Green Cement Market Size, Share, Trends and Forecast by Product Type, End-Use Industry, and Region, 2026-2034

Global Green Cement Market Size, Share, Trends & Forecast (2026-2034)

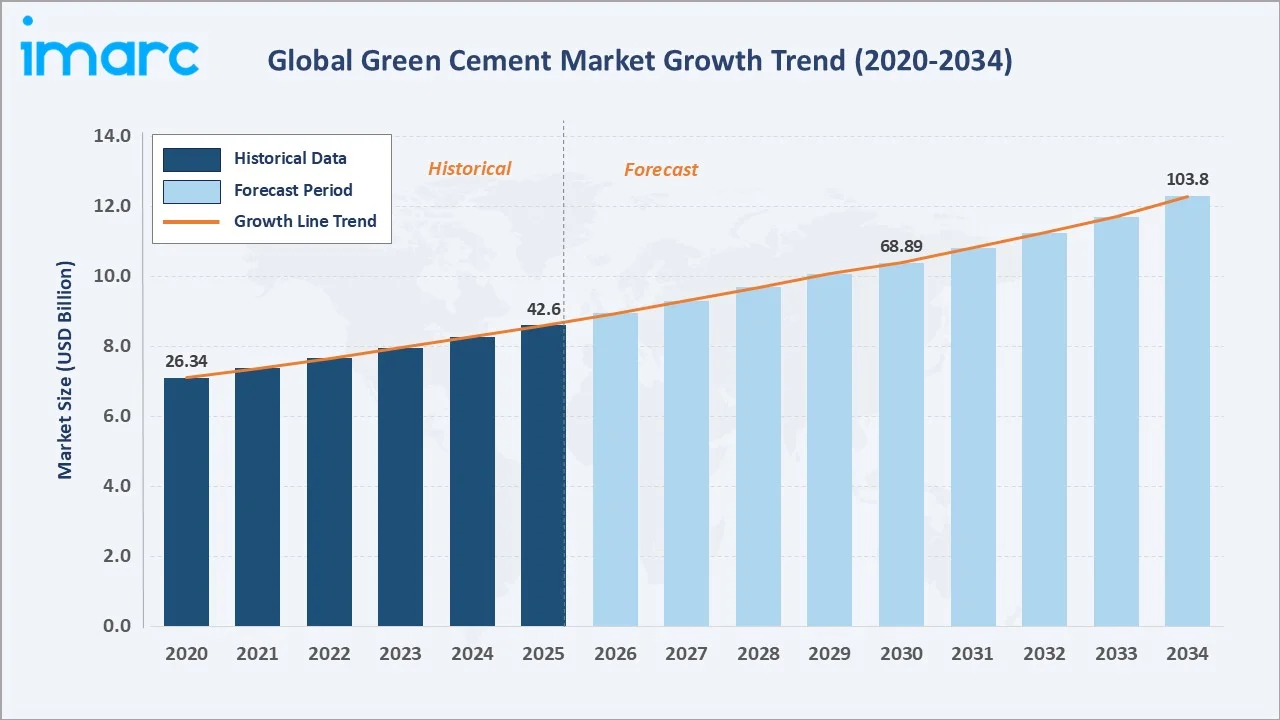

The global green cement market was valued at USD 42.6 Billion in 2025 and is projected to reach USD 103.8 Billion by 2034, expanding at a CAGR of 10.09% during the the forecast period 2026-2034. The green cement market growth is propelled by tightening carbon-emission regulations, widespread adoption of supplementary cementitious materials (SCMs) such as fly ash and slag, and surging demand for sustainable construction.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 42.6 Billion |

|

Forecast Market Size (2034) |

USD 103.8 Billion |

|

CAGR (2026-2034) |

10.09% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.6% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~12.5%) |

