GCC Car Rental Market Size, Share, Trends and Forecast by Booking Type, Rental Length, Vehicle Type, Application, End User, and Country, 2026-2034

GCC Car Rental Market Size, Share, Trends & Forecast (2026-2034)

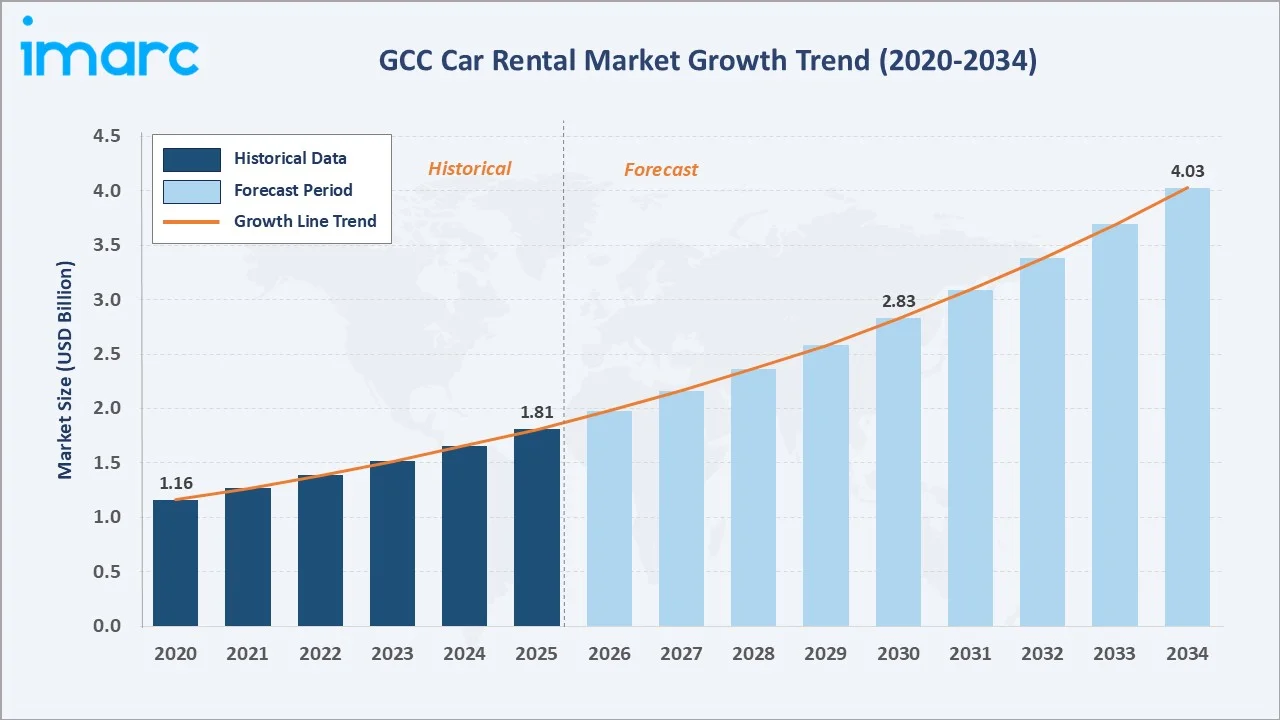

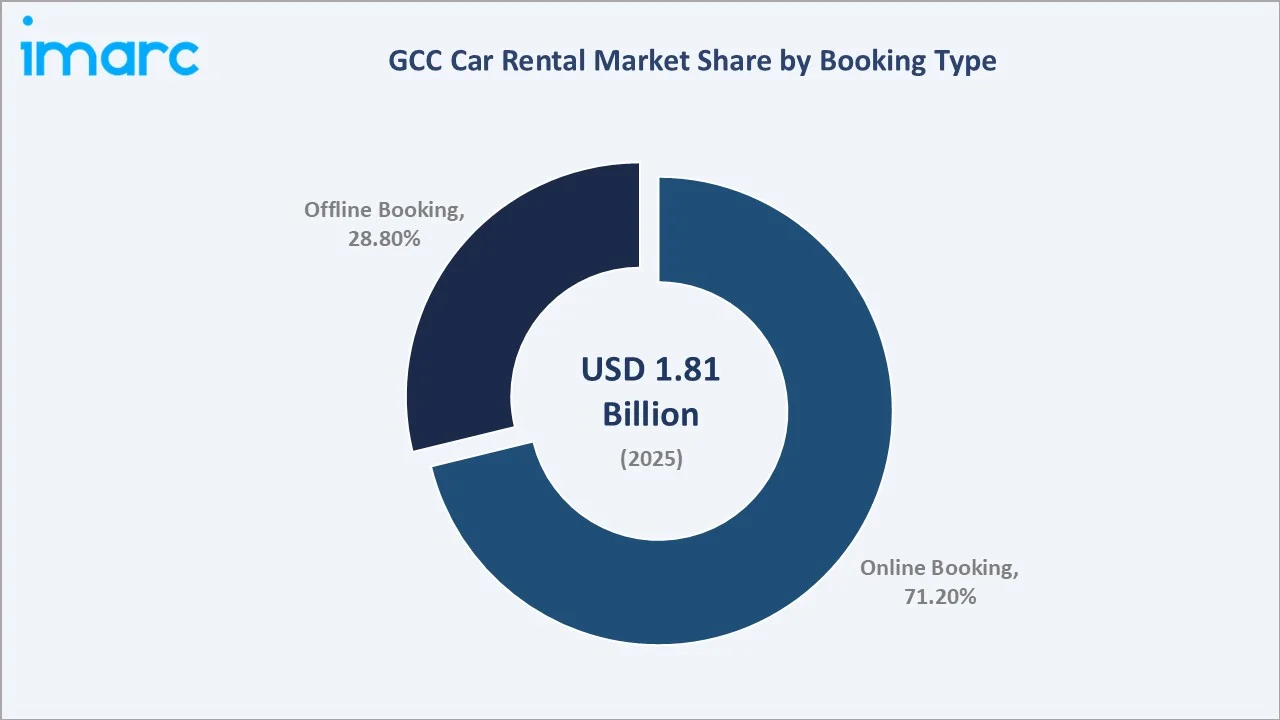

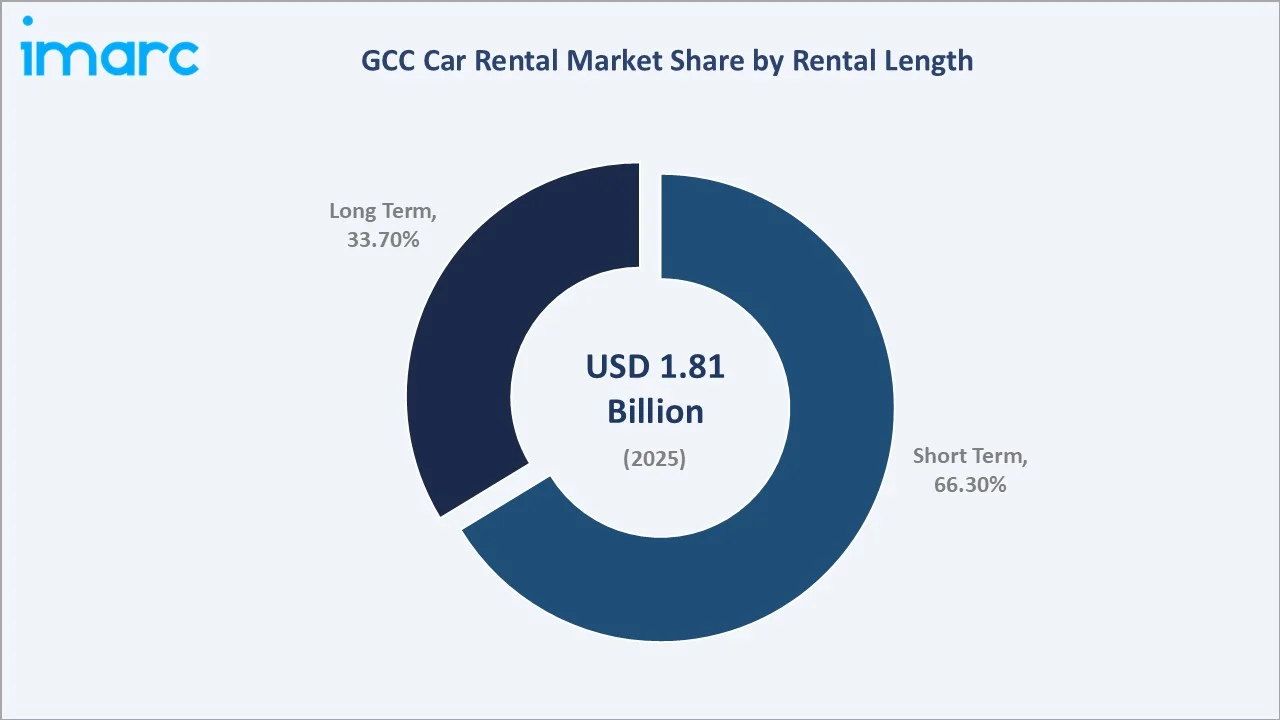

The GCC car rental market reached USD 1.81 Billion in 2025 and is projected to reach USD 4.03 Billion by 2034, growing at a CAGR of 9.31% during 2026-2034. Surging inbound tourism, expanding expatriate populations, robust business travel demand, and the rapid adoption of digital booking platforms are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.81 Billion |

