Halal Food Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region, 2026-2034

Global Halal Food Market Size, Share, Trends & Forecast (2026-2034)

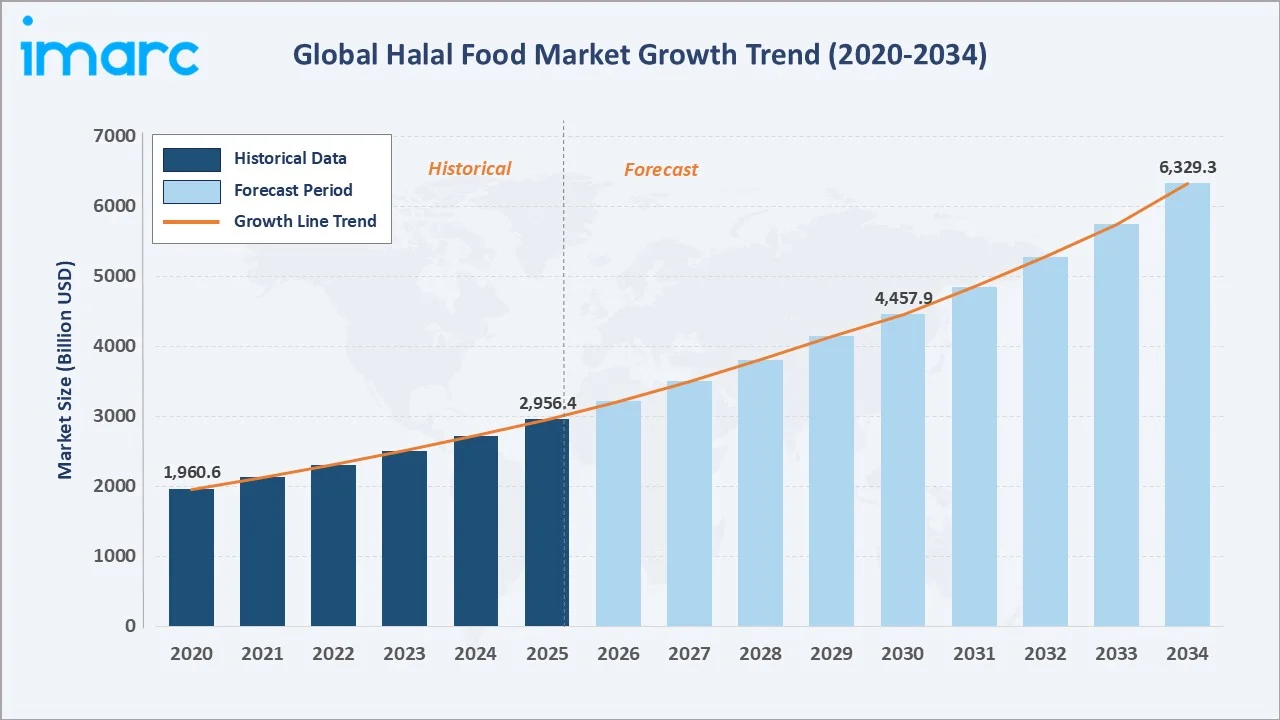

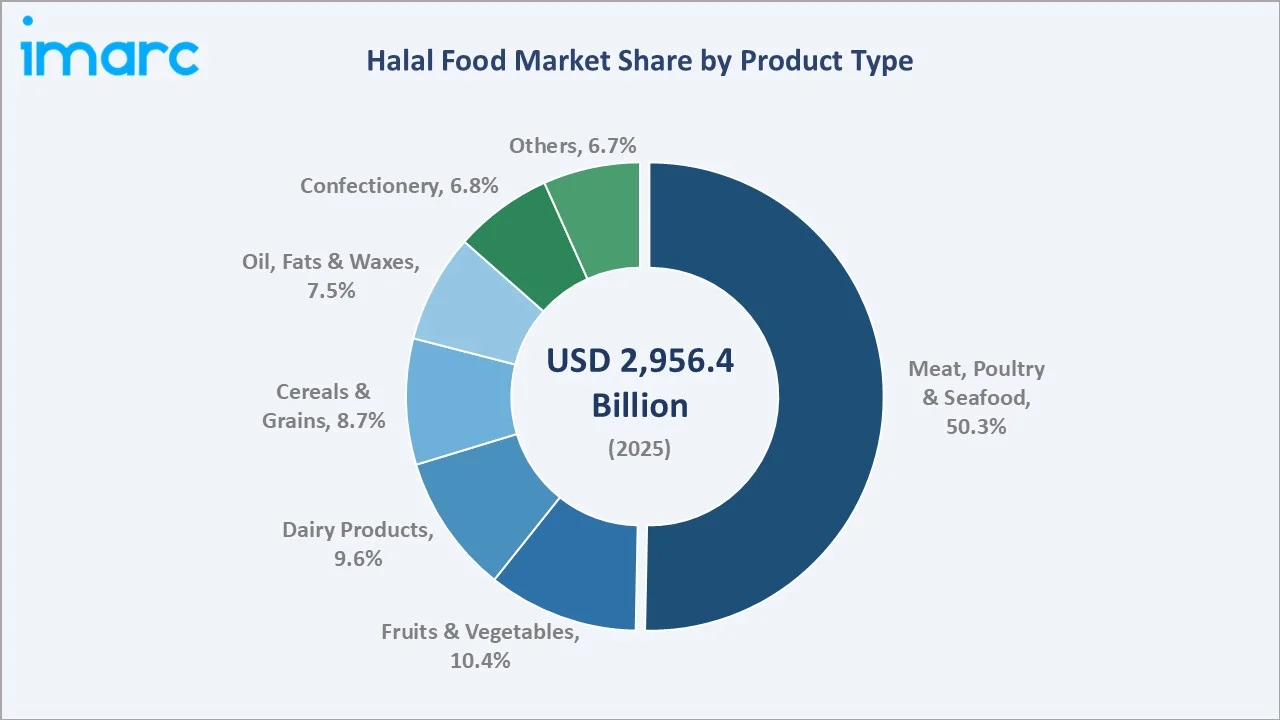

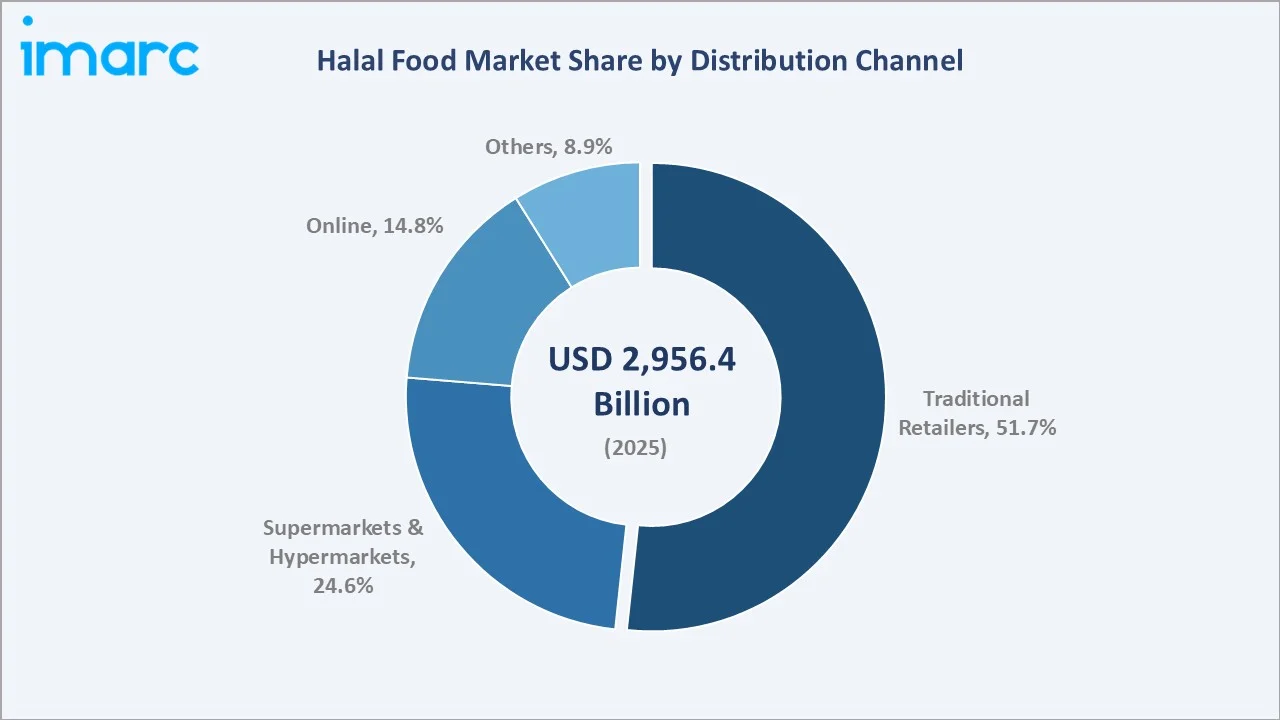

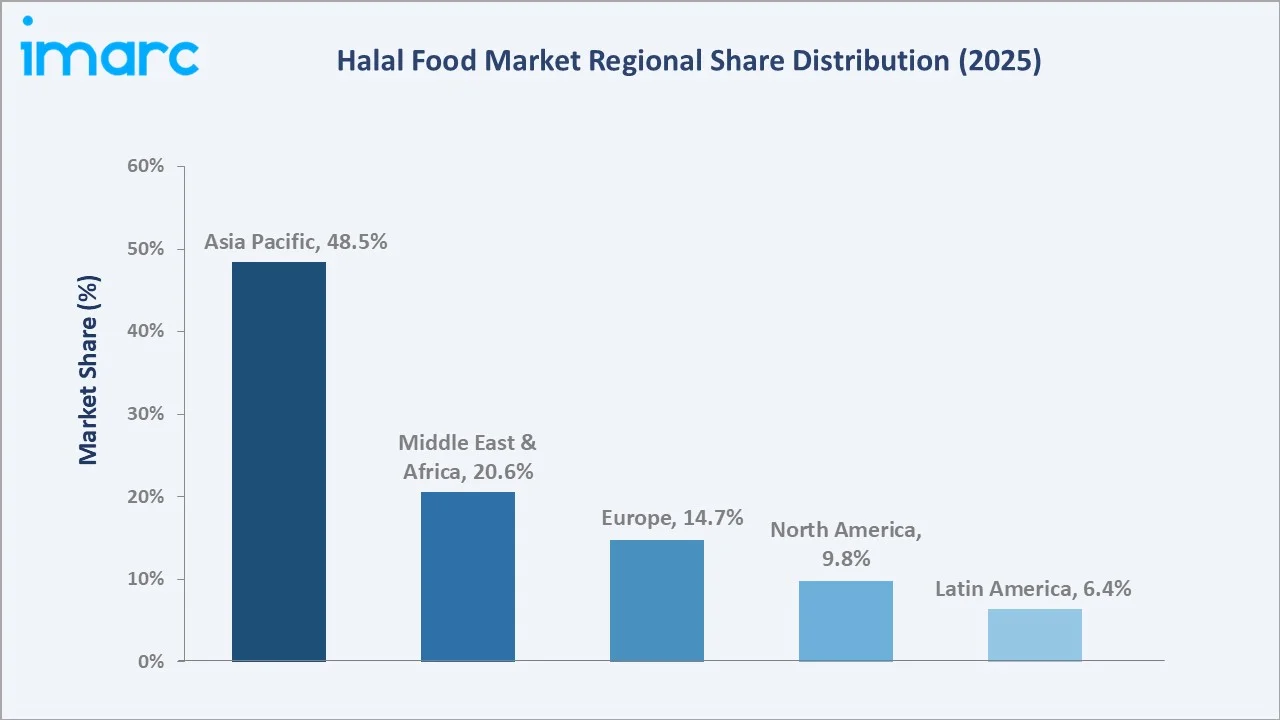

The global halal food market size was valued at USD 2,956.4 Billion in 2025 and is projected to reach USD 6,329.3 Billion by 2034, exhibiting a CAGR of 8.56% during the forecast period 2026-2034. Rising Muslim population, growing mainstream health and ethical consumption trends, expanding e-commerce channels, and increasingly harmonized halal certification frameworks are driving the halal food market growth. Meat, Poultry & Seafood leads product demand at 50.3% in 2025, while Traditional Retailers dominate distribution at 51.7%. Asia Pacific commands 48.5% global revenue share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2,956.4 Billion |

|

Forecast Market Size (2034) |

USD 6,329.3 Billion |

|

CAGR (2026-2034) |

8.56% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (48.5% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~9.2%) |

|

Leading Product Segment |

Meat, Poultry & Seafood (50.3%, 2025) |

|

Leading Distribution Channel |

Traditional Retailers (51.7%, 2025) |

The global halal food market growth trajectory from 2020 through 2034, illustrating historical expansion from USD 1,960.6 Billion in 2020 against a sustained forecast curve reaching USD 6,329.3 Billion by 2034 - powered by demographic growth, e-commerce expansion, and halal certification standardization across all major producing and consuming regions.

