Fire Fighting Chemicals Market Size, Share, Trends, and Forecast by Type, Chemicals, Application, and Region, 2025-2033

Fire Fighting Chemicals Market Size and Share:

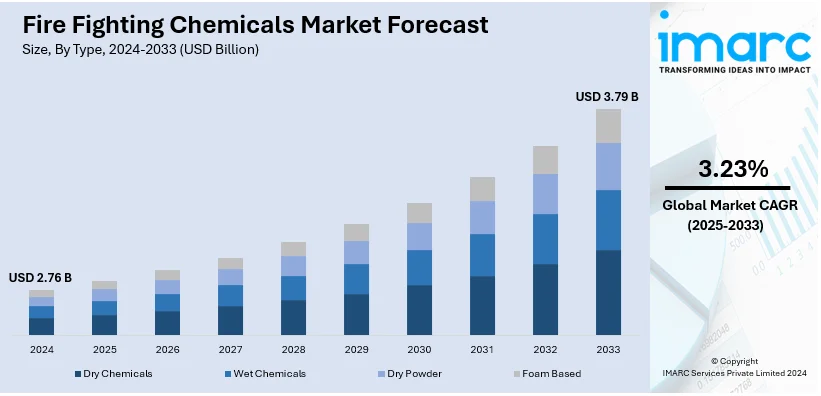

The global fire fighting chemicals market size was valued at USD 2.76 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 3.79 Billion by 2033, exhibiting a CAGR of 3.23% from 2025-2033. Europe currently dominates the market, holding a market share of over 30.9% in 2024. The fire fighting chemicals market share is expanding, driven by stringent fire safety regulations, increasing industrialization, and growing demand for advanced fire suppression solutions across various industries.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024 |

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 2.76 Billion |

| Market Forecast in 2033 | USD 3.79 Billion |

| Market Growth Rate 2025-2033 |

3.23%

|

The global fire fighting chemicals market is driven by stringent fire safety regulations mandating effective suppression solutions. In addition, ongoing technological advancements improve efficiency and environmental compliance, aiding the market growth. For instance, Carrier Global at the end of the year agreed to pay $730 million over per- and polyfluoroalkyl substances (PFAS), claims associated with the fire protection unit that used these chemicals in firefighting foam products, which shows the industry’s move toward sustainable solutions. Moreover, the growing construction activities, particularly in high-risk zones, and the expanding aerospace and automotive sectors are boosting the market demand. Besides this, the increasing awareness about fire safety in residential and commercial spaces is fueling the market expansion. Furthermore, rapid development in the oil, gas, and chemical industries, which are prone to fire hazards, underscores the need for specialized fire fighting chemicals, thus catalyzing the market growth.

The fire fighting chemicals market in the United States holds a share of 77.20%. The demand in the region is driven by rising investments in advanced fire protection infrastructure, especially in smart buildings. Additionally, the increasing prevalence of wildfires across the country has heightened the demand for effective fire retardants, which is impelling the market growth. Concurrently, the surge in defense and military applications, which require specialized fire suppression systems, is contributing to market expansion. For example, the US military is also dealing with pollution from PFAS, widely known as ‘forever chemicals’, which are present in almost 80% of military facilities across the United States. Moreover, the enhanced government funding for wildfire management and public safety initiatives is providing an impetus to the market. Apart from this, continuous advancements in eco-friendly and biodegradable fire fighting chemicals align with environmental regulations, while innovations in foam-based solutions and industrial safety protocols, thereby propelling the market forward.

Fire Fighting Chemicals Market Trends:

Technological Advancements in Fire Suppression Solutions

The advancement in fire suppression technologies forms one of the key drivers of the market growth. Further, the growing rate in material science, chemistry, and engineering in the development of new fire fighting chemicals is also enhancing the effectiveness of fire fighting chemicals with low ecological impact. In addition to this, the rising popularity of water-based fire fighting chemicals across numerous sectors due to their efficiency in cooling and extinguishing fires without the formation of toxic by-products is boosting the market growth. There is a growing adoption of smart fire suppression systems that include features such as sensors, actuators, and real-time data analytics. The American Chemistry Council projects that chemical production will grow by 3.4% in 2024 and 3.5% in 2025, reflecting the increasing potential for innovative chemical solutions in firefighting.

