Flexible Intermediate Bulk Container Market Size, Share, Trends and Forecast by Product, End Use, and Region, 2026-2034

Flexible Intermediate Bulk Container Market Size and Share:

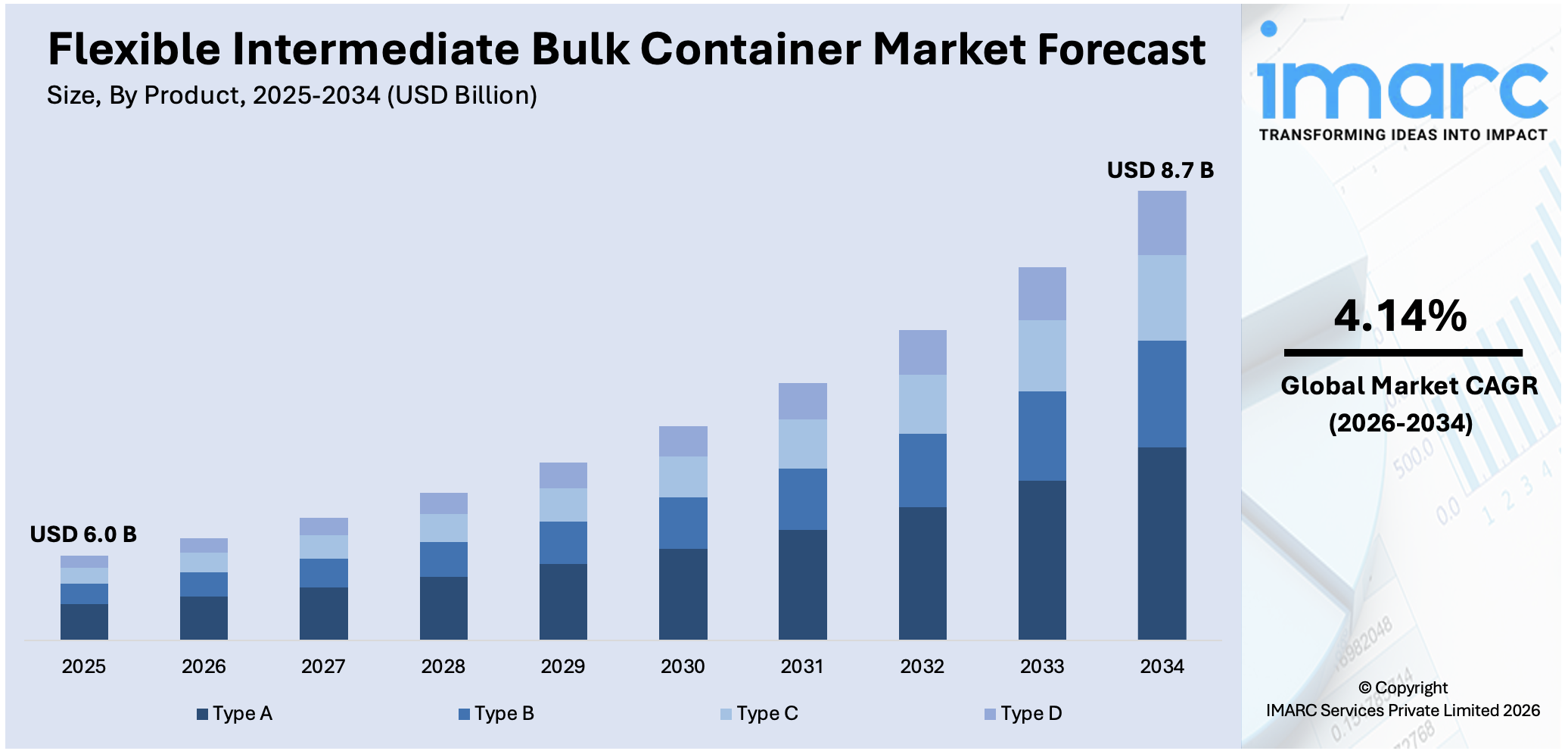

The global flexible intermediate bulk container market size was valued at USD 6.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 8.7 Billion by 2034, exhibiting a CAGR of 4.14% during 2026-2034. North America dominated the market in 2025. The increasing industrialization, growing demand for efficient packaging solutions, the burgeoning growth of the chemical and food industries, and widespread product utilization across the logistics and transportation sectors are some of the key factors contributing to the flexible intermediate bulk container market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 6.0 Billion |

|

Market Forecast in 2034

|

USD 8.7 Billion |

| Market Growth Rate 2026-2034 | 4.14% |

A variety of reasons are driving the market's expansion. Growing demand from the food, chemical, pharmaceutical, and construction industries is a significant driver, since these industries require effective bulk packaging solutions for powders, granules, and semi-solid materials. Increasing international trade and agricultural exports drive adoption even further, since FIBCs lower logistical costs and facilitate large-scale handling. Their lightweight, robust, and reusable design saves money over rigid containers, while material advancements improve safety and strength. Furthermore, the worldwide emphasis on sustainability promotes eco-friendly packaging by pushing the use of recyclable and biodegradable bulk bags. These features make FIBCs the chosen alternative for companies seeking efficiency, cost savings, and environmentally responsible packaging in global supply chains.