To get more information on this market, Request Sample

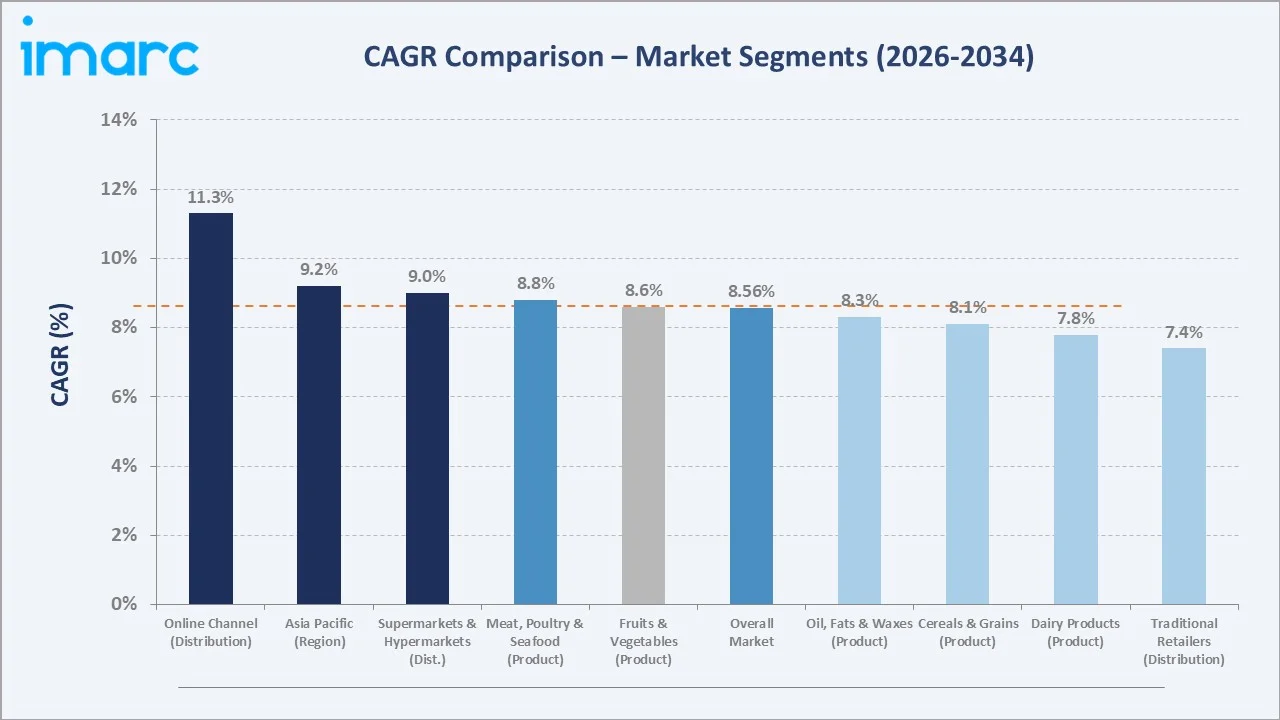

Segment-level CAGR comparisons highlighting online distribution channel adoption (11.3% CAGR) and Asia Pacific expansion (~9.2% CAGR) as the fastest-growing sub-categories within the global halal food market forecast through 2034.

Executive Summary

The global halal food market is undergoing sustained structural expansion. It is driven by rapid Muslim population growth, rising health and ethical consumption trends, and accelerating e-commerce adoption. Valued at USD 2,956.4 Billion in 2025, the market is forecast to reach USD 6,329.3 Billion by 2034 at a CAGR of 8.56%.

Meat, Poultry & Seafood commands 50.3% share in 2025, underpinned by Islamic dietary compliance requirements and global growth in certified protein trade. Traditional Retailers dominate distribution at 51.7%, though Online channels represent the fastest-growing distribution segment at an estimated CAGR of 11.3% through 2034, reflecting the convergence of global e-commerce expansion and dedicated halal marketplace proliferation.

Asia Pacific leads with 48.5% global revenue share in 2025, anchored by Indonesia's 231 million-strong Muslim population. Middle East & Africa follows at 20.6%, driven by OIC trade frameworks and mandatory halal certification in GCC markets. The halal food market outlook remains strongly positive as standard harmonization, digital retail penetration, and export-led growth strategies continue to reshape the competitive landscape through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Meat, Poultry & Seafood – 50.3% share (2025) |

|

Second Product Segment |

Fruits & Vegetables – 10.4% share (2025) |

|

Largest Distribution Channel |

Traditional Retailers – 51.7% share (2025) |

|

Fastest Growing Channel |

Online – ~11.3% CAGR (2026-2034) |

|

Leading Region |

Asia Pacific – 48.5% revenue share (2025) |

|

Top Companies |

Nestlé, MBRF, Al Islami Foods, Cargill, Tyson Foods |

|

Key Market Opportunity |

USD ~3.4 Trillion incremental value (2025-2034) |

Key Analytical Observations Supporting the Above Data:

- Meat, Poultry & Seafood's 50.3% dominance in 2025 is structurally non-cyclical, anchored in Islamic dietary law compliance requirements across 57 OIC member states — generating consistent certified protein procurement volumes irrespective of macroeconomic conditions.

- Fruits & Vegetables at 10.4% reflect growing urban demand for traceable, minimally processed, halal-certified produce — particularly in high-income GCC markets and rapidly urbanizing Southeast Asian cities.

- Traditional Retailers' 51.7% share is entrenched through proximity selling, community trust, and informal halal assurance prevalent in South and Southeast Asia, Sub-Saharan Africa, and the Middle East, where physical halal butchers and community stores remain primary access points.

- Online channel's 11.3% CAGR from 2026 to 2034 outpaces all other distribution channels, supported by IMARC Group's projection that global e-commerce will reach USD 183.8 Trillion by 2032 at a CAGR of 27.16%.

- Asia Pacific's 48.5% regional leadership is underpinned by Indonesia (244.41 million Muslims, 87.06% of population), Pakistan, Bangladesh, and Malaysia's globally recognized JAKIM certification infrastructure accepted in over 80 countries.

Global Halal Food Market Overview

Halal food refers to all food and beverages permissible under Islamic dietary laws, as defined by the Quran and Hadith. The global halal food industry encompasses a broad product ecosystem spanning meat and protein, packaged and processed food, dairy, beverages, confectionery, cereals, oils, and fresh produce. Products must comply with strict prohibitions against pork-derived ingredients, alcohol, improperly slaughtered animals, and specified harmful additives.

The industry operates at the convergence of religious compliance, food safety regulation, consumer health preferences, and global trade policy. Growth is supported by macroeconomic drivers including the world's expanding Muslim population, rising disposable incomes in Muslim-majority economies, and increasingly harmonized international certification standards advancing cross-border halal food industry access. Simultaneously, the market is experiencing a structural expansion of its addressable consumer base as mainstream health-conscious consumers in North America and Europe increasingly choose halal-certified products for their quality, ethical sourcing, and hygiene credentials.

