Healthcare Payer Services Market Size, Share, Trends and Forecast by Type, Application, End Use, and Region, 2025-2033

Healthcare Payer Services Market Size and Share:

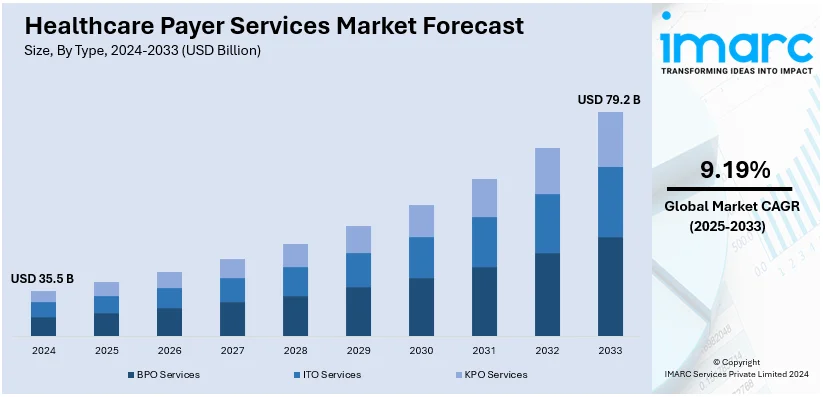

The global healthcare payer services market size reached USD 35.5 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 79.2 Billion by 2033, exhibiting a growth rate (CAGR) of 9.19% during 2025-2033. North America currently dominates the market holding a significant market share of over 74.9% in 2024. The changing healthcare regulations and compliance requirements, the increasing aging population, the growing importance of healthcare data security, and the rising patient demand for personalized and accessible healthcare experiences are favoring the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024 |

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 35.5 Billion |

| Market Forecast in 2033 | USD 79.2 Billion |

| Market Growth Rate (2025-2033) | 9.19% |

The global healthcare payer services market is driven by a growing demand for cost-effective healthcare delivery and enhanced operational efficiency among payers. Increasing healthcare costs are propelling the need for outsourcing non-core activities such as claims processing, member services, and analytics to reduce administrative burdens and improve service quality. Along with this, the adoption of advanced technologies, including artificial intelligence and data analytics, is further favoring market growth by enabling more accurate decision-making and streamlined processes. Rising emphasis on compliance with regulatory requirements and the need for scalable solutions to manage the growing volume of healthcare data also contribute to market expansion. Additionally, the shift toward value-based care models is driving payers to seek innovative service providers to achieve better outcomes.

The United States stands out as a key regional market, primarily driven by the rising prevalence of chronic diseases and an aging population, which increase the demand for efficient healthcare management. The push for improved patient experience and streamlined payer-provider communication has accelerated the adoption of outsourcing solutions. Growing focus on reducing fraud, waste, and abuse in healthcare expenditures is further promoting the use of advanced technologies, including automation and predictive analytics, in payer services. The transition to digital platforms for claims adjudication and enrollment services, combined with the push for interoperability in healthcare systems, is enhancing market growth. Additionally, government initiatives aimed at expanding healthcare access and improving affordability are encouraging payers to adopt innovative, cost-efficient service models.

Healthcare Payer Services Market Trends:

Increasing Implementation of Digital Technologies in Payer Operations

The increasing implementation of digital technologies in payer operations favors the market. As healthcare systems embrace digital transformation, payers must adopt cutting-edge technologies to remain competitive and efficient. The World Bank's commitment to increase digital health spending from 6% to 8% by 2030 underscores the increasing significance of digital health in global healthcare systems. Digital technologies, including artificial intelligence, machine learning, data analytics, and automation, are transforming payer operations. They enable streamlined claims processing, fraud detection, and data-driven decision-making. Payers are turning to specialized service providers to harness the full potential of these technologies, as these providers offer the expertise and infrastructure needed to navigate the complexities of digital integration effectively. Moreover, the COVID-19 pandemic has accelerated the need for digital solutions, especially in telehealth and remote patient management. Healthcare payer services providers are at the forefront of this transition, offering telehealth support, digital claims processing, and other innovative solutions to adapt to the rapidly changing healthcare landscape.