|

Forecast Market Size (2034) |

USD 4.03 Billion |

|

CAGR (2026-2034) |

9.31% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

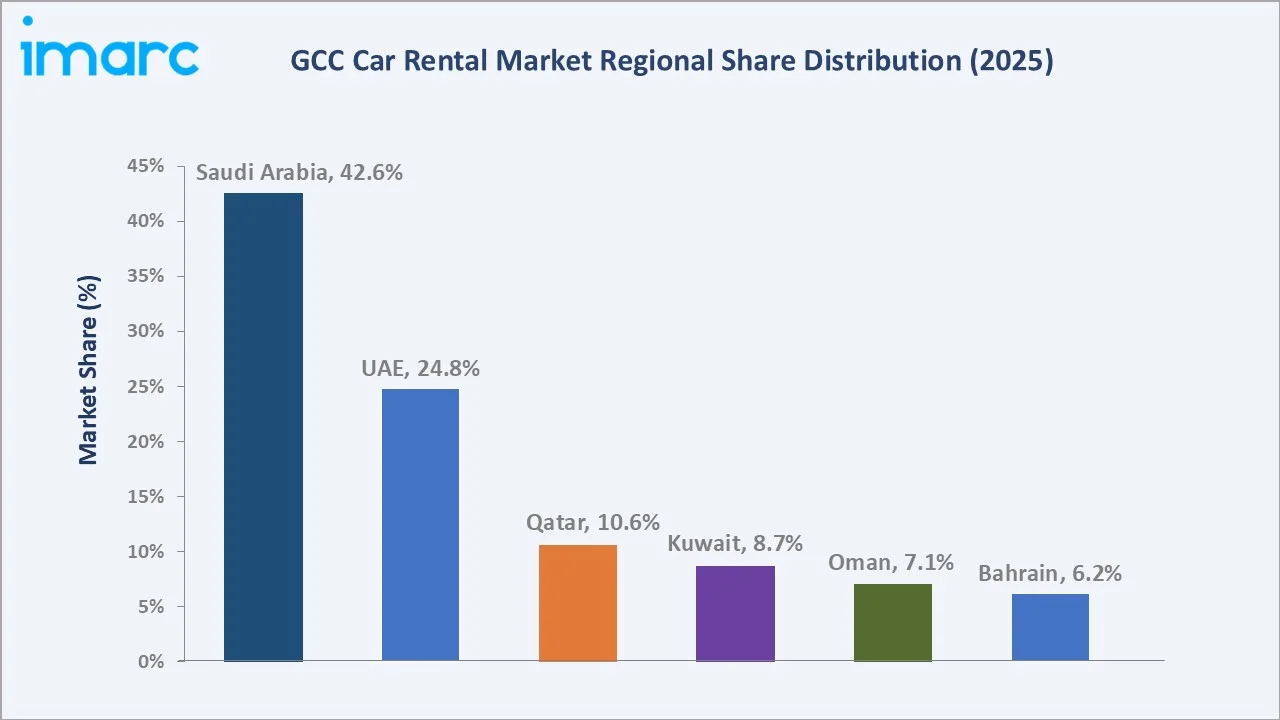

Saudi Arabia (42.6%) |

|

Fastest Growing Country |

Qatar / UAE |

To get more information on this market, Request Sample

The market exhibits a steady expansion across the historical window (2020-2025), driven by post-pandemic tourism recovery, rising infrastructure investment, and structural demand from the GCC's large expatriate workforce. The forecast period (2026–2034) is expected to sustain double-digit momentum underpinned by Vision 2030 and UAE Net Zero 2050 programs.

Executive Summary

The GCC car rental industry is on a strong structural expansion path. The market grew from USD 1.16 Billion in 2020 to USD 1.81 Billion in 2025, representing a 56% cumulative increase over five years. A rebound in international tourism underpinned this growth, with the hosting of mega events such as the FIFA World Cup 2022 in Qatar, Expo 2020 in Dubai, and expanding corporate mobility requirements.

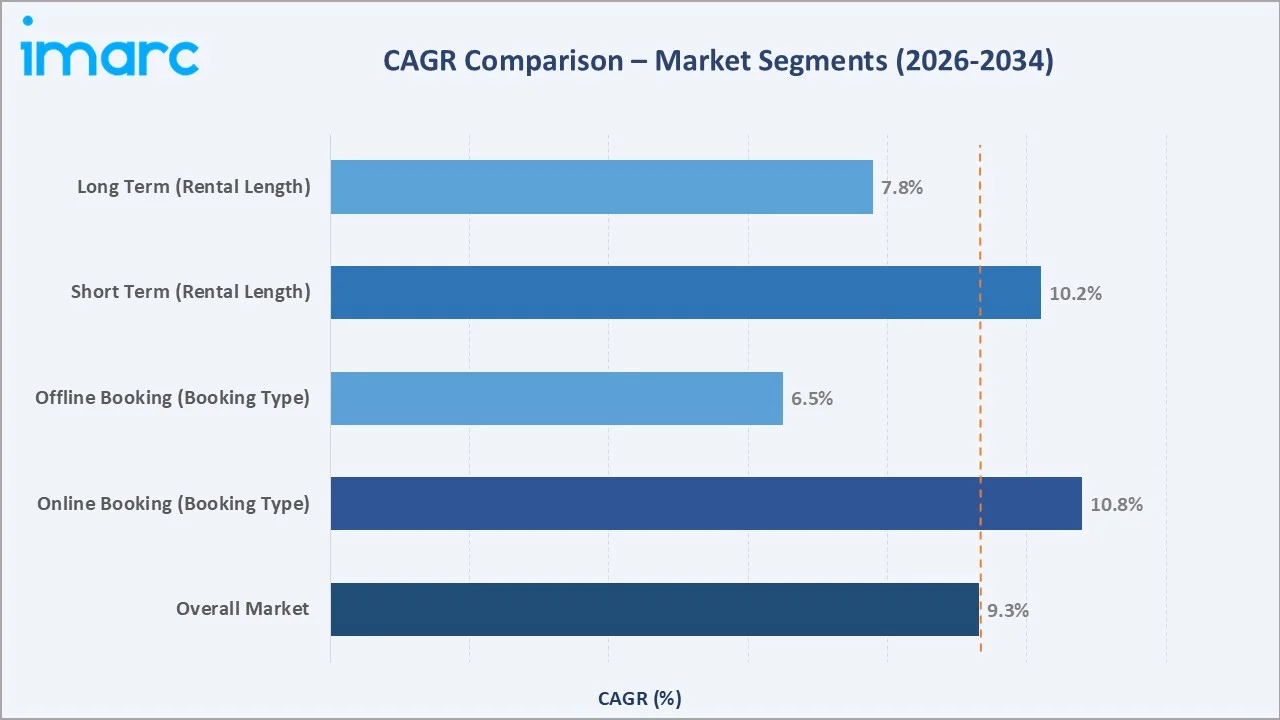

Online booking accounts for 71.2% of market revenue in 2025, signaling a decisive industry pivot toward app-based and platform-driven reservations. Short-term rentals retain dominance at 66.3%, catering primarily to tourists and business travelers seeking flexible, short-duration mobility. Saudi Arabia commands 42.6% of GCC car rental revenue in 2025, driven by its Vision 2030 tourism ambitions and the year-round Hajj and Umrah travel cycle.