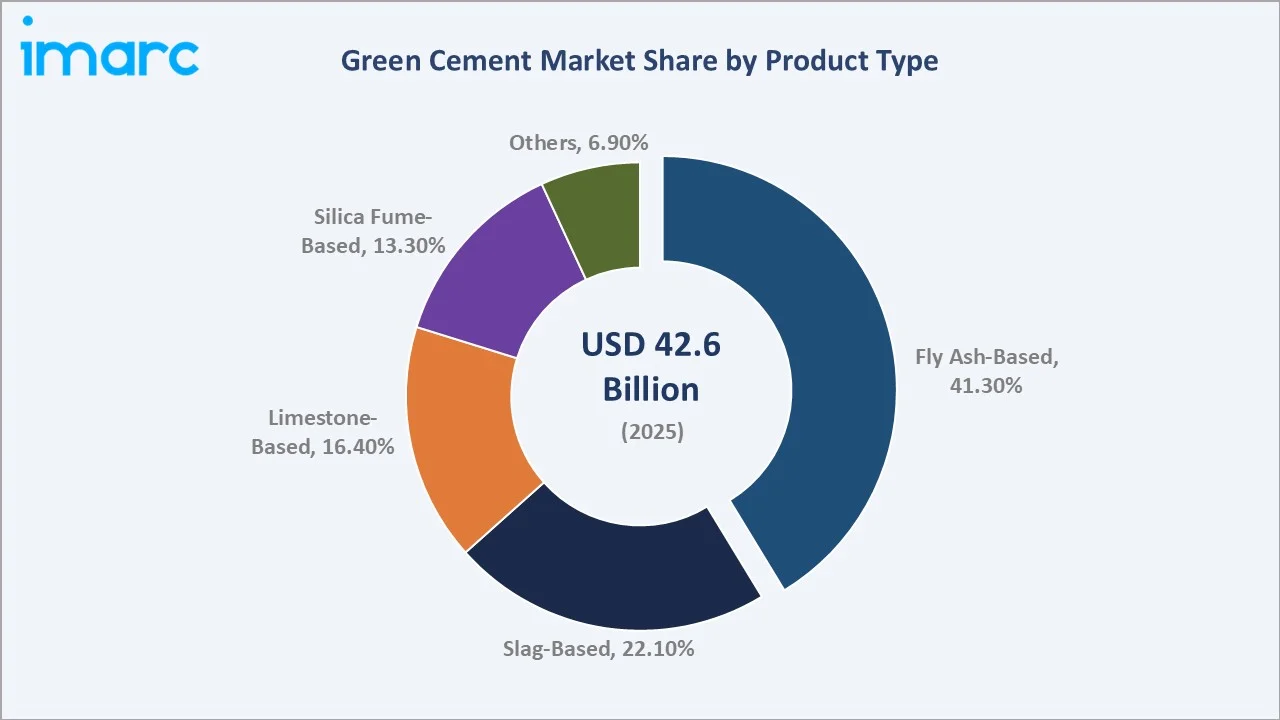

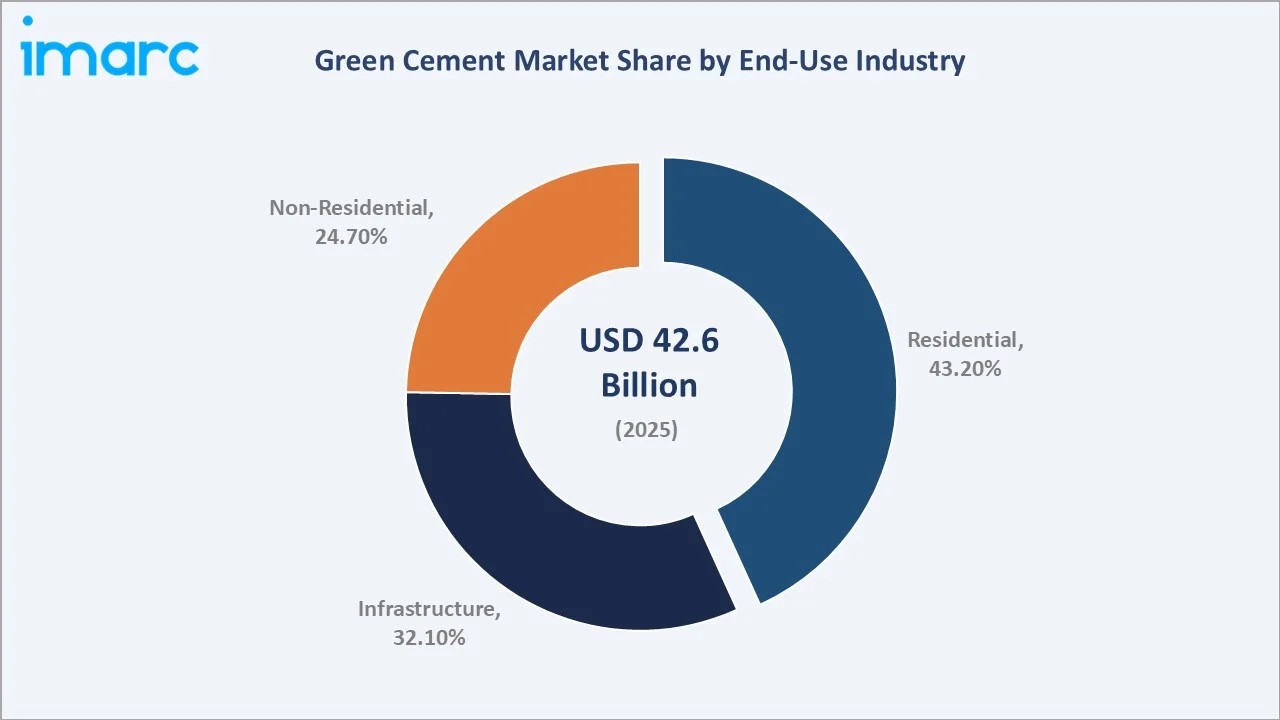

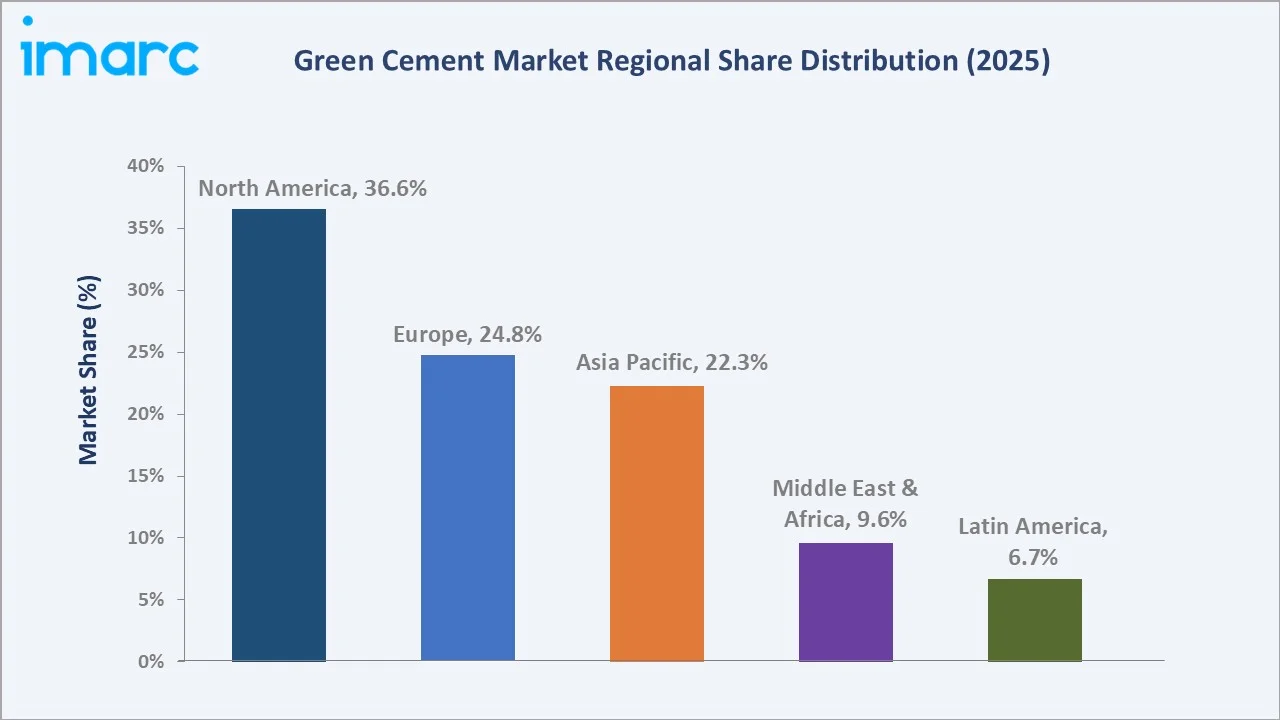

North America retains regional leadership with a 36.6% share in 2025. Among product types, fly ash-based cement commands the largest share at 41.3%, while the residential end-use industry sector accounts for 43.2% of total market demand.

To get more information on this market, Request Sample

The green cement market is gaining momentum globally as the construction industry shifts toward low-carbon and sustainable building materials. It leverages advanced technologies and alternative raw materials to significantly reduce environmental impact.

Executive Summary

The global green cement market continues to demonstrate robust expansion, underpinned by accelerating decarbonization mandates, rising ESG-linked construction financing, and the maturation of low-carbon cement technologies. Valued at USD 42.6 Billion in 2025, the market is forecasted to exceed USD 103.8 Billion by 2034 at a steady CAGR of 10.09%.

