Drug-Eluting Stents Market Report by Coating (Polymer Based Coating, Polymer Free Coating), Drug (Sirolimus, Paclitaxel, Zotarolimus, Everolimus, Biolimus, and Others), Stent Platform (Stainless-steel, Cobalt-Chromium, Platinum-Chromium, Nitinol, and Others), Generation (1st Generation, 2nd Generation, 3rd Generation, 4th Generation), Application (Coronary Artery Disease, Peripheral Artery Disease), End User (Hospitals, Ambulatory Surgical Centers, and Others), and Region 2026-2034

Global Drug-Eluting Stents Market:

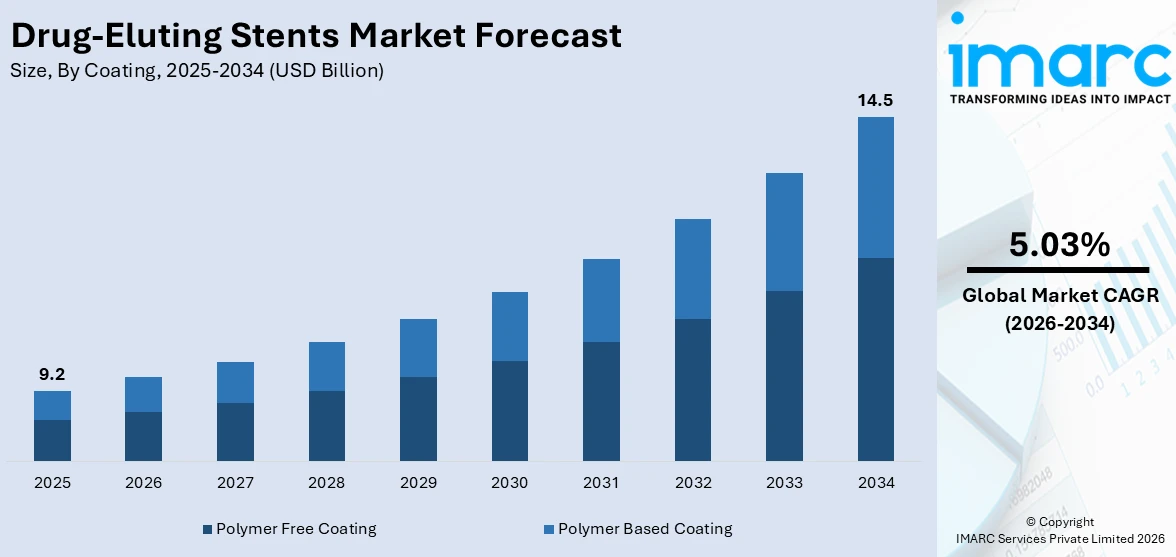

The global drug-eluting stents market size reached USD 9.2 Billion in 2025. Looking forward, the market is expected to reach USD 14.5 Billion by 2034, exhibiting a growth rate (CAGR) of 5.03% during 2026-2034. The increasing prevalence of cardiovascular diseases is propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 9.2 Billion |

|

Market Forecast in 2034

|

USD 14.5 Billion |

| Market Growth Rate 2026-2034 | 5.03% |

Drug-Eluting Stents Market Analysis:

- Major Market Drivers: The increasing prevalence of irregular heart rhythms, heart failure, and heart attack disease is stimulating the market.

- Key Market Trends: The widespread use of stents with polymer-free coatings is acting as a significant growth-inducing factor.

- Competitive Landscape: Some of the major market companies include Abbott, B. Braun SE, Biosensors International Group, Ltd., Biotronik, Boston Scientific Corporation, Cook Medical, Lepu Medical Technology (Beijing) Co., Ltd, Medinol, Medtronic plc, MicroPort Scientific Corporation, Sino Medical Sciences Technology Inc and Terumo Corporation, among many others.

- Geographical Trends: North America dominates the market owing to a robust healthcare system, rising incidence of coronary artery disease, and extensive use of innovative medical technologies.