Key operators, including Enterprise Holdings, Inc., The Hertz Corporation, Sixt, Budget Rent A Car LLC., and Al Sulaiman Rent-A-Car., are investing in fleet diversification, EV integration, and super-app partnerships. The market is forecast to reach USD 4.03 Billion by 2034 as mobility-as-a-service (MaaS) models gain traction across GCC smart cities.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Booking Type) |

Online Booking – 71.2% share (2025) |

|

Largest Segment (Rental Length) |

Short Term – 66.3% share (2025) |

|

Leading Country |

Saudi Arabia – 42.6% (2025) |

|

Fastest Growing Segment |

Online Booking (~10.8% CAGR, 2026-2034) |

|

Top Companies |

Enterprise Holdings, Inc., The Hertz Corporation, Sixt, Budget Rent A Car LLC., and Al Sulaiman Rent-A-Car. |

|

Market Opportunity |

EV fleet & MaaS platforms; USD 4.0B by 2034 |

Key analytical observations supporting the above data:

- Online booking (71.2% in 2025) continues to outpace offline channels due to smartphone penetration exceeding 98% in Saudi Arabia, and the rapid growth of super-apps such as Careem and Uber across the GCC.

- Short-term rentals (66.3% in 2025) dominate as visitors to the GCC average 5–7 day stays, while business travelers, accounting for approximately 38% of rental demand, prefer daily or weekly contracts.

- Saudi Arabia's 42.6% market share in 2025 is reinforced by over 30 million Hajj and Umrah pilgrims annually, requiring ground transportation between Mecca, Medina, and Jeddah.

- Qatar (10.6%) and the UAE (24.8%) are among the fastest-growing markets post-2022, benefiting from mega-event tourism infrastructure that now serves year-round commercial travel.

- EV fleet adoption remains below 5% of total GCC rental inventory in 2025 but is expected to reach 18–22% by 2030 as charging networks expand under UAE Net Zero 2050 and Saudi Arabia's Green Initiative.

GCC Car Rental Market Overview

Car rental in the GCC encompasses short- and long-term provision of passenger and commercial vehicles on a self-drive or chauffeur-driven basis. The industry ecosystem spans fleet operators, OEM suppliers, digital booking aggregators, insurance providers, and fuel distribution networks. The absence of a fully integrated public transit network across several GCC cities makes car rental an essential mobility solution for both residents and visitors.

Market Dynamics

The GCC car rental market is shaped by structural growth enablers, competitive restraints, strategic opportunities, and operational challenges. Understanding these dynamics is essential for stakeholders seeking to position effectively in this high-growth mobility market.

To evaluate market opportunities, Request Sample

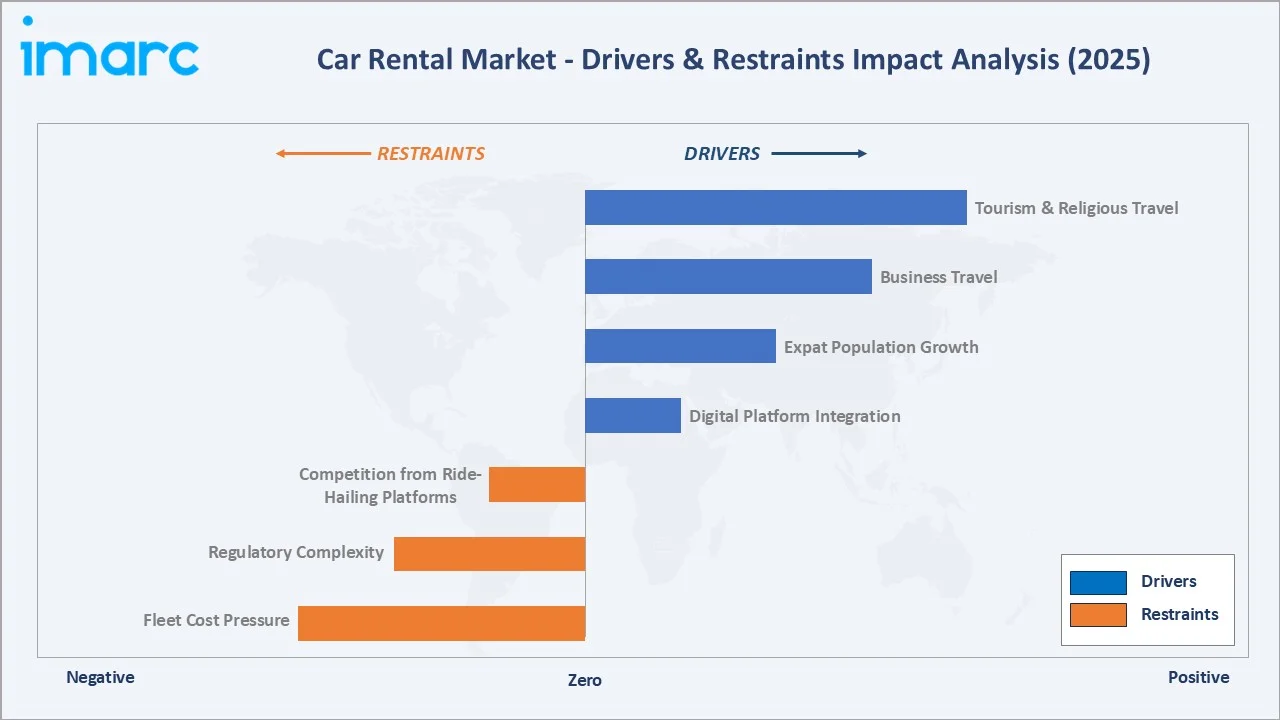

Market Drivers

- Rising Tourism and Religious Travel: Over 9.31 million tourists visited Dubai in H1 2024, an 8.9%+ year-on-year increase. Religious tourism in Saudi Arabia, anchored by Hajj and Umrah, drives over 10 million pilgrims requiring ground transport annually.