Market Dynamics

To evaluate market opportunities, Request Sample

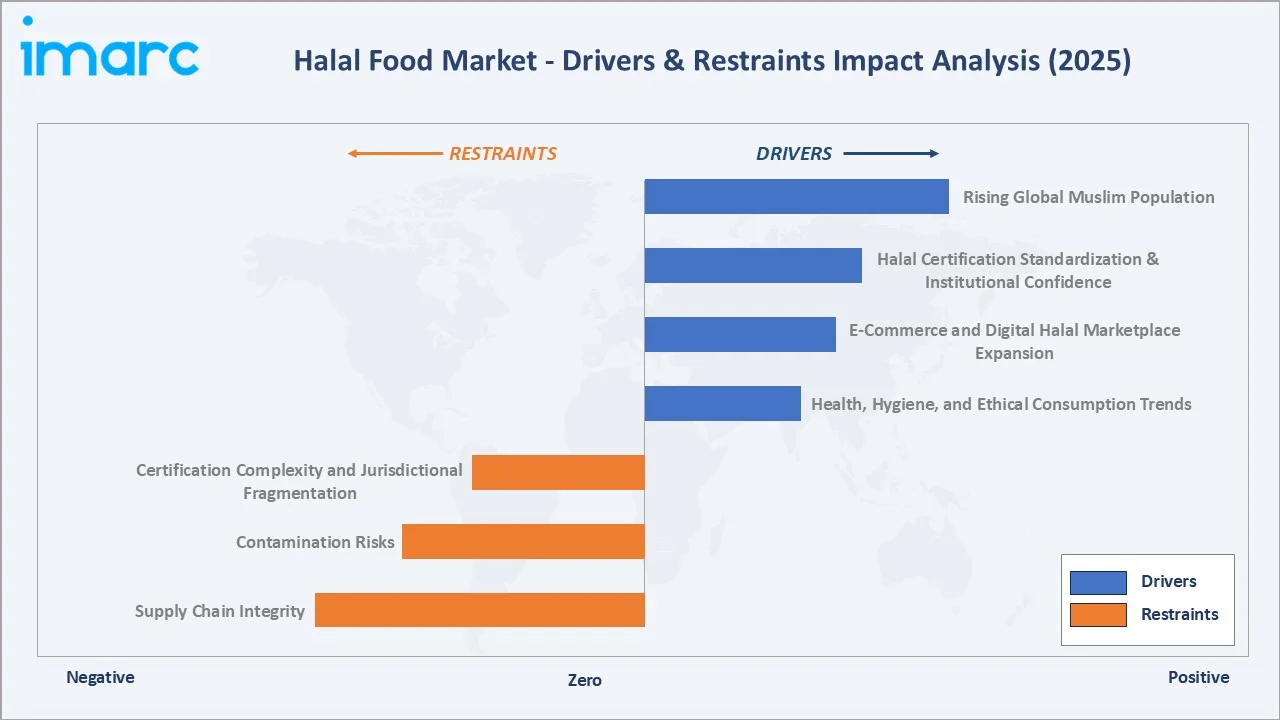

Market Drivers

- Rising Global Muslim Population: The world's Muslim population surpassed 2.0 billion in 2025, with Indonesia alone hosting 244.41 million Muslims — over 87.96% of its total population — generating the world's largest single-country halal food demand pool. Sustained demographic growth in Pakistan, Bangladesh, and Sub-Saharan Africa is creating structurally increasing demand for certified halal food products across all categories.

- Halal Certification Standardization & Institutional Confidence: Government-backed certification bodies including JAKIM (Malaysia), BPJPH (Indonesia), ESMA (UAE), and SASO (Saudi Arabia) are raising institutional credibility for certified products. Malaysia's JAKIM certification is now accepted in over 80 countries, significantly lowering trade barriers and strengthening consumer trust across both Muslim-majority and Muslim-minority markets.

- E-Commerce and Digital Halal Marketplace Expansion: Global e-commerce is projected to reach USD 183.8 Trillion by 2032 at a CAGR of 27.16%. Dedicated halal e-commerce platforms, certified product aggregators on mainstream marketplaces, and app-based halal grocery delivery services are dramatically expanding market access — especially in Muslim-minority markets with limited traditional halal retail infrastructure.

- Health, Hygiene, and Ethical Consumption Trends: Halal food certification is increasingly perceived as a premium quality and hygiene signal by non-Muslim consumers. Clean eating (16%), mindful eating (14%), and plant-based diet adoption (12%) trends identified in the IFIC 2022 Food and Health Survey closely align with halal production principles, meaningfully expanding the total addressable consumer base beyond the Muslim community.

Market Restraints

- Certification Complexity and Jurisdictional Fragmentation: The absence of a universally recognized global halal standard requires manufacturers to obtain multiple national certifications for different export markets. This creates significant compliance cost and operational complexity, particularly for multinational food companies managing diverse supply chains across regions with differing certification requirements.

- Supply Chain Integrity and Contamination Risks: Maintaining halal compliance across multi-tier supply chains — from raw material sourcing through processing, logistics, and retail — presents persistent documentation and contamination risks, especially in non-Muslim-majority countries with limited halal logistics infrastructure.

Market Opportunities

- Non-Muslim Health Consumer Segment: Growing alignment between halal food standards and mainstream health, ethical, and sustainability values creates significant incremental demand among Millennial and Gen Z consumers in North America and Europe — a segment that represents a high-value, fast-growing adjacent market for premium halal-positioned food brands.

- GCC and OIC Export Market Expansion: GCC nations collectively import over USD 40 Billion in food annually. Certified exporters in Brazil, Australia, India, and Southeast Asia have significant premium-margin export opportunities, supported by expanding bilateral halal trade agreements between OIC member states and major food-producing nations.

Market Challenges

- Halal Fraud and Mislabeling: Counterfeit halal labeling — involving uncertified products marketed as halal has increased in global halal food transactions annually. This undermines consumer trust and creates reputational risk for legitimate certified producers, particularly in emerging markets with weak regulatory enforcement infrastructure.

- Cold Chain Infrastructure Gaps: Maintaining halal-compliant temperature-controlled logistics in emerging markets — particularly Sub-Saharan Africa and parts of South Asia — limits market penetration for premium fresh and chilled certified products, restricting volume growth in high-potential frontier markets.

