Europe Molecular Diagnostics Market Size, Share, Trends and Forecast by Product, Technology, Application, End User, and Country, 2026-2034

Europe Molecular Diagnostics Market Summary:

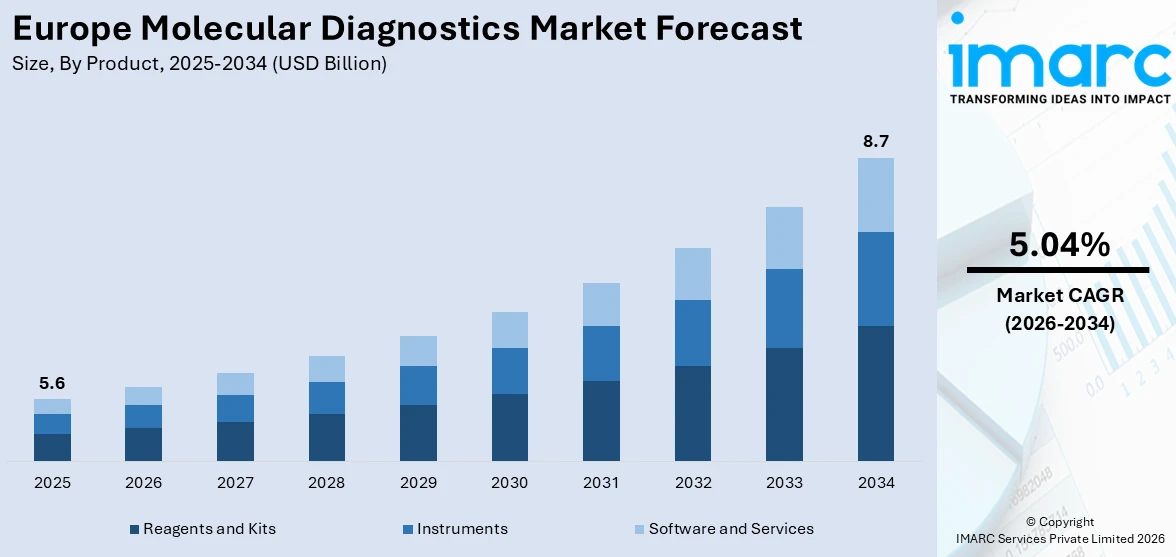

The Europe molecular diagnostics market size was valued at USD 5.6 Billion in 2025 and is projected to reach USD 8.7 Billion by 2034, growing at a compound annual growth rate of 5.04% from 2026 to 2034.

The Europe molecular diagnostics market is experiencing sustained growth driven by an aging population, rising prevalence of infectious diseases and cancer, and rapid adoption of precision medicine approaches. Increasing government investments in healthcare modernization, expanding point-of-care (POC) testing infrastructure, and the growing integration of next-generation sequencing in routine clinical workflows are strengthening diagnostic capabilities. Advancements in liquid biopsy technologies, digital polymerase chain reaction (PCR) platforms, and AI-powered bioinformatics are further enhancing diagnostic accuracy, contributing to the Europe molecular diagnostics market share.

Key Takeaways and Insights:

- By Product: Reagents and kits dominate the market with a share of 55% in 2025, driven by their indispensable role in high-throughput laboratory workflows, recurring procurement cycles across hospitals and diagnostic laboratories, and broad applicability across PCR, sequencing, and isothermal amplification platforms.

- By Technology: Polymerase chain reactions (PCR) lead the market with a share of 38% in 2025, owing to its established clinical utility in detecting a wide range of infectious diseases, rapid turnaround capabilities, and continuous technological refinements, including multiplex and digital PCR innovations.