Growing Awareness About Industrial Hazards and Risk Mitigation

Additionally, the expansion of industries across the globe and rising incidences of potential fire hazards, including flammable liquids, gases, and electrical equipment, are catalyzing the demand for firefighting chemicals. According to an industrial report, the global construction output is expected to increase from USD 10.2 Trillion in 2020 to USD 15.2 Trillion by 2030, further amplifying the need for effective fire suppression solutions to safeguard assets and comply with safety regulations. Apart from this, the growing consciousness among companies about the benefits of an initiative-taking approach to fire safety is driving the demand for efficient fire fighting chemicals to save human lives, protect valuable assets, and prevent production disruptions. Furthermore, the partnerships between the fire fighting chemical manufacturers and industrial companies to provide the solution that meets the risk levels of the companies are also supporting the market growth.

Implementation of Fire Safety Regulations and Standards

The implementation of various stringent regulations and standards across industries and regions is contributing to market growth. Additionally, the government and other regulatory agencies are undertaking several measures to educate the public and various industries including manufacturing, energy, and transportation. For example, International Fire Safety Standards - Common Principles (IFSS-CP) indicates key performance-based principles in design, construction, occupancy, and ongoing management by fire safety engineering. Moreover, the Regulatory Reform (Fire Safety) Order 2005 is the main piece of legislation in place for the control of fire safety in non-domestic premises, including transport. These regulations require the adoption of modern fire protection systems that would involve, fire fighting chemicals for the protection of people, property, and the environment. Besides this, several leading companies are consistently pursuing the development of new fire fighting chemicals with greater extinguishing efficiency and less harm to the environment.

Fire Fighting Chemicals Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global fire fighting chemicals market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on type, chemicals, and application.

Analysis by Type:

- Dry Chemicals

- Wet Chemicals

- Dry Powder

- Foam Based

Dry chemicals led the market with around 39.2% of the market share in 2024. This segment is growing due to its compatibility with a wide range of fire classes. Dry chemical agents are highly effective in combating class A, B, and C fires, which involve ordinary combustibles, flammable liquids, and electrical equipment. Apart from this, they possess a non-conductive nature, which makes them suitable for extinguishing electrical fires. They help form a barrier that prevents the flow of electricity and ensures the safe suppression of electrical equipment without the risk of electrocution. Furthermore, dry chemicals leave minimal residue after extinguishing fires, which helps minimize the cleanup process and reduces the potential damage caused by the suppression. Moreover, these chemicals are easy to store and transport due to their solid or powder form.

Analysis by Chemicals:

- Monoammonium Phosphate

- Halon

- Carbon Dioxide

- Potassium Bicarbonate

- Potassium Citrate

- Sodium Chloride

- Others

Monoammonium phosphate led the market with around 32.4% of the market share in 2024. It is a dry chemical compound widely used in fire extinguishers due to its effective suppression capabilities across multiple fire classes. It offers versatility and helps form a barrier that separates fuel and oxygen and prevents combustion. It is widely used in portable fire extinguishers, monoammonium phosphate is preferred across residential, commercial, and industrial sectors due to its affordability, ease of application, and proven reliability in emergency fire situations. Additionally, its non-conductive properties make it especially suitable for combating electrical fires, enhancing its appeal in modern infrastructure. Besides, compatibility with a variety of fire suppression systems and ease of storage enhance its continued demand in a wide range of applications.