- Expanding Expatriate Population: Expatriates constitute 88% of the UAE's population in 2025, which equals approximately 9.2 million foreign residents. Frequent job-linked relocations generate sustained demand for monthly and long-term rental contracts.

- Business Travel Growth: The Middle East business travel market is projected to grow by 11.2% in 2024, with executive class and chauffeur-driven rentals benefiting from increased MICE activity in Riyadh, Dubai, and Doha.

- Infrastructure Development: Saudi Arabia's Vision 2030 and the UAE's smart city investments have produced world-class road networks and modern airport terminals with embedded rental desks, supported by over USD 1.5 trillion in planned infrastructure projects through 2035.

Market Restraints

- Fleet Procurement and Maintenance Costs: New vehicle prices surged 18–22% during 2021–2023 due to global semiconductor shortages, compressing margins for fleet operators absorbing elevated acquisition costs.

- Regulatory Heterogeneity: Licensing, insurance regulations, and fleet-age restrictions differ across all six GCC member states, raising operational complexity and compliance costs for pan-GCC operators.

- Competition from Ride-Hailing Platforms: Uber and Careem collectively command a 30%+ share of urban point-to-point mobility in Dubai and Riyadh, competing directly with daily rental demand.

Market Opportunities

- Electric Vehicle Fleet Expansion: Aligned with UAE Net Zero 2050 and the Saudi Green Initiative, EV fleet segments represent an estimated incremental revenue opportunity of USD 320 Million by 2030 across the GCC.

- Super-App and API Integration: Integration with regional super-apps (Careem, Noon, stc pay) creates frictionless booking funnels, potentially improving average fleet occupancy rates from 68% to over 80%.

- Long-Term Subscription Models: Corporate fleet subscription services, offering fixed monthly rates inclusive of maintenance and insurance, are growing at an estimated 14% CAGR, driven by giga-project activity in Saudi Arabia.

Market Challenges

- EV Charging Infrastructure Gaps: Despite rapid investment, EV charging points per vehicle remain limited outside Abu Dhabi and Dubai, restricting fleet electrification beyond core urban corridors through 2027.

- Driver Shortage: Chauffeur-driven segments face a skilled driver deficit estimated at 15–20% of required headcount across Saudi Arabia and the UAE as of 2025, limiting capacity expansion in premium categories.

Emerging Market Trends

1. Digital-First Booking Platforms

Online channels now constitute 71.2% of GCC car rental revenues in 2025. Mobile-first booking apps enable real-time vehicle selection, digital KYC, and in-app payment, reducing check-in time. Companies such as Hertz and SIXT have launched dedicated GCC app versions with Arabic language support, boosting conversion among local and regional users.

2. Electric and Hybrid Fleet Integration

EV adoption is accelerating in the UAE and Saudi Arabia. The Dubai Taxi Company (DTC) introduced 250 new EV units in 2024, with rental operators following suit. The GCC EV market is projected to grow at a CAGR of 28.4% through 2030, enabling rental operators to reduce the total cost of ownership by 15–20% over five years.

3. Subscription-Based and Long-Term Lease Models

All-inclusive subscription rentals are displacing traditional ownership, particularly among expatriates and corporate clients. Selfdrive.ae, the largest mobility tech platform in the Middle East, rose by 20% in demand for car subscriptions in 2024, generating higher per-customer revenue.

4. Contactless and AI-Powered Operations

AI-driven dynamic pricing, predictive fleet management, and contactless vehicle handover are now standard among top-tier operators. Recent research indicates that AI-driven predictive maintenance can cut equipment downtime by up to 50% and extend machine life by 20-40%.

5. Sustainable Tourism Linkages

Saudi Arabia's Vision 2030 targets 150 million tourist visits by 2030. Car rental is a critical enabler of this ambition. Operators offering eco-labelled vehicles and carbon-offset packages are gaining preferential listing status on major travel platforms, including Booking.com and Expedia.