- Challenges and Opportunities: The risk of late stent thrombosis is hampering the market. However, developing innovative stent technologies with greater biocompatibility and polymer-free coatings to increase patient safety is expected to fuel the market in the coming years.

To get more information on this market Request Sample

Drug-Eluting Stents Market Trends:

Implementation of Next-Generation Drugs

The next generation of drug-eluting stents uses advanced medications, such as biolimus and zotarolimus, which have higher efficacy in preventing restenosis while reducing adverse effects, making these stents more useful for a wider variety of patients. For example, in May 2024, Abbott announced the launch of XIENCE Sierra Everolimus (drug) eluting coronary stent system in India. It is a CE-marked and one of the latest generation stents in the XIENCE family, now available to people suffering from blocked coronary arteries. This is leading to the drug-eluting stents market growth.

Expanded Use in Peripheral Artery Disease

Drug-eluting stents are being increasingly utilized to treat peripheral arterial disease (PAD), moving beyond coronary applications. This trend reflects stents' growing use in treating blockages in arteries beyond the heart. In April 2024, Cook Medical received a contract to supply implantable devices to hospitals run by the U.S. Department of Defense (DoD). The company would provide its Zilver PTX drug-eluting peripheral stent, Zenith aortic endograft, and other implantable devices. This is expanding the drug-eluting stents market share.

Increasing Focus on Complex Lesions

Drug-eluting stents are in high demand for treating complicated coronary lesions such as bifurcation and multi-vessel disease. These advanced stents are designed to handle complex anatomical issues with more precision. In June 2024, Elixir Medical's DynamX Sirolimus-Eluting Coronary Bioadaptor System received Breakthrough Device Designation from the FDA. This bioadaptive implant aims to improve coronary luminal diameter, restore hemodynamic modulation, and reduce plaque progression in patients with symptomatic ischemic heart disease.

Global Drug-Eluting Stents Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with the drug-eluting stents market forecast at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on the coating, drug, stent platform, generation, application, and end user.

Breakup by Coating:

- Polymer Based Coating

- Polymer Free Coating

Among these, polymer free coating holds the largest share of the drug-eluting stents market

The report has provided a detailed breakup and analysis of the market based on the coating. This includes polymer based coating and polymer free coating. According to the report, polymer free coating represented the largest market segmentation.

Polymer free coating is intended to minimize inflammation and promote healing. These coatings improve medication delivery while eliminating the problems associated with polymers, resulting in better patient outcomes during cardiovascular treatments. This is elevating the drug-eluting stents market revenue.

Breakup by Drug:

- Sirolimus

- Paclitaxel

- Zotarolimus

- Everolimus

- Biolimus

- Others

The report has provided a detailed breakup and analysis of the market based on the drug. This includes sirolimus, paclitaxel, zotarolimus, everolimus, biolimus, and others.

The drug-eluting stents market overview highlights that sirolimus reduces cell development to avoid arterial narrowing, while paclitaxel inhibits cell division, resulting in better blood flow. Zotarolimus enhances healing while causing less adverse effects, and everolimus has been shown to reduce re-narrowing over time. Biolimus, a biodegradable alternative, promotes vascular recovery, providing a variety of therapy options in the market.

Breakup by Stent Platform:

- Stainless-steel

- Cobalt-Chromium

- Platinum-Chromium

- Nitinol

- Others

Cobalt-chromium currently holds the largest drug-eluting stents market demand

The report has provided a detailed breakup and analysis of the market based on the stent platform. This includes stainless-steel, cobalt-chromium, platinum-chromium, nitinol, and others. According to the report, cobalt-chromium represented the largest market segmentation.

Cobalt-chromium stents are well-known for their long-lasting, flexible, and biocompatible design. These stents have a sturdy construction but allow for thinner struts, which improves vessel support and reduces problems during cardiovascular treatments. This is elevating the drug-eluting stents market statistics.

