Dairy Snacks Market Size, Share, Trends and Forecast by Type, Nature, Distribution Channel, End Use, and Region, 2025-2033

Dairy Snacks Market Size and Share:

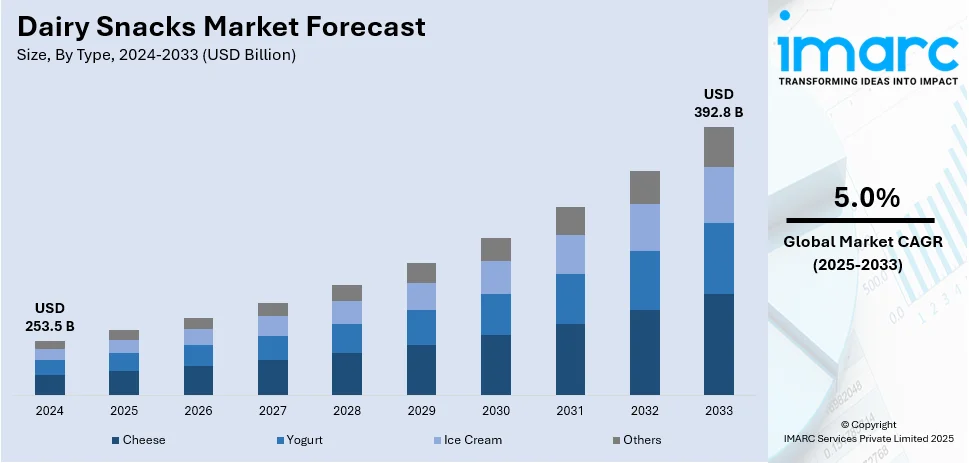

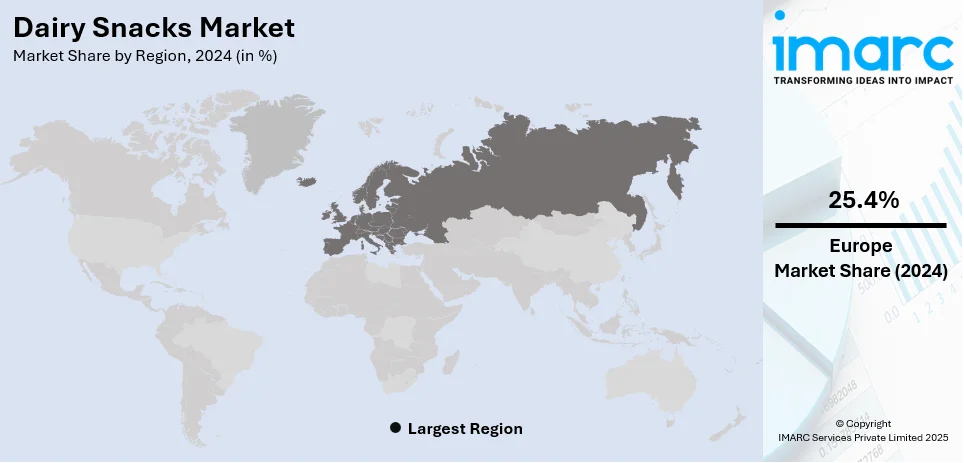

The global dairy snacks market size was valued at USD 253.5 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 392.8 Billion by 2033, exhibiting a CAGR of 5.0% during 2025-2033. Europe currently dominates the market, holding a significant market share of over 25.4% in 2024. The dairy snacks market share is driven by growing consumer preference for healthier, convenient snack options rich in protein and probiotics, increased awareness about gut health benefits, and innovation in product offerings, including new flavors and plant-based alternatives.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 253.5 Billion |

| Market Forecast in 2033 | USD 392.8 Billion |

| Market Growth Rate (2025-2033) | 5.0% |

The dairy snacks market growth is due to rising demand for healthier and convenient snacks, as health-conscious consumers demand nutritious substitutes to conventional snacks. Protein-rich, calcium, and probiotic content in dairy snacks are in harmony with health-trendy behaviors. The expanding trend of consuming food on-the-go, particularly among time-poor consumers, has increased the demand for instant-eat dairy snacks such as yogurt cups, cheese sticks, and flavored milk. Besides this, the rise in plant-based diets has created a platform for dairy alternatives to enter markets, broadening market offerings. Moreover, awareness of the necessity of gut health and the benefits of probiotics has made fermented dairy products like kefir and yogurt more popular.

