Advertising Market Size, Share, Trends and Forecast by Type and Region, 2026-2034

Global Advertising Market Size, Share, Trends & Forecast (2026-2034)

The global advertising market reached a value of USD 706.40 Billion in 2025 and is projected to reach USD 1,034.60 Billion by 2034, exhibiting a CAGR of 4.20% during the forecast period (2026-2034). Market expansion is driven by rapid digital transformation accelerating the shift of ad budgets toward online platforms, AI and data analytics enabling unprecedented targeting precision, and the explosive growth of connected TV (CTV), over-the-top (OTT), and mobile video advertising. North America dominates with a 32.6% revenue share in 2025, underpinned by high digital ad spending, advanced programmatic infrastructure, and strong engagement across social media and streaming platforms. Internet advertising leads all ad types at 34.7% (2025), followed by television advertising at 20.6%. In 2024, Omnicom Group and Interpublic Group completed a historic USD 13.25 Billion merger, underscoring the industry's accelerating convergence around AI-powered, data-driven advertising capabilities.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 706.40 Billion |

|

Forecast Market Size (2034) |

USD 1,034.60 Billion |

|

CAGR (2026-2034) |

4.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (32.6%, 2025) |

|

Fastest Growing Region |

Asia Pacific & MEA |

|

Leading Ad Type |

Internet Advertising (34.7%, 2025) |

|

Second Largest Ad Type |

Television Advertising (20.6%, 2025) |

The market's expansion from USD 575.06 Billion in 2020 to USD 706.40 Billion in 2025 reflects a robust recovery and structural shift post-pandemic, with digital channels absorbing an increasing share of total ad spend. The forecast addition of USD 328.2 Billion through 2034, a 46% value increase from the 2025 base, represents the largest absolute growth opportunity in the advertising industry's history.

Figure 1: Global Advertising Market Growth Trend (2020–2034)

The 4.20% CAGR through 2034 masks significant variation across ad types, internet and mobile advertising are growing at 8–10% annually, effectively absorbing share from traditional print and radio channels which are contracting in absolute terms in most developed markets. As per World Economic Forum, AI-projected economic contribution of USD 15.7 Trillion to the global economy by 2030 signals how deeply technology investment will reshape advertising effectiveness and ROI measurement.

Figure 2: CAGR Comparison – Advertising Market Segments (2026–2034)

Executive Summary

The global advertising market reached USD 706.40 Billion in 2025, representing one of the world's largest commercial communication ecosystems spanning traditional and digital media across all industry verticals. The market is forecast to reach USD 1,034.60 Billion by 2034 at a CAGR of 4.20%, crossing the USD 867.74 Billion milestone by 2030. Internet advertising dominates at 34.7% (2025), followed by television (20.6%), mobile (13.1%), print (11.6%), outdoor (9.6%), radio (7.6%), and cinema (2.8%). The combined digital advertising segment, internet plus mobile, commands 47.8% of total global ad spend in 2025, a share projected to reach approximately 55–58% by 2034 as digital transformation continues to redistribute media investment.

North America's 32.6% regional dominance (2025) is supported by the world's highest digital ad spending per capita, advanced programmatic trading infrastructure, and the headquarters concentration of global technology platforms including Google, Meta, Amazon, and The Trade Desk. Asia Pacific (28.4%) is the second-largest and fastest-growing major region, driven by China's domestic digital advertising ecosystem, India's rapidly expanding internet user base, and Southeast Asia's mobile-first advertising market.

Key Market Insights

|

Insight |

Data |

|

Market Size (2020) |

USD 575.06 Billion |

|

Market Size (2025) |

USD 706.40 Billion |

|

Market Size (2030) |

USD 867.74 Billion |

|

Market Forecast (2034) |

USD 1,034.60 Billion |

|

CAGR (2026–2034) |

4.20% |

|

Largest Ad Type |

Internet Advertising – 34.7% (2025) |

|

Fastest Growing Ad Type |

Mobile Advertising (~8.5% CAGR) |

|

Leading Region |

North America – 32.6% (2025) |

|

Second-Largest Region |

Asia Pacific – 28.4% (2025) |

|

Combined Digital Share |

47.8% (Internet + Mobile, 2025) |

|

Top Platform Players |

Google (Alphabet), Meta, Amazon Ads, The Trade Desk |

Key analytical observations supporting the above data:

- Internet advertising’s 34.7% share (2025) reflects the dominance of search, social media, display, and programmatic video formats as the primary media investment destination for performance-driven advertisers globally.

