Ethanol Prices, Trend, Chart, Demand, Market Analysis, News, Historical and Forecast Data Report 2026 Edition

Ethanol Price Trend, Index and Forecast

Track real-time and historical ethanol prices across global regions. Updated monthly with market insights, drivers, and forecasts.

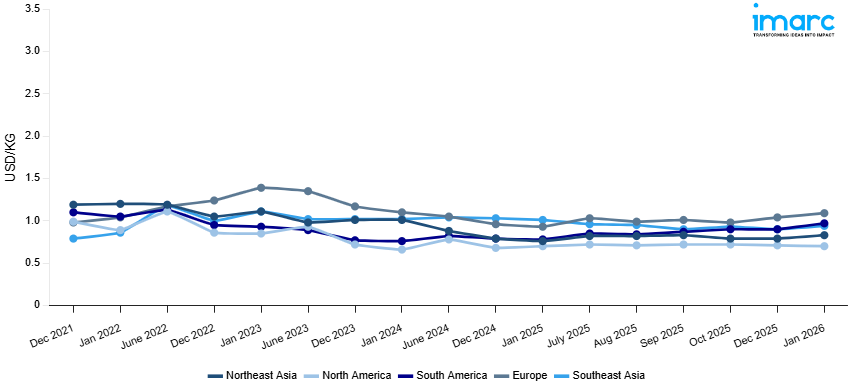

Ethanol Prices January 2026

| Region | Price (USD/Kg) | Latest Movement |

|---|---|---|

| Northeast Asia | 0.83 | 5.1% ↑ Up |

| Europe | 1.09 | 4.8% ↑ Up |

| South America | 0.97 | 7.8% ↑ Up |

| Southeast Asia | 0.94 | 4.4% ↑ Up |

| North America | 0.7 | -1.4% ↓ Down |

Ethanol Price Index (USD/KG):

The chart below highlights monthly ethanol prices across different regions.

Get Access to Monthly/Quarterly/Yearly Prices, Request Sample

Market Overview Q3 Ending September 2025

Northeast Asia: Ethanol prices in Northeast Asia posted slight gains, supported by steady industrial demand from chemicals and solvents. The ethanol price index showed resilience as stable raw material supply and consistent downstream activity kept the market balanced. Seasonal demand from fuel blending contributed to procurement activity, while export flows remained supportive. However, ample regional production capacity prevented stronger price escalation, keeping overall sentiment cautiously optimistic.

Europe: In Europe, ethanol prices moved upward, driven by rising demand from the fuel sector and industrial applications. The ethanol price index reflected improved buying momentum as energy sector blending mandates boosted consumption. Supply-side constraints stemming from logistics disruptions added further support to price increases. Strong industrial usage in pharmaceuticals and chemicals also contributed to bullish sentiment, although buyers continued to adopt measured procurement strategies due to cost pressures.

South America: South America experienced a firm increase in ethanol prices, supported by robust demand from fuel blending and beverage sectors. The ethanol price index reflected steady consumption levels, aided by seasonal demand drivers in the biofuel segment. Limited availability due to uneven harvest patterns further lifted market sentiment. Regional reliance on sugarcane feedstock created volatility in supply, and tighter inventory levels added to upward pressure on prices during this quarter.

Southeast Asia: Southeast Asia witnessed a decline in ethanol prices, reflecting weaker demand from fuel blending and industrial sectors. The ethanol price index moved lower as oversupply conditions, coupled with slower procurement from downstream industries, pressured market sentiment. Favorable feedstock availability further weighed on prices, while muted export demand limited opportunities for recovery. Buyers remained cautious, anticipating continued softness in regional pricing through the near term.

North America: In North America, ethanol prices edged higher on the back of consistent demand from the fuel and beverage industries. The ethanol price index showed modest gains as seasonal fuel consumption supported procurement activity. However, abundant domestic production and steady feedstock availability prevented significant upward movement. The industrial chemicals segment provided additional demand support, but overall pricing remained relatively stable, with gains constrained by competitive supply conditions.