To get more information on this market Request Sample

In the United States, one of the strongest flexible intermediate bulk container market trends is rising demand from the food and pharmaceutical industries, where cleanliness, safety, and regulatory compliance are key. Manufacturers are increasingly working on manufacturing food- and pharmaceutical-grade FIBCs that exceed FDA and ISO requirements, including dustproofing, anti-static characteristics, and contamination resistance. This trend is being driven by expanding packaged food consumption, increased export volumes, and stronger quality standards in pharmaceutical logistics. As a result, suppliers are investing in innovative materials and manufacturing processes to serve these high-value end-use industries.

Flexible Intermediate Bulk Container Market Trends:

Increased industrialization

Industries such as chemicals, agriculture, construction, and pharmaceuticals are experiencing rapid growth, leading to a higher demand for bulk packaging solutions. FIBCs, known for their ability to handle large quantities of materials efficiently, are increasingly favored in these sectors. Their adaptability in transporting a broad variety of products, from large granules to fine powders, makes them an essential component in these sectors. Moreover, the ongoing industrial expansion in emerging economies, particularly in the Asia Pacific and Latin America, is further propelling the demand for FIBCs. According to the National Statistics Office of Vietnam, the Industrial Production Index (IIP) increased by 7.6% in the first quarter of 2025, compared to a 5.9% growth in the same period in 2024. These regions are seeing a boom in manufacturing activities, which, in turn, is boosting the need for reliable and cost-effective bulk packaging solutions, thus supporting the flexible intermediate bulk container market growth.

Rise in demand for efficient packaging solutions

The growing need for more efficient and sustainable packaging solutions is acting as another significant growth-inducing factor. FIBCs offer significant advantages over traditional packaging methods, such as rigid containers and smaller sacks. They provide superior protection for goods, reduce packaging waste, and optimize storage and transportation efficiency. This efficiency is particularly crucial in industries where bulk handling and transportation are vital. As highlighted in a recent industry report, a chemical manufacturer that transitioned from using 25 kg paper bags to FIBCs for raw material handling experienced a 40% reduction in packaging costs and simultaneously cut labor requirements by 50%. Moreover, FIBCs minimize environmental impact and contribute to lower transportation costs because they are lightweight, collapsible, and reusable. Additionally, continuous advancements in FIBC design and manufacturing, such as the use of advanced materials and enhanced safety features, are further driving their adoption. These innovations comply with stringent safety and regulatory standards, thus bolstering the flexible intermediate bulk container demand in various industries seeking reliable and efficient packaging solutions.

Expansion of the logistics and transportation sectors

The increasing complexity of supply chains and the need for efficient material handling solutions have led to a higher demand for FIBCs. These containers are ideal for transporting large volumes of goods safely and efficiently. They are designed to withstand rigorous handling and environmental conditions, ensuring the safe delivery of products. The rise of e-commerce and the globalization of trade have further amplified the need for effective bulk packaging solutions. As reported, global B2C ecommerce revenue is expected to grow to USD 5.5 trillion by 2027 at a steady 14.4% compound annual growth rate. FIBCs offer the flexibility and durability required to meet the demands of modern logistics operations. Besides this, the trend towards automation in logistics and warehousing has also contributed to the growing adoption of FIBCs. Their compatibility with automated handling systems enhances operational efficiency and reduces labor costs, making them an attractive option for logistics and transportation companies.

Flexible Intermediate Bulk Container Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global flexible intermediate bulk container market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on product and end use industry.

Analysis by Product:

- Type A

- Type B

- Type C

- Type D

Type A stood as the largest product in 2025. Based on the flexible intermediate bulk container market research report, Type A dominated the market due to its widespread use in various non-flammable applications. These standard, non-conductive FIBCs are cost-effective and suitable for transporting and storing dry, non-hazardous materials such as grains, seeds, and powders. Their simplicity in design and lower manufacturing costs compared to more specialized FIBCs, like Type B, C, and D, make them highly attractive to industries with basic bulk packaging needs. Their popularity is further enhanced by their versatility and efficiency in handling large volumes of materials. In addition to this, the extensive availability and ease of production of Type A product variants are boosting the flexible intermediate bulk container market revenue.