Emerging Market Trends

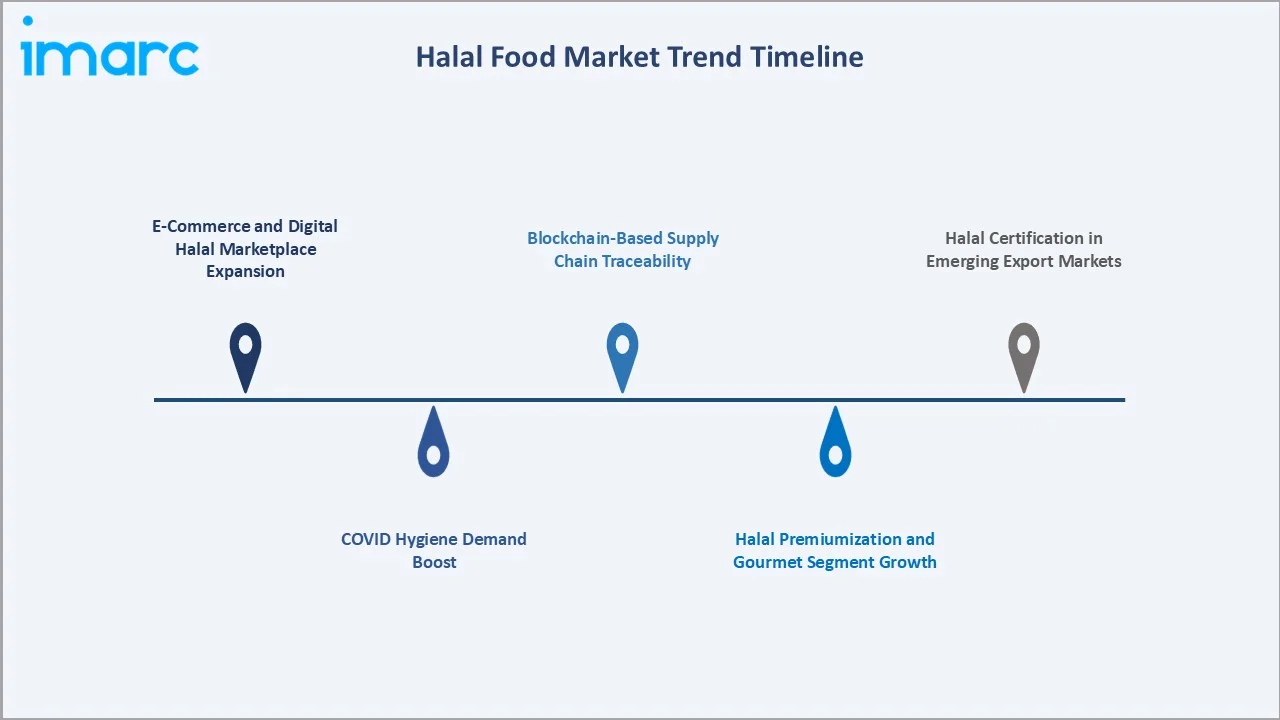

1. E-Commerce and Digital Halal Marketplace Expansion

Online platforms are emerging as the fastest-growing halal food distribution channel. Dedicated halal e-commerce portals, certified grocery delivery apps, and mainstream platform halal sections are expanding consumer access globally — particularly in urban Southeast Asia, the GCC, and Muslim-minority Western markets where traditional halal retail is dispersed.

2. Plant-Based Halal Product Innovation

The intersection of plant-based food innovation and halal compliance is generating significant market momentum. Plant-based proteins are inherently free of pork-derived ingredients, aligning naturally with halal requirements and lowering certification barriers. This convergence is attracting investment from both established halal food producers and plant-based food innovators targeting Muslim-majority markets across Southeast Asia and the Middle East.

3. Halal Premiumization and Gourmet Segment Growth

Consumer demand for premium halal food experiences is accelerating product innovation. Certified organic halal, halal-kosher dual-certified, and ethically raised halal protein products are commanding above-average price premiums. The gourmet halal segment — particularly in GCC and European markets — is growing exponentially CAGR through 2030, reshaping competitive positioning and margin profiles for established brands.

4. Blockchain-Based Supply Chain Traceability

Blockchain traceability platforms are gaining adoption among premium halal food producers. Distributed ledger systems provide immutable, timestamped documentation of halal compliance at each supply chain stage — directly addressing the fraud risk that undermines consumer confidence. This technology is increasingly becoming a competitive differentiator for premium brands targeting high-trust, high-margin export markets.

5. Halal Certification in Emerging Export Markets

Non-traditional halal food exporters including Brazil, India, Australia, and New Zealand are investing in halal certification to access the premium OIC import market. Brazil's BRF and JBS operate globally certified halal processing facilities. Brazil was the leading exporter of halal meat among nations, with a significant export value of USD 5.19 billion — ahead of other major exporters like Australia and India, the share that is projected to grow as bilateral trade agreements with OIC nations expand.

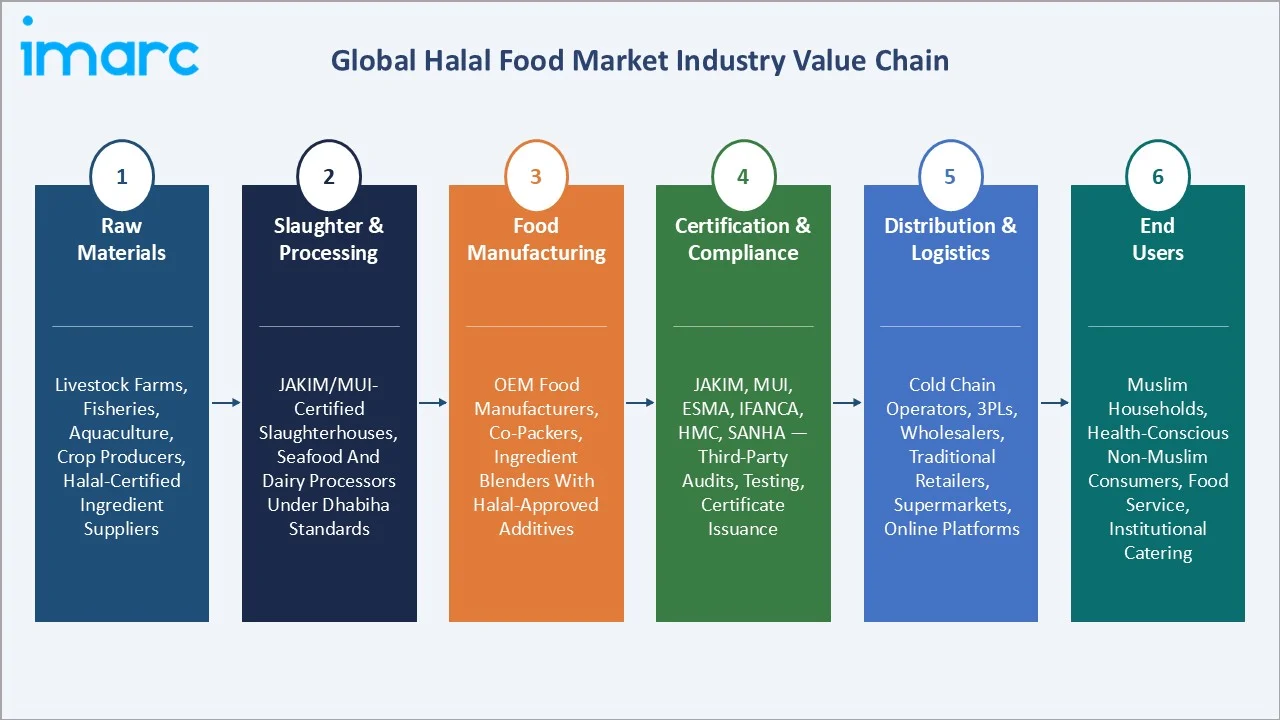

Industry Value Chain Analysis

The global halal food industry value chain spans six integrated stages from raw material supply through end-consumer delivery. Each stage is governed by halal compliance requirements that structurally differentiate it from conventional food supply chains, as every transition requires documented certification continuity to maintain product integrity. Each stage presents distinct competitive dynamics and technology investment priorities relevant to the overall halal food market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Livestock farms (cattle, poultry, lamb), fisheries, aquaculture, crop producers, halal-certified ingredient and additive suppliers |

|

Slaughter & Processing |

JAKIM/MUI-certified slaughterhouses, seafood processing plants, dairy processors — all governed by Dhabiha slaughter standards, Bismillah invocation, and blood drainage requirements |

|

Food Manufacturing |

OEM food manufacturers, co-packers, ingredient blenders — certified operations with no cross-contamination with haram substances, using halal-approved additives and certified equipment |

|

Certification & Compliance |

JAKIM (Malaysia), MUI (Indonesia), ESMA (UAE), IFANCA (USA), HMC (UK), SANHA (South Africa) — third-party audits, product testing, certificate issuance, and annual renewal |

|

Distribution & Logistics |

Cold chain operators, 3PLs, wholesalers, traditional retailers, supermarkets & hypermarkets, online platforms — segregated halal logistics, no co-mingling with non-halal goods |

|

End Users |

Muslim households, health-conscious non-Muslim consumers, food service operators, institutional catering, healthcare, and government procurement programs |

Certification bodies hold the highest strategic value in the halal food value chain, as their approval is the gateway to market access in OIC countries. Meanwhile, e-commerce and digital-direct channels are reshaping the distribution stage, enabling certified manufacturers to bypass intermediaries, reach consumers directly, and capture higher margins.

