Electric Truck Market Size, Share, Trends and Forecast by Vehicle Type, Propulsion, Range, Application, and Region, 2026-2034

Electric Truck Market Size and Share:

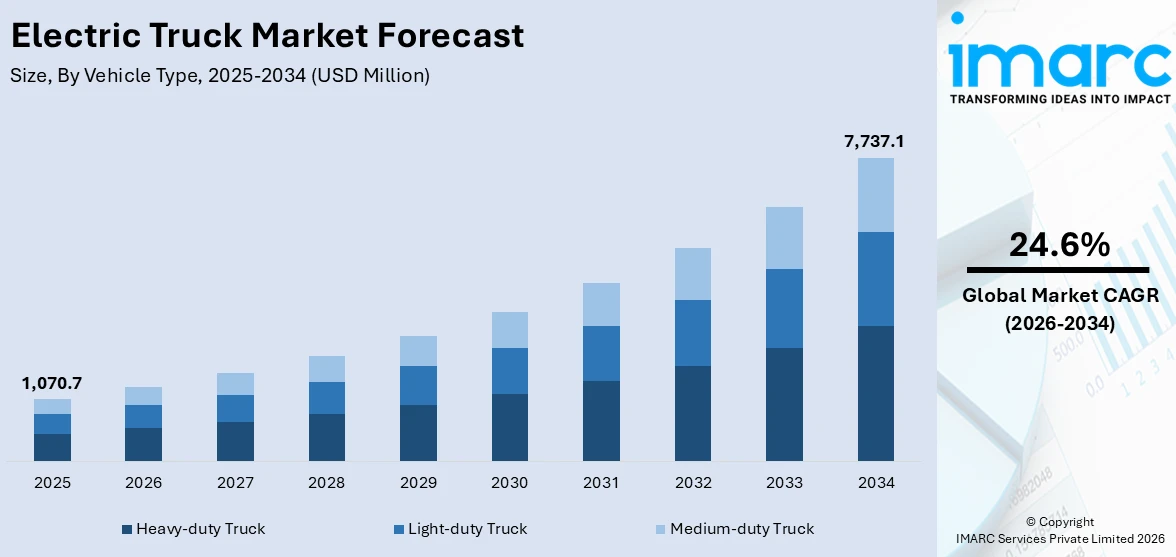

The global electric truck market size was valued at USD 1,070.7 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 7,737.1 Million by 2034, exhibiting a CAGR of 24.6% from 2026-2034. North America currently dominates the market, holding a market share of 31% in 2025. The region benefits from stringent government emission regulations, substantial federal and state incentives for zero-emission commercial vehicles, advanced charging infrastructure development along major freight corridors, and rising corporate commitments to sustainable fleet operations, all contributing to the electric truck market share.

The global electric truck market is being driven by a convergence of regulatory, economic, and technological factors. Governments worldwide are implementing increasingly stringent emission standards for commercial vehicles, compelling fleet operators to transition toward zero-emission alternatives. Advancements in battery technology, including higher energy density cells and improved thermal management systems, are extending the operational range and payload capacity of electric trucks, making them viable for a broader spectrum of logistics applications. The declining cost of lithium-ion battery packs is progressively narrowing the upfront price gap between electric and diesel-powered trucks, enhancing total cost of ownership competitiveness.

The United States has emerged as a major region in the electric truck market owing to many factors. Federal and state-level policies are creating a favorable ecosystem for electric truck adoption, with tax credits, purchase subsidies, and zero-emission vehicle mandates driving fleet electrification across the transportation sector. In March 2024, the U.S. Environmental Protection Agency finalized the Phase 3 greenhouse gas emission standards for heavy-duty vehicles, setting stricter national pollution requirements for trucks beginning with model year 2027 to support cleaner freight transport and accelerate deployment of zero-emission technology in the sector. Rising fuel costs and volatile diesel prices are further encouraging businesses to evaluate electric alternatives that offer lower and more predictable operating expenditures. The electric truck market outlook remains positive as logistics companies increasingly prioritize sustainable transportation solutions.