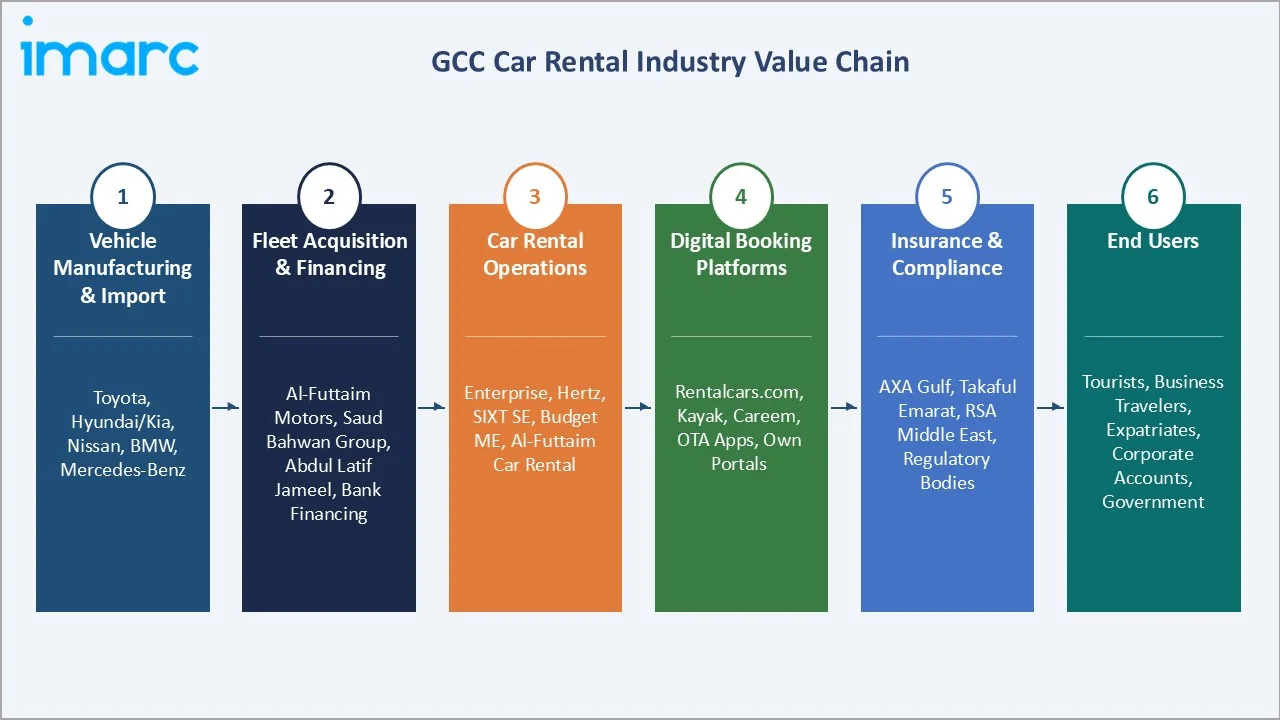

Industry Value Chain Analysis

The GCC car rental value chain spans vehicle manufacturing and import, fleet acquisition, technology platform integration, and end-user mobility delivery. Each stage adds strategic value and represents a distinct competitive battleground for operators seeking sustainable margin advantage.

|

Value Chain Stage |

Key Players / Description |

|

Vehicle Manufacturing & Import |

Toyota, Hyundai, Kia, Nissan, BMW, Mercedes-Benz – primary OEM suppliers to GCC fleets |

|

Fleet Acquisition & Financing |

Abdul Latif Jameel – fleet procurement and bank lease financing |

|

Car Rental Operations |

Enterprise Holdings, Inc., Hertz Corporation, SIXT SE, Budget Middle East, National Car Rental (GCC)– core rental operators |

|

Digital Booking Platforms |

Rentalcars.com, Kayak, Careem, proprietary apps – online aggregators driving 71.2% of bookings |

|

Insurance & Compliance |

GIG Gulf (Gulf Insurance Group), Liva (formerly RSA Middle East) – vehicle insurance and regulatory compliance |

|

Maintenance & Servicing |

Authorized service centers, OEM dealerships – critical for fleet uptime and safety standards |

|

End Users |

Tourists, business travelers, expatriates, corporate accounts, government entities |

Technology Landscape in the GCC Car Rental Industry

AI-Driven Fleet Management and Dynamic Pricing Platforms

Advanced machine learning algorithms process real-time inputs, including seasonal tourism surges, corporate booking patterns, vehicle availability, and competitive rate benchmarks, to generate dynamic pricing that maximises revenue per vehicle per day. Saudi Arabia's Transport General Authority recorded a 31% rise in digital vehicle registrations in 2024, a trend that has accelerated the deployment of AI-driven platforms capable of ingesting government data streams alongside operator analytics to refine fleet deployment decisions in real time.

Telematics and IoT-Based Fleet Tracking

Saudi Arabia's Transport General Authority has actively catalyzed telematics adoption by offering subsidies for telematics installation under its national fleet modernization program. Companies such as Aljomaih Automotive and Yelo are deploying IoT-driven systems to increase fleet uptime and lower total cost of operations, with the government subsidy framework ensuring that mid-sized operators can access connected-vehicle infrastructure at commercially viable cost points.

Digital Booking Platforms and Mobile-First Customer Engagement

The structural move to digital is grounded in the GCC's exceptionally high smartphone penetration. Ericsson Mobility data places GCC smartphone penetration at 82%, and a population that is both digitally literate and accustomed to app-driven service delivery across banking, retail, and mobility verticals. Automating check-in processes through digital platforms has trimmed average transaction times to under four minutes while simultaneously reducing labor costs for multi-branch operators.

Contactless and Keyless Vehicle Access Technology

Near-field communication (NFC) digital keys, QR-code unlock protocols, and Bluetooth-enabled smartphone-to-vehicle pairing allow customers to complete identity verification, payment authorization, and vehicle unlock in a single digital workflow, bypassing traditional counter check-in entirely. In December 2023, UAE-based EV mobility platform EVLAB launched an all-in-one app that enables seamless rental, leasing, and vehicle hosting across multiple EV brands — a model that embeds keyless access as a core service feature rather than an optional upgrade.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Booking Type |

Online Booking |

71.2% |

2025 |

|

Rental Length |

Short Term |

66.3% |

2025 |

|

Vehicle Type |

SUVs |

42.4% |

2025 |

|

Application |

Leisure/Tourism |

68.5% |

2025 |

|

End-User |

Self-Driven |

60.4% |

2025 |

|

Country |

Saudi Arabia |

42.6% |

2025 |

By Booking Type

To access detailed market analysis, Request Sample

The GCC car rental market is segmented by booking type into online booking and offline booking. Online booking dominated with a 71.2% share in 2025, driven by high smartphone penetration and consumer preference for seamless digital experiences across the GCC.

Offline booking retains a 28.8% share in 2025, serving airport walk-in customers, SMEs with negotiated contracts, and travelers in lower-connectivity markets. Growth in this segment, estimated at approximately 6.5% CAGR, is driven by premium concierge-style services at GCC airports, where on-counter upselling generates higher average transaction values than digital channels.