Among key growth drivers, the tightening of carbon pricing mechanisms and mandatory low-carbon procurement rules in public infrastructure spending remains the primary catalyst. The fly ash-based segment alone represented 41.3% of the global market value in 2025, reflecting deep penetration driven by abundant feedstock and proven performance. LC3 technology is gaining momentum, capable of reducing emissions by up to 40% while leveraging geographically widespread clay resources.

North America retains market leadership with a 36.6% share (2025), while Asia Pacific emerges as the fastest-growing region at a CAGR of ~12.5%, driven by China’s ultra-low emission cement plan and India’s five Carbon Capture and Utilization (CCU) testbed initiatives launched in May 2025. Leading market participants are investing in CCUS partnerships, clinker-free formulations, and ESG certification programs – all key areas reshaping the competitive landscape through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Fly Ash-Based - 41.3% share (2025) |

|

Largest Segment (End-Use Industry) |

Residential - 43.2% share (2025) |

|

Leading Region |

North America – 36.6% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – CAGR ~12.5% (2026-2034) |

|

Top Companies |

CarbonCure, CEMEX, LafargeHolcim, CRH, Heidelberg, UltraTech |

|

Market Opportunity |

The infrastructure segment is projected at ~USD 36.3 Billion by 2034 |

Key analytical observations supporting the above data:

- Fly ash-based cement dominates with 41.3% share (2025), driven by abundant coal combustion by-product availability, proven pozzolanic performance, and alignment with regulatory mandates on industrial waste utilization.

- Slag-based cement accounts for 22.1% (2025), retaining relevance near integrated steelworks due to superior long-term strength and reduced heat of hydration, especially in marine and mass concrete applications.

- Residential construction leads end-use industry at 43.2% (2025), propelled by green building certifications, ESG mortgage programs, and government incentives for low-carbon housing in the U.S., EU, and Australia.

- North America generates 36.6% of global revenues (2025), bolstered by the U.S. federal Buy Clean initiative and state-level LEED mandates in California, New York, and Massachusetts.

- Asia Pacific is the fastest-growing region (CAGR ~12.5%, 2026-2034), supported by India’s CCU testbed launch (May 2025) and China’s ultra-low emission cement plan targeting carbon neutrality by 2060.

Global Green Cement Market Overview

Green cement is an eco-friendly alternative to conventional Portland cement, formulated by replacing energy-intensive clinker with supplementary cementitious materials (SCMs) such as fly ash, ground granulated blast-furnace slag (GGBFS), limestone, calcined clay (LC3), and silica fume. The global cement industry contributes approximately 8% of global CO₂ emission, with each ton of conventional clinker releasing nearly 0.9 tons of CO₂.

The green cement industry has evolved from a niche sustainability product to a mainstream construction material. Policies such as the U.S. Buy Clean initiative, EU Green Deal, and Nationally Determined Contributions (NDCs) under the Paris Agreement are converting voluntary sustainability goals into binding procurement requirements.

The green cement market outlook is increasingly shaped by three converging forces: regulatory tightening, technological innovation, and ESG-driven capital allocation. Carbon pricing through emissions-trading schemes in the EU, Canada, and China structurally raises the cost of conventional clinker, conferring a competitive advantage on low-carbon alternatives.

Meanwhile, breakthroughs in LC3 technology, carbon capture and utilization (CCU), and CO₂ mineralization are expanding the technical toolkit for producers. ESG-linked bonds and sustainability-linked loans increasingly specify verified low-carbon building materials, creating a self-reinforcing demand loop.

Market Dynamics

To evaluate market opportunities, Request Sample

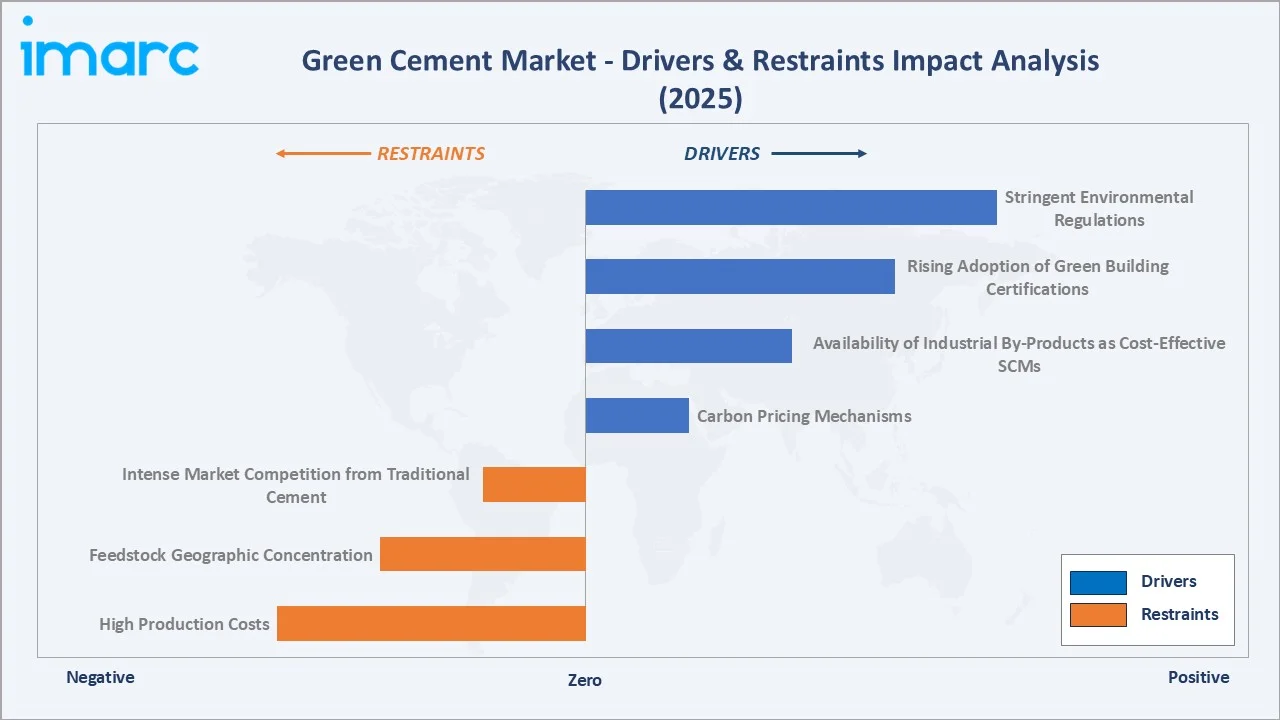

Market Drivers

- Stringent Environmental Regulations: Ireland mandated low-carbon cement in all state-funded projects in 2024, while Denmark introduced an average of 7.1 kg CO₂e/m²/year emission ceiling in 2025. These binding policies create a structural demand floor for green cement in public infrastructure.

