Data Classification Market Size, Share, Trends and Forecast by Component, Type, Deployment Mode, Application, Industry Vertical, and Region, 2025-2033

Data Classification Market Size and Share:

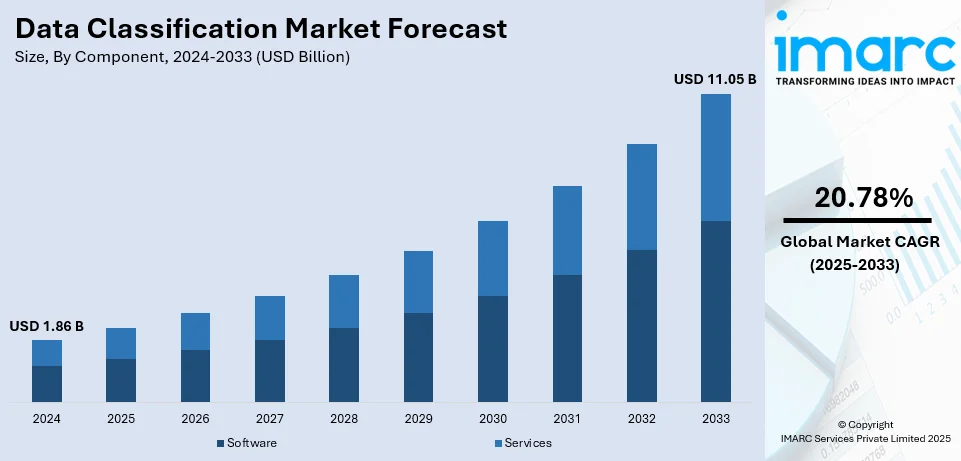

The global data classification market size was valued at USD 1.86 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 11.05 Billion by 2033, exhibiting a CAGR of 20.78% during 2025-2033. North America currently dominates the market, holding a significant market share of over 32.8% in 2024. The growing need to maintain data integrity and confidentiality, rising volumes of unstructured data, and the implementation of stringent government rules and regulations represent some of the key factors driving the market.

|

Report Attribute

|

Key Statistics |

|---|---|

|

Base Year

|

2024 |

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 1.86 Billion |

| Market Forecast in 2033 | USD 11.05 Billion |

| Market Growth Rate (2025-2033) | 20.78% |

Key drivers influencing the global data classification industry mainly encompass the escalating concerns regarding cybersecurity, magnifying sets of unstructured data, and the rapid increase in sophistication of data privacy policies. Several enterprises are currently witnessing the complication of managing huge sets of data, positioning classification as requisite service for effective security, storage, and retrieval. Besides this, regulatory policies, for instance HIPAA or GDPR, make it essential to opt for stricter data management methodologies, bolstering need for classification services. In addition, the rapid emergence in data breachers as well as cyber threats escalated the requirement for resilient data protection tactics, further boosting market demand globally. Furthermore, technological innovations in both machine learning and AI also foster the utilization of data classification services.

The United States holds a crucial position in the global market for data classification, typically being impacted by its leading-edge technological infrastructure and stricter implementation of regulatory policies. The nation’s significant number of enterprises across crucial industries, majorly encompassing government, finance, and healthcare make it essential to navigate for resilient data classification services that can effectively aid in adherence with regulatory frameworks. In addition to this, the amplifying incidents of data breaches or cyber-attacks heightens the requirement for improved data security strategies. For instance, in December 2024, Phreesia, a U.S.-based healthcare SaaS firm, revealed that more than 910,000 individuals' health as well as personal data was compromised due to a data breach. Besides, the robust establishment of leading industry players and heavy investments in ML as well as AI-based techniques further fortify the U.S.'s dominance in bolstering advancements along with market expansion in data classification.

Data Classification Market Trends:

Rising Need for Data Integrity and Confidentiality

As industries such as BFSI, government, healthcare, and retail handle increasingly sensitive user data, the demand for maintaining data integrity and confidentiality is growing. In these sectors, securing user information is paramount due to the potential for financial losses and reputational damage resulting from data breaches. According to reports, unstructured data is growing at an astounding rate of 55-65% annually. Resultantly, organizations face mounting challenges in managing and protecting such data. Data classification plays a crucial role in transforming this unstructured data into a structured format, making it easier to apply necessary protection measures and derive valuable insights. This growing need for security and efficient data handling is propelling the market forward.