Analysis by End Use Industry:

Access the comprehensive market breakdown Request Sample

- Food

- Chemicals

- Pharmaceuticals

- Others

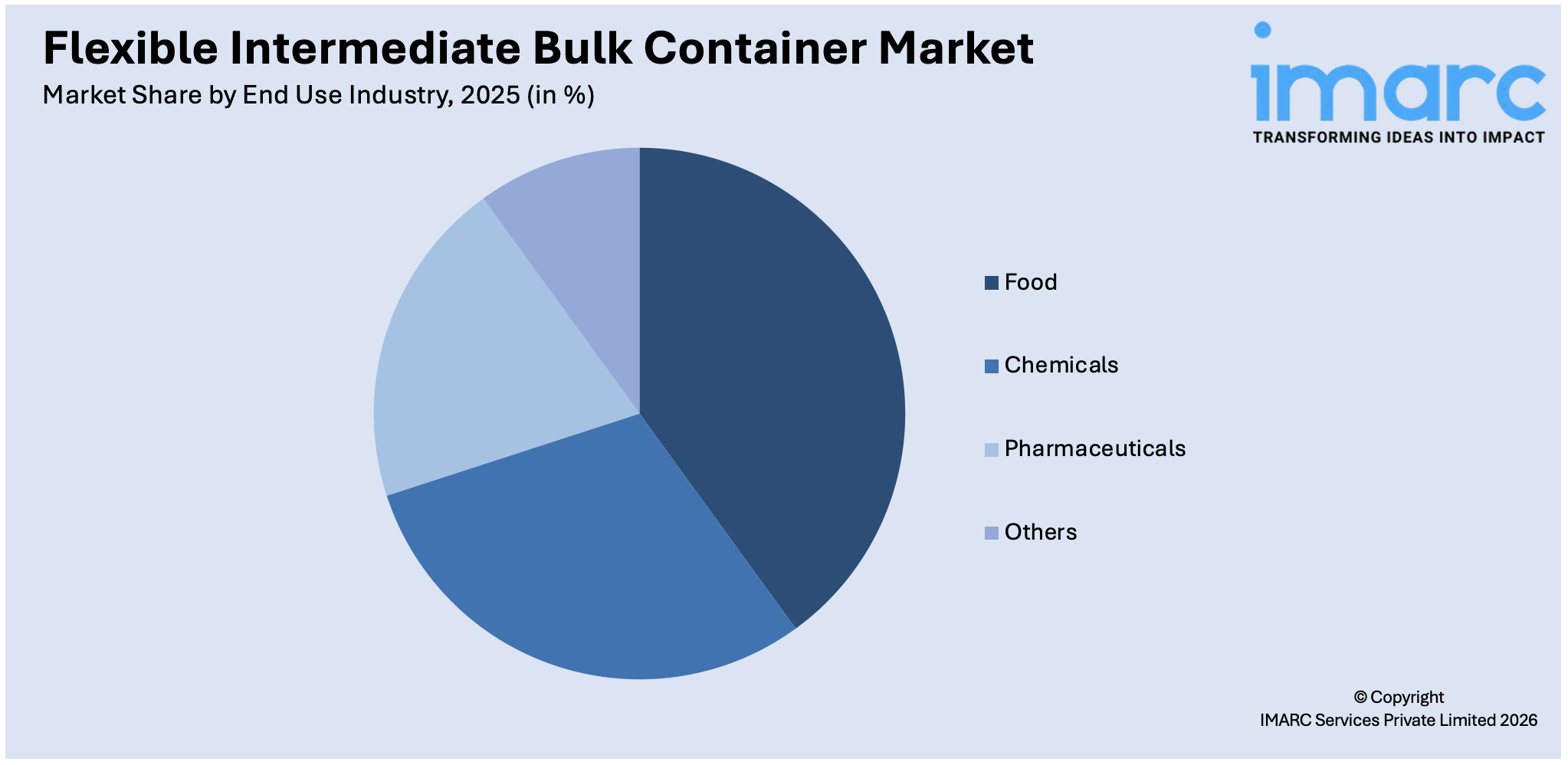

Food led the market in 2025. The increasing demand from the food industry, where these products are used for efficient and hygienic bulk packaging solutions, is impelling the flexible intermediate bulk container market value. FIBCs are ideal for transporting and storing large quantities of food products such as grains, flour, sugar, and spices, providing excellent protection against contamination and moisture. Their cost-effectiveness, reusability, and ability to preserve product quality make them a preferred choice in the food sector. Furthermore, stringent food safety regulations are also driving the adoption of high-quality, food-grade FIBCs that meet these standards. Besides this, the increasing global population and rising food trade are presenting lucrative opportunities for market expansion.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share. The flexible intermediate bulk container market forecast revealed North America as the leading region due to its robust industrial base, particularly in the chemical, food, and pharmaceutical sectors. Concurrent with this, advanced manufacturing technologies and stringent regulatory standards in the region, leading to the introduction of high-quality FIBCs are further strengthening the market growth. Additionally, the presence of key market players and extensive distribution networks, combined with a strong logistics and transportation infrastructure in North America, is increasing the reliance on FIBCs for bulk material handling. Moreover, rising environmental awareness and the shift towards sustainable packaging solutions, spurring the demand for reusable and durable FIBCs, are positively impacting the flexible intermediate bulk container market outlook.

Key Regional Takeaways:

United States Flexible Intermediate Bulk Container Market Analysis

The United States flexible intermediate bulk container (FIBC) market is experiencing steady growth, driven by the increasing demand for efficient and sustainable packaging in the agricultural and chemical sectors. The emphasis on reducing packaging waste and enhancing logistics efficiency is encouraging the adoption of FIBCs due to their lightweight and space-saving characteristics. According to a 2025 report, over half, about 54%, of Americans reported deliberately choosing products with sustainable packaging in the past six months, highlighting a consumer-driven push toward eco-friendly solutions. The market is further supported by the rise in e-commerce and third-party logistics, which favor bulk packaging solutions that offer durability and ease of handling. Technological advancements in packaging design, including UV-resistant and moisture-proof FIBCs, are expanding application scope. Moreover, heightened regulatory focus on workplace safety has led to greater preference for FIBCs that meet rigorous safety standards. Increased industrial output across various verticals is enhancing the utility of FIBCs for material storage and intra-plant transfers. Additionally, sustainability initiatives promoting the use of recyclable and reusable materials are driving innovation within the market. Growth in export-oriented industries requiring cost-effective bulk shipping further underlines the rising demand for these containers.