- Television advertising at 20.6% (2025) remains resilient despite digital disruption, sustained by its unmatched reach for brand-building campaigns, live sports and entertainment programming, and the rapid growth of connected TV (CTV) advertising bridging traditional broadcast and streaming consumption.

- Mobile advertising’s 13.1% share (2025) is growing rapidly, driven by global smartphone penetration, 5G network rollout enabling richer mobile ad formats, and the mobile-first nature of social media, gaming, and short-form video platforms including TikTok and Instagram Reels.

- North America's 32.6% share reflects the concentration of major global digital advertising platforms (Google, Meta, Amazon), the world's largest advertising holding companies (WPP, Omnicom, Publicis, IPG), and the highest-per-capita advertising investment among all major geographies.

- Print advertising’s 11.6% share is declining in relative terms across developed markets, but remains significant in emerging economies where print media retains strong local readership, and in specialized B2B publication advertising segments.

Global Advertising Market Overview

The global advertising industry encompasses all paid communication activities through which businesses, organizations, and individuals promote their products, services, ideas, or brands to target audiences across media channels. The ecosystem spans traditional media including television, print, radio, outdoor, and cinema alongside digital channels including search engine marketing, social media advertising, programmatic display, video (CTV/OTT), mobile in-app, email, and emerging formats including AR/VR and audio streaming. The U.S. accounts for approximately 90% of North American ad spend and holds a dominant global position, with nearly half of the population uses social media daily, creating vast audience targeting opportunities for advertisers across all sectors.

Figure 3: Global Advertising Industry Value Chain

Market Dynamics

Figure 4: Advertising Market Drivers & Restraints – Impact Analysis (2025)

Market Drivers

- Rapid Digital Transformation and Online Platform Migration: The fundamental shift of consumer attention from traditional to digital media is driving sustained reallocation of advertising budgets toward online channels. Television advertising grew by USD 17 Billion between 2020 and 2021 and is projected to maintain a consistent spend of approximately USD 131 Billion between 2023 and 2028, but its share of total ad spend is declining as digital channels absorb a growing proportion of incremental advertising investment globally.

- AI and Data Analytics Revolution: Artificial intelligence is transforming advertising effectiveness through machine learning-powered audience targeting, real-time bidding optimization, AI-generated creative variations, and predictive campaign analytics. AI is projected to contribute USD 15.7 Trillion to the global economy by 2030, with advertising among the highest-impact application sectors. Advertisers leveraging AI platforms are achieving 20–40% improvements in cost-per-acquisition metrics versus manually optimized campaigns.

- Mobile Penetration and 5G Network Rollout: The global smartphone user base exceeds 6.9 Billion (2025), with mobile devices representing the primary internet access point for more than half of global internet users. 5G network deployment is enabling richer, lower-latency mobile ad formats including interactive video, AR overlays, and immersive gaming ad units. Mobile advertising's share of total digital spend is growing at approximately 9.33% CAGR of 2026-2034.

Market Restraints

- Data Privacy Regulations and Cookie Deprecation: GDPR in Europe, CCPA in California, and global equivalents are reshaping advertising targeting capabilities. Google's deprecation of third-party cookies, delayed multiple times but progressing through 2025, is forcing the industry to develop privacy-compliant identity and targeting alternatives. Compliance investment and reduced targeting precision create operational headwinds.

- Ad Fraud and Brand Safety Risks: Digital advertising faces endemic fraud challenges including click fraud, impression fraud, domain spoofing, and invalid traffic. Brand safety incidents, where ads appear alongside inappropriate content, create reputational risk and drive advertiser pullback from open programmatic exchanges.