Analysis by Application:

- Portable Fire Extinguishers

- Automatic Fire Sprinklers

- Fire Retardant Bulkhead

- Fire Dampers

- Others

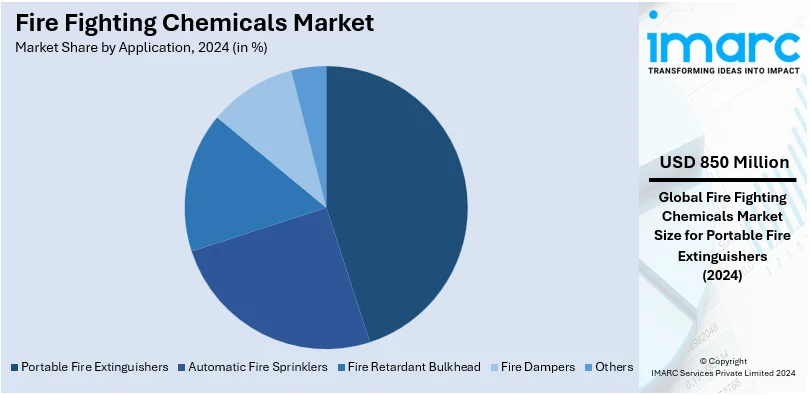

Portable fire extinguishers led the market with around 30.7% of the market share in 2024. This segment is expanding as they provide immediate access to fire suppression tools. Additionally, their compact size and ease of deployment allow for swift action in the initial stages of a fire outbreak and aid in minimizing potential damage and enhancing overall safety. Apart from this, they are easier to produce, install, and maintain than the large, fixed fire suppression systems, and are less costly. Furthermore, the user-friendly design includes clear operating instructions and visual indicators, which promote the adoption of portable fire extinguishers across residential and commercial sectors. Moreover, many authorities and safety standards require the presence of portable fire extinguishers in commercial buildings, public spaces, and residential properties.

Analysis by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, Europe accounted for the largest market share of over 30.9%. The demand in the region is increasing due to high fire safety standards and preventive measures to improve fire safety. As the leading economies like Germany, the United Kingdom (UK), and France are leading the innovation, the region has developed industrial and commercial segments that need reliable fire extinguishing systems. Moreover, European countries have led sustainable practices, which have triggered the use of eco-friendly and biodegradable fire fighting chemicals to match the region’s environmental standards. Also, a growing concern with fire safety across residential and commercial spaces has also fostered growth for the market. Furthermore, the construction, automotive and aerospace industries in the region require the best of fire safety solutions. Apart from this, owing to continuous innovation in technology and increased support from the regulatory authorities, is significantly contributing to the market expansion.

Key Regional Takeaways:

North America Fire Fighting Chemicals Market Analysis

The fire fighting chemicals market in North America is growing due to the presence of a robust infrastructure and advanced manufacturing capabilities in the region. The region has well-established chemical production facilities, which enable the timely and efficient creation of firefighting chemicals in massive quantities. They further allow the manufacturers to respond swiftly to market demands and provide a steady supply of products. Apart from this, the region has a robust network of research institutions, universities, and private companies dedicated to advancing firefighting technology. Furthermore, the implementation of rigorous safety protocols by the governing authorities and regulatory bodies in the region promotes the use of high-quality, certified firefighting chemicals. For instance, The U.S. Environmental Working Group notes that better alternatives to Aqueous Film-Forming Foam (AFFF) are available. Some of the U.S. states have already outlawed PFAS-based foams such as AFFF. The National Defense Authorization Act requires all fire departments under the Department of Defense to discontinue using AFFF and AR-AFFF by 2024. Moreover, the efficient organization infrastructure in North America ensures the timely delivery of firefighting chemicals to various end-users, such as industrial facilities, commercial buildings, and residential areas.

United States Fire Fighting Chemicals Market Analysis

Manufacturing in the United States is a significant contributor to the fire fighting chemicals market. According to the National Institute of Standards and Technology (NIST), manufacturing contributed USD 2.3 Trillion to the United States GDP in 2023 and made up 10.2% of the GDP. Key industries for this growth would include chemicals, food and beverages, and electronics, many of which manage hazardous chemicals, flammable substances, and large machinery. As those industries grow, it is essential to have state-of-the-art fire suppression systems and chemicals to safeguard workers and assets. The complexity of the operations and safety regulations create demand for fire fighting chemicals, providing a solution in reducing risk, ensuring business continuation, and mitigating loss of assets. Overall, robust growth in the U.S. manufacturing sector has increased the demand for fire fighting chemicals.