Compliance Challenges and Cybersecurity Threats

Governments worldwide are enforcing stricter regulations concerning data privacy and usage, leading to complex compliance requirements for large organizations. Enterprises face significant risks, including hefty fines, for failing to meet these regulatory standards. This has sparked a surge in demand for data classification tools that ensure proper data handling and mitigate non-compliance risks. Additionally, the rise in cyber threats, such as data breaches, malware attacks, and ransomware, exacerbates the situation. According to reports, the number of data breached records in 2023 was 8,214,886,660, highlighting the urgent need for enhanced data security solutions. This increase in data thefts and the need for compliance are key drivers behind the growing adoption of data classification technologies.

Technological Advancements in Data Classification

Technological innovations are significantly transforming the data classification market, with big data and machine learning technologies leading the charge. These advancements allow for more accurate, efficient, and scalable classification processes, improving both data security and management. By automating the classification of vast datasets, organizations can identify and secure sensitive information more effectively. Furthermore, technological progress is not limited to data classification alone. As per the Ministry of External Affairs Government of India, digital transformation in India will create a USD 1 Trillion economy by 2028. This digital shift will accelerate the adoption of data-driven technologies, fueling further growth in the data classification sector as businesses embrace new tools for securing and managing their data.

Data Classification Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global data classification market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on component, type, deployment mode, application, and industry vertical.

Analysis by Component:

- Software

- Services

The global data classification market is heavily steered by the software segment, driven by increasing regulatory requirements, data security concerns, and the rapid expansion of digital enterprises. Organizations are deploying advanced classification software to automate data tagging, improve information governance, and ensure compliance with regulations such as GDPR, HIPAA, and CCPA. Artificial intelligence and machine learning are enhancing classification accuracy, reducing manual effort, and mitigating risks associated with unauthorized data access. Cloud-based solutions are gaining traction, offering scalability, real-time monitoring, and seamless integration with existing enterprise security frameworks. Large enterprises and government agencies are investing in robust software tools to manage structured and unstructured data efficiently. The demand for intelligent classification solutions continues to grow as businesses prioritize cybersecurity, operational efficiency, and regulatory adherence.

The services segment holds the largest market share in the global data classification industry, driven by the growing demand for consulting, implementation, and managed services. Enterprises seek expert guidance to deploy classification frameworks, optimize data governance strategies, and comply with evolving regulatory mandates. Professional services providers offer tailored solutions, addressing industry-specific security requirements and risk management challenges. Managed services are gaining prominence as businesses outsource classification processes to specialized vendors, ensuring continuous monitoring and compliance without additional in-house resource allocation. The rise of hybrid and multi-cloud environments is increasing the need for integration services, enhancing interoperability across IT infrastructures. As organizations focus on data-driven decision-making, service providers play a crucial role in helping businesses extract actionable insights while maintaining security and regulatory compliance.

Analysis by Type:

- Content-based Classification

- Context-based Classification

- User-based Classification

User-based classification leads the market in 2024, allowing organizations to categorize data according to user profiles, roles, and access levels. This approach ensures that critical data is only available to validated personnels, enhancing data security and minimizing the risk of internal breaches. User-based classification also facilitates efficient data governance by establishing clear parameters for data access, modification, and sharing. As organizations increasingly adopt digital platforms, the demand for this classification method has grown, particularly in industries handling sensitive information, such as healthcare and finance. By applying user-specific classifications, businesses can tailor data protection measures more effectively, reduce operational risks, and ensure compliance with regulatory standards. Furthermore, the ability to track and audit data usage by user profile provides an added layer of security, making it a fundamental strategy for organizations striving to protect proprietary and confidential data.

Analysis by Deployment Mode:

- On-premises

- Cloud-based

The on-premises deployment mode is prominent in the global data classification market due to its strong security and control features, which are highly valued by organizations dealing with sensitive data. This model enables businesses to store and manage data within their own infrastructure, ensuring that critical information is under direct supervision and protected by internal security measures. Industries such as healthcare, finance, and government, where data privacy is paramount, prefer on-premises solutions to meet regulatory compliance requirements and minimize exposure to external threats. Additionally, the flexibility to customize security protocols and access controls makes on-premises solutions attractive for large enterprises with complex data protection needs. As such, on-premises deployment continues to hold a significant market share, driven by the need for secure and highly controlled environments.