- Rising Adoption of Green Building Certifications: Over 600,000 buildings across 93 countries have received BREEAM certification, while around 100,000 buildings worldwide are LEED-certified, covering 180 countries.

- Availability of Industrial By-Products as Cost-Effective SCMs: Fly ash from coal-fired power plants and GGBFS from steel mills are abundant, low-cost feedstocks that enable clinker substitution without sacrificing structural performance. U.S. ASTM C618 and EU EN 450 standards formalize their use, underpinning market confidence.

- Carbon Pricing Mechanisms: Rising carbon credit prices in emissions-trading schemes in the EU, Canada, and China systematically raise the relative cost of conventional clinker-based cement, conferring a structural cost advantage on green cement formulations and accelerating producer transitions.

Market Restraints

- High Production Costs: Advanced green cement formulations such as geopolymer cement can be 32% more expensive than conventional options. In cost-sensitive construction markets, especially across Sub-Saharan Africa and parts of South and Southeast Asia, this price premium remains a significant barrier to mass adoption.

- Feedstock Geographic Concentration: Industrial by-products such as fly ash and slag are concentrated near power plants and steelworks. Remote construction sites face elevated logistics costs that erode the economic case for green cement, limiting penetration in geographically dispersed markets.

- Intense Market Competition from Traditional Cement: Conventional Portland cement benefits from deeply entrenched supply chains, established standards, and lower upfront investment costs. Resistance from construction contractors unfamiliar with the new curing and workability requirements of green cement formulations slows specification uptake.

Market Opportunities

- Infrastructure Expansion in Asia Pacific: Rapid urbanization and government-backed infrastructure programs in India, Vietnam, Indonesia, and China present the most compelling growth opportunity. India launched the first cluster of CCU testbeds in academia-industry collaboration for cement in May 2025 , accelerating the commercial viability of low-carbon production.

- Carbon-Negative Technologies: CarbonCure’s CO₂ mineralization technology, Fortera’s ReCarb platform (which secured USD 85 Million in funding in August 2024),and algae-based cement are positioning the industry for carbon-negative production by the early 2030s, creating premium market segments.

- ESG-Linked Project Finance: Green bonds, sustainability-linked loans, and development finance increasingly require third-party environmental product declarations (EPDs). This financing-side mandate is converting specifiers and developers into active green cement adopters across commercial real estate and public infrastructure sectors.

Market Challenges

- Limited Standards Harmonization: Fragmented regulatory standards across national markets complicate product validation and cross-border market entry. Producers must invest in multiple certification pathways simultaneously, increasing compliance costs and lengthening time-to-market for new formulations.

- Declining Coal Generation Narrowing Fly Ash Supply: As coal power plants retire globally to meet climate targets, the long-term supply of fly ash, the largest SCM source today, is projected to tighten. Producers are already pivoting to legacy ash pond reclamation and alternative binders such as LC3 to mitigate feedstock risk.

- Consumer and Contractor Awareness Gaps: In many emerging markets, contractors lack familiarity with green cement’s workability characteristics, curing times, and performance benchmarks. Without targeted technical training and demonstration projects, specification uptake remains constrained beyond large institutional buyers.

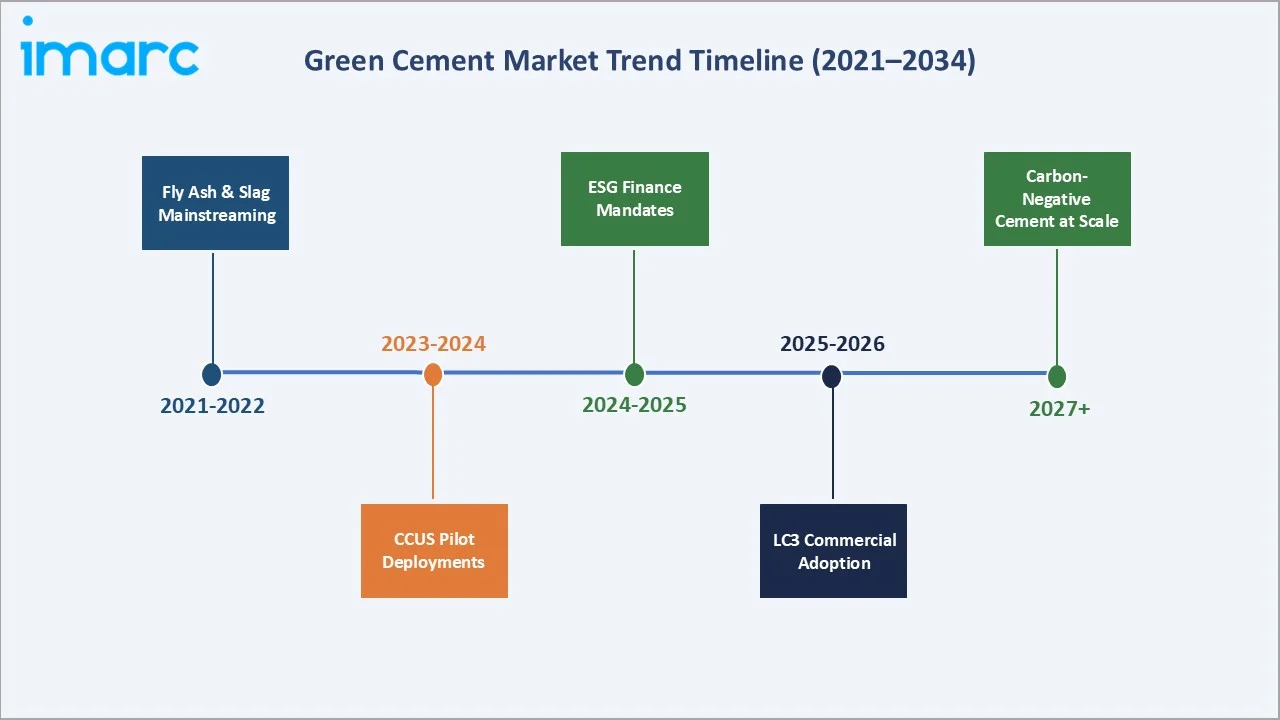

Emerging Green Cement Market Trends

1. Accelerated Adoption of Limestone Calcined Clay (LC3) Technology

Limestone Calcined Clay Cement (LC3) is emerging as the most transformative green cement market trend, capable of cutting CO₂ emissions by up to 30-40% using raw materials available in most geographies. Governments across 40+ countries have announced incentives for green building projects in 2025, driving LC3 integration into public-sector tenders.