Europe Fire Fighting Chemicals Market Analysis

The retail sector is a significant contributor to the Europe fire fighting chemicals market, for the economy of the region. With 11.5% of the value added in the EU, retail is not only the largest industrial ecosystem but also the biggest private employer, providing nearly 30 million people with jobs, as per industry reports. According to the European Environment Agency (EEA), there are 5.5 million enterprises, 99% of which are SMEs, making up this sector. In general, retailing, including warehousing, distribution centers, and retailing businesses, have flammable materials and electrical equipment along with high stock inventories and thus expose them to fire hazards. As the retail business grows and progresses, the need for strong fire fighting chemicals and other effective fire safety solutions grows. Regulations that are growingly strict and focus on the protection of not just assets but also personnel push the need across the retail industry in Europe for advanced fire suppression solutions.

Asia Pacific Fire Fighting Chemicals Market Analysis

The Asia Pacific fire fighting chemicals market is likely to see significant infrastructure development initiatives, including the "Parvatmala Pariyojana" National Ropeways Development Programme by the Government of India. The project encompasses more than 200 projects, with a total allocation of INR 1.25 lakh crore (USD 14.77 Billion) for the next five years and is likely to add connectivity in the challenging terrains, which is expected to improve economic activity, increase demand for fire safety measures across the region. The Union Cabinet's approval of INR 4,406 Crore (USD 0.52 Billion) for the construction of 2,280 km of roads in the border areas of Punjab and Rajasthan in 2024 will further strengthen infrastructure development, particularly in remote and high-risk areas. These developments will increase the demand for advanced fire fighting chemicals, as the fire safety regulations become more stringent and the need for protecting valuable assets and personnel in newly developed areas rises.

Latin America Fire Fighting Chemicals Market Analysis

Latin America fire fighting chemicals market is going to be developed with the development of the region's energy scenario. According to the International Energy Agency, Latin America and the Caribbean have accounted for 5% of global energy-related greenhouse gas (GHG) emissions since 1971, while showcasing 9% of the global GDP. The region is poised to become a net exporter of crude oil and coal, and it is already a net importer of oil products and natural gas; this makes energy infrastructure paramount. Expanding energy production and extraction boosts the demand for fire safety solutions, including fire fighting chemicals. This calls for advanced fire suppression systems, which can eliminate the risks caused by flammable materials, industrial processes, and transport. Moreover, increasing regulatory norms on fire safety in the energy sector are accelerating demand for fire fighting chemicals in Latin America.

Middle East and Africa Fire Fighting Chemicals Market Analysis

The Middle East and Africa fire fighting chemicals market is growing at a significant rate, due to the growth of the aviation sector in the region. According to reports, Africa currently accounts for only 2% of global air passengers, but it has huge growth potential. In 2023, Africa recorded an impressive 39.3% growth in international Revenue Passenger Kilometers (RPK) compared to the previous year, indicating rising air traffic and capacity. This increase in air travel means more demand for fire safety solutions such as fire fighting chemicals, specifically in airports, aviation facilities, and other structures. The demand for sophisticated fire suppression technologies in the region is expected to be higher with increasing growth in its aviation industry to provide safety to passengers, crew, and assets. Additionally, the increasing demand for fire safety in industries such as aviation, manufacturing, and energy further fuels the demand for effective fire fighting chemicals across the Middle East and Africa.

Competitive Landscape:

Manufacturers are actively engaged in research and development (R&D) to create new chemical products that are effective in suppressing fires and have minimal adverse effects on the environment. Furthermore, they are expanding their product range and providing specific firefighting chemicals for industries and different classes of fire and uses for industrial, commercial, and residential buildings. Besides this, they are conducting awareness creation among the end-users and the emergency response team in the use of their products. Also, the manufacturing procedures of several top companies are environmentally friendly; the use of biodegradable chemicals in the industry is being researched, and most companies are striving to reduce their carbon footprint in an attempt to meet global sustainability goals and enhance environmental health.

The report provides a comprehensive analysis of the competitive landscape in the fire fighting chemicals market with detailed profiles of all major companies, including:

- Angus Fire

- DIC Corporation

- Fire Safety Devices Pvt. Ltd.

