that require effective hemostasis and tissue sealing agents. These facilities encompass specialized departments such as operating rooms, emergency departments, and intensive care units where surgeries of varying complexity are performed. The segment’s dominance is attributable to the comprehensive resources available within hospital settings, including advanced surgical equipment, trained healthcare personnel, and integrated diagnostic and therapeutic services. Hospitals handle the highest volume of surgical procedures, particularly for chronic disease management, trauma care, and emergency interventions, all of which demand reliable hemostatic products. For instance, according to data published, hospitals held a major percentage share of the hemostasis products market in 2025, reflecting their pivotal role in driving demand. The ongoing expansion of hospital infrastructure globally further reinforces the segment’s leading market position in the hemostasis and tissue sealing agents market trends.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 40% of the share, enjoys the leading position in the market. The region’s dominance is primarily driven by well-established healthcare infrastructure, high adoption rates of innovative surgical technologies, and the presence of major market players who continuously invest in research and development. North America benefits from a high volume of surgical procedures, particularly for chronic diseases such as cardiovascular disorders, diabetes, and cancer, which create sustained demand for effective hemostatic and tissue sealing products. Favorable reimbursement policies and stringent regulatory standards further support market growth in the region. For instance, the United States minimally invasive surgery market was valued at USD 25.7 Billion in 2024 and is projected to reach USD 36.3 Billion by 2033, growing at a CAGR of 3.73% during 2025-2033, reflecting the strong demand for surgical products including hemostatic agents. Additionally, the well-established network of hospitals and ambulatory surgical centers ensures widespread availability and utilization of these products.

Key Regional Takeaways:

United States Hemostasis and Tissue Sealing Agents Market Analysis

The United States represents the largest national market for hemostasis and tissue sealing agents, driven by the country’s extensive healthcare infrastructure, high surgical volumes, and widespread adoption of advanced medical technologies. The rising prevalence of chronic conditions, including cardiovascular diseases, diabetes, and cancer, continues to generate substantial demand for surgical interventions requiring effective hemostatic control. The country’s aging population is particularly susceptible to conditions necessitating surgical procedures, further sustaining market demand. Additionally, the United States benefits from strong reimbursement frameworks that support the adoption of advanced hemostatic products across hospitals and ambulatory surgical centers. The growing preference for minimally invasive surgical techniques, including robotic-assisted procedures, is driving demand for hemostats and sealants specifically designed for use through small incisions. A survey commissioned by the Society of Interventional Radiology (SIR) and carried out by The Harris Poll uncovered notable insights regarding the treatment choices available to women diagnosed with uterine fibroids. The survey, involving more than 1,000 women in the USA, revealed that a considerable majority of women diagnosed with uterine fibroids were mainly offered hysterectomy as a treatment option (53%). Conversely, under 20% had knowledge of less invasive options like over-the-counter non-steroidal anti-inflammatory drugs (NSAIDs), uterine fibroid embolization (UFE), oral contraceptives, and endometrial ablation.

Europe Hemostasis and Tissue Sealing Agents Market Analysis

Europe represents a significant market for hemostasis and tissue sealing agents, supported by a well-developed healthcare system, strong regulatory frameworks, and favorable government-backed reimbursement policies that encourage the adoption of innovative surgical products. The region benefits from high adoption rates of advanced hemostatic solutions across cardiovascular, orthopedic, and general surgical procedures. Key markets including Germany, France, and the United Kingdom drive regional demand through their established hospital networks and ongoing investments in surgical technology. The implementation of the Medical Device Regulation has strengthened product quality standards, promoting the use of clinically validated hemostatic agents. For instance, in April 2025, Baxter International launched the Hemopatch sealing hemostat with room-temperature storage across European markets, eliminating refrigeration requirements and offering enhanced accessibility for surgical teams. Moreover, the growing geriatric population in Europe, coupled with increasing surgical volumes and rising prevalence of chronic diseases, continues to expand the addressable market for hemostatic and tissue sealing products across the region.

Asia-Pacific Hemostasis and Tissue Sealing Agents Market Analysis

Asia-Pacific is emerging as the fastest-growing regional market for hemostasis and tissue sealing agents, driven by rapid healthcare infrastructure expansion, rising surgical volumes, and increasing government investments in healthcare across major economies. Countries including China, Japan, India, South Korea, and Australia are witnessing significant improvements in medical facility capabilities, enabling greater adoption of advanced surgical technologies and hemostatic products. The rising prevalence of chronic diseases, expanding medical tourism, and growing awareness of advanced surgical techniques are further catalyzing regional market growth. For instance, in India, nearly 100 out of every 1 lakh people are diagnosed with cancer, underscoring the vast patient population requiring surgical intervention and hemostatic management. Additionally, favorable government policies aimed at improving healthcare access and increasing per capita healthcare expenditure continue to support market expansion across the region.