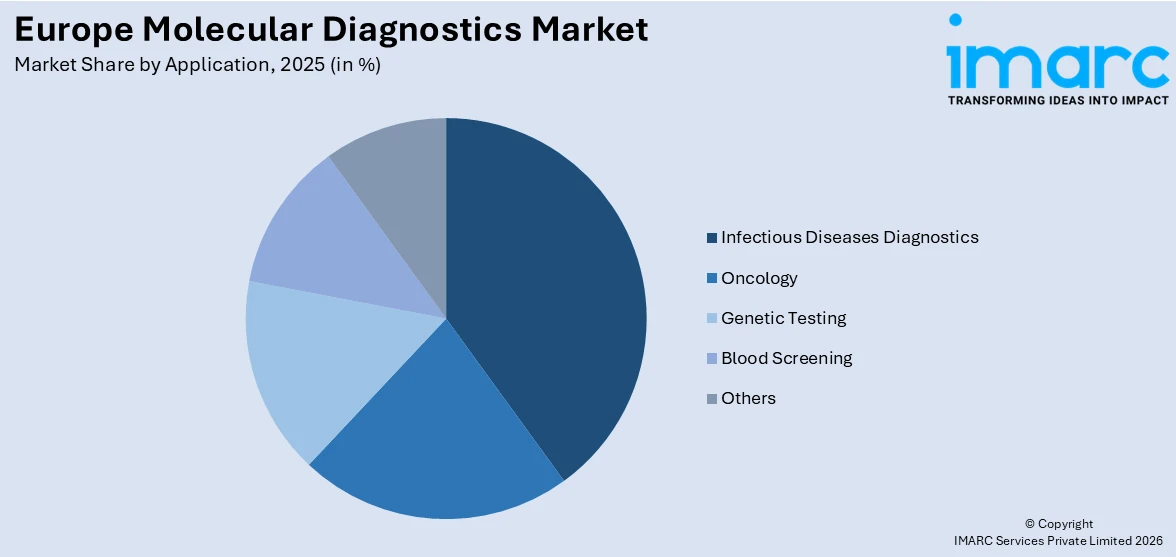

- By Application: Infectious diseases diagnostics represents the largest segment with a market share of 46% in 2025, supported by sustained demand for rapid pathogen detection, expanded antimicrobial resistance surveillance mandates, and the growing deployment of syndromic multiplex panels across European healthcare systems.

- By End User: Hospitals dominate the market with a share of 42% in 2025, due to the integration of molecular testing into emergency departments, oncology units, and transplant care workflows, alongside the growing adoption of point-of-care molecular platforms.

- Key Players: The Europe molecular diagnostics market features an intensely competitive landscape, with leading multinational diagnostics corporations investing in product innovation, strategic acquisitions, decentralized testing capabilities, and AI-powered analytics platforms to strengthen market positioning and expand clinical adoption across diverse healthcare settings.

The Europe molecular diagnostics market is being driven by rising disease burden, wider adoption of precision medicine, and rapid progress in genomic and PCR-based technologies. Increasing prevalence of infectious diseases, cancer, and chronic genetic disorders is catalyzing the demand for highly sensitive and accurate diagnostic solutions. Healthcare systems are prioritizing early detection and personalized treatment pathways, strengthening the role of biomarker testing and companion diagnostics. Investments in laboratory automation, modernization, and high-throughput platforms are improving testing capacity across hospitals and private laboratories. Innovation is also expanding into AI-supported diagnostics, as reflected in 2026 when the European Institute of Oncology and Laife Reply launched “Bianca,” Italy’s first large-scale AI-driven digital biobank project to digitize tissue slides, train algorithms, and enhance molecular cancer analysis. These advancements reinforce molecular diagnostics as a core pillar of Europe’s evolving healthcare infrastructure.

To get more information on this market Request Sample

Europe Molecular Diagnostics Market Trends:

Expansion of Automated PCR Platforms

Strategic distribution partnerships are accelerating the adoption of automated PCR-based molecular diagnostics across Europe. Clinical laboratories are increasingly seeking integrated systems that combine extraction and amplification workflows to improve efficiency and reduce turnaround times for infectious disease detection. This trend is reflected in 2025, when Sysmex Europe SE signed a multi-market agreement with SMD GmbH to supply the geneLEAD® VIII platform and associated kits across France, Germany, Austria, and Switzerland. By enabling fully automated RT-qPCR results within 120 minutes, such collaborations support broader market penetration of advanced molecular testing technologies.