Rising Adoption of Analytics in Healthcare

The rising adoption of analytics in healthcare is fuelling the market growth. Analytics has become a linchpin in the healthcare industry, offering valuable insights that drive informed decision-making, cost reduction, and improved patient outcomes. These service providers leverage advanced analytics to help payers sift through massive volumes of data efficiently. This data encompasses claims, clinical records, patient histories, and more. By applying analytics, payers can identify trends, patterns, and anomalies that might go unnoticed. This not only aids in fraud detection and prevention but also enhances the overall operational efficiency of payers. Additionally, analytics plays a crucial role in population health management, enabling payers to address their members' health needs proactively. According to an industrial report, in 2023, the global big data market in healthcare was valued at USD 67 Billion and is projected to grow at a CAGR exceeding 19% throughout the forecast period of 2023-2035. Predictive analytics can forecast disease outbreaks, identify at-risk populations, and tailor interventions accordingly. In a healthcare landscape where data-driven decisions are paramount, the rising adoption of analytics acts as a catalyst for market expansion. Providers that offer expertise in healthcare analytics are in high demand, making this factor a key driver of market growth.

Escalating number of individuals opting for healthcare insurance

The escalating number of individuals opting for healthcare insurance is bolstering the market. According to World Economic Forum data, the healthcare insurance sector is anticipated to be strengthened by the 99.5% growth in chronic illnesses by 2050, which is reflected in the rise in people purchasing private health insurance (apart from what their jobs cover). Particularly in the UK, the number of insured people increased by an astounding 83% between 2021 and 2022, reaching 11.7 million. As healthcare awareness and the importance of financial protection against medical expenses continue to grow, more individuals seek insurance coverage. This trend substantially increases the volume of insurance claims, policy management, and member services, which puts pressure on healthcare payers. To cope with this rise, healthcare payers increasingly turn to specialized service providers to handle the influx efficiently. Healthcare payer services providers offer expertise in claims processing, member enrolment, and customer support, ensuring a seamless experience for policyholders. They play a crucial role in managing the administrative aspects of insurance, allowing payers to focus on providing quality healthcare services. The ever-expanding base of insured individuals, driven by regulatory changes and increased healthcare awareness, drives the market.

Healthcare Payer Services Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global healthcare payer services market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on type, application, and end use.

Analysis by Type:

- BPO Services

- ITO Services

- KPO Services

BPO services lead the market in 2024. BPO services within the healthcare payer domain encompass multiple critical functions essential for efficient operations. Healthcare payers can significantly reduce operational costs by outsourcing processes such as claims processing, enrollment, billing, and member services to specialized BPO providers. This cost-saving advantage is crucial in an industry where cost containment is paramount. Moreover, BPO services in healthcare payer operations offer scalability. Payers can quickly adjust their outsourcing requirements as the healthcare industry changes and adapts to regulations and market dynamics changes. BPO providers can readily scale up or down, ensuring flexibility and agility in response to the continually changing healthcare landscape.

BPO service providers have the expertise and technology infrastructure to streamline processes, reduce errors, and improve operational efficiency. This, in turn, leads to quicker claims processing, improved customer service, and enhanced member experiences. Furthermore, BPO services enable healthcare payers to focus on their core competencies – delivering quality healthcare services. Payers can redirect their resources and attention toward patient care, research, and innovation by outsourcing administrative and operational functions.

Analysis by Application:

- Analytics and Fraud Management Services

- Claims Management Services

- Integrated Front Office Service and Back Office Operations

- Member Management Services

- Provider Management Services

- Billing and Accounts Management Services

- HR Services

Claims management services lead the market with a market share of 33.8% in 2024. Claims management is a critical function in healthcare insurance, and outsourcing this process has numerous advantages that contribute to its market-driving role. These services streamline the complex and time-consuming process of handling insurance claims. Healthcare payers can offload the burden of managing a vast volume of claims, including data entry, verification, and processing, to specialized service providers. This results in quicker claims resolution, reduced errors, and improved customer satisfaction. Efficiency and accuracy are pivotal factors driving this segment's growth. Claims management service providers utilize advanced automation and data analytics technologies to optimize claims processing. This not only speeds up the reimbursement process but also helps in identifying potential fraud or errors, saving costs for payers.