To get more information on this market Request Sample

Electric Truck Market Trends:

Rapid Growth in Battery Electric Truck Adoption

The accelerating adoption of battery electric trucks across global markets is significantly reshaping the commercial vehicle landscape. Fleet operators are increasingly transitioning to electric powertrains driven by favorable total cost of ownership calculations that account for lower fuel and maintenance expenditures over vehicle lifecycles. In 2024, global electric medium- and heavy-duty truck sales exceeded 90 000 units, rising nearly 80% year-on-year, with China accounting for over 80% of total sales, supported by renewed scrappage incentives and tighter emission standards. The operational advantages of electric trucks, including reduced noise levels, zero tailpipe emissions, and compliance with emerging urban low-emission zone regulations, are making them particularly attractive for last-mile delivery and urban logistics applications.

Advancements in Battery Technology and Range Extension

Continuous improvements in battery technology are extending the operational capabilities of electric trucks, enabling them to compete with conventional diesel vehicles across a wider range of applications. Higher energy density battery cells, advanced thermal management systems, and optimized powertrain architectures are collectively increasing vehicle range while minimizing weight penalties that impact payload capacity. Electric truck market trends indicate that manufacturers are rapidly closing the performance gap with diesel counterparts. In September 2024, Volvo Trucks announced its next‑generation heavy‑duty electric truck will deliver up to 600 km range on a single charge, enabling long‑distance zero‑emission freight operations without mid‑day recharging. Leading original equipment manufacturers are developing long-haul electric trucks with battery capacities exceeding traditional offerings and ranges suitable for regional and inter-city freight operations on a single charge. The integration of megawatt charging systems is further enhancing operational efficiency by enabling rapid recharging within mandated driver rest periods.

Expansion of Charging Infrastructure Networks

The rapid deployment of dedicated charging infrastructure for commercial electric vehicles (EVs) is removing a critical barrier to widespread electric truck adoption across global markets. Public and private investments in high-power charging stations along major freight corridors, at logistics hubs, and within fleet depots are creating the operational foundation necessary for electric truck market forecast expansion. In January 2025, the U.S. Department of Energy announced a $68 million investment under its SuperTruck Charge initiative to accelerate development of high‑capacity public charging sites for medium‑ and heavy‑duty electric trucks near ports, distribution hubs, and key corridors. Government-led initiatives across major economies are mandating the installation of heavy-duty vehicle charging stations at regular intervals along key transportation networks, ensuring comprehensive corridor coverage. Strategic partnerships between truck manufacturers, energy companies, and charging network operators are accelerating the buildout of comprehensive charging ecosystems that address the specific requirements of commercial trucking operations.

Electric Truck Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global electric truck market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on vehicle type, propulsion, range, and application.

Analysis by Vehicle Type:

- Light-duty Truck

- Medium-duty Truck

- Heavy-duty Truck

Heavy-duty truck holds 40% of the market share, engineered for demanding freight and logistics operations, including long-haul transportation, construction material hauling, and industrial supply chain applications. These vehicles are equipped with high-capacity battery technology and powerful powertrain solutions that can support high gross vehicle weight ratings and offer zero tailpipe emissions. The increasing focus on the decarbonization of heavy freight transport, which contributes to a disproportionately large share of total transportation-related greenhouse gas emissions, is driving major investments in the development of heavy-duty electric trucks. The manufacturers are continuously working on improving powertrain solutions to offer higher horsepower and torque ratings through electric powertrain solutions and optimizing battery technologies to support long lifetimes and fast-charging solutions. The launch of lithium iron phosphate battery solutions and energy management solutions is improving the reliability and efficiency of heavy-duty electric trucks.

Analysis by Propulsion:

- Battery Electric Truck

- Hybrid Electric Truck

- Plug-in Hybrid Electric Truck

- Fuel Cell Electric Truck

Battery electric truck leads the market with a share of 47%, utilizing fully electric powertrains powered by rechargeable lithium-ion battery packs, eliminating the need for internal combustion engines and delivering zero tailpipe emissions during operation. These vehicles offer significant advantages in terms of energy efficiency, with electric drivetrains converting a substantially higher percentage of stored energy into vehicle movement compared to diesel engines. As per sources, Daimler Truck announced that its Mercedes‑Benz eActros electric truck entered series production for European customers, marking one of the first large‑scale commercial deployments of heavy‑duty battery electric trucks in regional freight operations. The declining cost of battery packs, improved energy density, and expanding charging infrastructure are collectively enhancing the commercial viability of battery electric trucks across diverse applications. Battery electric trucks demonstrate superior energy efficiency compared to diesel heavy-duty trucks of equivalent size, resulting in considerably lower direct fuel costs across major markets globally.