- Ad Blocking Technology Adoption: 1 out of 3 internet users globally employ ad blocking software, reducing the effective reach of display and pre-roll video advertising. Ad blockers are most prevalent among high-income, tech-savvy demographics, precisely the audiences most valuable to premium advertisers – creating a material reach gap for digital display campaigns.

Market Opportunities

- Connected TV (CTV) and Streaming Advertising: Netflix, Disney+, Amazon Prime Video, and HBO Max have all introduced ad-supported subscription tiers, creating significant new premium video advertising inventory. In terms of television's growth engine, connected TV (CTV) is surpassing linear. CTV is expected to surpass 40% of global ad spending by 2030, while linear TV, which was once the unchallenged monarch, has dropped to just 12%.

- Programmatic Audio and Podcast Advertising: Podcast advertising revenues in the U.S. exceeded USD 2 Billion in 2023 and are growing at 12% annually. Programmatic audio advertising on platforms including Spotify, Apple Music, and iHeartRadio enables precise demographic targeting in a non-skippable, attention-rich audio environment.

- AR/VR and Immersive Advertising Formats: Augmented reality advertising, enabling consumers to virtually try products, interact with brand experiences, and engage with geo-located AR overlays is generating click-through achieved 20% more clicks than standard display advertising. Meta's AR ad formats and Snapchat's AR lens advertising demonstrate the commercial viability of immersive formats at scale.

Market Challenges

- Attribution and Measurement Complexity: The proliferation of consumer touchpoints across devices, channels, and platforms has made advertising attribution increasingly complex and contested. Multi-touch attribution models, media mix modeling, and incrementality testing require significant investment and statistical expertise, creating measurement uncertainty that complicates advertising budget allocation decisions.

- Talent and Technology Investment Requirements: The advertising industry's digital transformation requires continuous investment in data science, programmatic buying, creative technology, and AI capabilities. The talent shortage in data-driven advertising specializations, particularly in programmatic trading, audience modeling, and marketing analytics is constraining industry growth capacity.

- Platform Concentration and Dependency Risk: Google, Amazon, and Meta collectively control approximately 55% of global digital advertising revenues, creating significant platform dependency risk for advertisers and agencies. Algorithm changes, policy shifts, or regulatory actions affecting either platform can materially disrupt advertiser ROI without advance warning.

Emerging Market Trends

The global advertising market is experiencing its most transformative period in decades, driven by five converging technological and behavioral shifts that are fundamentally redefining how brands reach, engage, and convert consumers through 2034.

Figure 5: Advertising Market Trend Timeline (2020–2034)

1. Generative AI and Creative Automation

Generative AI is disrupting advertising creative production, enabling brands to produce hundreds of ad variations, personalize creative at scale, and reduce production costs. Nearly 90% advertisers have already started using Generative AI. Platforms including Google Performance Max, Meta Advantage+, and Adobe Firefly are embedding generative AI into campaign creation workflows.

2. Retail Media Networks: The Third Wave of Digital Advertising

After search (Google) and social media (Meta), retail media represents the third major programmatic advertising category. Amazon Advertising alone generated approximately USD 46.9 Billion in ad revenues in 2023, surpassing all global advertising holding companies. Walmart Connect, Kroger Precision Marketing, Target Roundel, and international equivalents are building scaled first-party data advertising platforms that enable closed-loop attribution from ad exposure to purchase.

3. Privacy-First Targeting and First-Party Data Strategies

The deprecation of third-party cookies is accelerating advertiser investment in first-party data collection, customer data platforms (CDPs), and privacy-compliant identity solutions including Google Privacy Sandbox, universal IDs (Unified ID 2.0), and contextual targeting. Brands with rich CRM databases and customer loyalty programs are gaining structural targeting advantages.