Technology Landscape in the Halal Food Industry

Digital Certification and Compliance Platforms

Digital certification management systems are replacing manual halal audit processes, reducing certification cycle times and enabling real-time compliance monitoring. Malaysia's HDC digital certification portal and UAE's ESMA e-certification system represent the leading examples of this institutional shift. These platforms are accelerating access and reducing certification costs for food manufacturers in high-volume export markets, while improving audit trail documentation quality.

Blockchain-Based Traceability

Blockchain traceability is emerging as the leading technology investment area for premium halal food producers. Distributed ledger platforms provide immutable, time-stamped documentation of halal compliance at each supply chain stage — from farm certification through logistics to retail point of sale. This technology directly addresses halal fraud risk, and is increasingly becoming a prerequisite for premium market access.

Advanced Food Testing and DNA Analysis

PCR (polymerase chain reaction) DNA testing and spectroscopy-based adulteration detection technologies are becoming standard in halal quality assurance laboratories. These methods detect pork-derived gelatin, lard, and alcohol contaminants at trace concentrations enabling manufacturers and certification bodies to maintain compliance integrity in complex multi-ingredient processed food products where manual inspection is insufficient.

IoT-Enabled Cold Chain and Smart Logistics

Internet of Things (IoT) sensor networks in cold chain logistics are improving the integrity of temperature-sensitive halal food products — particularly fresh meat, chilled dairy, and prepared meals. Smart containers with real-time temperature, humidity, and location tracking reduce spoilage, ensure regulatory compliance, and support the growing cross-border halal food trade corridors between Asia Pacific production hubs and GCC import markets.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the global halal food market, along with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been categorized based on product and distribution channel.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Meat, Poultry & Seafood | 50.3% | 2025 |

| Distribution Channel | Traditional Retailer | 51.7% | 2025 |

| Region | Asia Pacific | 48.5% | 2025 |

By Product

Meat, Poultry and Seafood leads the global halal food market with a 50.3% share in 2025. According to the report, Meat, Poultry and Seafood represented the largest segment. These food items are the most critical category within the halal ecosystem, governed by strict Islamic slaughter standards (Dhabiha) and certified inspection protocols. The rising global Muslim population, combined with growing demand for certified protein across Asia Pacific, the Middle East, and North Africa, sustains this segment's structural dominance.

To access detailed market analysis, Request Sample

Fruits & Vegetables account for 10.4% of the 2025 product mix, driven by rising demand for traceable, minimally processed, and pesticide-limited certified produce in urban Southeast Asia and the GCC. Dairy Products follow at 9.6%, with halal-certified milk powder, yogurt, and cheese seeing strong demand in South Asia and the Middle East. Cereals & Grains hold 8.7%, supported by staple food demand across Sub-Saharan Africa and South Asia. Oil, Fats & Waxes represent 7.5%, while Confectionery accounts for 6.8% a fast-growing sub-segment reflecting expanding demand for halal-certified gelatin-free confectionery in Europe and North America.

By Distribution Channel

Traditional Retailers dominate the global halal food distribution landscape with a 51.7% share in 2025. Informal halal butchers, neighbourhood grocery stores, and community markets remain the primary access point across South and Southeast Asia, Sub-Saharan Africa, and the Middle East — collectively representing the majority of the world's Muslim population. These channels benefit from proximity, community trust, and embedded informal halal assurance that formal retail cannot easily replicate.

Supermarkets & Hypermarkets account for 24.6% of distribution, reflecting growing mainstream retail integration of dedicated halal food sections across Asia Pacific and Europe. Online channels hold 14.8% in 2025 and are the fastest-growing distribution segment, advancing at approximately 11.3% CAGR through 2034. The Others segment (8.9%) includes food service, institutional catering, and specialty halal stores.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

48.5% |

Indonesia 244M Muslims; Malaysia JAKIM certification hub; South and Southeast Asia demographic growth; expanding modern halal retail |

|

Middle East & Africa |

20.6% |

Mandatory GCC halal certification (ESMA, SASO, GSO); OIC bilateral trade frameworks; high per-capita halal food spend in Saudi Arabia, UAE, Kuwait |

|

Europe |

14.7% |

Muslim diaspora 80M; mainstream health-driven adoption in UK, France, Germany; premium gourmet halal segment growth; EU food labeling regulation |

|

North America |

9.8% |

US Muslim population growth (724K in New York, 504K in California); QSR halal certification expansion; IFANCA certification widely recognized in OIC markets |

|

Latin America |

6.4% |

Brazil & Argentina as major halal protein exporters; OIC export certification investment; growing domestic Muslim community awareness |

Asia Pacific commands 48.5% global revenue share in 2025. Indonesia is the single most important national market, hosting over 244 million Muslims (87.06% of population). Malaysia is the global benchmark for halal certification infrastructure, with JAKIM certifications accepted in over 80 countries. Asia Pacific is also forecast to be the fastest-growing region, advancing at approximately 9.2% CAGR through 2034, driven by urbanization, rising middle-class incomes, and rapidly expanding formal halal retail infrastructure.

Middle East & Africa holds 20.6%, underpinned by GCC nations' high per-capita halal food expenditure and mandatory certification frameworks. Saudi Arabia, UAE, and Kuwait are the highest-value import markets within this region. Sub-Saharan Africa represents the highest-potential growth frontier with an estimated 500 million Muslims and rapidly developing urban food retail infrastructure.

Europe at 14.7% reflects a dual-driver market: a Muslim diaspora population of over 26 million and growing mainstream adoption among health-conscious non-Muslim consumers in the UK, France, and Germany. North America's 9.8% is supported by QSR halal certification expansion and rising Muslim-community-driven demand across major US cities. Latin America accounts for 6.4%, led by Brazil and Argentina as major halal protein exporters leveraging OIC trade partnerships.