Ethanol Price Trend, Market Analysis, and News

IMARC's latest publication, “Ethanol Prices, Trend, Chart, Demand, Market Analysis, News, Historical and Forecast Data Report 2026 Edition,” presents a detailed examination of the ethanol market, providing insights into both global and regional trends that are shaping prices. This report delves into the spot price of ethanol at major ports and analyzes the composition of prices, including FOB and CIF terms. It also presents detailed ethanol prices trend analysis by region, covering North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. The factors affecting ethanol pricing, such as the dynamics of supply and demand, geopolitical influences, and sector-specific developments, are thoroughly explored. This comprehensive report helps stakeholders stay informed with the latest market news, regulatory updates, and technological progress, facilitating informed strategic decision-making and forecasting.

.webp)

Ethanol Industry Analysis

The global ethanol industry size reached USD 104.80 Billion in 2025. By 2034, IMARC Group expects the market to reach USD 158.45 Billion, at a projected CAGR of 4.47% during 2026-2034. Market expansion is fueled by increasing biofuel mandates, rising consumption in beverages, and growing use in industrial solvents and disinfectants. Sustainability initiatives and the shift toward renewable energy sources further strengthen long-term demand.

Latest developments in the Ethanol Industry:

- January 2025: Advanta Seeds and Baidyanath Biofuels Private Ltd announced a strategic partnership to advance India's ethanol production. The partnership aims to contribute to India's National Biofuels Policy goal of achieving 20% ethanol blending with petrol by 2025-26.

- January 2025: RCM Technologies, Inc., through its RCM Thermal Kinetics division, announced the launch of its New Ethanol eXpansion Technology (NEXT) program. The initiative is developed to transform ethanol plant expansion projects by increasing production capacity and improving energy efficiency, while avoiding the need for expensive and time-consuming replacement of major equipment.

- December 2024: Godavari Biorefineries Limited (GBL), the largest biofuels company in India, proposed investing USD 15.6 million in a 200 KLPD ethanol distillery based on corn and grains in order to increase its output. The choice aligns with GBL's mission to support India's green energy transition and climate-related risk resilience.

- May 2024: Nayara Energy Ltd, backed by Rosneft, announced an INR 600 crore investment to establish two ethanol production plants in Andhra Pradesh and Madhya Pradesh, each with a capacity of 200 kiloliters per day. The company plans to create a total of five facilities, aiming for a combined production capacity of 1,000 kiloliters per day.

- May 2024: Verbio, a German renewable energy company, announced to expand its South Bend, Indiana ethanol plant into an innovative biorefinery with combined bioethanol-biomethane production.

Product Description

Ethanol (C₂H₅OH) is a volatile, flammable, and colorless alcohol produced either synthetically from petrochemical feedstocks or biologically through the fermentation of sugars derived from crops such as corn, sugarcane, and wheat. It is widely valued for its solvent properties, high octane rating, and role as a renewable biofuel. Ethanol is extensively used as a fuel additive to reduce emissions, as well as in the beverage industry for alcoholic products. Industrially, it is employed in the production of pharmaceuticals, personal care products, disinfectants, and specialty chemicals. Its versatility, renewability, and relatively low environmental impact make ethanol a critical component across energy, industrial, and consumer sectors.

Report Coverage

| Key Attributes | Details |

|---|---|

| Product Name | Ethanol |

| Report Features | Exploration of Historical Trends and Market Outlook, Industry Demand, Industry Supply, Gap Analysis, Challenges, Ethanol Price Analysis, and Segment-Wise Assessment. |

| Currency/Units | US$ (Data can also be provided in local currency) or Metric Tons |