Moreover, these services enhance cost control. Outsourcing claims management allows healthcare payers to achieve cost efficiencies, reduce administrative overhead, and allocate resources more effectively. This cost-effectiveness is particularly crucial in an industry grappling with rising healthcare expenses. Additionally, these services offer scalability. Healthcare payers can adjust their outsourcing requirements to match fluctuations in claims volume, ensuring flexibility and adaptability in response to market dynamics.

Analysis by End Use:

- Private Payers

- Public Payers

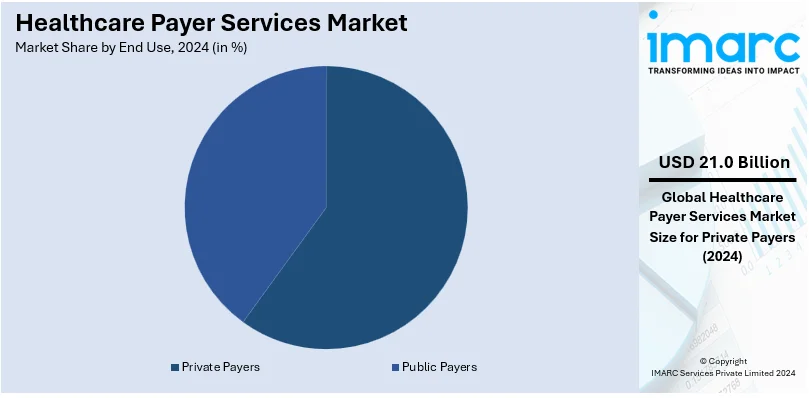

Private payers lead the market with a market share of 59.0% in 2024. Private payers, including insurance companies and employer-sponsored health plans, play a crucial role in the healthcare ecosystem, and their reliance on specialized services is a key factor shaping this market. They seek efficiency and cost containment. The complexity of managing private insurance claims, member enrolment, and customer service can get too cumbersome. Outsourcing such activities to health payer service providers brings a competitive advantage to private payers as their process gets streamlined and they save costs simultaneously. Moreover, they prioritize member satisfaction and retention. High-quality customer service and efficient claims processing are essential to retaining policyholders.

Healthcare payer services help private payers deliver exceptional member experiences, fostering loyalty and attracting new clients. Scalability is another driving factor. Private payers often experience fluctuations in their membership and claims volume. Healthcare payer service providers offer flexibility in scaling services up or down based on the changing needs of private payers, ensuring operational adaptability. The private payer sector's compliance and regulatory requirements are also complex and ever-changing. Specialized service providers in healthcare payer services are well-versed in these regulations, helping private payers stay compliant while avoiding potential legal pitfalls.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 74.9%. The North American region is a dominant growth driver in healthcare payer services. The region boasts a highly developed healthcare industry with a complex public and private payers network. The sheer size and diversity of the North American healthcare market create substantial demand for specialized payer services. Payers face the challenges of managing vast volumes of claims, adhering to stringent regulations, and meeting the changing needs of their members. Additionally, the United States, in particular, plays a pivotal role in driving market growth within North America. The U.S. healthcare system is complex, with a mix of private and public insurance programs. This complexity necessitates advanced payer services to efficiently manage claims, enrolment, and member services.

Moreover, the adoption of digital health solutions, electronic health records, and telemedicine is rapidly expanding. Healthcare payer services providers leverage these technologies to offer cutting-edge solutions, enhancing operational efficiency and member experiences. It is further driven by the commitment of this region towards security and compliance when it comes to data. As regulations such as HIPAA keep changing, payers in North America lean on the experience of service providers to navigate complex healthcare data management. This region will continue to dictate the growth trajectory in this industry over the next few years.

Key Regional Takeaways:

United States Healthcare Payer Services Market Analysis

The US market for healthcare payer services is being driven by the move towards value-based treatment, the growing complexity of healthcare systems, and the growing need for cost optimisation. With growing U.S. health care spending at 4.1 percent in 2022 reaching USD 4.5 Trillion or USD 13,493 per person, as per Centre for Medicare and Medicaid Services, to cut costs and enhance the efficiency of payers is shifting focus on outsourcing administrative as well as operational duties. As a result, more than 40% of outsourced payer services revolve around claims processing. Consequently, services such as provider network management, member services, and claims management have seen great demand.

