Europe Carbon Black Market Size, Share, Trends and Forecast by Type, Grade, Application, and Country, 2026-2034

Europe Carbon Black Market Summary:

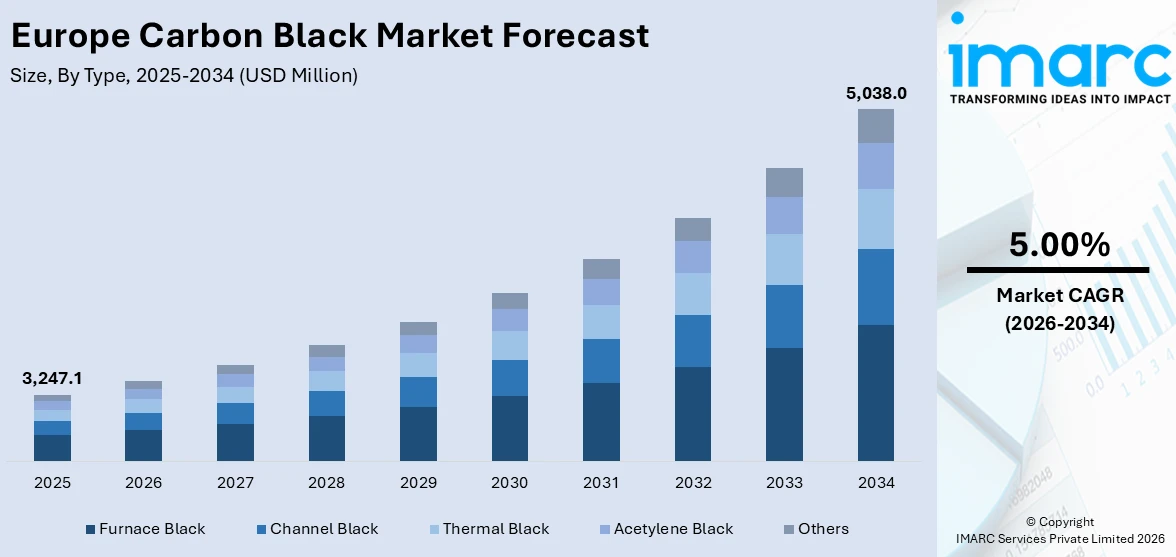

The Europe carbon black market size was valued at USD 3,247.1 Million in 2025 and is projected to reach USD 5,038.0 Million by 2034, growing at a compound annual growth rate of 5.00% from 2026-2034.

The Europe carbon black market is witnessing sustained expansion driven by robust demand from the automotive and tire manufacturing sectors, which remain the primary consumers of this essential industrial material. Increasing adoption of electric vehicles is creating demand for specialized carbon black formulations in high-performance tires and battery components. Concurrently, stringent EU environmental regulations are accelerating the shift toward sustainable and circular production methods, encouraging investment in recovered carbon black and low-emission manufacturing technologies. Growing applications in plastics, coatings, and conductive materials, coupled with ongoing capacity expansions across key European countries, are further strengthening the Europe carbon black market share.

Key Takeaways and Insights:

- By Type: Furnace black dominates the market with a share of 74% in 2025, owing to its versatility across tire reinforcement and industrial applications, cost-effective large-scale production capabilities, and adaptability to both standard and specialty formulations demanded by European manufacturers.

- By Grade: Standard grade leads the market with a share of 76% in 2025, driven by its widespread utilization in tire and non-tire rubber applications, cost-effectiveness as a reinforcing agent, and consistent demand from automotive, construction, and industrial sectors across Europe.