Cloud-based deployment mode is rapidly gaining traction in the global data classification market because of its high cost-efficiency, scalability, and convenience of access. The cloud allows organizations to manage and classify data without the constraints of on-premises infrastructure, making it an attractive option for businesses seeking flexibility and efficiency. This mode is particularly popular among small and medium-sized enterprises (SMEs) and global organizations with distributed teams, as it enables centralized data management across multiple locations. Cloud platforms also offer enhanced disaster recovery capabilities and automatic updates, reducing operational burdens. With the growing trend of digital transformation, the cloud-based deployment model is expected to continue gaining market share, driven by its ability to support dynamic, remote, and hybrid work environments while ensuring compliance with evolving data protection regulations.

Analysis by Application:

- Access Control

- Governance and Regularity Compliance

- Web, Mobile and Email Protection

- Auditing and Reporting

- Others

Governance and regularity compliance leads the market share in 2024. The global data classification market is significantly propelled by the escalating requirement for organizations to adhere to stringent regulations, involving HIPAA or CCPA, which mandate resilient data protection methods. Data classification enables businesses to comply with these regulatory requirements by ensuring that sensitive data is properly identified, categorized, and protected according to predefined guidelines. Regulatory compliance is particularly important for organizations in industries like healthcare, finance, and government, where the penalties for non-compliance can be severe. Moreover, regulatory bodies are constantly updating requirements to address new threats, including cyber-attacks and data breaches. As a result, businesses must continuously update their data classification practices to stay compliant. The integration of automated tools, machine learning, and AI into data governance frameworks further streamlines the compliance process, ensuring data is classified and protected in real time.

Analysis by Industry Vertical:

- BFSI

- Healthcare

- Government and Defense

- IT and Telecom

- Energy and Utilities

- Others

BFSI leads the market share in 2024, driven by the critical need for safeguarding sensitive financial data. This vertical handles vast amounts of confidential customer information, including personal details, financial transactions, and investment records, all of which require stringent protection against unauthorized access. Data classification solutions in BFSI help segregate data based on its sensitivity, ensuring that only certified individual can avail certain types of information, thereby reducing the risk of breaches. Moreover, these solutions play an essential role in ensuring compliance with industry-specific regulations like PCI-DSS and SOX. The magnifying utilization of digital banking services and mobile applications has further escalated the demand for data classification solutions in the BFSI sector, as institutions seek to secure customer data and maintain operational integrity in a highly regulated environment. This trend is expected to continue, with BFSI remaining the dominant industry vertical in the market.

Regional Analysis:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 32.8%, driven by advanced technological infrastructure, stringent data protection regulations, and the presence of leading market players. The region’s high deployment of digital technologies across industries, including healthcare, finance, and government, increases the demand for robust data classification solutions. Regulatory policies like CCPA and GDPR further intensify the need for effective data management practices to ensure compliance and mitigate risks. Additionally, the rising prevalence of cyber threats and data breaches in North America has heightened the focus on data security. For instance, in December 2024, Byte Federal, a U.S.-based Bitcoin operator, announced that around 58,000 individuals’ crucial information was exposed due to a severe data breach. Furthermore, with ongoing innovations in AI, machine learning, and automation, the region is anticipated to sustain its domination in the global industry.

Key Regional Takeaways:

United States Data Classification Market Analysis

In 2024, United States accounted for 89.80% of the market share in North America. The data classification market in the United States is expanding due to stringent regulatory requirements and the growing emphasis on data privacy. Around 86% of the general population in the U.S. accepts that data privacy is an intensifying concern for them, as per reports. Regulatory frameworks, encompassing Health Insurance Portability and Accountability Act (HIPAA) and California Consumer Privacy Act (CCPA) compel organizations to adopt robust data classification practices to safeguard sensitive information. The increasing volume of unstructured data across industries, such as healthcare, finance, and technology, is further driving demand for classification solutions to ensure compliance and streamline data management. Additionally, the rapid adoption of cloud technologies is another significant driver, with enterprises seeking efficient ways to classify and secure data stored across hybrid and multi-cloud environments. The heightened risk of cyberattacks and insider threats also fuels the need for solutions that can classify and protect data based on sensitivity levels. Moreover, the notable emergence of machine learning or AI integration into data classification tools enhances accuracy and operational efficiency, attracting investments from enterprises. Besides this, the competitive landscape in the United States, characterized by the presence of major technology players, promotes innovation and continuous development of advanced solutions. Government and defense sectors are increasingly adopting classification tools to ensure secure handling of sensitive information, which bolsters market growth. Lastly, boosting consciousness amongst both medium and small-sized enterprises (SMEs) about the significant profits of data classification solutions further contributes to the market's expansion.