By Rental Length

The market is segmented by rental duration into short-term and long-term rentals. Short-term rentals dominate with a 66.3% share in 2025, reflecting the GCC's high proportion of tourist and transient business traveler demand.

Long-term rentals (one month and above) account for 33.7% of market revenue in 2025 and are growing at approximately 7.8% CAGR. Corporate clients engaged in giga-project construction in Saudi Arabia, including NEOM, the Red Sea Project, and Diriyah Gate, represent the primary growth engine, alongside expatriate households preferring subscription models over vehicle ownership.

Regional Market Insights

Saudi Arabia leads the GCC car rental market at 42.6% of revenues in 2025, followed by the UAE (24.8%), Qatar (10.6%), Kuwait (8.7%), Oman (7.1%), and Bahrain (6.2%). Each market presents distinct demand characteristics and regulatory environments.

|

Country |

2025 Share |

Key Growth Drivers |

Notable Dynamics |

|

Saudi Arabia |

42.6% |

Vision 2030; Hajj/Umrah; NEOM & giga-projects |

Largest fleet base; major airport hubs (Riyadh, Jeddah); 18.5 million total Hajj and Umrah pilgrims in 2024 |

|

UAE |

24.8% |

Global business hub; 9.3M Dubai tourists H1 2024 |

Highest rental rate per day (~USD 55–80); strong corporate demand; EV fleet early adopter |

|

Qatar |

10.6% |

FIFA 2022 legacy infrastructure; growing MICE market |

Post-2022 infrastructure serves year-round tourism; Smart city platform implementation (Q4 2024–2027) |

|

Kuwait |

8.7% |

Large expat workforce; growing retail/commercial hub |

Strong demand from oil and gas contractors; limited public transit drives rentals |

|

Oman |

7.1% |

Eco-tourism growth; Oman Vision 2040 |

Expanding tourist destination; scenic road trips driving short-term rental demand. |

|

Bahrain |

6.2% |

Financial services sector; Saudi weekend tourism |

Smallest market; cross-border demand via the King Fahd Causeway supports rental volumes |

Saudi Arabia's dominance is structurally reinforced by the scale of Hajj and Umrah travel and giga-project construction activity. The UAE commands the highest revenue per rental day in the GCC, estimated at USD 55–80 in 2024, versus a GCC average of USD 40–55. Qatar's post-2022 infrastructure investment supports year-round tourism, with the country targeting 6 million annual visitors by 2030.

Competitive Landscape

The GCC car rental market is moderately concentrated. The top four operators – Enterprise Holdings, Inc., The Hertz Corporation, Sixt, Budget Rent A Car LLC., and Al Sulaiman Rent-A-Car, – collectively account for an estimated 65–70% of total market revenues in 2025. These players compete on fleet size, digital platform capabilities, geographic coverage, and premium service tiers.

|

Company Name |

Key Brand / Service |

Market Position |

Core Strength |

|

Enterprise Holdings, Inc. |

Enterprise Rent-A-Car, Alamo Rent-A-Car, National Car Rental omitted |

Market Leader |

Largest global fleet; corporate accounts |

|

The Hertz Corporation |

Hertz, Dollar, Thrifty, and Firefly |

Market Leader |

AI pricing; premium segment focus |

|

Sixt |

SIXT+ Car Subscription, Car rental deals |

Strong Challenger |

Digital-first; luxury EV fleet expansion |

|

Budget Rent A Car Inc. |

Short Term Rental |

Strong Challenger |

Economy & SME segment dominance |

|

Al Sulaiman Rent-A-Car. |

Flexible Rental Services |

Strong Challenger |

UAE/GCC regional roots; fleet diversification |

Key Company Profiles

Enterprise Holdings, Inc.

Enterprise Holdings, Inc., is the world's largest car rental company with a fleet of 2.3 million vehicles globally, operating in all six GCC member states through company-owned and franchised locations.

- Product Portfolio: Sedan, SUV, luxury, and van categories; corporate fleet leasing; chauffeur services; and subscription models.

- Recent Developments: Introduced 500+ EV units to its UAE fleet.

- Strategic Focus: Deepening corporate account penetration across Saudi giga-projects; expansion of long-term subscription fleet products.

The Hertz Corporation

The Hertz Corporation operates in 160+ countries, with a significant GCC presence through airport-located counters across all six member states.

- Product Portfolio: Hertz Gold Plus Rewards; luxury Prestige Collection; Dollar, Thrifty, and Firefly economy sub-brands.

- Recent Developments: Introduced AI-based dynamic pricing.

- Strategic Focus: Premiumization via Prestige Collection; AI-powered predictive fleet management; contactless check-in deployment.

Sixt

Sixt is a German-origin global mobility provider entering the GCC with flagship locations in Dubai, Riyadh, and Doha, targeting premium and digital-native customers.

- Product Portfolio: SIXT ONE subscription; SIXT+ monthly plans; premium and exotic vehicle categories; chauffeur-on-demand app.

- Recent Developments: Opened its first Saudi Arabia location in 2022; launched an Arabic-language app interface.

- Strategic Focus: Capturing the ultra-premium segment; app-first customer acquisition; EV fleet leadership in urban GCC markets.

Market Concentration Analysis

The GCC car rental market is moderately concentrated, with the top five players holding an estimated 65–70% of total revenue in 2025. This concentration is driven by the high capital intensity of fleet procurement; a top-tier GCC rental operator may hold 10,000–50,000 vehicles, creating significant barriers to entry. Mid-tier regional operators such as Al-Futtaim leverage local relationships and government fleet contracts to maintain their competitive positions.