2. Integration of Carbon Capture, Utilization, and Storage (CCUS) in Cement Plants

In January 2026, Holcim invested in Capsol Technologies to expand its decarbonization efforts by adopting advanced carbon capture technology aimed at reducing CO₂ emissions in cement production. Cemex has formalized a grant agreement with the EU Innovation Fund to advance its CO2LLECT project, to capture around 1.3 million tons of CO₂ annually at its Rüdersdorf plant in Germany.

3. ESG-Linked Financing Mandating Low-Carbon Materials

In May 2025, EMSTEEL (UAE) launched its first Green Finance Framework, earmarking capital for low-carbon cement and renewable energy. Holcim’s ECOPlanet expansion into Southeast Asia targeted high-growth markets where ESG-finance demand is surging. Procurement documents for commercial real estate and public-sector buildings now routinely require EPDs, converting major institutional developers into green cement adopters.

4. Hoffmann Green Cement and Clinker-Free Formulations Gaining Ground

In July 2025, Hoffmann Green Cement received major certification for its H-UKR 0% clinker cement in the U.S, with the product also recognized in Saudi Arabia. Clinker-free cements eliminate the single largest source of CO₂ in conventional production. This milestone reflects a broader industry shift: specialized disruptors are achieving regulatory recognition in key markets.

5. Digitalization and AI-Based Quality Control in Green Cement Production

Dangote Cement leverages AI-powered vision systems to enhance quality control in its production processes, resulting in a 20% reduction in defects. Predictive analytics tools are increasingly deployed to optimize SCM blending ratios, minimize energy consumption, and ensure consistent compressive strength across variable raw material inputs.

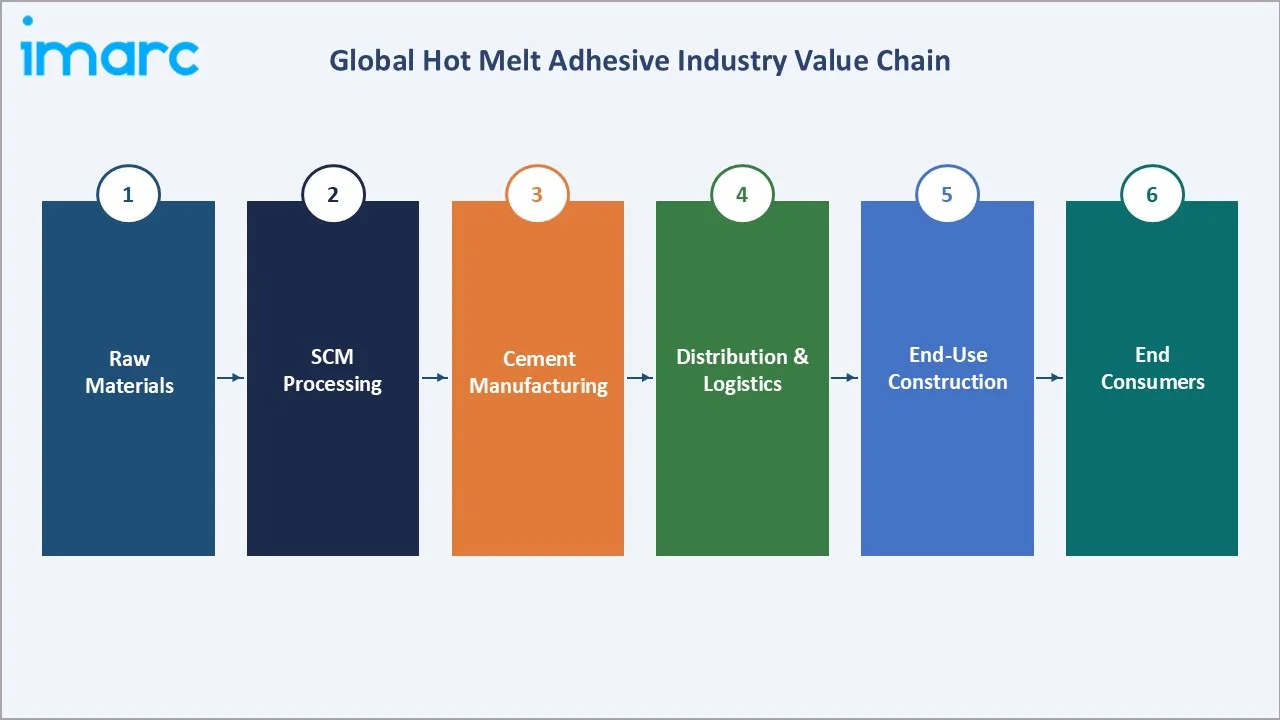

Industry Value Chain Analysis

The green cement industry value chain encompasses multiple interconnected stages, from raw material sourcing to end-use construction delivery. Each stage is populated by specialized operators whose performance directly influences product quality, cost competitiveness, and carbon compliance.

|

Stage |

Key Activities & Examples |

|

Raw Material Sourcing |

Fly ash collection from coal power plants; slag procurement from steel mills; limestone and clay mining for LC3 production. |

|

SCM Processing |

Fly ash classification and beneficiation; GGBFS grinding; clay calcination for LC3; silica fume collection from ferrosilicon smelters |

|

Green Cement Manufacturing |

Clinker substitution blending; low-carbon kiln operations; CCUS integration; alternative fuel use (waste, biomass) |

|

Quality Testing & Certification |

Third-party EPD generation; ASTM/EN standard compliance; carbon-intensity verification; LEED/BREEAM material documentation |

|

Distribution & Logistics |

Bulk cement terminals; bagged cement supply chains; regional distribution hubs; last-mile delivery to construction sites |

|

End-Use Construction |

Residential housing; commercial & industrial buildings; infrastructure (roads, bridges, metro systems, ports) |

|

End Consumers |

Homebuilders; real estate developers; infrastructure authorities; industrial plant operators; government agencies |

Technology Landscape in the Green Cement Industry

Supplementary Cementitious Material (SCM) Innovation

Advanced SCM science is enabling manufacturers to develop high-performance blends that reduce clinker content up to 80% while maintaining or exceeding conventional compressive strength benchmarks. Limestone calcined clay (LC3) formulations achieved mechanical parity with OPC in multi-country trials (2024–2025). Geopolymer cements using alkali-activated slags and fly ash represent the frontier, with pilot projects demonstrating up to 80% lower carbon intensity versus conventional production.