Europe Flexible Intermediate Bulk Container Market Analysis

The flexible intermediate bulk container (FIBC) market in Europe is expanding due to the growing importance of automation and operational efficiency in industrial packaging systems. European industries are increasingly integrating bulk containers into automated material handling systems to streamline production and minimize labor costs. According to market projections, the Europe end-of-line packaging market is expected to grow from USD 2.92 Billion in 2025 to USD 4.46 Billion by 2034, at a CAGR of 4.76% (2025–2034), reflecting rising investments in packaging technology and industrial automation. The market is also benefiting from stricter environmental regulations that promote the use of reusable and recyclable packaging materials, which align with the sustainable nature of FIBCs. Advancements in manufacturing standards and quality control are boosting the production of high-performance FIBCs for hazardous materials. The pharmaceutical and specialty chemical sectors are boosting demand for contamination-resistant packaging. Smart packaging solutions, like RFID-enabled FIBCs, are being adopted for traceability and inventory management.

Asia Pacific Flexible Intermediate Bulk Container Market Analysis

The Asia Pacific flexible intermediate bulk container (FIBC) market is witnessing rapid growth, supported by surging industrial production and expanding intra-regional trade. In January 2025, the India’s IIP recorded a 5.0% YoY increase, up from 3.5% in December 2024. The region’s growing construction sector is fueling the demand for heavy-duty packaging to handle sand, gravel, and other bulk materials efficiently. Accelerated urbanization and infrastructure development are further amplifying this need. FIBCs are increasingly favored for their high load-bearing capacity and versatility, especially in the mining and ceramics industries. The growing bulk transportation of powdered chemicals and resins is increasing demand for anti-static and conductive FIBCs. Local manufacturers are using weaving technology to create durable, cost-effective containers, while industrial parks and logistics hubs encourage investment in bulk handling systems.

Latin America Flexible Intermediate Bulk Container Market Analysis

The Latin American flexible intermediate bulk container (FIBC) market is expanding as regional industries seek efficient and durable packaging solutions for handling granular and powdered materials. According to provisional data, Latin America’s containerized trade volumes rose by 5% in Q1 2025 compared to the same period in 2024, illustrating the increasing demand for large-capacity export packaging such as FIBCs. Growth in the region’s agro-industrial output is fostering greater use of FIBCs for the bulk movement and storage of agricultural produce and fertilizers. Rising export activities, particularly in raw materials, are also contributing to market demand as industries opt for scalable, high-capacity containers that ensure product integrity during long-distance transportation. Investments in domestic manufacturing facilities and increasing focus on reducing logistics costs are further enhancing the relevance of FIBCs.