- Foamtech Antifire Company

- Johnson Controls International plc

- Linde plc

- Orchidee Europe

- Perimeter Solutions

- Safequip Pty Ltd

- Solvay S.A

Latest News and Developments:

- In August 2024: Environmentalists raised alarm about a massive leak of PFAS-containing fire fighting foam that took place at the Brunswick Executive Airport in Maine. Water testing afterward showed levels of PFAS that fell below Maine state safety limits. However, it reignited pressure on the government for initiative-taking management of PFAS and mitigation.

- In September 2024: PPG has revealed the introduction of PPG Steelguard 951 epoxy intumescent fire protection coating in the United States. This distinctive product is designed for sophisticated manufacturing environments.

- In October 2024: Siemens declared the purchase of Danfoss Fire Safety, a company focused on fire suppression technology and a division of the Denmark-based Danfoss Group. This acquisition is anticipated to boost growth and support the transition to a sustainable fire safety portfolio.

- In April 2024: Summit Fire & Security LLC declared the acquisition of West Fire Extinguisher Service, Inc., which specializes in fire extinguishers, fire dampers, and many other fire protection systems.

- In October 2024: Elementis announced its expansion of specialty additives into plastic compounding applications with the launch of CHARGUARD™ organoclay-based fire-retardant synergists. CHARGUARD™ flame retardant synergists are formulated to improve the anti-drip and char development characteristics of non-halogenated fire retardants.

Fire Fighting Chemicals Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Dry Chemicals, Wet Chemicals, Dry Powder, Foam Based |

| Chemicals Covered | Monoammonium Phosphate, Halon, Carbon Dioxide, Potassium Bicarbonate, Potassium Citrate, Sodium Chloride, Others |

| Applications Covered | Portable Fire Extinguishers, Automatic Fire Sprinklers, Fire Retardant Bulkhead, Fire Dampers, Others |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Angus Fire, DIC Corporation, Fire Safety Devices Pvt. Ltd., Foamtech Antifire Company, Johnson Controls International plc, Linde plc, Orchidee Europe, Perimeter Solutions, Safequip Pty Ltd, Solvay S.A, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the fire fighting chemicals market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global fire fighting chemicals market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the fire fighting chemicals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

Firefighting chemicals are specialized substances used to suppress, control, or extinguish fires. These chemicals enhance the effectiveness of firefighting efforts by interrupting the combustion process, cooling the fire, or creating barriers to prevent its spread. Common types include foams, powders, and gaseous agents, tailored for specific fire types and environments.

The fire fighting chemicals market was valued at USD 2.76 Billion in 2024.

IMARC estimates the global fire fighting chemicals market to exhibit a CAGR of 3.23% during 2025-2033.

Key factors driving the global firefighting chemicals market include rising urbanization and industrialization, stringent fire safety regulations, increasing awareness of fire hazards, advancements in chemical formulations, growing demand from sectors such as oil and gas, manufacturing, and aviation, ensuring improved fire protection solutions.

In 2024, dry chemicals represented the largest segment by type, due to their ability to quickly suppress fires involving flammable liquids, gases, and electrical sources. Their cost-effectiveness, ease of storage, and rapid deployment make them the preferred choice across multiple industries, including industrial, automotive, and aviation sectors.

Monoammonium phosphate leads the market by chemicals, particularly for tackling fires involving ordinary combustibles and flammable liquids. Its ability to form a stable, non-flammable barrier on burning materials makes it highly effective and widely used across industrial and commercial sectors.

The portable fire extinguishers are the leading segment by application, driven by Their compact size, ease of use, and accessibility in various environments, including homes, offices, and factories. They are crucial for providing immediate fire response, especially in small-scale or localized fires, making them a convenient option globally.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein Europe currently dominates the global market.

Some of the major players in the global fire fighting chemicals market include Angus Fire, DIC Corporation, Fire Safety Devices Pvt. Ltd., Foamtech Antifire Company, Johnson Controls International plc, Linde plc, Orchidee Europe, Perimeter Solutions, Safequip Pty Ltd, Solvay S.A, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)