Carbon Capture, Utilization & Storage (CCUS)

CarbonCure Technologies’ CO₂ injection technology, which permanently mineralizes recycled carbon dioxide into concrete , has been deployed across hundreds of concrete plants in North America. Fortera’s ReCarb platform, which secured USD 85 Million in Series C funding (August 2024), integrates with existing kiln infrastructure to capture CO₂ and convert it into reactive calcium carbonate for re-use as a cement component – targeting 70% lower emissions per ton.

Digital Manufacturing and AI Quality Control

AI-powered quality control systems deployed across cement plants improved production efficiency by approximately 20% in 2024 by optimizing SCM blending ratios and minimizing kiln energy use in real time. Digital twin technology is enabling virtual commissioning of low-carbon cement plant retrofits, reducing capital risk for producers transitioning from conventional to green production at scale.

Alternative Fuel Technology

Major cement producers are replacing conventional fossil fuels with alternative fuel blends including municipal solid waste, biomass, refuse-derived fuel (RDF), and green hydrogen. Alternative fuel substitution rates of 30–60% have been achieved by European cement leaders, materially reducing Scope 1 emissions from kiln operations.

Market Segmentation Analysis

By Product Type

The fly ash-based sub-segment dominates the green cement market with a 41.3% share (2025), driven by abundant availability, cost-effectiveness, and well-documented performance across large-scale infrastructure and residential construction. The slag-based segment holds 22.1% (2025), remaining strong near integrated steel production centers. Limestone-based cement accounts for 16.4%, with LC3 technology expanding its commercial viability.

To access detailed market analysis, Request Sample

Fly ash-based cement's leadership is reinforced by mature logistics networks and standardized acceptance under U.S. ASTM C618 and EU EN 450 specifications. However, declining coal generation is narrowing long-term fly ash supply. Silica fume-based variants (13.3%) serve high-specification niches, including marine, bridge, and chemical containment structures.

By End-Use Industry

Residential construction leads end-use industry demand at 43.2% (2025), supported by green building mandates, LEED/BREEAM housing requirements, and ESG mortgage programs in North America, Europe, and Australia. Infrastructure accounts for 32.1% of consumption, reflecting mandatory low-carbon specifications in state-funded civil works across metro rail, highway, port, and water infrastructure projects.

Residential uptake is supported by declining mortgage rates in 2025, anticipated to lift housing starts globally, particularly in the U.S. and European markets. Non-residential growth is accelerating as data center, logistics, and manufacturing facility developers incorporate green cement into ESG reporting frameworks.

Regional Market Insights

North America’s market leadership (36.6% share, 2025) is entrenched by mature procurement systems and active policy infrastructure. The U.S. federal Buy Clean initiative requires federal agencies to prioritize low-carbon construction materials in publicly funded projects. EPA’s embodied-carbon reporting requirements for federal buildings, combined with LEED mandates across California, New York, and Massachusetts, are driving green cement specification across residential and civil infrastructure alike.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

North America |

36.6% |

Buy Clean initiative; LEED mandates; ESG housing finance; mature supply chains |

Federal embodied-carbon reporting; state/local public-building LEED requirements and incentives in selected jurisdictions; EPA emission rules |

Holcim, CEMEX, CRH plc, CarbonCure Technologies |

|

Europe |

24.8% |

EU Green Deal; CBAM; carbon pricing; circular economy mandates |

EU ETS; Denmark 7.1kg CO₂e/m² ceiling (2025); Ireland state mandate (2024); EN 450 standards |

Heidelberg Materials, Holcim, CRH plc, Hoffmann Green Cement |

|

Asia Pacific |

22.3% |

Urbanization; India CCU testbeds (2025); China ultra-low emission plan; smart city programs |

China's carbon neutrality by 2060; 50% cumulative installed electric power capacity from non-fossil fuel sources by 2030 |

Taiheiyo Cement, Anhui Conch, UltraTech, ACC Ltd., SCG |

|

Middle East & Africa |

9.6% |

Gulf hydrogen hubs; UAE net-zero roadmap; Qatar MECC sustainability rules; smart city infrastructure |

Qatar’s MECC announced a green cement innovation/project in 2024; UAE Net Zero 2050; GCC harmonization efforts |

Holcim MENA, Kiran Global Chem, Votorantim |

|

Latin America |

6.7% |

Urban housing programs; Brazil/Mexico green building incentives; ESG infrastructure financing |

Brazil carbon market launch; Mexico NAMA program; evolving emission standards |

Votorantim Cimentos, CEMEX, LafargeHolcim Latin America |

Asia Pacific (22.3%) is the fastest-growing region at an estimated CAGR of ~12.5% (2026–2034). China’s ultra-low emission cement plan aligns with its carbon neutrality goal by 2060. Southeast Asian nations are integrating green cement requirements into large-scale urban development programs, with Vietnam and Indonesia representing high-growth opportunity markets. The region’s abundant clay and limestone reserves make LC3 technology particularly cost-competitive.

Competitive Landscape

The global green cement market is moderately consolidated. The top five players, Holcim (LafargeHolcim), CEMEX, Heidelberg Materials, CRH plc, and Taiheiyo Cement, collectively account for approximately 54% of global market revenues in 2025.

|

Company Name |

Brand / Key Product |

Market Position |

Core Strength |

|

LafargeHolcim (Holcim) |

ECOPlanet |

Market Leader |

CCUS partnerships; eco-cement plants; global distribution network |

|

CEMEX S.A.B. de C.V. |

Vertua |

Market Leader |

Low-carbon cement R&D; EU Innovation Fund collaboration |

|

Heidelberg Materials |

evoBuild (global) / EcoCem PLC in North America |

Market Leader |

Carbon-neutral cement launches; Science-Based Targets commitment |

|

CRH plc |

ECO3 (Europe), Kolmossementti (Nordics) |

Strong Challenger |

Alternative fuel integration; North American & European scale |

|

CarbonCure Technologies |

CarbonCure Concrete |

Innovator |

CO₂ mineralization technology; it injects CO₂ into fresh concrete during mixing |

|

Fortera Corporation |

ReAct Cement |

Innovator |

ReCarb® platform; USD 85M Series C (Aug 2024); 70% lower CO₂/ton |

|

Taiheiyo Cement Corp |

Eco-Cement |

Regional Leader |

Asia Pacific leadership; waste-utilization technology |

|

UltraTech Cement Ltd. |

UltraTech Green |

Regional Leader |

India’s largest cement producer; sustainability product portfolio; CCU pilot projects |

|

Anhui Conch Cement |

Conch Green Series |

Regional Leader |

China’s largest producer; operational scale; low-carbon pilot CCUS deployments |

|

Votorantim Cimentos |

Votoran ECO |

Regional Leader |

Latin America market leader; alternative fuel use; green product range |

|

Siam Cement (SCG) |

SCG Low-Carbon Structural Cement |

Emerging Player |

Southeast Asia-focused; sustainable building solutions ecosystem |

Incumbent majors are scaling green portfolios by retrofitting kilns, increasing clinker substitution ratios, and forming CCUS partnerships, while specialized disruptors leverage proprietary chemistry to serve early adopters in premium specification markets.