Breakup by Generation:

- 1st Generation

- 2nd Generation

- 3rd Generation

- 4th Generation

The report has provided a detailed breakup and analysis of the market based on the generation. This includes 1st generation, 2nd generation, 3rd generation, and 4th generation.

The 1st generation drug-eluting stents used basic drug coatings to minimize restenosis. The 2nd generation increased safety by improving biocompatibility and using thinner struts. The 3rd generation focused on biodegradable polymers to improve healing, while the 4th generation uses polymer-free coatings to promote speedier recovery and reduce inflammation. Each generation represents advances in safety, efficacy, and patient outcomes.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Coronary Artery Disease

- Peripheral Artery Disease

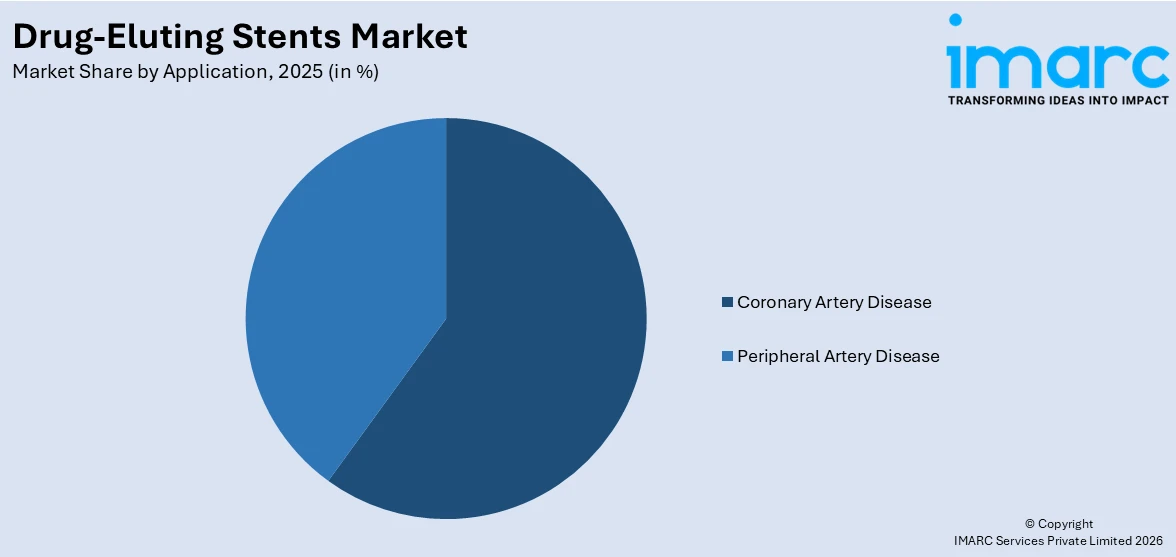

Currently, coronary artery disease holds the largest share of the drug-eluting stents market recent price

The report has provided a detailed breakup and analysis of the market based on the application. This includes coronary artery disease and peripheral artery disease. According to the report, coronary artery disease represented the largest market segmentation.

The market largely focuses on coronary artery disease by releasing medications that prevent restenosis. These stents help to maintain artery patency, improve blood flow, and reduce the need for repeat treatments in patients with blocked or narrowed arteries.

Breakup by End User:

- Hospitals

- Ambulatory Surgical Centers

- Others

Among these, hospitals currently hold the largest share of the market

The report has provided a detailed breakup and analysis of the market based on the end user. This includes hospitals, ambulatory surgical centers, and others. According to the report, hospitals represented the largest market segmentation.

Hospitals are the primary end users in this market, as these devices are commonly utilized in cardiovascular surgeries to treat coronary artery disease. These stents are used in hospitals to improve patient outcomes, lower restenosis, and reduce the need for recurrent treatments. This represents one of the drug-eluting stents market recent opportunities.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America currently dominates the drug-eluting stents market outlook

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia-Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America exhibits a clear dominance in the market. This can be attributed to the enhanced healthcare infrastructure, a high prevalence of cardiovascular illnesses, and the growing adoption of cutting-edge stent technology. The region's focus on reducing coronary artery disease promotes demand for these devices.