Rising Demand for Explainable and Regulation-Compliant Diagnostic AI Solutions

The growing regulatory focus on transparency and trust in diagnostic algorithms is driving the demand for explainable AI platforms in molecular diagnostics. Laboratories and manufacturers require solutions that ensure auditability, regulatory compliance, and clear interpretability under evolving EU frameworks. Transparent AI systems help reduce uncertainty associated with automated decision-making and strengthen trust in diagnostic outcomes. This shift is reflected in 2025, when Diagnostics.ai introduced the first CE-IVDR certified transparent AI platform for real-time PCR diagnostics in Europe. By enabling full algorithm visibility and per-test monitoring, such platforms support compliant, reliable, and trustworthy AI-assisted molecular testing practices.

Growth of Spatial Omics Technologies Supporting Precision Medicine Research

Advancements in spatial omics are becoming an important trend shaping Europe’s molecular diagnostics ecosystem, particularly within research and personalized medicine. Spatially resolved molecular profiling allows scientists to study cellular activity within intact tissue environments, supporting deeper understanding of disease biology, tumor behavior, and therapeutic response. This capability strengthens biomarker discovery and accelerates drug development by revealing how cells interact in their natural spatial organization. The trend is reflected in 2026, when IRB Barcelona launched Spain’s first fully integrated Spatial Omics Platform, enabling researchers to preserve tissue architecture while mapping molecular signals, advancing next-generation diagnostic innovation.

Market Outlook 2026-2034:

The Europe molecular diagnostics market is positioned for steady advancement, underpinned by irreversible demographic trends, precision medicine adoption, and expanding testing infrastructure. The market generated a revenue of USD 5.6 Billion in 2025 and is projected to reach a revenue of USD 8.7 Billion by 2034, growing at a compound annual growth rate of 5.04% from 2026-2034. Increasing adoption of companion diagnostics, expanding POC testing networks, and the growing investment in antimicrobial resistance surveillance are expected to drive higher revenue streams and foster a more advanced, accessible molecular diagnostics landscape across the region.

Europe Molecular Diagnostics Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Reagents and Kits |

55% |

|

Technology |

Polymerase Chain Reactions (PCR) |

38% |

|

Application |

Infectious Diseases Diagnostics |

46% |

|

End User |

Hospitals |

42% |

Product Insights:

- Reagents and Kits

- Instruments

- Software and Services

Reagents and kits dominate with a market share of 55% of the total Europe molecular diagnostics market in 2025.

Reagents and kits lead the market due to their central role in routine testing and disease detection workflows. Molecular diagnostic procedures, such as PCR, RT-PCR, sequencing, and nucleic acid amplification, depend heavily on high-quality reagents and ready-to-use kits. Hospitals, reference laboratories, and research institutes rely on standardized kits to ensure accuracy, reproducibility, and regulatory compliance. The growing burden of infectious diseases, cancer, and genetic disorders across Europe is catalyzing the demand for reliable diagnostic consumables. Moreover, the 14th AIOM National Report “Cancer numbers in Italy 2024” was presented in Rome, outlining updated national cancer data. The report estimates 390,100 new cancer diagnoses in 2024.

Their dominance is also supported by recurring usage across a wide range of clinical applications, including oncology screening, respiratory testing, and personalized medicine. Unlike diagnostic instruments, which are capital purchases, reagents and kits generate continuous revenue through repeat employment. Strong regulatory standards in Europe encourage laboratories to adopt validated commercial kits, further strengthening the dominance of this segment. Ongoing innovation in multiplex assays, automation-compatible reagents, and rapid test kits enhances efficiency and throughput, reinforcing the leading position of reagents and kits in the market.