4. Connected TV and Streaming Platform Advertising

The advertising opportunities will rise in tandem with the amount of time spent on CTV. Despite the fact that CTV ad spend growth would decrease from 18.8% in 2024 to 13.3% in 2025. Netflix, Disney+, Amazon, and HBO Max ad-supported tier launches have created premium, brand-safe video inventory at scale.

Industry Value Chain Analysis

The advertising industry value chain encompasses seven interconnected stages from brand strategy development through to audience delivery and campaign measurement. Each stage involves specialized expertise and technology infrastructure that collectively determines advertising campaign effectiveness and return on investment.

|

Stage |

Key Activities |

Representative Players |

|

Advertiser / Brand |

Marketing strategy, budget allocation, campaign objectives, brand governance |

P&G, Unilever, Apple, Samsung, L'Oreal, financial services brands |

|

Creative & Media Agency |

Campaign strategy, creative production, media planning and buying |

WPP, Publicis, Omnicom/IPG, Dentsu, Havas, independent agencies |

|

Ad Tech Platforms |

DSP/SSP technology, DMP, CDPs, programmatic trading, ad verification |

The Trade Desk, Google DV360, Xandr, LiveRamp, DoubleVerify, IAS |

|

Media Channels |

Ad inventory supply across all media types: digital, TV, print, OOH, radio |

Google, Meta, Amazon, TV networks, publishers, OOH companies |

|

Data & Analytics |

Audience data, attribution modeling, brand lift measurement, fraud detection |

Nielsen, Comscore, IRI, Oracle Data Cloud, Acxiom |

|

Publishing & Distribution |

Content platforms, streaming services, social networks, websites |

YouTube, Netflix, Spotify, news publishers, app developers |

|

End Audience |

Consumer engagement across all screens and touchpoints; purchase conversion |

Global internet users, TV viewers, radio listeners, OOH audiences |

The ad tech platform stage has become the most strategically significant value chain layer, as programmatic trading infrastructure now mediates the majority of global digital advertising transactions. The Trade Desk's independent DSP position, processing over USD 12 Billion in annual media spend, exemplifies how ad tech platforms capture value by sitting between advertisers and media inventory at industrial scale.

Technology Landscape in the Advertising Industry

Programmatic Advertising Infrastructure

Real-time bidding (RTB) and programmatic direct technologies now facilitate the majority of digital display, video, mobile, and connected TV advertising transactions. The programmatic ecosystem, comprising demand-side platforms (DSPs), supply-side platforms (SSPs), data management platforms (DMPs), and ad exchanges, processes billions of ad auction requests per second globally.

Artificial Intelligence and Machine Learning

AI applications in advertising span campaign planning, audience modeling, creative optimization, bid management, attribution, and fraud detection. Google's Performance Max and Meta's Advantage+ campaigns use AI to automatically allocate budget across channels, optimize creative delivery, and identify high-value audience segments in real time.

Data Clean Rooms and Privacy-Safe Analytics

Data clean rooms, secure environments where first-party data from multiple parties can be analyzed without raw data sharing are becoming essential infrastructure for privacy-compliant audience insights and attribution. Amazon Marketing Cloud, Google Ads Data Hub, and NBCUniversal's One Platform are leading examples of clean room deployments enabling advertisers to measure cross-channel campaign effectiveness while maintaining compliance with privacy regulations.

Market Segmentation Analysis

By Advertising Type

The global advertising market is segmented into seven primary ad format categories, each with distinct audience reach profiles, campaign suitability, and growth trajectories as of 2025.

Internet and mobile advertising collectively command above 47% of global ad spend (2025) and are the primary drivers of market growth, projected to reach approximately 55% of total spend by 2034. Television advertising’s 20.6% share remains significant, underpinned by the CTV/streaming transition that is preserving TV advertising’s value proposition in digital-addressable form.

Figure 6: Global Advertising Market Share by Type (2025)

Figure 7: Advertising Market Share by Ad Type – Donut View (2025)

By Region

The global advertising market exhibits pronounced regional differentiation, with North America's digital infrastructure maturity and high per-capita advertising investment creating a structurally dominant position, while Asia Pacific's scale and growth momentum positions it as the most strategically significant region for future advertising expansion.