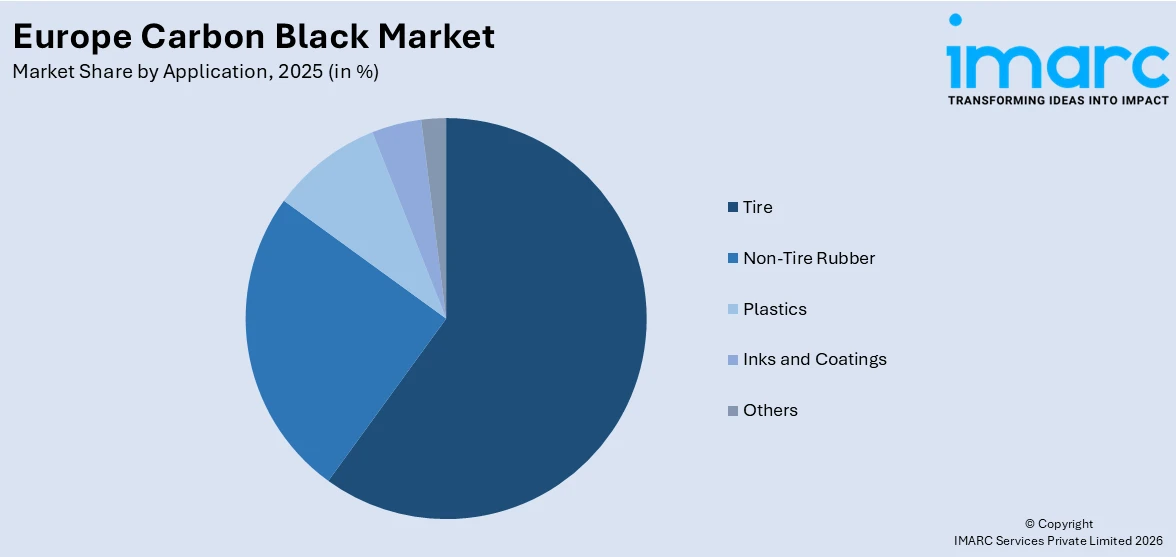

- By Application: Tire represents the largest segment with a market share of 60% in 2025, reflecting the strong dependence of European tire manufacturing on carbon black for enhancing tread durability, rolling resistance, and overall performance in both passenger and commercial vehicle tires.

- Key players: Leading manufacturers in the Europe carbon black market are strengthening their competitive positions through capacity expansions, sustainability-driven innovations in recovered and circular carbon black, and strategic investments in specialty grades for electric vehicle batteries and advanced industrial applications.

To get more information on this market Request Sample

The market for carbon black is expanding steadily in the region of Europe as different sectors across the region are increasingly incorporating this important component into their systems to improve their performances, longevity, and compliance to sustainability. Without a doubt, the automotive sector leads the demand for carbon black in the region of Europe, especially for the tire industry since the component is essential for enhancing the strength of rubber products. The move towards electric cars has led to the introduction of different products to meet the changed needs of the market since manufacturers are designing products for different applications ranging from low-rolling-resistance tires to conductive materials used in the production of lithium-ion batteries. The need to protect the environment has seen different regulations being introduced in the region of Europe, such as the Circular Economy Action Plan implemented by the European Union and the altered REACH regulations concerning polycyclic aromatic hydrocarbons, compelling manufacturers to adopt green technology to produce the product. Different uses of the component in the production of plastics, coatings, and electronic materials are expanding the scope of the market for carbon black in the region.

Europe Carbon Black Market Trends:

Accelerating Shift Toward Recovered and Circular Carbon Black

The European carbon black industry is witnessing a significant pivot toward sustainability as producers and tire manufacturers invest in recovered carbon black derived from end-of-life tires through pyrolysis. Regulatory pressure from the EU Circular Economy Action Plan and growing commitments from tire makers to incorporate recycled content are driving this transition. In February 2024, Enviro Systems and Antin Infrastructure Partners signed the final investment decision for a tire recycling plant in Uddevalla, Sweden, designed to produce recovered carbon black at commercial scale. This shift toward circularity is fundamentally altering supply chain dynamics and opening new competitive opportunities across the market, supporting the Europe carbon black market growth.

Rising Demand for Specialty Carbon Black in Electric Vehicle Applications

The rapid growth of electric vehicle adoption across Europe is generating increased demand for specialty carbon black formulations tailored to EV-specific requirements. Low rolling resistance tires for electric vehicles require precisely controlled particle size distribution and customized surface treatments that reduce energy loss, enabling manufacturers to command significant price premiums over commodity grades. Leading companies are investing in research and development to create conductive carbon black grades suitable for lithium-ion battery electrodes and advanced polymer composites. These innovations are diversifying the application landscape and positioning specialty carbon black as a high-growth segment within the broader European market.