The usage of modern technologies such as robotic process automation (RPA), machine learning (ML), and artificial intelligence (AI) continues to enhance industry growth due to the improvement of fraud detection and easy processes. For instance, in 2023, claims adjudication through AI-driven technologies increased speed and accuracy by 30%-50% and reduced errors by 30%-50%. Due to the growth of value-based payment models, which tie reimbursement to patient outcomes, payers are also investing in analytics and care management services. Due to government mandates such as the Health Insurance Portability and Accountability Act (HIPAA), payers are compelled to follow very stringent regulatory criteria, which is becoming more and more crucial for specialised services.

Europe Healthcare Payer Services Market Analysis

The market for healthcare payer services in Europe is driven by the region's focus on digital healthcare systems, regulatory compliance, and universal healthcare coverage. The industry is dominated by countries such as Germany, France, and the UK. The Netherlands accounted for more than 40% of the total European health claims in 2019, which is a growth of 4.4% compared to 2018, according to data by the European Insurance and Reinsurance Federation. The subsequent largest markets for health claims were Germany (+4.3%), Switzerland (+5.7%), and France (+7.5%). Payer services are in high demand due to the need for efficient analytics, fraud management, and claims processing.

The European Union's focus on eHealth and digital transformation through programs such as the European Health Data Space encourages payers to use cutting-edge IT systems for member management and data analytics. The major causes of death in circulatory disorders, which happen more than 1.7 million times annually, occur within the EU boundaries. Over 6 million individuals are afflicted with heart disorders; hence, the need for care management services that assist reduce costs and improve results is increasing. More to the point, this has to be done with the changing aging population that is growing. The ageing population across Europe currently makes up over 20% of people 65 years old and older as at 2023. Using specialized providers in doing all administrative work ensures efficiency and compliance with GDPR as well as other healthcare-specific legislation.

Asia Pacific Healthcare Payer Services Market Analysis

Expansion of health insurance coverage and digitization of healthcare systems are driving the rapid growth of the Asia-Pacific healthcare payer services market. Nations such as China, Japan, and India are at the forefront of this expansion. For instance, the Ayushman Bharat program in India is looking to insure more than 50 crore people, thereby resulting in a high demand for payer services. Effective claims management and analytics systems are needed due to the increase in chronic diseases and growing health care costs. China spent more than USD 49 Billion on health care in 2023, which shows the region's commitment to upgrading the health care infrastructure. The usage of telemedicine and mobile health solutions also increased the demand for member and care management services. Asia-Pacific places significant importance on technologically advanced healthcare solutions, which ensures payer services will continue to transform.

Latin America Healthcare Payer Services Market Analysis

The primary drivers of the Latin American healthcare payer services market are the need for low-cost administrative solutions and the increasing trend of health insurance programs. With coverage for more than 70% of the population, Brazil's Unified Health System (SUS) and Mexico lead the area. More people are also obtaining private insurance, which increases the demand for payer services such as fraud detection and claims processing. The region's health expenditure is growing at a CAGR of 3.2% during 2018-2050, according to the statistics by Inter-American Development Bank, which further supports the market. Governments and insurers are spending money on digital solutions to boost patient happiness and streamline operations. It is a more affordable approach to address the health concerns in the region by outsourcing payer services to specialized providers.

Middle East and Africa Healthcare Payer Services Market Analysis

According to an industrial report, the healthcare assiduity in the Middle East region is thriving. Driven by adding interest in preventative care approaches and a amenability to borrow new technologies, healthcare spending in the Gulf Cooperation Council (GCC) is anticipated to reach USD 135.5 Billion by 2027. Attempts at modernizing healthcare systems as well as increasing health insurance coverage are driving the MEA healthcare payer services market. Required health insurance plans in GCC countries, for instance, Saudi Arabia and United Arab Emirates, are driving demand for payer services. Initiatives toward digital transformation are boosting adoption of member services and claims management. To ensure operational efficiency and scalability, African insurers are increasingly being nudged to outsource payer services as part of initiatives for enhanced healthcare accessibility and reduced administrative inefficiencies.