Fragmentation is most evident at the city or country level, where dozens of independent operators compete for SME and tourist demand. Consolidation is ongoing: three significant M&A transactions involving GCC fleet operators were recorded between 2022 and 2024. Digital aggregators such as Rentalcars.com are accelerating price transparency, compressing margins for smaller operators and reinforcing the competitive advantage of brands with proprietary loyalty programs.

Investment & Growth Opportunities

Fastest Growing Segments

Online booking (~10.8% CAGR), short-term rentals (~10.2% CAGR), and EV fleet subscription services (~14% CAGR) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable opportunity of approximately USD 1.8 Billion in incremental revenue by 2034.

Emerging Market Expansion

Oman and Bahrain collectively represent under-penetrated sub-markets, together accounting for only 13.3% of GCC revenues in 2025. Oman's eco-tourism and adventure travel target of 11 million visitors by 2040 creates a latent demand pool for self-drive rental services. Saudi Arabia's Vision 2030 positions the Kingdom as the single largest greenfield opportunity in the region, with the Saudi Tourism Authority's OTA partnerships now including integrated rental offerings.

Venture and Institutional Investment Trends

- Key investment themes include EV fleet financing, AI-driven fleet optimization platforms, and white-label mobility-as-a-service (MaaS) integration with GCC super-apps.

- Sovereign wealth funds, including Saudi Arabia's PIF and Abu Dhabi's ADQ, are increasingly targeting vertical integration plays, consolidating fleet procurement, digital booking, maintenance, and insurance into single platform companies.

- AI fleet optimization platforms reduce idle asset ratios from an industry average of 32% to approximately 20%, releasing 12% of fleet capital for yield-generating deployments.

Future Market Outlook (2026-2034)

The GCC car rental market is projected to nearly triple from USD 1.81 Billion in 2025 to USD 4.03 Billion by 2034. This reflects a compounded 9.31% annual growth rate, exceeding the global car rental market's projected CAGR of approximately 6.5% over the same period. The GCC's outperformance is anchored in government-driven tourism mega-programs, rising middle-class mobility aspirations, and accelerating digital adoption.

Mobility-as-a-Service (MaaS) platforms integrating rental, ride-hailing, and public transit into unified apps are expected to capture 15–20% of urban mobility spending by 2030. Operators that build API-first architectures and data monetization capabilities will outperform those relying on legacy reservation systems. Fleet electrification, cross-border GCC mobility frameworks, and AI-driven personalized pricing represent the three foundational technology shifts expected to define market leadership through 2034.

Research Methodology

Primary Research

In-depth interviews with senior executives at major GCC car rental operators, fleet procurement managers, tourism ministry representatives, and digital platform leads. Approximately 45 structured interviews were conducted across the six GCC member states during 2024–2025.

Secondary Research

Analysis of company annual reports, GCC Tourism Authority publications, IATA travel demand data, IMF economic forecasts, and GCC government Vision strategy documents. Over 180 secondary sources were reviewed and triangulated to ensure data consistency.

Forecasting Models

A hybrid top-down/bottom-up approach was applied. Market size estimations were triangulated across revenue-based, fleet-size-based, and rental-transaction-volume models. A base-case CAGR of 9.31% reflects consensus analyst estimates validated against reported operator revenue growth rates and regional tourism data.

GCC Car Rental Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Booking Types Covered | Offline Booking, Online Booking |

| Rental Lengths Covered | Short Term, Long Term |

| Vehicle Types Covered | Luxury, Executive, Economy, SUVs, Others |

| Applications Covered | Leisure/Tourism, Business |

| End-Users Covered | Self-Driven, Chauffeur-Driven |

| Companies Covered | Enterprise Holdings Inc., The Hertz Corporation, Sixt , Budget Rent A Car Inc., Al Sulaiman Rent-A-Car. |

| Countries Covered | Saudi Arabia, UAE, Qatar, Bahrain, Kuwait, Oman |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the GCC car rental market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the GCC car rental market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the GCC car rental industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the GCC Car Rental Market Report

The GCC car rental market reached USD 1.81 Billion in 2025. It is projected to reach USD 4.03 Billion by 2034, exhibiting a CAGR of 9.31% during 2026-2034.

The GCC car rental market is expected to grow at a CAGR of 9.31% during the forecast period from 2026 to 2034, supported by rising tourism, expanding expatriate populations, and rapid digital platform adoption.

Online booking dominates with a 71.2% market share in 2025. High smartphone penetration, exceeding 98% in the UAE and Saudi Arabia, combined with the rapid growth of OTA integrations and super-app partnerships, has made digital channels the primary booking avenue across the GCC.

Short-term rentals hold the largest share at 66.3% in 2025. This segment caters primarily to tourists averaging 5–7 day stays and business travelers on 2–3 day itineraries.

Saudi Arabia leads the GCC car rental market with a 42.6% share in 2025. The country's dominance is underpinned by Hajj and Umrah religious travel alongside Vision 2030 tourism targets and large-scale giga-project construction activity in NEOM.

The UAE holds a 24.8% share of the GCC car rental market in 2025. Dubai alone attracted over 9.3 million tourists in H1 2024, and the UAE is the most advanced market for EV fleet adoption and digital booking integration.

Qatar holds a 10.6% share, benefiting from FIFA 2022 legacy infrastructure and growing MICE activity. Kuwait accounts for 8.7%, driven by its large oil-sector expatriate workforce. Oman (7.1%) is an emerging eco-tourism destination.

Key players in the GCC car rental market include Enterprise Holdings, Inc., The Hertz Corporation, Sixt, Budget Rent A Car Inc., and Al Sulaiman Rent-A-Car.

Major growth drivers include rising inbound tourism, expanding expatriate populations, robust business travel demand, digital platform adoption, and government infrastructure investment under Vision 2030 and UAE Net Zero 2050 programs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)