Expansion of Low-PAH and Environmentally Compliant Production Technologies

European carbon black producers are accelerating investments in environmentally compliant production technologies to align with tightening regulatory frameworks. Updated REACH regulations on polycyclic aromatic hydrocarbons are compelling manufacturers to develop low-PAH carbon black variants for tire and industrial applications. Companies are channelling resources into clean production research and development projects, supported by government grants and public funding mechanisms, aimed at enhancing production efficiency using circular feedstocks and reducing overall carbon footprints. This regulatory-driven innovation is reshaping competitive dynamics and establishing Europe as a leader in sustainable carbon black manufacturing.

Market Outlook 2026-2034:

The demand for carbon black in Europe will, therefore, see steady growth throughout the forecast period, supported by resilient automotive and industrial demand, coupled with an accelerating shift toward sustainability in production methods. Further capacity additions in progress, increasingly adopted recovered carbon black, applications in electric vehicle components, and advanced materials are expected to drive market momentum. Such regulatory initiatives facilitate circularity and emission reduction, hence reshaping the competitive landscape and incentivizing producers to innovate in product development and manufacturing processes. Strategic investments in specialty grades for batteries, conductive polymers, and advanced coatings are likely to complement traditional applications in tires and rubber, hence, expanding the revenue base and reinforcing the long-term market expansion across the region. The market generated a revenue of USD 3,247.1 Million in 2025 and is projected to reach a revenue of USD 5,038.0 Million by 2034, growing at a compound annual growth rate of 5.00% from 2026-2034.

Europe Carbon Black Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Furnace Black |

74% |

|

Grade |

Standard Grade |

76% |

|

Application |

Tire |

60% |

Type Insights:

- Furnace Black

- Channel Black

- Thermal Black

- Acetylene Black

- Others

Furnace black dominates with a 74% share of the total Europe carbon black market in 2025.

Furnace black maintains its commanding position in the European market due to its unmatched versatility in both reinforcement and pigmentation applications. The furnace process enables large-scale production of carbon black grades with precisely controlled particle size, structure, and surface area, making it the preferred choice for tire manufacturers seeking to optimize tread wear, rolling resistance, and fuel efficiency. European producers have invested heavily in modernizing furnace technology to reduce emissions and improve energy efficiency, with facilities increasingly co-generating electricity from process waste heat to supply both plant operations and regional power grids.

The dominance of furnace black is further reinforced by its adaptability to evolving market requirements, including the development of low-PAH variants to comply with updated European REACH regulations. Manufacturers are extending their product portfolios with surface-modified grades tailored to electric vehicle tires, coatings, and industrial rubber applications. Ongoing capacity expansions across key European production facilities are strengthening regional supply security, enabling producers to meet growing demand for both standard and specialty rubber carbon black grades while reducing dependency on external suppliers and ensuring reliable delivery to downstream industries.

Grade Insights:

- Standard Grade

- Specialty Grade

Standard grade leads with a share of 76% of the total Europe carbon black market in 2025.

Standard grade carbon black commands the largest share in Europe, driven by its extensive utilization as a reinforcing filler in tire manufacturing and non-tire rubber goods. This grade offers an optimal balance of cost-effectiveness and performance enhancement, improving the durability, tensile strength, and abrasion resistance of rubber products used across automotive, construction, and industrial applications. The sustained demand from European tire producers, who rely on standard grade for both original equipment and replacement tires, underpins this segment's dominant position within the market.

The resilience of standard grade demand is supported by the continued strength of European vehicle production, which sustains robust consumption across both original equipment and replacement tire channels. As tire manufacturers scale output to meet domestic and export requirements, standard carbon black remains the foundational material for achieving required mechanical properties at competitive production costs. Additionally, growing utilization in mechanical rubber goods such as seals, hoses, conveyor belts, and vibration dampeners across industrial sectors further reinforces the segment's leading market position in Europe.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Tire

- Non-Tire Rubber

- Plastics

- Inks and Coatings

- Others

Tire exhibits a clear dominance with a 60% share of the total Europe carbon black market in 2025.