Competitive Landscape:

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major drug-eluting stents market companies have also been provided. Some of the key players in the market include:

- Abbott

- B. Braun SE

- Biosensors International Group, Ltd.

- Biotronik

- Boston Scientific Corporation

- Cook Medical

- Lepu Medical Technology (Beijing) Co., Ltd

- Medinol

- Medtronic plc

- MicroPort Scientific Corporation

- Sino Medical Sciences Technology Inc

- Terumo Corporation

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Drug-Eluting Stents Market Recent Developments:

- June 2024: Elixir Medical's DynamX Sirolimus-Eluting Coronary Bioadaptor System received Breakthrough Device Designation from the FDA. This bioadaptive implant aims to improve coronary luminal diameter, restore hemodynamic modulation, and reduce plaque progression in patients with symptomatic ischemic heart disease.

- May 2024: Abbott announced the launch of XIENCE Sierra Everolimus (drug) eluting coronary stent system in India. It is a CE-marked and one of the latest generation stents in the XIENCE family.

- April 2024: Cook Medical received a contract to supply implantable devices to hospitals run by the U.S. Department of Defense (DoD). The company would provide its Zilver PTX drug-eluting peripheral stent, Zenith aortic endograft, and other implantable devices.

Drug-Eluting Stents Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Coatings Covered | Polymer Based Coating, Polymer Free Coating |

| Drugs Covered | Sirolimus, Paclitaxel, Zotarolimus, Everolimus, Biolimus, Others |

| Stent Platforms Covered | Stainless-steel, Cobalt-Chromium, Platinum-Chromium, Nitinol, Others |

| Generations Covered | 1st Generation, 2nd Generation, 3rd Generation, 4th Generation |

| Applications Covered | Coronary Artery Disease, Peripheral Artery Disease |

| End Users Covered | Hospitals, Ambulatory Surgical |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott, B. Braun SE, Biosensors International Group, Ltd., Biotronik, Boston Scientific Corporation, Cook Medical, Lepu Medical Technology (Beijing) Co., Ltd, Medinol, Medtronic plc, MicroPort Scientific Corporation, Sino Medical Sciences Technology Inc, Terumo Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the drug-eluting stents market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global drug-eluting stents market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the drug-eluting stents industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global drug-eluting stents market was valued at USD 9.2 Billion in 2025.

We expect the global drug-eluting stents market to exhibit a CAGR of 5.03% during 2026-2034.

The rising need for drug-eluting stents to treat blockages in heart arteries, prevent plaque buildup and blood clots, reduce repeated revascularization, etc., is primarily driving the global drug-eluting stents market.

The sudden outbreak of the COVID-19 pandemic had led to the postponement of elective cardiovascular surgeries to minimize the risk of the coronavirus infection during hospital visits, thereby negatively impacting the global market for drug-eluting stents.

Based on the coating, the global drug-eluting stents market has been segmented into polymer based coating and polymer free coating. Currently, polymer free coating holds the majority of the total market share.

Based on the stent platform, the global drug-eluting stents market can be categorized into stainless-steel, cobalt-chromium, platinum-chromium, nitinol, and others. Among these, cobalt-chromium currently exhibits a clear dominance in the market.

Based on the application, the global drug-eluting stents market has been bifurcated into coronary artery disease and peripheral artery disease. Currently, coronary artery disease holds the largest market share.

Based on the end user, the global drug-eluting stents market can be divided into hospitals, ambulatory surgical centers, and others. Among these, hospitals account for the majority of the global market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global drug-eluting stents market include Abbott, B. Braun SE, Biosensors International Group, Ltd., Biotronik, Boston Scientific Corporation, Cook Medical, Lepu Medical Technology (Beijing) Co., Ltd, Medinol, Medtronic plc, MicroPort Scientific Corporation, Sino Medical Sciences Technology Inc, and Terumo Corporation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)