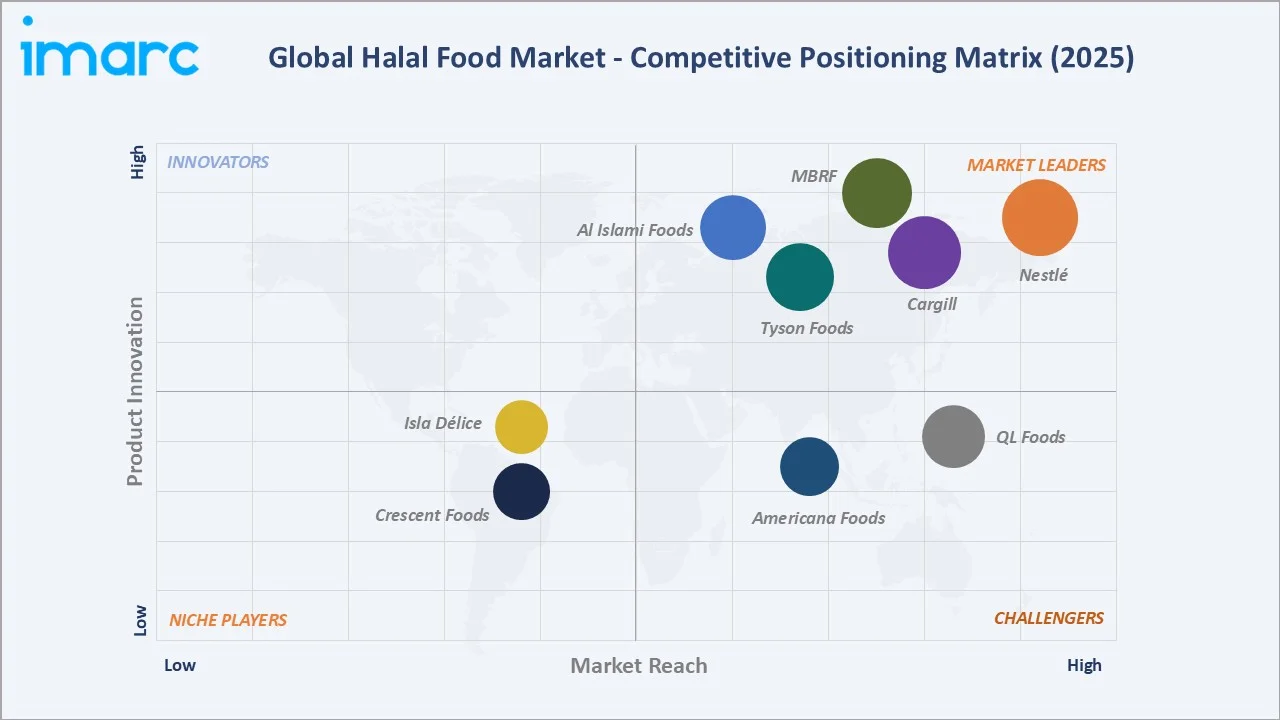

Competitive Landscape

|

Company Name |

Key Halal Brand |

Market Position |

Core Strength |

|

Nestlé |

Buitoni, Maggi |

Leader |

World's largest halal food portfolio; certified in 60+ countries; strong Asia Pacific and MENA presence |

|

MBRF |

Sadia Halal, Perdigao |

Leader |

Brazil's largest halal meat exporter; certified to 100+ countries; dominant GCC and Southeast Asia presence |

|

Cargill |

Adrogel, Leanardo |

Leader |

Integrated halal supply chain from feed to packaged meat; strong North America and European reach |

|

Tyson Foods |

Tyson |

Leader |

Leading halal poultry in North America; USDA-certified; growing OIC export capacity |

|

Al Islami Foods |

Al Islami |

Leader |

UAE-based dedicated halal brand; dominant across GCC; frozen halal meals, poultry, and seafood |

|

QL Foods |

OceanRia, Figo |

Challenger |

Malaysia-based; strong Southeast Asia footprint; integrated halal poultry and aquaculture |

|

Americana Foods |

KFC, Krispy Kreme |

Challenger |

GCC foodservice and retail leader; KFC, Pizza Hut halal franchise operator across 13+ countries |

|

Isla Délice |

Isla Délice |

Niche |

France-based European halal leader; fast-growing in UK, Germany; premium halal deli and meat |

|

Crescent Foods |

Crescent Foods |

Niche |

US-focused antibiotic-free halal poultry; premium positioning aligned with health consumer trends |

The global halal food market's competitive landscape is moderately fragmented, with global food conglomerates competing alongside dedicated halal producers, regional processors, and a large base of local certified suppliers. Leading players compete on certification breadth, production scale, cold chain logistics capability, and brand equity. Strategic acquisitions are a key competitive tool — MBRF has been consistently expanding its halal-certified processing capacity in Brazil to serve growing GCC and Southeast Asian import demand.

Key Company Profiles

Nestlé S.A.

Nestlé S.A. is the world's largest food and beverage company, headquartered in Vevey, Switzerland. With operations in over 188 countries and annual revenues exceeding CHF 89.5 Billion in 2025, Nestlé is also the single largest global producer of halal-certified food products across multiple categories.

- Product & Platform Portfolio: Nestlé's halal portfolio spans Maggi noodles and seasonings, Milo fortified beverages, KitKat (halal-certified variants), Coffee-Mate, Nestlé dairy products, and infant nutrition — all manufactured under halal-certified production standards in Malaysia, Indonesia, UAE, and Turkey.

- Recent Developments: In 2024, Nestlé Malaysia expanded its JAKIM-certified halal production facilities, reinforcing its benchmark position as the world's largest halal food manufacturer. Nestlé's halal business is estimated to represent over 15% of its total global revenue.

- Strategic Focus: Nestlé's halal strategy centres on leveraging its global R&D, supply chain scale, and brand trust to deepen penetration in OIC markets while capturing growth in mainstream Western markets through health-positioned certified products.

MBRF

MBRF is Brazil's largest food company and one of the world's leading halal protein exporters. Headquartered in Itajaí, Brazil, MBRF's Sadia and Perdix brands are distributed across over 100 countries, with the Middle East, Southeast Asia, and Central Asia as its primary halal export destinations.

- Product & Platform Portfolio: MBRF's halal product range includes certified frozen poultry (Sadia), processed halal meat products, marinated chicken portions, and ready-to-cook halal meal kits targeting GCC retail and foodservice markets.

- Recent Developments: In 2023-2024, MBRF expanded its halal-certified production capacity in Brazil to serve growing demand from Saudi Arabia, UAE, and Malaysia, supported by Brazil's bilateral halal trade agreements with OIC member states.

- Strategic Focus: MBRF focuses on vertically integrated halal supply chain excellence — from certified Brazilian farms through certified slaughter and processing, to direct import relationships with GCC retail chains and foodservice operators.

Al Islami Foods

Al Islami Foods is a dedicated halal food company headquartered in Dubai, UAE. As one of the GCC's most recognized halal brands, Al Islami Foods specializes in frozen halal meat, poultry, seafood, and ready-to-eat products for the Middle East retail and foodservice market.

- Product & Platform Portfolio: Al Islami's product range includes frozen halal chicken, beef and lamb cuts, seafood, burgers, sausages, nuggets, and a growing line of marinated and value-added halal protein products — all certified under ESMA and UAE Food Safety Authority standards.

- Recent Developments: Al Islami Foods has invested in expanding its production facilities and cold chain distribution network across the GCC to accommodate growing demand from institutional foodservice clients and modern trade retail chains across the region.

- Strategic Focus: Al Islami's strategy focuses on deepening GCC market penetration through product innovation in convenience and value-added halal categories, while expanding export relationships with emerging halal markets in Europe and Southeast Asia.

Market Concentration Analysis

The global halal food market was valued in the trillions USD range in 2025 and is projected to grow significantly by 2034, with major players including Nestlé, Cargill, BRF S.A., Tyson Foods, and Al Islami Foods. The remaining market share is distributed across a large base of regional certified producers, national brands, and informal halal food operators across Muslim-majority markets.

