Defibrillators Market Report by Product Type (Implantable Defibrillators, External Defibrillators), End-User (Hospitals and Clinics, Prehospital Care Settings, Cardiac Centers, Homecare Settings, and Others), and Region 2026-2034

Defibrillators Market Overview:

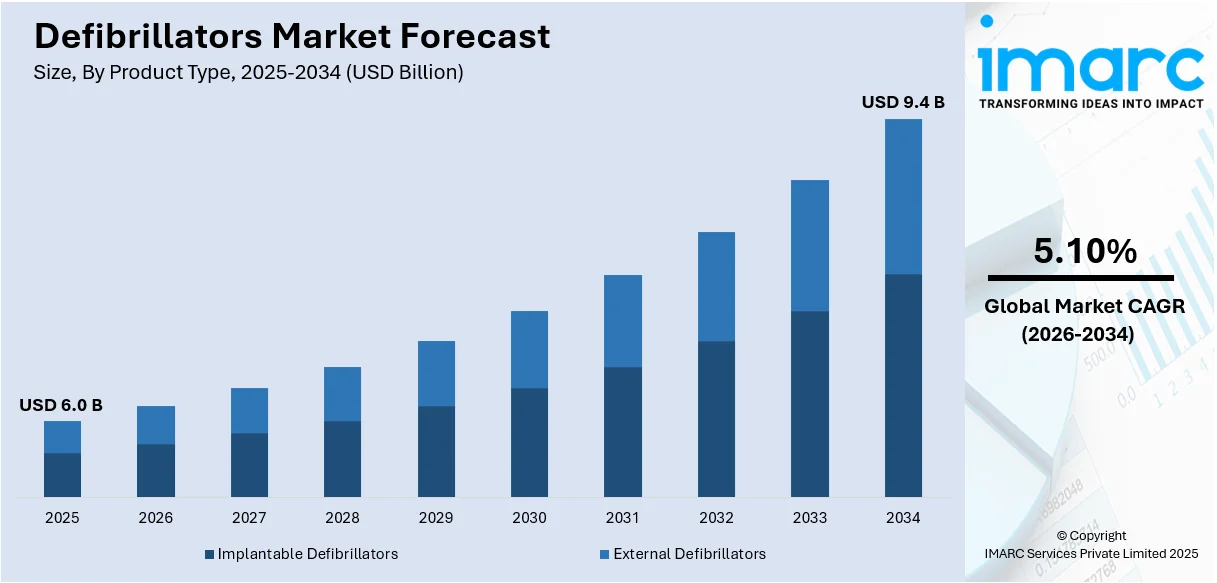

The global defibrillators market size reached USD 6.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 9.4 Billion by 2034, exhibiting a growth rate (CAGR) of 5.10% during 2026-2034. The increasing incidence of heart diseases, such as coronary artery disease and arrhythmias, rising number of public access locations, and the growing number of ambulance services are some of the major factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 6.0 Billion |

| Market Forecast in 2034 | USD 9.4 Billion |

| Market Growth Rate 2026-2034 | 5.10% |

Defibrillators are medical devices designed to restore a normal heartbeat by delivering an electrical shock to the heart. They are designed to be user friendly to ensure that people without medical training can also operate them in emergency situations. They are crucial in emergency situations involving cardiac arrest, which is a condition wherein the heart suddenly stops beating effectively. They provide an electrical shock that can jolt the heart back into a normal rhythm, which potentially saves the life of an individual. They are commonly used in hospitals, ambulances, and public places like airports and shopping malls.

To get more information on this market Request Sample

Increasing incidence of heart diseases, such as coronary artery disease and arrhythmias, is driving the demand for defibrillators around the world. Moreover, the rising number of public access locations, including malls, parks, and transportation hubs, is favoring the growth of the market. In addition, the growing number of ambulance services that are equipped with defibrillators in vehicles to enhance emergency medical care during transit is influencing the market positively. Apart from this, the expansion of the sports and fitness industry is increasing the adoption of defibrillators in gyms, sports facilities, and recreational areas. Furthermore, the surging prevalence of obesity, which is correlated with a higher risk of cardiac issues, is bolstering the market growth.

Defibrillators Market Trends/Drivers:

Increasing awareness about cardiac health

The demand for defibrillators is on a rise due to the increasing awareness about cardiac health among the masses. Individuals and organizations are becoming more cognizant of the risks associated with sudden cardiac arrest (SCA), which can strike anyone, anywhere. This heightened awareness has led to a proactive approach in preparedness. Schools, offices, public spaces, and even households are recognizing the importance of having defibrillators readily available. The potential to save lives in critical moments has driven the demand. Moreover, educational campaigns and training initiatives have demystified the use of defibrillators, making them more accessible and user-friendly.