Analysis by Range:

- 0-150 Miles

- 151-300 Miles

- Above 300 Miles

151-300 miles dominates the market, with a share of 38%, well-suited for regional delivery operations, inter-city freight transport, and logistics applications that require moderate daily driving distances with predictable route patterns. Electric trucks within this range segment offer an optimal balance between battery capacity, vehicle weight, and operational flexibility, making them attractive for fleet operators managing distribution networks across metropolitan areas and surrounding regions. The range capability allows for full-day operations without intermediate charging in many regional applications, while fast-charging technology provides the ability to extend daily operating distances when required. Leading manufacturers are developing collaborative transport solutions that demonstrate the viability of electric trucking along established freight corridors, showcasing substantial reductions in carbon dioxide emissions while maintaining high levels of vehicle utilization. Advancements in battery efficiency, regenerative braking systems, and energy management algorithms continue to improve the real-world range performance of electric trucks operating within this segment category.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Logistics

- Municipal

- Construction

- Mining

- Others

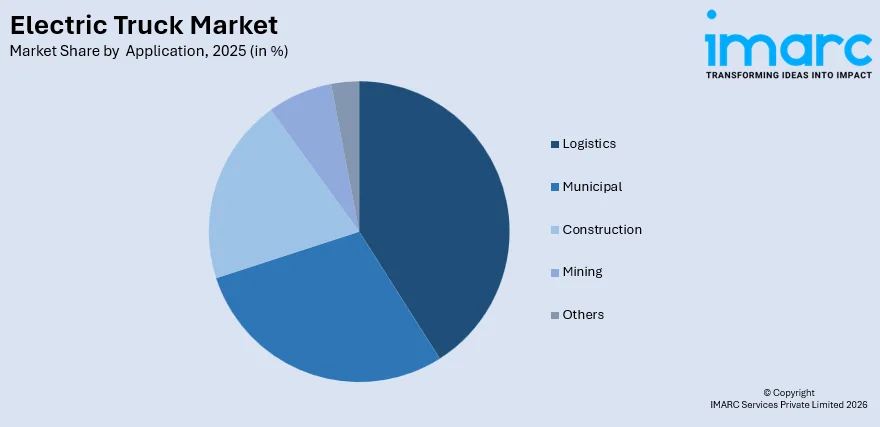

Logistics represents the leading segment, with a market share of 41%, driven by the high volume of goods movement, frequency of daily operations, and strong alignment between electric vehicle (EV) characteristics and logistics operational requirements. Electric trucks are particularly well-suited for urban and suburban delivery routes, last-mile logistics, and distribution center operations, where predictable driving patterns and return-to-base operations enable efficient charging management. The growing emphasis on sustainable supply chain practices among major retailers, e-commerce platforms, and parcel delivery companies is accelerating the electrification of logistics fleets worldwide. Leading global logistics operators are securing supply contracts for electric heavy-duty trucks to decarbonize their transportation networks, reflecting the increasing commercial readiness of electric trucking solutions for high-volume freight applications. The increasing availability of electric trucks across multiple duty cycles and weight classes is enabling comprehensive fleet electrification strategies for logistics operators seeking to reduce carbon footprints and operating costs simultaneously.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 31% of the share, underpinned by a comprehensive policy framework that includes stringent emission regulations, substantial financial incentives for zero-emission vehicle adoption, and significant government investment in charging infrastructure development. Federal programs and state-level mandates targeting zero-emission commercial vehicles are creating strong demand signals for electric truck manufacturers and fleet operators across the region. The presence of major electric truck manufacturers and technology companies is fostering continuous innovation in battery technology, autonomous driving integration, and charging solutions that address the operational needs of diverse commercial trucking applications. Corporate sustainability commitments from major logistics, retail, and e-commerce companies are further accelerating fleet electrification efforts. The well-established transportation network and growing depot charging infrastructure provide a supportive operational environment for electric trucks across urban delivery, drayage, and regional freight applications throughout the region.