Asia Pacific Data Classification Market Analysis

The Asia Pacific data classification market is growing due to the rapid digital transformation across key economies such as China, India, and Japan. Expanding e-commerce, banking, and telecommunications industries are generating vast amounts of data, necessitating efficient classification for regulatory compliance and operational efficiency. The India Brand Equity Foundation (IBEF) reports that the e-commerce segment across India is anticipated to reach USD 325 Billion by the year 2030. Besides this, governing agencies in the region are introducing stricter data protection laws, such as India’s Personal Data Protection Bill and China’s Cybersecurity Law, encouraging organizations to adopt classification solutions. Moreover, the cloud computing expansion and rapid increase in utilization of bring-your-own-device (BYOD) regulations are further accelerating the need for data classification, as enterprises seek to secure data across distributed environments. The region’s high mobile and internet penetration drives demand for solutions that classify and protect data generated through various digital platforms. Apart from this, large-scale investments in smart city projects and IoT deployments, especially in countries like China and South Korea, are also contributing to the market growth. These initiatives generate complex data streams that require efficient classification for effective utilization. Additionally, rising cybersecurity threats in the region are prompting businesses to adopt proactive measures, including implementing data classification systems. The availability of affordable and scalable classification tools tailored to SMEs is encouraging adoption among smaller organizations, further driving the market.

Europe Data Classification Market Analysis

The European data classification market is heavily influenced by stricter data safety policies, especially the General Data Protection Regulation (GDPR). Numerous enterprises across several industries, mainly enveloping finance, manufacturing, and healthcare, are investing in classification tools to ensure compliance with these laws and avoid hefty penalties. This legal framework prioritizes data privacy and security, making classification solutions essential for businesses managing sensitive and personal information. In line with this, the increasing use of cloud computing and digital technologies in Europe is another key driver. As enterprises transition to hybrid IT infrastructures, the need for classifying and securing data across on-premises and cloud environments has grown significantly. The region also faces rising cybersecurity challenges, with an increasing frequency of data breaches and ransomware attacks. According to reports, 50% of businesses in the United Kingdom underwent certain kind of cyber-attack during the year 2023. This risk prompts organizations to adopt advanced classification systems to enhance their security posture. Besides this, Europe’s focus on data sovereignty and localized data storage is fostering demand for classification solutions that align with regional policies. Additionally, the magnifying popularity of remote work and BYOD has increased the complexity of data management, further driving the need for classification tools. Investments in advanced analytics and AI-driven solutions by key European players are also contributing to market expansion.

Latin America Data Classification Market Analysis

The increasing digitization and growing awareness of data security across the region is impelling the market growth. Brazil invested USD 30.1 Billion in digital transformation, as stated by the Brazilian NR. Countries like Brazil and Mexico are implementing more stringent data security laws, like Brazil’s Lei Geral de Proteção de Dados (LGPD), encouraging businesses to adopt classification solutions to ensure compliance. The rise of e-commerce and financial technology (fintech) industries is generating massive amounts of sensitive data, which necessitates efficient classification. The region is also witnessing an increase in cybersecurity threats, prompting organizations to adopt data classification to safeguard critical information. Apart from this, investments in IT infrastructure modernization and cloud adoption are further driving market growth, as enterprises seek to secure their data in distributed environments.

Middle East and Africa Data Classification Market Analysis

In the Middle East and Africa, the data classification industry is growing because of the increasing digitalization and a focus on cybersecurity. Government-led initiatives such as Saudi Vision 2030 and the UAE’s National Cybersecurity Strategy are driving investments in data security solutions, including classification tools. The region’s growing reliance on cloud computing and IoT applications adds to the demand for efficient data management systems. In addition, rising cyber threats, particularly targeting critical infrastructure and financial institutions, are pushing organizations to adopt robust classification systems to secure sensitive information. The top four malware families (Emotet, Upatre, Qakbot, and Qbot) represent 68% of the attributed malware attacks in the Saudi Arabia, as per reports. Furthermore, emerging regulatory frameworks around data privacy in countries like South Africa are encouraging enterprises to classify and protect data effectively.