Asia Pacific's 28.4% share (2025) is bifurcated into two distinct sub-markets: China's domestic digital advertising ecosystem, controlled by Baidu, ByteDance/TikTok, Alibaba, and Tencent, operates largely independently of the global programmatic infrastructure dominated by Google and Meta. The rest of Asia Pacific, including India, Southeast Asia, Australia, and Japan, is deeply integrated with the Google-Meta programmatic duopoly, representing significant scale for global platform advertising revenues.

Figure 8: Regional Advertising Market Share Distribution (2025)

Digital Advertising Format Evolution: 2025 vs. 2034

Within the internet advertising segment, the market's largest and fastest-growing category – significant format-level shifts are expected over the 2025–2034 forecast period. Video advertising (CTV, OTT, in-stream) is projected to gain the most share, at the expense of traditional search and display formats.

Figure 9: Digital Advertising Format Share – 2025 vs. 2034 Forecast

Video advertising's share is expected to significantly increase within digital formats (2025–2034) reflects the structural migration from linear television to streaming video, the monetization of short-form video platforms (TikTok, YouTube Shorts, Instagram Reels), and the rapid adoption of CTV advertising by both direct-response and brand advertisers.

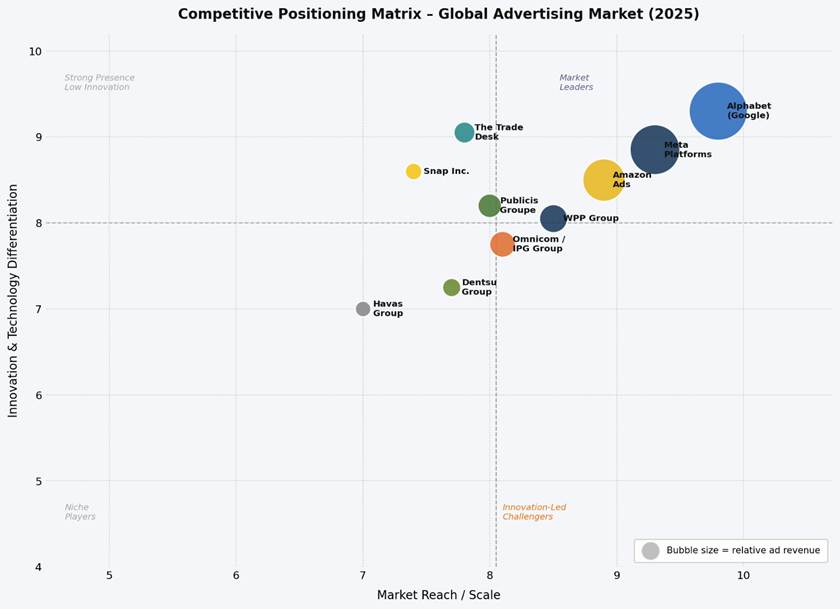

Competitive Landscape

The global advertising market is structurally divided between two primary competitive tiers: the dominant technology platform layer (Alphabet/Google, Meta, Amazon) that controls the majority of digital advertising inventory and data infrastructure; and the advertising agency holding company layer (WPP, Omnicom/IPG, Publicis, Dentsu) that manages brand strategy, creative production, and media buying execution on behalf of advertiser clients.

|

Company |

Key Brand(s) |

Market Position |

Primary Strategy |

|

Alphabet Inc. (Google) |

Google Ads, YouTube, DV360 |

Global Digital Ad Leader |

Search dominance, YouTube video, programmatic ecosystem, AI-first campaign tools |

|

Meta Platforms Inc. |

Facebook Ads, Instagram, WhatsApp |

Leader – Social Advertising |

Social commerce, AI creative tools (Advantage+), Reels video, WhatsApp business |

|

Amazon Advertising |

Amazon Ads, DSP |

Leader – Retail Media |

Retail media closed-loop attribution, Prime Video ads, programmatic DSP expansion |