Technology Insights:

- Polymerase Chain Reactions (PCR)

- Hybridization

- DNA Sequencing

- Microarray

- Isothermal Nucleic Acid Amplification Technology (INAAT)

- Others

Polymerase chain reactions (PCR) lead with a market share of 38% of the total Europe molecular diagnostics market in 2025.

Polymerase chain reactions (PCR) dominate the market owing to its proven accuracy, high sensitivity, and broad clinical utility. PCR-based method is widely used for detecting infectious agents, identifying genetic abnormalities, and supporting cancer diagnostics. The ability to amplify small amounts of DNA or RNA makes PCR an essential tool for early and reliable diagnosis. Laboratories and hospitals in Europe have extensively adopted real-time PCR platforms, supported by strong clinical validation, standardized protocols, and regulatory acceptance across the region.

The dominance of PCR technology is supported by continuous advancements in assay design, automation, and multiplex testing capabilities. PCR offers rapid turnaround, high reproducibility, and strong compatibility with high-throughput laboratory workflows, making it widely preferred across clinical applications. Regulatory progress is also reinforcing adoption, as in 2024 altona Diagnostics received the IVDR Quality Management System certificate under EU Regulation 2017/746 for its PCR testing products, enabling the launch of CE-IVD marked assays under stricter standards. Such developments strengthen confidence in PCR platforms and support sustained demand for precision diagnostics.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Infectious Diseases Diagnostics

- Oncology

- Genetic Testing

- Blood Screening

- Others

Infectious diseases diagnostics exhibits a clear dominance with a 46% share of the total Europe molecular diagnostics market in 2025.

Infectious diseases diagnostics hold the biggest share in the market driven by the persistent burden of viral, bacterial, and respiratory infections across the region. Molecular testing plays a vital role in early and accurate detection of pathogens, such as influenza, HIV, hepatitis, and emerging respiratory viruses. Public health agencies and hospital laboratories depend on rapid nucleic acid–based tests to control outbreaks and guide treatment decisions. This persistent need is reflected in regional disease prevalence, as the annual HIV/AIDS surveillance report recorded 105,922 HIV diagnoses across the WHO European Region in 2024, covering 53 countries. Such infection reinforces sustained reliance on rapid nucleic acid–based diagnostic technologies.

The leading position of the segment is also supported by continuous investment in laboratory capacity and preparedness following recent pandemic experiences. Many countries expanded molecular testing facilities, increasing installed equipment and trained personnel. Routine screening programs for sexually transmitted infections, tuberculosis, and hospital-acquired infections contribute to steady test volumes. The need for rapid turnaround times and high sensitivity has encouraged widespread adoption of PCR and multiplex assays. These factors collectively position infectious diseases diagnostics as the dominant segment in the market.

End User Insights:

- Hospitals

- Laboratories

- Others

Hospitals dominate with a market share of 42% of the total Europe molecular diagnostics market in 2025.

Hospitals represent the largest segment because of their central role in patient diagnosis, treatment planning, and disease monitoring. Large hospitals across Europe are equipped with advanced laboratories capable of performing PCR, sequencing, and other nucleic acid–based tests. These facilities handle high patient volumes, including emergency cases, inpatient care, and outpatient referrals, which drives consistent demand for molecular testing. The integration of diagnostics with clinical departments, such as oncology, infectious diseases, and critical care, further strengthens hospital-based testing activity.

Another factor supporting the dominance of hospitals is their access to funding, skilled laboratory personnel, and automated diagnostic platforms. Many public and private hospitals invest in in-house molecular testing to reduce turnaround time and improve clinical decision-making. Government reimbursement policies and strong healthcare infrastructure across Western and Northern Europe encourage hospitals to expand diagnostic capabilities. In addition, hospitals often serve as reference centers for complex cases and regional surveillance programs, contributing to higher test volumes and reinforcing their leading position in the Europe molecular diagnostics market.