Key Regional Takeaways:

United States Electric Truck Market Analysis

The United States electric truck market growth is experiencing substantial growth driven by a convergence of regulatory mandates, financial incentives, and evolving corporate sustainability priorities. Federal policies, including generous tax credits for qualifying commercial EVs and dedicated grant programs for heavy-duty zero-emission vehicle purchases, are significantly reducing the financial barriers to electric truck adoption. State-level regulations, particularly those requiring manufacturers to sell increasing percentages of zero-emission trucks, are establishing clear market direction for the industry and encouraging manufacturers to expand their electric truck portfolios. The expansion of charging infrastructure is creating a more supportive operational environment, with public and private investments increasing the availability of high-power charging stations along major freight corridors and at distribution hubs. Major logistics companies and fleet operators are increasingly committing to fleet electrification as part of broader environmental, social, and governance strategies aimed at reducing carbon emissions across supply chains. The growing availability of electric truck models across light-duty, medium-duty, and heavy-duty segments is enabling operators to match vehicle specifications with specific operational requirements.

Europe Electric Truck Market Analysis

The European electric truck market is supported by ambitious climate targets and comprehensive regulatory frameworks that are driving fleet electrification across the continent. The European Union's CO2 emission standards for heavy-duty vehicles, which mandate significant reductions in coming years compared to baseline levels, are creating strong incentives for manufacturers and fleet operators to transition toward zero-emission solutions. The expansion of heavy-duty vehicle charging infrastructure is progressing steadily, with an increasing number of charging locations deployed across the continent, including stations equipped with high-power charging capacity suitable for commercial trucking operations. Strategic joint ventures between leading commercial vehicle manufacturers to install high-performance charging points across European highways represent significant commitments to infrastructure development and industry collaboration. The proliferation of low-emission zones across European cities is further incentivizing the adoption of electric trucks for urban logistics operations, while national-level purchase subsidies and tax incentives are reducing acquisition costs for fleet operators seeking to modernize their commercial vehicle fleets with sustainable alternatives.

Asia-Pacific Electric Truck Market Analysis

The Asia-Pacific electric truck market is experiencing dynamic growth, led predominantly by China's rapidly expanding electric commercial vehicle sector. Government policies including vehicle scrappage schemes with purchase incentives, tightened emission standards, and substantial investments in battery-swapping infrastructure are driving widespread adoption across the region. Leading manufacturers expect battery- EVs to capture a dominant share of heavy-duty truck sales within the coming years, reflecting strong industry confidence in the electrification trajectory. Japan and South Korea are investing in electric truck technology and hydrogen fuel cell alternatives for heavy-duty applications, while India has allocated dedicated funding for electric truck purchase incentives to accelerate market development. The region benefits from established battery manufacturing ecosystems and competitive production costs that support aggressive pricing strategies and enable rapid scaling of electric truck production capacity.

Latin America Electric Truck Market Analysis

The Latin American electric truck market is at an emerging stage, with Brazil serving as the primary growth driver in the region. Government initiatives to reduce urban air pollution and promote EV adoption are creating foundational demand for electric commercial vehicles. The expansion of public charging infrastructure across major Brazilian cities and transportation corridors is improving the operational feasibility of electric trucking operations. Investments from international manufacturers establishing local production capabilities are enhancing vehicle availability and affordability in the region. Additionally, growing environmental awareness and corporate sustainability commitments among logistics companies are supporting the gradual transition toward electric commercial vehicles across urban delivery and distribution applications.

Middle East and Africa Electric Truck Market Analysis

The Middle East and Africa electric truck market is in the nascent stages of development, with adoption primarily concentrated in the United Arab Emirates and South Africa. Government diversification strategies away from fossil fuel dependence and emerging sustainability mandates are creating initial demand for electric commercial vehicles. Leading logistics operators in the region are pioneering commercial electric truck deployments, utilizing solar-powered charging infrastructure to reduce operational costs and demonstrate the viability of fleet electrification in regional climatic conditions. Growing e-commerce activity across the continent is driving demand for last-mile delivery solutions that align with sustainability objectives. Improving charging infrastructure availability and declining vehicle acquisition costs are expected to support gradual market expansion across the region.