|

WPP Group |

Ogilvy, Grey, GroupM, Wunderman |

Leader – Agency Holding |

AI transformation, data-driven creative, GroupM programmatic media buying scale |

|

Publicis Groupe |

Saatchi & Saatchi, Leo Burnett, Epsilon |

Leader – Agency & Data |

Epsilon first-party data platform, AI creative, integrated media-data-tech model |

|

Omnicom / IPG |

BBDO, TBWA, McCann, OMD, Mediabrands |

Leader – Agency (post-merger) |

AI capabilities post-merger, data platform consolidation, media scale |

|

The Trade Desk |

The Trade Desk DSP |

Leader – Independent AdTech |

Independent programmatic DSP, OpenPath publisher direct, UID 2.0, CTV leadership |

|

Dentsu Group |

dentsu, Carat, iProspect |

Established – Agency |

Creative transformation, APAC strength, data and performance media services |

|

Havas Group |

Havas Media, Havas Creative |

Challenger – Agency |

Integrated village model, sustainability positioning, mid-market advertiser focus |

|

Snap Inc. |

Snapchat Ads |

Challenger – Social/AR |

AR advertising innovation, Gen-Z audience, Snap Map location ads |

Google, Amazon, and Meta collectively control approximately 55% of global digital advertising revenues, creating a structural duopoly that shapes competitive dynamics for all participants in the digital advertising ecosystem. Amazon's emergence as the third major digital advertising platform represents the most significant competitive disruption to the Google-Meta duopoly in the industry's history.

Figure 10: Competitive Positioning Matrix – Global Advertising Market (2025)

Key Company Profiles

Alphabet Inc. (Google)

Alphabet's Google is the world's largest advertising company, generating approximately USD 82.3 Billion in advertising revenues in Q4 of FY25 through Google Search, YouTube, Google Display Network, and Google Cloud-powered advertising tools. YouTube's advertising business hit $11.4 billion in Q4 2025, up from $10.5 billion in the same period last year.

- Product Portfolio: Google Search Ads, Google Display Network, YouTube (TrueView, Shorts ads, CTV), Google Performance Max, DV360 (programmatic DSP), Google Ad Manager (SSP), Google Analytics 4.

- Recent Developments: Launched Privacy Sandbox as the cookie-replacement framework; expanded Gemini AI integration into Performance Max; accelerated YouTube Shorts monetization globally in 2024.

- Strategic Focus: AI-first advertising automation (Performance Max), Privacy Sandbox cookieless targeting, YouTube CTV growth, Google Cloud AI infrastructure for advertiser data analytics.

Meta Platforms Inc.

Meta generated approximately USD 200 Billion in revenues in 2025, making it the world's second-largest digital advertising platform. Facebook, Instagram, and WhatsApp collectively serve over 3 Billion daily active users.

- Product Portfolio: Facebook Ads Manager, Instagram Ads, WhatsApp Business Ads, Meta Advantage+ (AI campaigns), Reels Ads, Meta Audience Network, AR ad formats.

- Recent Developments: Launched Threads platform with ad integration (2023); expanded Meta Advantage+ AI campaign automation globally; introduced limited WhatsApp advertising in select markets.

- Strategic Focus: AI-driven campaign automation (Advantage+), social commerce integration, Reels short-form video monetization, AR/VR advertising platform development via Meta Reality Labs.

Amazon Advertising

Amazon Advertising is the world's third-largest digital advertising platform, generating approximately USD 46.9 Billion in ad revenues in 2023. Amazon's retail media network benefits from unparalleled purchase intent data from its e-commerce platform.

- Product Portfolio: Sponsored Products, Sponsored Brands, Amazon DSP, Amazon Marketing Cloud (clean room), Prime Video Ads, Twitch advertising, Amazon Fresh and Whole Foods media.

- Recent Developments: Launched Prime Video advertising with the transition of Prime Video to ad-supported model in 2024; expanded Amazon DSP deal ID offerings for programmatic buyers.