The tire application segment maintains its leading position in the European carbon black market owing to the critical role this material plays in enhancing tire performance, durability, and safety. Carbon black serves as the primary reinforcing filler in tire tread compounds, improving abrasion resistance, tensile strength, and heat dissipation while contributing to optimal rolling resistance and fuel efficiency. Europe's position as a major hub for global tire manufacturing, home to leading producers, generates consistent and substantial demand for high-quality carbon black grades.

The growing emphasis on electric vehicle tires is creating additional demand within this segment, as EV-specific tires require precisely engineered carbon black formulations to achieve low rolling resistance without compromising grip or longevity. Sustained vehicle registrations across the European Union continue to support both replacement and original equipment tire demand, reinforcing carbon black consumption. Furthermore, the introduction of stricter emission standards that encompass tire particle abrasion limits for the first time is compelling manufacturers to develop advanced tire compounds with optimized carbon black integration to meet evolving environmental requirements.

Country Insights:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Germany’s carbon black market is driven by strong automotive manufacturing and tire production, supported by advanced rubber processing industries. Demand also comes from plastics, coatings, and specialty applications, with emphasis on sustainable production methods and compliance with strict EU environmental regulations.

France’s carbon black market benefits from its tire, aerospace, and industrial manufacturing sectors. Growing use in high-performance rubber goods, coatings, and conductive plastics supports demand. The market is influenced by sustainability goals and the transition toward low-emission industrial processes.

The United Kingdom carbon black market is supported by demand from tire replacement, automotive components, and plastics industries. Specialty grades are increasingly used in inks, coatings, and electronics. Regulatory focus on emissions and supply chain resilience shapes market developments post-Brexit.

Italy’s carbon black market is fueled by automotive parts, tire manufacturing, and industrial rubber goods production. Strong presence of small and mid-sized manufacturers drives steady consumption. Demand also comes from pigments in coatings and plastics, alongside sustainability initiatives.

Spain’s carbon black market growth is linked to automotive assembly, tire manufacturing, and construction-related plastics. Rising demand for specialty carbon black in coatings and conductive applications supports expansion. Environmental regulations and energy costs remain key influencing factors.

Market Dynamics:

Growth Drivers:

Why is the Europe Carbon Black Market Growing?

Robust Automotive and Tire Manufacturing Demand

The European automotive sector remains a primary catalyst for carbon black market growth, as tire and rubber component manufacturers require substantial volumes of this material for production. Europe hosts numerous world-leading tire manufacturers and maintains a significant vehicle production base, generating consistent demand across original equipment and aftermarket channels. The continent's tire industry consumes carbon black to enhance critical performance attributes including tread wear resistance, rolling efficiency, and structural integrity. The European Automobile Manufacturers Association reported that new car registrations in the EU reached approximately 10.6 Million Units in 2024, sustaining replacement tire demand and driving aftermarket consumption. Moreover, the growing fleet of commercial vehicles and the expansion of logistics infrastructure across the region contribute to increasing demand for heavy-duty tires, which utilize higher carbon black loadings to withstand intensive operational conditions and extended mileage requirements.

Stringent EU Environmental and Sustainability Regulations

The regulatory landscape in Europe is significantly shaping carbon black market dynamics by mandating cleaner production processes, lower emissions, and increased use of recycled materials. The European Union's Circular Economy Action Plan identifies recovered carbon black as a strategic secondary raw material, encouraging manufacturers to integrate sustainable alternatives into their supply chains. Updated REACH regulations on polycyclic aromatic hydrocarbons are compelling producers to reformulate products and invest in advanced manufacturing technologies. Trade policy shifts restricting carbon black imports from certain origins have further accelerated supply chain localization and domestic capacity expansion, prompting European manufacturers to strengthen regional production capabilities. These regulatory pressures are creating a favorable environment for producers investing in green manufacturing, with companies increasingly adopting bio-based feedstocks, pyrolysis oils, and co-generation systems to reduce their environmental footprint while maintaining product quality and competitive pricing. The convergence of environmental mandates, circular economy objectives, and supply chain resilience strategies is driving a fundamental transformation in how carbon black is produced and sourced across the continent, positioning compliant manufacturers for long-term competitive advantage.