Latin America Hemostasis and Tissue Sealing Agents Market Analysis

Latin America presents growing opportunities for hemostasis and tissue sealing agents, supported by improving healthcare infrastructure, rising surgical volumes, and increasing economic development across the region. Brazil, Mexico, and Argentina represent key markets where expanding hospital networks and growing access to advanced surgical technologies are driving demand for hemostatic products. The increasing emphasis on modernizing healthcare systems and improving access to essential surgical services is creating new opportunities for market growth. For instance, the Brazilian government has allocated substantial funding toward expanding public healthcare infrastructure, supporting the growth of surgical services. The growing prevalence of chronic diseases and rising awareness of advanced surgical techniques further support market growth.

Middle East and Africa Hemostasis and Tissue Sealing Agents Market Analysis

The Middle East and Africa region offers emerging growth potential for hemostasis and tissue sealing agents, driven by ongoing healthcare infrastructure development, increasing government investments in medical facilities, and growing surgical volumes. The region is witnessing rising demand for advanced hemostatic products as healthcare systems expand to address the growing burden of chronic diseases and trauma cases. Moreover, governments are launching public robotic surgery facility, reflecting the broader trend of expanding advanced surgical capabilities across emerging markets. Improving healthcare access and increasing awareness of modern surgical techniques continue to support market development.

Competitive Landscape:

The hemostasis and tissue sealing agents market features a moderately consolidated competitive landscape, with several established multinational corporations holding significant market positions through extensive product portfolios, robust distribution networks, and continuous investments in research and development. Key players are actively pursuing strategies including product innovation, strategic acquisitions, geographic expansion, and collaborative partnerships to strengthen their competitive positioning. The market has witnessed notable merger and acquisition activity, with companies seeking to broaden their product offerings and enhance technological capabilities in hemostatic solutions. Additionally, companies are increasingly focusing on developing next-generation hemostatic agents with improved biocompatibility, faster clotting mechanisms, and enhanced storage stability to address evolving surgical requirements across diverse clinical settings worldwide.

The report provides a comprehensive analysis of the competitive landscape in the hemostasis and tissue sealing agents market with detailed profiles of all major companies, including:

- Advanced Medical Solutions Group plc

- Artivion, Inc

- B. Braun SE

- Baxter International Inc.

- Becton, Dickinson and Company

- BioCer Entwicklungs-GmbH

- Ethicon, Inc. (Johnson & Johnson)

- Medtronic

- Pfizer Inc.

- Terumo Aortic

Hemostasis and Tissue Sealing Agents Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Topical Hemostats, Adhesive and Tissue Sealant |

| Material Types Covered | Collagen-based, Oxidized Regenerated Cellulose (ORC) based, Gelatin-based, Polysaccharide-based, Others |

| Applications Covered | General Surgery, Minimally Invasive Surgery, Others |

| End Users Covered | Hospitals, Ambulatory Surgical Centers, Home Care Settings, Others |

| Regions Covered | Asia-Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Advanced Medical Solutions Group plc, Artivion, Inc, B. Braun SE, Baxter International Inc., Becton, Dickinson and Company, BioCer Entwicklungs-GmbH, Ethicon, Inc. (Johnson & Johnson), Medtronic, Pfizer Inc., Terumo Aortic, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the hemostasis and tissue sealing agents market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global hemostasis and tissue sealing agents market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the hemostasis and tissue sealing agents industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The hemostasis and tissue sealing agents market was valued at USD 7.68 Billion in 2025.

The hemostasis and tissue sealing agents market is projected to exhibit a CAGR of 5.65% during 2026-2034, reaching a value of USD 12.61 Billion by 2034.

The hemostasis and tissue sealing agents market is driven by the rising volume of surgical procedures globally, increasing prevalence of chronic diseases such as cardiovascular disorders and diabetes, growing adoption of minimally invasive surgical techniques, technological advancements in product formulations, and expanding geriatric population requiring surgical interventions.

North America currently dominates the hemostasis and tissue sealing agents market, accounting for a share of 40%. The region benefits from advanced healthcare infrastructure, high surgical volumes driven by rising chronic disease prevalence, widespread adoption of innovative hemostatic technologies, and favorable reimbursement policies.

Some of the major players in the hemostasis and tissue sealing agents market include Advanced Medical Solutions Group plc, Artivion, Inc, B. Braun SE, Baxter International Inc., Becton, Dickinson and Company, BioCer Entwicklungs-GmbH, Ethicon, Inc. (Johnson & Johnson), Medtronic, Pfizer Inc., Terumo Aortic, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)