- Strategic Focus: Retail media closed-loop measurement, Prime Video advertising scale, programmatic DSP expansion beyond Amazon.com, and Amazon Marketing Cloud clean room growth.

WPP Group

WPP is the world's largest advertising agency holding company by revenue, generating approximately USD 14.8 Billion in annual revenues in 2023. WPP's GroupM division is the world's largest media investment management company.

- Product Portfolio: Ogilvy, VMLY&R, Wunderman Thompson, Grey, GroupM (media buying), Mindshare, Wavemaker, MediaCom, Choreograph (data platform).

- Recent Developments: Launched WPP Open Pro AI platform for creative and media production automation in 2025; merged Wunderman Thompson and VMLY&R into VML agency brand.

- Strategic Focus: AI transformation of creative and media production, Choreograph first-party data platform development, portfolio simplification, and client retention through integrated services.

The Trade Desk

The Trade Desk is the world's largest independent demand-side platform (DSP). Its independence from media ownership is a key competitive differentiator for advertisers seeking unbiased programmatic execution.

- Product Portfolio: Trade Desk DSP, OpenPath (publisher direct access), Unified ID 2.0 (privacy-compliant identity), Kokai AI platform, CTV buying infrastructure.

- Recent Developments: Launched Kokai AI platform for campaign intelligence in 2023; expanded OpenPath direct publisher connections to over 100 major media companies; advanced UID 2.0 adoption across the open internet.

- Strategic Focus: Independent programmatic leadership, CTV advertising growth, cookieless identity (UID 2.0), AI-powered campaign optimization (Kokai), and retail media data integration.

Market Concentration Analysis

The global advertising market exhibits a dual concentration structure: at the platform layer, the digital advertising ecosystem is highly concentrated around Google, Meta, and Amazon, which collectively control approximately 55–60% of global digital advertising revenues.

The traditional media sector, broadcast television, print publishing, outdoor advertising, remains more fragmented, with national public and commercial broadcasting groups, regional newspaper and magazine publishers, and diversified outdoor companies competing across geographically defined markets. Consolidation in this segment is driven by audience fragmentation and digital migration rather than technology investment requirements.

Investment & Growth Opportunities

Fastest Growing Segments

Connected TV advertising, retail media networks, programmatic audio and podcast advertising, and digital out-of-home (DOOH) advertising represent the highest-growth investment vectors in the global advertising market through 2034. These segments collectively address a total addressable market exceeding USD 150 Billion by 2034.

Emerging Market Expansion

India's digital advertising market is growing at approximately 15% annually, driven by the world's largest internet user growth trajectory, UPI-enabled digital commerce, and the rapid adoption of short-form video platforms. Southeast Asia's combined advertising market is growing at 10–12% annually, led by Indonesia, Vietnam, and Thailand's expanding digital economies. Sub-Saharan Africa's mobile-first advertising market represents a long-term opportunity.

Technology and Innovation Investment Trends

- Generative AI advertising technology companies are attracting significant venture and corporate investment, with tools for AI creative generation, AI media planning, and AI campaign measurement representing the three highest-value application categories.

- Retail media technology platforms enabling brands to access first-party purchase data from retailers are attracting private equity and strategic investment, with CommerceIQ, Skai, and Perpetua among the leading scaled players.

- Privacy-tech and identity resolution companies developing cookieless targeting solutions are attracting investment as the industry's over USD 100 Billion annual ad fraud and targeting loss problem intensifies post-cookie deprecation.

- CTV and streaming advertising technology including interactive ad formats, CTV measurement platforms, and addressable TV infrastructure, represents a USD 20+ Billion investment opportunity as linear TV advertising migrates to digital-addressed formats.

Future Market Outlook (2026-2034)

AI will be the most consequential structural force reshaping advertising through 2034. Generative AI for creative production, AI-powered media optimization, and AI-driven attribution are projected to automate more than half of the tasks currently performed by human advertising professionals by 2030. This automation will simultaneously reduce cost per campaign outcome for advertisers and compress margins for agencies, forcing business model transformation toward strategic consulting, proprietary data ownership, and technology platform development.