Key Company Profiles

CarbonCure Technologies Inc.

CarbonCure is a Canada-based concrete decarbonization company whose technology injects captured CO₂ into fresh concrete during mixing, where it mineralizes permanently and supports cement efficiency. Its systems are deployed in hundreds of concrete plants globally.

- Product Portfolio: CO₂ injection systems for ready-mix concrete; retrofit solutions for existing concrete plants across North America, Europe, and the Asia Pacific.

- Recent Developments: Secured USD 20 Million in Q1 2024 to expand carbon capture technology deployment; active in over 700 concrete plants globally.

- Strategic Focus: Technology licensing, CCUS scale-up, and establishment of carbon credit frameworks for concrete producers.

CEMEX S.A.B. de C.V.

Founded in 1906 and headquartered in Monterrey, Mexico, CEMEX is a global building materials company operating in 50+ countries. Its Vertua range of reduced-emission cements is a flagship sustainable product.

- Product Portfolio: Vertua low-carbon and carbon-neutral cements; Vertua range is a core lower-carbon offering; sustainable aggregates and ready-mix.

- Recent Developments: Q2 2025 EU Innovation Fund agreement for next-generation green cement R&D; September 2025 launch of eco-friendly recycled-material cement products.

- Strategic Focus: Carbon-neutrality by 2050; USD 200M+ invested in low-carbon manufacturing technologies (2022–2024); digital carbon tracking across supply chain.

LafargeHolcim (Holcim Group)

Headquartered in Zug, Switzerland, Holcim (formerly LafargeHolcim) operates eco-cement plants across 43 countries. Its ECOPlanet product line delivers CO₂ reductions of up to 50% versus conventional cement.

- Product Portfolio: ECOPlanet green cement; ECOPact low-carbon concrete; ECOCycle recycled-material solutions.

- Recent Developments: August 2025 CCUS technology partnership announced; Q2 2025 ECOPlanet launch in Southeast Asia; Science-Based Target to reduce CO₂ intensity by 21% by 2030 vs 2018 baseline.

- Strategic Focus: CCUS commercial deployment; circular construction materials; Net-Zero CO₂ by 2050 under SBTi 1.5°C pathway.

Fortera Corporation

Fortera is a California-based company developing carbon capture and utilization technologies for the cement industry. Its ReCarb® platform integrates with existing manufacturing infrastructure to decarbonize cement production economically.

- Product Portfolio: ReAct green cement (emits 70% less CO₂/ton vs conventional); ReCarb CO₂ capture and conversion technology.

- Recent Developments: Secured USD 85 Million in Series C funding (August 2024) to accelerate global deployment of ReCarb® technology and expand ReAct manufacturing capacity.

- Strategic Focus: Scaling proprietary CCU technology; retrofit-first approach to decarbonization; expanding global manufacturing facility footprint.

Market Concentration Analysis

The global green cement market exhibits moderate concentration at the top end, with the leading five players, Holcim, CEMEX, Heidelberg Materials, CRH plc, and Taiheiyo Cement, holding approximately 54% of total revenues in 2025. The remainder is distributed among regional producers, national champions, and emerging clean-technology disruptors.

The market is more consolidated than conventional cement due to the higher capital intensity of green technology adoption and the regulatory certification barriers favoring established producers with global compliance infrastructure. The product segment level shows higher concentration in fly ash-based cement, where large producers with established SCM supply agreements dominate.

In specialized segments such as silica fume-based and geopolymer cements, the competitive landscape is more fragmented, with niche innovators competing on technical differentiation rather than scale. The top three players in the North American green cement market, Holcim, CEMEX, and CRH, command approximately 58% of regional revenues (2025), reflecting deep entrenchment supported by existing logistics networks and regulatory expertise.

Investment & Growth Opportunities

Fastest Growing Segments

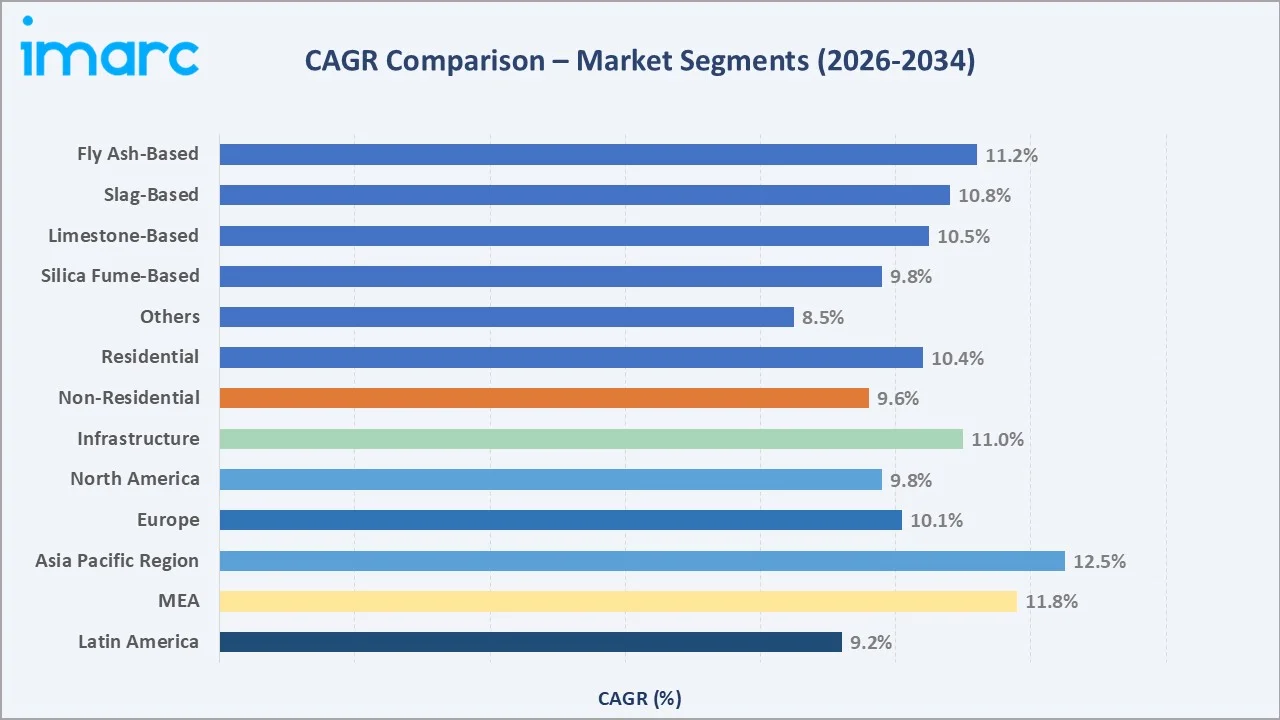

Asia Pacific (CAGR ~12.5%), Middle East and Africa (CAGR ~11.8%), and the infrastructure end-use industry segment (CAGR ~11.0%) represent the three highest-growth investment vectors through 2034. Within product types, limestone-based (LC3) and silica fume-based segments are gaining share rapidly as producers diversify away from fly ash dependency.