Competitive Landscape:

Top companies are strengthening the market through a range of strategic initiatives and capabilities that resonate with the changing needs of the healthcare industry. These leading service providers invest heavily in cutting-edge technology. They harness the power of artificial intelligence, data analytics, and automation to streamline payer operations. This enhances efficiency and enables quicker claims processing, fraud detection, and improved decision-making. Furthermore, top players prioritize data security and compliance. They implement robust cybersecurity measures to safeguard sensitive patient information and ensure strict adherence to the ever-changing regulatory landscape, giving their clients peace of mind. Moreover, these industry leaders offer comprehensive solutions. They offer end-to-end services, such as claims management, member engagement, customer support, and data analytics, which enables payers to bring all their needs under one roof, thus reducing complexity. Moreover, the best vendors are agile and flexible. They can quickly respond to changes in the market, whether due to policy changes in healthcare or technological developments, so that their clients stay ahead of the game and well-equipped for the future.

The report provides a comprehensive analysis of the competitive landscape in the healthcare payer services market with detailed profiles of all major companies, including:

- Accenture plc

- Cognizant Technology Solutions Corporation

- Concentrix Corporation

- ExlService Holdings Inc.

- Genpact Limited

- HCL Technologies Limited

- Hinduja Global Solutions Limited

- HP Development Company L.P.

- McKesson Corporation

- UnitedHealth Group Incorporated

- Wipro Limited

- Xerox Corporation

Latest News and Developments:

- October 2024: The healthcare consulting company Consus Health was recently acquired by Accenture. Through the integration of Consus Health's value-based care and payer-provider cooperation skills, this move seeks to strengthen Accenture's strengths in healthcare payer services. The acquisition is in line with Accenture's plan to grow its healthcare consulting business and provide cutting-edge solutions to enhance patient outcomes and lower healthcare system expenses.

- September 2024: The healthcare revenue cycle management (RCM) division of Navient has been acquired by CorroHealth, completing a strategic portfolio expansion. With the goal of increasing healthcare providers' efficiency and compliance, this acquisition is expected to strengthen CorroHealth's capacity to offer complete RCM solutions, including coding, auditing, and financial management services.

- August 2023: Accenture plc acquired ATI Solutions Group (ATI), a Perth-based consulting service provider, to aid clients in Australia in automating field operations efficiently and quickly.

- August 2023: Cognizant announced that it is set to leverage Google Cloud's generative AI technology to develop innovative healthcare large language model (LLM) solutions. This initiative aims to harness the capabilities of generative AI in addressing various healthcare-related business challenges.

- March 2023: Concentrix Corporation, a prominent global provider of customer experience (CX) solutions and technologies, announced a strategic agreement to merge with Webhelp in a transaction valued at around USD 4.8 Billion, including net debt.

Healthcare Payer Services Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | BPO Services, ITO Services, KPO Services |

| Applications Covered | Analytics and Fraud Management Services, Claims Management Services, Integrated Front Office Service and Back Office Operations, Member Management Services, Provider Management Services, Billing and Accounts Management Services, HR Services |

| End Uses Covered | Private Payers, Public Payers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Accenture plc, Cognizant Technology Solutions Corporation, Concentrix Corporation, ExlService Holdings Inc., Genpact Limited, HCL Technologies Limited, Hinduja Global Solutions Limited, HP Development Company L.P., McKesson Corporation, UnitedHealth Group Incorporated, Wipro Limited, Xerox Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, healthcare payer services market forecast, and dynamics of the market from 2019-2033.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global healthcare payer services market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the healthcare payer services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The healthcare payer services market was valued at USD 35.5 Billion in 2024.

The healthcare payer services market is projected to exhibit a CAGR of 9.19% during 2025-2033, reaching a value of USD 79.2 Billion by 2033.

The market is driven by the increasing need for cost-effective healthcare delivery, the growing usage of advanced technologies such as artificial intelligence (AI) and analytics, an aging population, rising chronic disease prevalence, and a shift toward value-based care models.

North America currently dominates the healthcare payer services market, accounting for a share of 74.9% in 2024. The dominance is fueled by advanced healthcare systems, increasing healthcare expenditures, robust regulatory frameworks, and the growing adoption of outsourcing for administrative services.

.Some of the major players in the healthcare payer services market include Accenture plc, Cognizant Technology Solutions Corporation, Concentrix Corporation, ExlService Holdings Inc., Genpact Limited, HCL Technologies Limited, Hinduja Global Solutions Limited, HP Development Company L.P., McKesson Corporation, UnitedHealth Group Incorporated, Wipro Limited, and Xerox Corporation, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)