The market is experiencing a bifurcated competitive dynamic. At the premium OEM and global brand tier, consolidation is accelerating around certification breadth, digital distribution capability, and sustainability credentials. Simultaneously, regional producers in Indonesia, Malaysia, Pakistan, and Egypt are generating competitive challengers that are increasingly targeting export markets with cost-competitive, domestically certified products.

This dual dynamic — global consolidation at the premium end and high fragmentation at the volume end — will persist through 2034. Consolidation pressure is most acute in the GCC institutional and food service segment, where large-scale certified suppliers are displacing smaller importers. In the online channel, platform-led aggregation of certified small producers is simultaneously enabling fragmentation to persist across the long tail of the market.

Investment & Growth Opportunities

Fastest-Growing Segments

Online distribution is the highest-growth channel at approximately 11.3% CAGR through 2034. Confectionery is the fastest-growing product sub-segment in absolute incremental value terms, expanding at an estimated CAGR of 9.5% through 2034 as halal-certified alternatives to gelatin-based products gain mainstream distribution. Asia Pacific is the fastest-growing region at approximately 9.2% CAGR through 2034.

Emerging Market Expansion

Sub-Saharan Africa represents the highest-potential frontier market for halal food investment. An estimated 500 million Muslims, rapidly urbanizing populations, and underdeveloped formal halal retail infrastructure collectively create a greenfield expansion opportunity for certified food producers with local distribution capabilities. Bangladesh and Pakistan represent additional high-volume, underserved domestic markets where formal halal retail infrastructure is expanding rapidly.

Venture and Strategic Investment Trends

Strategic investments are flowing toward blockchain-based halal traceability platforms, digital certification management systems, and halal e-commerce infrastructure. GCC sovereign wealth funds are allocating capital to halal food supply chain infrastructure investments across Southeast Asia and Sub-Saharan Africa as part of food security diversification strategies. Corporate M&A activity is focused on acquiring regionally certified producers with established distribution networks in high-growth OIC markets.

Future Market Outlook (2026-2034)

The global halal food market forecast projects sustained value expansion from USD 2,956.4 Billion in 2025 to USD 6,329.3 Billion by 2034 at a CAGR of 8.56%. An interim milestone of USD 4,457.9 Billion is projected for 2030, representing approximately USD 1.5 Trillion in incremental market value in the first five years of the forecast period alone.

Asia Pacific will retain and strengthen its regional leadership through 2034, supported by Indonesia's and Pakistan's demographic growth, Malaysia's halal export infrastructure investment, and the rapid formalization of halal retail across Bangladesh, India, and Southeast Asian urban markets. The Middle East & Africa region will sustain above-average growth as GCC certification frameworks become increasingly harmonized with international standards.

Three key shifts will reshape the global halal food market through 2034. Digital traceability will become a baseline market access requirement for premium halal brands in high-value export markets. E-commerce convergence will enable certified small and mid-size producers to access global Muslim consumer markets directly, disrupting traditional distributor-led trade flows. And mainstream health positioning will progressively expand the total addressable market beyond the Muslim consumer base, as halal food's alignment with organic, ethical, and sustainable production principles deepens its appeal among global health-conscious consumers.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with halal food industry stakeholders — including production directors at OEM food manufacturers, halal certification body officials (JAKIM, MUI, ESMA, IFANCA), procurement managers at GCC retail chains, and institutional food service operators. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines across all major regions.

Secondary Research

Secondary sources include OIC trade statistics, national statistical agencies, halal certification body databases, World Population Review demographic data, IMARC Group global e-commerce projections, trade publications (Halal Focus, Salaam Gateway, Halal Journal), company annual reports of listed halal food producers, and regulatory frameworks from JAKIM, GSO, SASO, and ESMA. Historical market data spans 2020-2025, providing a robust baseline for forecast calibration.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up and top-down forecasting models. The bottom-up model aggregates segment-level demand projections across product categories, distribution channels, and regional markets. The top-down model benchmarks projections against macroeconomic indicators including Muslim population growth rates, disposable income trends, and halal trade flow data. Both models are reconciled and validated to produce the final market forecast.

Halal Food Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Meat, Poultry and Seafood, Fruits and Vegetables, Dairy Products, Cereals and Grains, Oil, Fats, and Waxes, Confectionery, Others |

| Distribution Channels Covered | Traditional Retailers, Supermarkets and Hypermarkets, Online, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Nestlé, MBRF, Cargill, Tyson Foods, Al Islami Foods, QL Foods, Americana Foods, Isla Délice, Crescent Foods, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the halal food market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global halal food market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the halal food industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Halal Food Market Report

The global halal food market was valued at USD 2,956.4 Billion in 2025, driven by rising Muslim population, expanding e-commerce adoption, and growing mainstream health consumer interest in certified food products globally.

The market is projected to reach USD 6,329.3 Billion by 2034, growing at a CAGR of 8.56% during 2026-2034, supported by demographic expansion, digital retail penetration, and international certification harmonization.

Meat, Poultry & Seafood leads with a 50.3% share in 2025, driven by Islamic dietary compliance requirements, global certified protein trade growth, and rising consumer demand for halal-certified animal protein products.

Online is the fastest-growing distribution channel, advancing at approximately 11.3% CAGR from 2026 to 2034, driven by global e-commerce expansion and the proliferation of dedicated halal marketplace platforms.

Asia Pacific dominates with a 48.5% share in 2025. Indonesia's 231 million Muslims, Malaysia's JAKIM certification leadership, and rapid urban retail formalization across Southeast Asia underpin its dominant position.

Key drivers include a rising global Muslim population exceeding 2.0 billion, expanding halal certification standards, growing mainstream health consumer adoption, e-commerce channel growth, and OIC trade integration frameworks.

Major players include Nestlé S.A., MBRF, Cargill Inc., Tyson Foods, Al Islami Foods, QL Foods, Americana Foods, Isla Délice, and Crescent Foods — spanning global conglomerates and dedicated regional halal specialists.

Key challenges include lack of universal certification harmonization across jurisdictions, supply chain integrity and contamination risks, halal fraud and mislabeling issues, and cold chain infrastructure gaps in frontier markets.

The global halal food market is projected to reach USD 4,457.9 Billion by 2030 — representing approximately USD 1.5 Trillion in incremental market value added over the 2025 base, at a sustained 8.56% annual growth rate.

Key emerging trends include e-commerce halal marketplace expansion, plant-based halal product innovation, blockchain supply chain traceability, halal premiumization in Western markets, and growing export certification investment from Brazil, India, and Australia.

Asia Pacific is the fastest-growing region, advancing at approximately 9.2% CAGR through 2034, driven by Indonesia's Muslim population growth, Malaysia's certification infrastructure, and rapidly expanding urban halal retail markets.

The market is segmented by Product (Meat, Poultry & Seafood; Fruits & Vegetables; Dairy Products; Cereals & Grains; Oil, Fats & Waxes; Confectionery; Others) and Distribution Channel (Traditional Retailers; Supermarkets & Hypermarkets; Online; Others), with country-level analysis available on a customized basis.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)