Competitive Landscape:

The competitive landscape of the global electric truck market is characterized by the strategic activities of established automotive manufacturers, emerging EV specialists, and technology companies seeking to establish leadership positions in zero-emission commercial transportation. Leading players are investing heavily in research and development to advance battery technology, extend vehicle range, and reduce production costs, while simultaneously expanding manufacturing capacity to meet growing demand. Strategic partnerships between truck manufacturers, battery producers, and charging infrastructure providers are reshaping the competitive dynamics by creating integrated ecosystem solutions. Companies are pursuing diverse market entry strategies, ranging from premium long-haul electric trucks to cost-effective urban delivery vehicles, to capture opportunities across multiple market segments. Mergers, acquisitions, and joint ventures are accelerating, as industry participants seek to consolidate capabilities and strengthen their competitive positioning in a rapidly evolving market environment.

The report provides a comprehensive analysis of the competitive landscape in the electric truck market with detailed profiles of all major companies, including:

- VolvoGroup

- BYD Company Ltd.

- Mercedes-Benz Group AG

- China FAW Group Co. Ltd.

- Isuzu Motors Ltd.

- Navistar Inc.

- PACCAR Inc.

- Rivian Automotive Inc.

- Volkswagen AG

- Tata Motors Limited

- Tesla Inc.

- Tevva Motors Limited

Latest News and Developments:

- In April 2025, Windrose Technology launched the first all-electric long-haul sleeper truck in the U.S., featuring a 420-mile range. Partnering with JoyRide Logistics and EO Charging, the truck is set for deployment across Arizona, California, and Nevada, delivering zero-emission freight while achieving total cost of ownership parity for shippers.

- In February 2025, Renault Trucks and Schwing-Stetter unveiled the E-Tech C 10x4, a five-axle electric concrete mixer capable of carrying up to 10 m³ of concrete. Designed for urban manoeuvrability, it offers up to 140 km range, enabling four daily trips while delivering a zero-emission, decarbonised solution for the construction industry.

Electric Truck Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Light-Duty Truck, Medium-Duty Truck, Heavy-Duty Truck |

| Propulsions Covered | Battery Electric Truck, Hybrid Electric Truck, Plug-In Hybrid Electric Truck, Fuel Cell Electric Truck |

| Ranges Covered | 0-150 Miles, 151-300 Miles, Above 300 Miles |

| Applications Covered | Logistics, Municipal, Construction, Mining, Others |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | VolvoGroup, BYD Company Ltd., Mercedes-Benz Group AG, China FAW Group Co. Ltd., Isuzu Motors Ltd, Navistar Inc., PACCAR Inc., Rivian Automotive Inc., Volkswagen AG, Tata Motors Limited, Tesla Inc., Tevva Motors Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the electric truck market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global electric truck market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the electric truck industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The electric truck market was valued at USD 1,070.7 Million in 2025.

The electric truck market is projected to exhibit a CAGR of 24.6% during 2026-2034, reaching a value of USD 7,737.1 Million by 2034.

The electric truck market is driven by stringent government emission regulations, declining battery costs improving total cost of ownership, expanding charging infrastructure networks, growing corporate sustainability commitments, and rising demand for zero-emission logistics solutions. Advancements in battery technology extending vehicle range and reducing charging times are further accelerating adoption across urban delivery and regional freight applications.

North America currently dominates the electric truck market, accounting for a share of 31%. The region benefits from comprehensive regulatory frameworks, substantial government incentives, advanced charging infrastructure, and strong corporate demand for sustainable freight transportation solutions.

Some of the major players in the electric truck market include VolvoGroup, BYD Company Ltd., Mercedes-Benz Group AG, China FAW Group Co. Ltd., Isuzu Motors Ltd, Navistar Inc., PACCAR Inc., Rivian Automotive Inc., Volkswagen AG, Tata Motors Limited, Tesla Inc., Tevva Motors Limited., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)