Emerging Market Expansion

Asia Pacific and the Middle East present the most compelling geographic investment opportunities. In line with its COP26 commitment, the country is working toward achieving 500 GW of non-fossil fuel electricity capacity by 2030. The Gulf Cooperation Council (GCC) region is planning USD 1+ trillion in infrastructure and smart city investment through 2030 , with Qatar’s MECC sustainability mandate and the UAE’s Net Zero 2050 roadmap creating binding demand for green building materials.

Venture Investment Trends

Investments in the green cement market surged over the years, as governments, private equity, and ESG-aligned institutional investors prioritized sustainable infrastructure. Green construction represents 31% of total ConTech venture funding, ranking as the second most funded segment , with key themes including CO₂ utilization, clinker-free chemistry, and LC3 commercialization.

- Key growth bets: CCU technology licensing, LC3 joint ventures, and clinker-free certification expansion into new national markets.

- ESG-aligned institutional investors are channeling capital into green cement projects that qualify under green bond frameworks and sustainability-linked loan structures.

- Development finance institutions (World Bank, ADB, IFC) are targeting low-carbon construction material supply chains in emerging Asia and Sub-Saharan Africa.

Future Green Cement Market Outlook (2026-2034)

The global green cement market is poised for sustained double-digit expansion through 2034, anchored by regulatory tightening, technological breakthroughs, and capital reallocation toward low-carbon construction. From a base of USD 42.6 Billion in 2025, the market is forecast to reach USD 103.8 Billion by 2034, representing an absolute incremental value addition of over USD 61.2 Billion over the forecast decade.

Technological disruptions, including carbon-negative cement formulations, AI-optimized SCM blending, and CCUS retrofit programs, are expected to materially reduce the production cost gap between green and conventional cement by 2028–2030. Producers achieving clinker substitution rates of 50%+ will gain a decisive competitive advantage in procurement-driven markets.

The next decade will witness a fundamental industry bifurcation: producers who invest early in CCUS, alternative binders, and certification infrastructure will capture premium pricing and long-term institutional contracts, while laggards face carbon cost escalation and potential regulatory exclusion from public-sector markets.

Research Methodology

Primary Research

Primary research for this report included structured interviews and consultations with over 150 industry participants in 2025, comprising cement plant executives, procurement managers, construction developers, government policy officials, and sustainability consultants across North America, Europe, and the Asia Pacific. Primary data was used to validate market size estimates and identify current strategic priorities.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, trade publications (Global Cement Magazine, International Cement Review, Construction Week), industry databases, and publicly available environmental reports and government policy documents. Over 200 secondary sources were reviewed and triangulated to ensure data accuracy and consistency.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, construction output data, carbon pricing trajectories, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was applied to account for regulatory uncertainty and feedstock supply volatility.

Green Cement Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Fly Ash-Based, Slag-Based, Limestone-Based, Silica Fume-Based, Others |

| End-Use Industries Covered | Residential, Non-Residential, Infrastructure |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | LafargeHolcim (Holcim), CEMEX S.A.B. de C.V., Heidelberg Materials, CRH plc, CarbonCure Technologies, Fortera Corporation, Taiheiyo Cement Corp, UltraTech Cement Ltd., Anhui Conch Cement, Votorantim Cimentos, Siam Cement (SCG), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the green cement market from 2020-2034.

- The green cement market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the green cement industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Green Cement Market Report

The global green cement market was valued at USD 42.6 Billion in 2025 and is projected to reach USD 103.8 Billion by 2034.

The green cement market is expected to grow at a CAGR of 10.09% during the forecast period 2026-2034, driven by tightening carbon-emission regulations, rising ESG-linked project financing, and growing demand for sustainable construction materials.

Fly ash-based cement is the largest segment, holding a 41.3% market share in 2025, driven by abundant feedstock availability, proven pozzolanic performance, and regulatory frameworks such as ASTM C618 and EU EN 450 formalizing its use.

Residential construction is the largest segment, accounting for 43.2% of the market, driven by rapid urbanization, rising housing demand, and increasing adoption of sustainable building materials supported by green building standards and government incentives.

North America is the dominant region, accounting for approximately 36.6% of global green cement market revenues in 2025, driven by the federal Buy Clean initiative, LEED mandates, and mature low-carbon cement supply chains in the U.S. and Canada.

Asia Pacific is the fastest-growing region, registering an estimated CAGR of ~12.5% (2026-2034), led by India’s CCU testbed program, China’s ultra-low emission cement plan, and rapid urbanization across Southeast Asian markets.

Key drivers include stringent carbon-emission regulations, rising adoption of ESG-linked project finance, availability of industrial by-products such as fly ash and slag, and growing demand for LEED/BREEAM green building certifications mandating low-carbon materials.

LC3 technology adoption, CCUS commercial deployment, ESG-linked financing mandating EPDs, Hoffmann-style clinker-free certifications, and AI-based production optimization are the fastest-growing green cement market trends through 2034.

Leading companies include CarbonCure Technologies, CEMEX, CRH plc, LafargeHolcim, Fortera Corporation, Heidelberg Materials, Siam Cement (SCG), Taiheiyo Cement Corp, Anhui Conch Cement, Votorantim Cimentos, UltraTech Cement, etc.

The top five green cement producers, Holcim, CEMEX, Heidelberg Materials, CRH plc, and Taiheiyo Cement, collectively account for approximately 54% of global revenues in 2025, reflecting a moderately consolidated but competitive market environment.

Key challenges include higher production costs for advanced formulations (20–30% premium over conventional cement), feedstock geographic concentration, fragmented regulatory standards across national markets, and contractor awareness gaps in emerging economies.

High-growth investment opportunities exist in Asia Pacific and GCC infrastructure programs, LC3 joint ventures, CCUS technology licensing, and clinker-free cement certification expansion into the U.S. and Middle Eastern markets, collectively targeting the USD 103.8 Billion market by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)