Expanding Applications in Electric Vehicles and Energy Storage

The accelerating transition toward electric mobility across Europe is opening substantial new demand avenues for specialty carbon black formulations. Electric vehicles require specially engineered tires with low rolling resistance to maximize battery range, creating demand for premium carbon black grades with precisely controlled particle morphology. Beyond tires, carbon black is increasingly used as a conductive additive in lithium-ion battery electrodes, where it enhances electron transfer and improves cell performance. Orion Engineered Carbons has been expanding into conductive additives critical for high-voltage cable compounds and battery energy storage systems, leveraging its PRINTEX kappa product line to serve the growing electrification market. The broader adoption of renewable energy storage systems and the expansion of EV charging infrastructure are further broadening the application scope, positioning specialty carbon black as an essential material in Europe's clean energy transition.

Market Restraints:

What Challenges the Europe Carbon Black Market is Facing?

Feedstock Price Volatility and Supply Chain Disruptions

European carbon black producers face significant challenges from volatile feedstock pricing, particularly coal-tar pitch and carbon black feedstock oil, which have experienced substantial price fluctuations in recent years. The green-steel transition has reduced European blast-furnace output, tightening coal-tar pitch availability and contributing to price instability. Since producers typically operate under multiyear supply contracts with tire customers, sudden feedstock cost spikes can compress margins and create financial pressure, forcing greater reliance on hedging strategies and alternative raw materials to maintain operational stability.

Competition from Low-Cost Imports

The European carbon black market faces mounting competitive pressure from lower-priced imports, particularly from Asian producers benefiting from cost advantages in raw materials and energy. Elevated levels of tire imports from Southeast Asia and China have put pressure on Western European tire production volumes, indirectly reducing domestic carbon black consumption. This import competition challenges the profitability of European manufacturers who must simultaneously invest in regulatory compliance, sustainability initiatives, and technological upgrades while defending market share against more cost-competitive alternatives.

High Environmental Compliance and Production Costs

Meeting stringent European environmental standards imposes significant capital and operational costs on carbon black manufacturers. Investments in emission control equipment, low-PAH production technologies, waste heat recovery systems, and circular feedstock processing add to production expenses. Smaller producers face particular challenges in absorbing these costs, potentially leading to market consolidation. The cumulative burden of compliance with REACH regulations, industrial emissions directives, and emerging sustainability mandates raises the barrier to entry and increases operational complexity for all market participants.

Competitive Landscape:

The competitive landscape of the Europe carbon black market is moderately consolidated, with several established global manufacturers holding significant market shares based on their large production networks, diversified product portfolios, and good customer relationships. Sustainability-related new product developments in the lines of recovered carbon black and low-emission production processes have become synonymous with the name of the companies while adhering to the increasingly strict EU environmental standards. Specialty-grade production for electric vehicle applications and energy storage would be another strategic and differentiating investment. Supply chain localization strategies will reduce the imports dependence, improve delivery reliability, and give further competitive edge to the players in an evolving regulatory and industrial ecosystem.

Europe Carbon Black Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Furnace Black, Channel Black, Thermal Black, Acetylene Black, Others |

| Grades Covered | Standard Grade, Specialty Grade |

| Applications Covered | Tire, Non-Tire Rubber, Plastics, Inks and Coatings, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The Europe carbon black market size was valued at USD 3,247.1 Million in 2025.

The Europe carbon black market is expected to grow at a compound annual growth rate of 5.00% from 2026-2034 to reach USD 5,038.0 Million by 2034.

Furnace black dominated the market with a share of 74%, driven by its versatility across tire reinforcement, industrial rubber, plastics, and pigment applications, making it the most widely produced and consumed carbon black type in Europe.

Key factors driving the Europe carbon black market include strong automotive and tire manufacturing demand, stringent EU environmental regulations promoting sustainable production, expanding electric vehicle adoption, and growing applications in specialty and high-performance industrial segments.

Major challenges include feedstock price volatility and supply chain disruptions, competition from lower-cost imports, high environmental compliance costs, regulatory burden on manufacturers, and the need for significant capital investment in sustainable production technologies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)