| Region/Countries Covered | The current coverage includes analysis at the global and regional levels only. Based on your requirements, we can also customize the report and provide specific information for the following countries: Asia Pacific: China, India, Indonesia, Pakistan, Bangladesh, Japan, Philippines, Vietnam, Thailand, South Korea, Malaysia, Nepal, Taiwan, Sri Lanka, Hongkong, Singapore, Australia, and New Zealand* Europe: Germany, France, United Kingdom, Italy, Spain, Russia, Turkey, Netherlands, Poland, Sweden, Belgium, Austria, Ireland, Switzerland, Norway, Denmark, Romania, Finland, Czech Republic, Portugal and Greece* North America: United States and Canada Latin America: Brazil, Mexico, Argentina, Columbia, Chile, Ecuador, and Peru* Middle East & Africa: Saudi Arabia, UAE, Israel, Iran, South Africa, Nigeria, Oman, Kuwait, Qatar, Iraq, Egypt, Algeria, and Morocco* *The list of countries presented is not exhaustive. Information on additional countries can be provided if required by the client. |

| Information Covered for Key Suppliers |

|

| Customization Scope | The report can be customized as per the requirements of the customer |

| Report Price and Purchase Option |

Plan A: Monthly Updates - Annual Subscription

Plan B: Quarterly Updates - Annual Subscription

Plan C: Biannually Updates - Annual Subscription

|

| Post-Sale Analyst Support | 360-degree analyst support after report delivery |

| Delivery Format | PDF and Excel through email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report presents a detailed analysis of ethanol pricing, covering global and regional trends, spot prices at key ports, and a breakdown of FOB and CIF prices.

- The study examines factors affecting ethanol price trend, including input costs, supply-demand shifts, and geopolitical impacts, offering insights for informed decision-making.

- The competitive landscape review equips stakeholders with crucial insights into the latest market news, regulatory changes, and technological advancements, ensuring a well-rounded, strategic overview for forecasting and planning.

- IMARC offers various subscription options, including monthly, quarterly, and biannual updates, allowing clients to stay informed with the latest market trends, ongoing developments, and comprehensive market insights. The ethanol price charts ensure our clients remain at the forefront of the industry.

Key Questions Answered in This Report

The ethanol prices in January 2026 were 0.83 USD/KG in Northeast Asia, 1.09 USD/KG in Europe, 0.97 USD/KG in South America, 0.94 USD/KG in Southeast Asia, and 0.7 USD/KG in North America.

The ethanol pricing data is updated on a monthly basis.

We provide the pricing data primarily in the form of an Excel sheet and a PDF.

Yes, our report includes a forecast for ethanol prices.

The regions covered include North America, Europe, Asia Pacific, Middle East, and Latin America. Countries can be customized based on the request (additional charges may be applicable).

Yes, we provide both FOB and CIF prices in our report.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Inquire Before Buying

Inquire Before Buying

Speak to an Analyst

Speak to an Analyst Request Brochure

Request Brochure

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)

Why Choose Us

IMARC offers trustworthy, data-centric insights into commodity pricing and evolving market trends, enabling businesses to make well-informed decisions in areas such as procurement, strategic planning, and investments. With in-depth knowledge spanning more than 1000 commodities and a vast global presence in over 150 countries, we provide tailored, actionable intelligence designed to meet the specific needs of diverse industries and markets.

1000

+Commodities

150

+Countries Covered

3000

+Clients

20

+Industry

Robust Methodologies & Extensive Resources

IMARC delivers precise commodity pricing insights using proven methodologies and a wealth of data to support strategic decision-making.

Subscription-Based Databases

Our extensive databases provide detailed commodity pricing, import-export trade statistics, and shipment-level tracking for comprehensive market analysis.

Primary Research-Driven Insights

Through direct supplier surveys and expert interviews, we gather real-time market data to enhance pricing accuracy and trend forecasting.

Extensive Secondary Research

We analyze industry reports, trade publications, and market studies to offer tailored intelligence and actionable commodity market insights.

Trusted by 3000+ industry leaders worldwide to drive data-backed decisions. From global manufacturers to government agencies, our clients rely on us for accurate pricing, deep market intelligence, and forward-looking insights.