Middle East and Africa Flexible Intermediate Bulk Container Market Analysis

The flexible intermediate bulk container (FIBC) market in the Middle East and Africa is growing due to the rising demand for efficient dry bulk packaging across the petrochemical and cement sectors. A recent report shows that Saudi Arabia’s crude oil exports rose to 6.19 Million barrels per day in May 2025, marking a 1.19% year-on-year increase, an indicator of the region’s expanding industrial activity that directly impacts bulk packaging needs. Regional infrastructure development and expansion in industrial activity are driving the need for reliable containers that can withstand harsh handling and climatic conditions. FIBCs are gaining traction for their suitability in transporting high-volume, fine-grained materials over long distances. Improved trade connectivity and storage optimization in arid environments are increasing the use of bulk containers, particularly those with UV-resistant and moisture-controlled features.

Competitive Landscape:

The flexible intermediate bulk container market is seeing steady activity around product innovation, with manufacturers focusing on bags made from recyclable and sustainable materials, along with designs that improve safety and durability. Companies are investing in research to develop features like UV resistance, anti-static performance, moisture barriers, and smart tracking. Partnerships and collaborations occur, but they are less frequent compared to new product launches and R&D efforts. Government initiatives and funding are rarely highlighted in this space. At present, the most common practices are product development and research-driven improvements, reflecting the industry’s shift toward sustainability, efficiency, and tailored solutions for sectors like food, chemicals, and construction.

The report provides a comprehensive analysis of the competitive landscape in the flexible intermediate bulk container market with detailed profiles of all major companies, including:

- Bag Corp.

- Berry Global Inc.

- Bulk Lift International LLC

- Global-Pak Inc.

- Greif Inc.

- Isbir Sentetik Dokuma Sanayi A.S.

- Langston Companies Inc.

- LC Packaging International BV

- Plastipak Group

- Rishi FIBC Solutions PVT. Ltd.

Latest News and Developments:

- April 2025: RDA Bulk Packaging inaugurated a new factory in India to produce FIBCs with expanded capacity and advanced technology. The company introduced bags with 40% recycled content, meeting ISO standards and UK Plastic Packaging Tax compliance. The facility aimed to boost delivery speed and ensure sustainable, eco-friendly manufacturing practices.

- April 2024: Packem Umasree, a joint venture between Brazil’s Packem S.A. and India’s Umasree Texplast, made history as the first company globally to produce 100% sustainable FIBCs using recycled PET from used bottles. The company celebrated this milestone by inaugurating its first Indian plant near Ahmedabad in April 2024. The new facility highlights their commitment to eco-friendly packaging solutions.

Flexible Intermediate Bulk Container Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products | Type A, Type B, Type C, Type D |

| End Use Industries | Food, Chemicals, Pharmaceuticals, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bag Corp., Berry Global Inc., Bulk Lift International LLC, Global-Pak Inc., Greif Inc., Isbir Sentetik Dokuma Sanayi A.S., Langston Companies Inc., LC Packaging International BV, Plastipak Group, Rishi FIBC Solutions PVT. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the flexible intermediate bulk container market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global flexible intermediate bulk container market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the flexible intermediate bulk container industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Flexible Intermediate Bulk Container Market Report

The flexible intermediate bulk container market was valued at USD 6.0 Billion in 2025.

The flexible intermediate bulk container market is projected to exhibit a CAGR of 4.14% during 2026-2034, reaching a value of USD 8.7 Billion by 2034.

The flexible intermediate bulk container (FIBC) market is driven by growing demand from the food, chemical, and pharmaceutical industries, rising agricultural exports, and increasing international trade. Their cost-effectiveness, reusability, and efficiency in handling bulk materials, along with sustainability initiatives promoting lightweight, eco-friendly packaging, further support widespread adoption across industries worldwide.

North America dominated the flexible intermediate bulk container market in 2025 due to strong industrial growth, extensive agriculture exports, rising demand for bulk packaging solutions, and well-established logistics infrastructure supporting large-scale commodity transport.

Some of the major players in the flexible intermediate bulk container market include Bag Corp., Berry Global Inc., Bulk Lift International LLC, Global-Pak Inc., Greif Inc., Isbir Sentetik Dokuma Sanayi A.S., Langston Companies Inc., LC Packaging International BV, Plastipak Group, Rishi FIBC Solutions PVT. Ltd., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)