Country Insights:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Germany holds a vital position in the market due to its advanced healthcare infrastructure, strong presence of diagnostic companies, and high adoption of PCR and sequencing technologies. The country’s focus on precision medicine, well-funded research institutes, and rising demand for early disease detection support steady growth in molecular testing services.

France is a key market for molecular diagnostics in Europe, driven by increasing use of genetic testing, oncology diagnostics, and infectious disease screening. Strong government support for healthcare innovation, expanding laboratory networks, and the growing awareness about personalized treatment approaches contribute to the rising demand for advanced molecular diagnostic solutions.

The United Kingdom represents a significant share of the market owing to widespread adoption of advanced testing technologies in hospitals and reference labs. Strong focus on genomics research, early disease detection, and integration of molecular diagnostics into routine clinical care continues to drive market expansion.

Italy’s molecular diagnostics market is growing, supported by increasing demand for cancer screening, infectious disease testing, and genetic disorder diagnosis. Expansion of private diagnostic laboratories, improving healthcare investments, and rising awareness about precision medicine are key factors strengthening the country’s adoption of molecular diagnostic technologies.

Spain contributes to the Europe molecular diagnostics market through the growing investments in healthcare modernization and expanding diagnostic capabilities. Rising use of PCR-based testing, increasing focus on oncology applications, and improving access to advanced laboratory services support market growth across both public and private healthcare sectors.

Others, including the Netherlands, Sweden, Switzerland, and Belgium, play an important role in the molecular diagnostics market due to strong healthcare systems and rising adoption of innovative diagnostic tools. The growing demand for early detection, personalized medicine, and improved laboratory infrastructure supports continued regional market development.

Market Dynamics:

Growth Drivers:

Why is the Europe Molecular Diagnostics Market Growing?

Growing Geriatric Population

Europe’s rapidly aging demographic structure is fundamentally reshaping healthcare demand patterns and driving sustained growth in molecular diagnostics. Older populations face significantly higher susceptibility to infectious diseases, cancer, and chronic conditions, creating structural long-term demand for advanced diagnostic tools. As of 1 January 2024, the European Union population stood at approximately 449.3 million, with 21.6% aged 65 years and above, highlighting the scale of demographic transition. This shift is contributing to higher testing volumes in areas, such as infectious disease detection, oncology profiling, and pharmacogenomic analysis. In response, healthcare systems are expanding molecular diagnostic integration across primary care, geriatric services, and chronic disease management pathways.

Rising Prevalence of Infectious and Chronic Diseases

The growing incidence of viral infections, antimicrobial resistance, cancer, and genetic disorders is catalyzing the demand for rapid and highly accurate diagnostic solutions across Europe. Molecular diagnostics supports early disease detection, precise pathogen identification, and effective monitoring of disease progression, enabling improved clinical outcomes and more efficient treatment pathways. Healthcare systems are increasingly prioritizing sensitive testing technologies to manage complex disease burdens. This trend is reflected in 2025, when MVZ HPH Institute in Hamburg launched HPH MRD, a tumor-informed ctDNA blood test for detecting minimal residual disease in solid cancer patients, improving access to advanced recurrence monitoring within Europe.

Increasing Healthcare Expenditure and Infrastructure Development

Rising healthcare investment across Europe is supporting the modernization of laboratory infrastructure and strengthening diagnostic capabilities. Increased funding for advanced equipment, workforce training, and research is enabling broader adoption of automated and high-precision molecular testing platforms. Public and private providers are upgrading facilities to expand access beyond specialized centers, improving overall healthcare readiness. This progress is reflected in 2024, when The Royal Marsden NHS Foundation Trust launched the UK’s first genome testing facility using robotic automation through Automata Technologies’ LINQ platform, designed to double somatic cancer testing throughput. Such developments are accelerating innovation and sustaining growth of the Europe molecular diagnostics market.

Market Restraints:

What Challenges the Europe Molecular Diagnostics Market is Facing?