The advertising market of 2034 will be characterized by the convergence of previously distinct media channels, television, digital display, social media, audio, and out-of-home, into a unified programmatic, AI-optimized omnichannel advertising ecosystem. Brands with rich first-party data assets, real-time creative generation capabilities, and cross-channel measurement sophistication will achieve decisive competitive advantages in an advertising environment where audience attention is more fragmented, privacy-regulated, and algorithmically intermediated than at any prior point in the industry's history.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 180 industry participants in 2024–2025, comprising brand advertisers, agency media buyers, programmatic ad technology executives, media publishers, digital platform representatives, and advertising industry analysts across North America, Europe, Asia Pacific, and emerging markets.

Secondary Research

Secondary research encompassed a comprehensive review of advertiser annual reports, agency group financial disclosures, regulatory filings, trade publications (Advertising Age, Campaign, Digiday, The Drum), industry associations (IAB, WARC, GroupM This Year Next Year forecast), and publicly available advertising market data from major research firms. Over 400 secondary sources were reviewed and triangulated for market size validation.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down GDP-correlated advertising expenditure modeling and bottom-up ad type segment forecasting, incorporating media consumption data, digital penetration rates, programmatic trading volumes, and historical ad-to-GDP ratio analysis by region. Scenario analysis across base, optimistic, and conservative macroeconomic cases was performed to account for economic cycle uncertainty over the 2026–2034 forecast horizon.

Advertising Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Alphabet Inc. (Google), Meta Platforms Inc., Amazon Advertising, WPP Group, Publicis Groupe, Omnicom / IPG, The Trade Desk, Dentsu Group, Havas Group, Snap Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the advertising market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global advertising market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the advertising industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global advertising market was valued at USD 706.4 Billion in 2025 and is projected to reach USD 1,034.60 Billion by 2034, growing at a CAGR of 4.20%.

The market is forecast to grow at a CAGR of 4.20% during 2026-2034, driven by digital transformation, AI-powered advertising capabilities, mobile penetration, and retail media network expansion.

North America dominates with a 32.6% market share in 2025, driven by high digital ad spending, concentration of major advertising platforms, and advanced programmatic trading infrastructure.

Internet advertising leads all segments with a 34.7% share in 2025, encompassing search, social media, display, programmatic, and video formats across desktop and streaming platforms.

Key drivers include digital transformation and online platform migration, AI and data analytics enabling precise targeting, mobile and 5G penetration, social media and influencer marketing growth, and retail media network expansion.

The global advertising market is projected to reach USD 867.74 Billion by 2030, reflecting sustained compound growth from the 2025 base of USD 706.40 Billion at the market's 4.20% CAGR.

Leading companies include Alphabet Inc. (Google), Meta Platforms Inc., Amazon Advertising, WPP Group, Publicis Groupe, Omnicom/IPG, The Trade Desk, Dentsu Group, Havas Group, and Snap Inc.

Internet and mobile advertising collectively command 47.8% of global ad spend in 2025, projected to reach approximately 55–58% by 2034 as digital channels continue to absorb ad budget share from traditional media.

AI is transforming advertising through generative creative production, ML-powered audience targeting, real-time bid optimization, and automated campaign management, driving 20–40% improvements in advertiser cost-per-acquisition metrics.

The USD 13.25 Billion Omnicom-IPG merger completed in 2024 created the world's largest advertising holding company, explicitly driven by AI and data capability requirements, signaling that scale in first-party data and AI infrastructure is now the decisive competitive advantage in agency advertising.

Key investment opportunities include CTV advertising technology (~22% CAGR), retail media networks (~15-20% CAGR), programmatic audio and podcast advertising (~12% CAGR), and digital out-of-home advertising (~10% CAGR).

Key challenges include data privacy regulations and cookie deprecation reshaping targeting, ad fraud costing advertisers ~USD 84 Billion annually, ad blocking reducing digital reach, attribution complexity across fragmented media channels, and platform concentration dependency risks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)