Rise in aging population and chronic diseases

The aging population worldwide is another significant factor catalyzing the demand for defibrillators. As people age, the risk of cardiac-related issues increases. Moreover, the surging prevalence of chronic diseases, such as hypertension and diabetes has also risen. These conditions can lead to heart problems, which makes defibrillators a crucial medical device for emergency response. Healthcare facilities, senior living communities, and home care providers are all investing in defibrillators to ensure timely intervention in case of cardiac emergencies. This demographic shift is expected to sustain and further catalyzing the demand for defibrillators.

Growing legislation and regulatory mandates

Regulatory mandates and legislation have played a pivotal role in driving the demand for defibrillators. Many countries and regions have implemented laws requiring specific locations, such as airports, sports stadiums, and public buildings, to have automated external defibrillators (AEDs) readily available. This legal framework has created a compelling need for organizations to comply with these requirements, thus leading to increased procurement of defibrillators. Additionally, industries with high occupational health and safety standards like construction and manufacturing are investing in defibrillators to ensure compliance and enhance workplace safety. The convergence of legislation and safety regulations has made defibrillators an indispensable component of emergency response infrastructure.

Defibrillators Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels from 2026-2034. Our report has categorized the market based on product type, and end-user.

Breakup by Product Type:

- Implantable Defibrillators

- Transvenous Implantable Cardioverter Defibrillator (T-ICDs)

- Subcutaneous Implantable Cardioverter Defibrillator (S-ICDs)

- Cardiac Resynchronization Therapy Defibrillator (CRT-D)

- External Defibrillators

- Manual External Defibrillator

- Automated External Defibrillator (AEDs)

- Wearable Cardioverter Defibrillator (WCDs)

Automated external defibrillator (AEDs) dominate the market

The report has provided a detailed breakup and analysis of the market based on the product type. This includes implantable defibrillators [transvenous implantable cardioverter defibrillator (T-ICDs), subcutaneous implantable cardioverter defibrillator (S-ICDs), and cardiac resynchronization therapy defibrillator (CRT-D)] and external defibrillators [manual external defibrillator, automated external defibrillator (AEDs), and wearable cardioverter defibrillator (WCDs)]. According to the report, automated external defibrillator (AEDs) represented the largest segment. AEDs are designed to be used by the public and are commonly found in public places like schools, airports, and shopping centers. They come with pre-set energy levels and automated voice instructions, making them user-friendly. They can automatically analyze the heart rhythm of the patients and advise whether a shock is needed, which ensures that the device is not misused.

T-ICDs are inserted into the body via a vein, typically in the upper chest area. They are connected to the heart through leads placed inside the veins. The device continually monitors the rhythm of the heart and automatically administers an electrical shock when it detects dangerous arrhythmias. T-ICDs are commonly used in patients who have had previous episodes of sudden cardiac arrest or are at high risk for it.

Breakup by End-User:

Access the comprehensive market breakdown Request Sample

- Hospitals and Clinics

- Prehospital Care Settings

- Cardiac Centers

- Homecare Settings

- Others

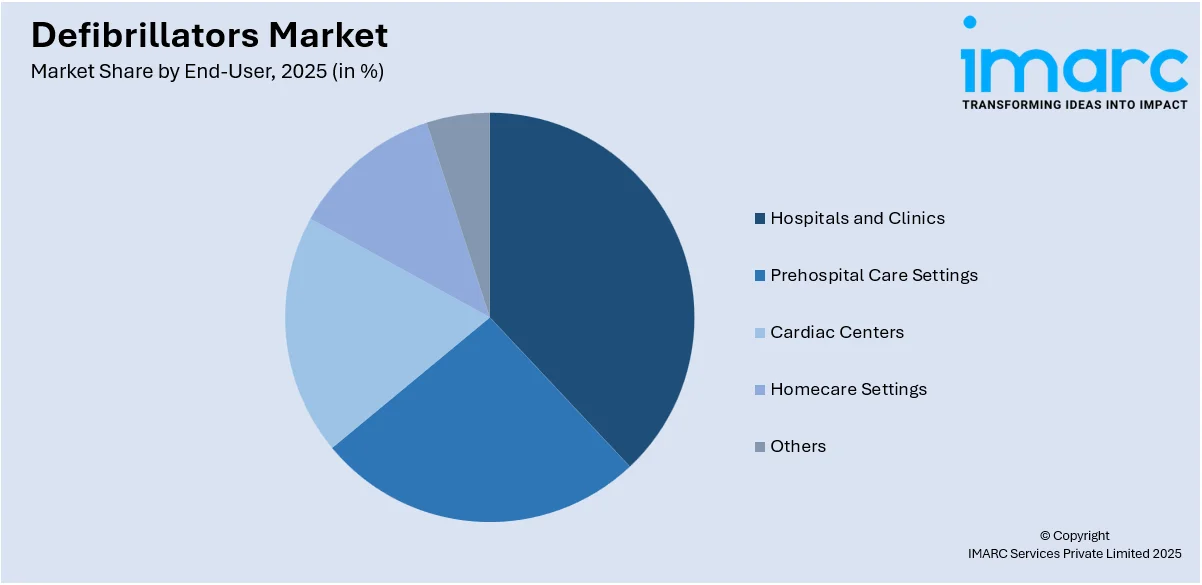

Hospitals and clinics hold the largest share in the market

A detailed breakup and analysis of the market based on the end-user has also been provided in the report. This includes hospitals and clinics, prehospital care settings, cardiac centers, homecare settings, and others. According to the report, hospitals and clinics accounted for the largest market share. In hospitals and clinics, defibrillators are a standard part of the medical equipment available for emergency care. Usually, these healthcare settings use manual external defibrillators, which allow medical professionals more control over the treatment process. These devices are often integrated into advanced life-support systems and used in conjunction with other monitoring equipment to provide comprehensive care. The staff in these settings are typically well-trained in the use of these sophisticated devices, which ensures that patients who experience cardiac emergencies have immediate access to potentially life-saving interventions. Hospitals and clinics are controlled environments with skilled personnel and they are often best suited for managing complex or high-risk cardiac events.

Prehospital care settings refer to emergency medical services that are administered before a patient arrives at a hospital. This can include care given by paramedics in ambulances or first responders at the scene of a medical emergency. In these settings, AEDs or portable manual external defibrillators are commonly used. AEDs are especially useful in this context because they can be operated by a broader range of medical personnel and even by bystanders under guidance, allowing for more immediate intervention. Prehospital care providers often receive specialized training in cardiac life support, which includes the effective use of defibrillators.

Breakup by Region:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance, accounting for the largest defibrillators market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

The surging prevalence of cardiovascular-related health issues represents one of the primary factors driving the demand for defibrillators in the North America region. Moreover, the rising public awareness about the risks of sudden cardiac arrest is favoring the growth of the market in the region. Besides this, a well-established healthcare facilities are influencing the market positively in the region.

Asia Pacific is estimated to witness stable growth, owing to ongoing research and development (R&D) projects, government initiatives, integration of advanced technologies, etc.

Competitive Landscape:

The leading companies are developing advanced defibrillators that are equipped with real time monitoring and feedback mechanisms to provide instant analysis of a heart rhythm of a patient and offer guidance to the operator, which improves the chances of successful defibrillation. Moreover, key players are introducing defibrillators integrated with touch screen technology, voice-guided prompts, and visual aids to reduce the time it takes to administer life-saving treatment. They are also adopting the usage of wireless connectivity that allows for remote monitoring and data analysis and enables healthcare providers to keep track of device performance and patient data seamlessly, which can be invaluable for post-care assessment and ongoing treatment planning.

The report has provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Asahi Kasei Zoll Medical Corporation

- Biotronik

- Boston Scientific Corporation

- Koninklijke Philips N.V.

- LivaNova PLC

- Medtronic Inc.

- Nihon Kohden Corporation

- Schiller AG

- Shenzhen Mindray Bio-Medical Electronics Co. Ltd.

- Stryker Corporation

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Recent Developments:

- In 2020, Koninklijke Philips N.V. announced that its Emergency Care and Resuscitation (ECR) business recommenced the US manufacturing and shipping of external defibrillators.

- In 2022, Medtronic Inc. declared that its investigational EV ICD™ System – a first-of-its-kind defibrillator with the lead placed under the breastbone, outside of the heart and veins – achieved a defibrillation success rate of 98.7% and met its safety endpoints in a global clinical trial.

- In July 2021, Asahi Kasei Zoll Medical Corporation stated that it has received FDA 510(k) clearance to release the TBI Dashboard™ feature on its Propaq® M monitor and Propaq MD monitor/defibrillator.

Defibrillators Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| End-Users Covered | Hospitals and Clinics, Prehospital Care Settings, Cardiac Centers, Homecare Settings, Others |

| Region Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia Brazil, Mexico |

| Companies Covered | Asahi Kasei Zoll Medical Corporation, Biotronik, Boston Scientific Corporation, Koninklijke Philips N.V., LivaNova PLC, Medtronic Inc., Nihon Kohden Corporation, Schiller AG, Shenzhen Mindray Bio-Medical Electronics Co. Ltd., Stryker Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global defibrillators market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global defibrillators market?

- What is the impact of each driver, restraint, and opportunity on the global defibrillators market?

- What are the key regional markets?

- Which countries represent the most attractive defibrillators market?

- What is the breakup of the market based on the product type?

- Which is the most attractive product type in the defibrillators market?

- What is the breakup of the market based on the end-user?

- Which is the most attractive end-user in the defibrillators market?

- What is the competitive structure of the global defibrillators market?

- Who are the key players/companies in the global defibrillators market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the defibrillators market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global defibrillators market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the defibrillators industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)