High Testing Costs Limiting Broader Market Penetration

The significant costs associated with molecular diagnostic testing, including sophisticated instrumentation, specialized reagents, and skilled technical personnel, represent a fundamental barrier to broader adoption. Many healthcare systems in Central and Eastern Europe face constrained budgets that limit investment in advanced molecular platforms, restricting equitable access to cutting-edge diagnostics across the region.

Regulatory Complexity and Compliance Burdens Under IVDR

The stringent requirements of the In Vitro Diagnostic Regulation have created certification bottlenecks and increased compliance costs for manufacturers, particularly small and medium-sized firms. Fragmented reimbursement pathways across 27 EU member states further complicate market access, with varying health technology assessment frameworks creating inconsistent adoption patterns for new molecular diagnostic products.

Shortage of Skilled Bioinformatics Professionals

The growing complexity of molecular diagnostic workflows, particularly those involving next-generation sequencing and genomic data interpretation, is constrained by a significant shortage of qualified bioinformatics professionals. Advanced diagnostic platforms require specialized expertise in data analysis, clinical interpretation, and quality assurance, and the insufficient talent pipeline is delaying report turnaround and limiting the capacity of laboratories to adopt next-generation testing methodologies.

Competitive Landscape:

The Europe molecular diagnostics market is characterized by intense competition among established multinational corporations and innovative specialized players. Companies are competing through diversified strategies encompassing product innovation, strategic acquisitions, manufacturing capacity expansion, and development of integrated diagnostic platforms that combine instrumentation, reagents, and software analytics. The competitive landscape is increasingly shaped by investments in point-of-care testing capabilities, AI-powered bioinformatics solutions, companion diagnostics development, and IVDR compliance readiness, as manufacturers seek to capture market share across centralized and decentralized testing environments.

Recent Developments:

- December 2025: Seegene, a global leader in molecular diagnostics, announced the establishment of a new subsidiary in France to strengthen its European footprint and expand local customer support. The move targeted France’s fast-growing molecular diagnostics market, driven by demand for STI, gastrointestinal, and respiratory infection testing. The subsidiary also supported the future rollout of Seegene’s developing platforms, CURECA™ and STAgora™, across Europe.

- July 2025: SYSTAAQ Diagnostic Products announced it received CE Mark certification for its HBV and HCV molecular diagnostic tests. The approval allowed the Virginia-based company to market its real-time PCR kits for clinical use across Europe and other CE-recognizing regions. The tests were designed for early detection and quantitation of Hepatitis B and C viral loads.

Europe Molecular Diagnostics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Reagents and Kits, Instruments, Software and Services |

| Technologies Covered | Polymerase Chain Reactions (PCR), Hybridization, DNA Sequencing, Microarray, Isothermal Nucleic Acid Amplification Technology (INAAT), Others |

| Applications Covered | Infectious Diseases Diagnostics, Oncology, Genetic Testing, Blood Screening, Others |

| End Users Covered | Hospitals, Laboratories, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Molecular Diagnostics Market Report

The Europe molecular diagnostics market size was valued at USD 5.6 Billion in 2025.

The Europe molecular diagnostics market is expected to grow at a compound annual growth rate of 5.04% from 2026-2034 to reach USD 8.7 Billion by 2034.

Reagents and kits held the largest revenue share of 55% in 2025, driven by their essential role in high-throughput diagnostic workflows, recurring procurement requirements, and broad applicability across PCR, NGS, and isothermal amplification platforms.

Key factors driving the Europe molecular diagnostics market include the expansion of strategic distribution partnerships that accelerate adoption of automated PCR platforms. This is reflected in 2025, when Sysmex Europe partnered with SMD GmbH to supply the geneLEAD® VIII system across multiple countries, enabling fully automated RT-qPCR results within 120 minutes.

Major challenges include high testing costs limiting broader adoption, regulatory complexity and compliance burdens under IVDR, fragmented reimbursement pathways across EU member states, shortage of skilled bioinformatics professionals, and infrastructure gaps restricting access in less-resourced regions of Central and Eastern Europe.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)