Competitive Landscape:

The market is highly competitive, with prominent players focusing on technology innovation, strategic acquisitions, and expanding service offerings. Key companies lead the market by providing advanced data classification solutions that enhance data security, compliance, and governance. For instance, as per industry reports, Spirion, a major data classification firm, and Thales Group, an encryption software firm, collaboratively provides an integrated service for safeguarding as well as classifying crucial data with top-tier encryption and management of rights. In addition to this, these firms invest heavily in research and development to incorporate AI, machine learning, and automation into their offerings, improving classification accuracy and efficiency. Besides, emerging players are gaining traction by offering specialized solutions for specific industries, such as healthcare and finance, further intensifying market competition. Partnerships and collaborations with cloud service providers also contribute to the market's competitive dynamics.

The report provides a comprehensive analysis of the competitive landscape in the data classification market with detailed profiles of all major companies, including:

- Forcepoint LLC

- Fortra LLC

- HANDD Business Solutions

- Netwrix Corporation

- Varonis Systems Inc.

Latest News and Developments:

- November 2024: Congruity360, a firm providing assistance to companies seeking to leverage AI features, introduced its new next-gen platform for data classification, called Classify360 v3.1. The 3.1 release introduces a host of new features in Classify360 that empower businesses to navigate the complexities of unstructured data management and compliance.

- August 2024: Varonis announced AI-based data classification as well as discovery. The company’s new data scanning feature based on LLM offers consumers in-depth business insights with exceptional expandability as well as accuracy.

- May 2024: OneTrust, an intelligence company, launched new platform abilities and improvements to aid enterprises explore, safeguard, and responsibly leverage data. Such advancements strengthen businesses to carry out responsible data activation, manage risks, and navigate the complicated regulatory ecosystem. OneTrust Data Discovery fosters detecting and assessing adherence as well as security complications by automatically applying for ideal policies minimizing data risk. An improved Data Classification Engine streamline both customization and configuration for unstructured as well as structured data.

- May 2024: Alation, Inc., a data intelligence firm, launched Alation Workflow Automation to aid data stewards in catering to the complicated data governance requirements of enterprise data ecosystems. Automation Bots boost productivity of data steward facilitating automation of security classifications, efficiently mitigating identified gaps and locating incomplete metadata.

- August 2023: Google unveiled new abilities for Workspace, its office productivity suite, encompassing attributes like generative AI that can label as well as classify Drive files automatically for zero trust applications. These new attributes highlight the latest generative AI abilities integrated together with pre-existing tools like virtual assistant Duet AI. The new capabilities also encompass digital sovereignty controls and data loss prevention (DLP) abilities.

Data Classification Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Services |

| Types Covered | Content-based Classification, Context-based Classification, User-based Classification |

| Deployment Modes Covered | On-premises, Cloud-based |

| Applications Covered | Access Control, Governance and Regularity Compliance, Web, Mobile and Email Protection, Auditing and Reporting, Others |

| Industry Verticals Covered | BFSI, Healthcare, Government and Defense, IT and Telecom, Energy and Utilities, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Forcepoint LLC, Fortra LLC, HANDD Business Solutions, Netwrix Corporation, Varonis Systems Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the data classification market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global data classification market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the data classification industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The data classification market was valued at USD 1.86 Billion in 2024.

IMARC estimates the data classification market to reach USD 11.05 Billion by 2033, exhibiting a CAGR of 20.78% during 2025-2033.

The market is influenced by struct data privacy regulations, amplifying cybersecurity risks, increase in deployment of cloud computing, AI-powered automation, increase in data volumes, and need for effective data governance. Organizations focus on compliance, risk mitigation, and information security, bolstering investments in enhanced classification solutions and managed services.

North America currently dominates the data classification market, accounting for a share exceeding 32.8%. This dominance is fueled by stricter regulatory policies, elevated cybersecurity investments, notable increase in cloud adoption, and robust establishment of key technology providers.

Some of the major players in the data classification market include Forcepoint LLC, Fortra LLC, HANDD Business Solutions, Netwrix Corporation, Varonis Systems Inc, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)