The United States stands out as a key market disruptor, fueled by its robust consumer base, creativity, and culinary diversity trends. As a leading consumer of dairy foods, the US has led strong demand for healthy, convenient snack foods. With increasing health and wellness concerns, American consumers are increasingly turning to high-protein, low-calorie dairy snacks, driving market expansion. In addition, the US is a product innovation leader, where businesses never cease to create new dairy snacks, including yogurt beverages, probiotic products, and plant-based products, to serve a variety of consumers. The growing popularity of ready-to-eat and on-the-go dairy snacks, as well as the movement toward clean-label and organic products, have also helped the US play a disrupting role in the market globally.

Dairy Snacks Market Trends:

Rising Demand for Protein-Enriched Dairy Snacks

Consumer focus on high-protein diets is sensing the demand towards dairy-based snacks, which are easy and healthy. Examples of these products include Greek yogurt, cottage cheese, protein-dense dairy bars, and cheese sticks. Research indicates that 71% of adults in the US consume more protein than in previous years, reflecting a significant rise, while high-protein foods are priced 12% higher than other items. Such products have high consumption levels among health-conscious individuals, athletes, and busy professionals who want quick nutritious options. Moreover, the rise of fitness trends and weight management programs has further propelled demand for protein-enriched dairy snacks, with 62% of consumers globally seeking snacks with high protein content, as per reports. Companies are experimenting with different formulations to meet these changing needs of consumers. Dairy-dominated snacks usually involve functional ingredients comprising whey protein and casein to consider the protein content. Additionally, clean-label products with least number of additives and artificial ingredients are becoming popular among consumers, creating a demand for promotional strategies with constant emphasis on amelioration in the area of fresh and natural formulations. Therefore, the entry of the high-protein dairy innovations to the market covers all age groups-from children to elderly consumers-that reinforce the position of dairy snacks as the favorite substitute to fill the void traditionally occupied by high-carbohydrate and sugar-laden snack alternatives.

Expansion of Plant-Based and Lactose-Free Dairy Snacks

With the growing prevalence of lactose intolerance and milk allergy and the popularity of plant-based diets, the market for nondairy plant-based and lactose-free dairy snacks has grown. As per NIH, almost 68% of the world's population suffers from some level of lactose malabsorption, which leads to greater demand for plant-based options. Dairy-free consumers look for products that most closely replicate conventional dairy in terms of taste and texture but are not compromising in other areas. Accordingly, companies are investing in creating innovative dairy-free alternative products from almond, oat, soy, and coconut origins, to meet the growing consumer demand. The dairy-free plant-based snacks category has expanded significantly, with dairy-free yogurt, cheese alternative, and frozen desserts being leading categories. Similarly significant, clean label and organic positioning becomes crucial to attract health-aware consumers. Businesses have embraced sophisticated processing technology, which has benefited the sensory attractiveness of their dairy-free products and brought them in line with consumer demands. Sustainability is placing even more emphasis on the trend, with a group aware of the environment choosing plant-based foods because they have a lower carbon footprint compared to traditional dairy.

Premiumization and Functional Dairy Snacks

Consumers are seeking out high-quality dairy snacks, alongside fundamental nutrition, and precious functional benefits. This trend has created a rise in demand for value-added dairy products: functional dairy products like probiotic yogurts to support gut health; immunity-stimulating cheese types; and these therapies contain adaptogens or even collagen to support healthy skin-they all have mass consumer appeal among health-conscious consumers. In addition, the expansion of premiumization expands the demand for grass-fed, organic, and non-GMO offerings: customers appear desperately eager to pay more for apparently healthier, higher-quality variations of the products they like. Nowadays, foodies are being treated to gourmet and artisanal dairy snacks presented in exotic flavorings, hard-to-find, aged types of cheese, and fusion-style dairy products. Developing new product ideas in functional and premium dairy is supposed to be spurred by this trend: ingredient clarity followed by sustainably sourced ingredients and health-improving forms are to be the priorities for manufacturers. The trend is powerful and will take even greater pace when it concerns indulgence-with-wellness snacking trends.

Dairy Snacks Industry Segmentation:

IMARC Group provides an analysis of the key trends in each sub-segment of the global dairy snacks market report, along with forecasts at the global, regional and country level from 2025-2033. Our report has categorized the market based on type, nature, distribution channel, and end use.

Analysis by Type:

- Cheese

- Yogurt

- Ice Cream

- Others

Yogurt leads the market share in 2024. Yogurt is the leading segment in the dairy snacks market due to its versatility, health benefits, and consumer demand for convenient, nutritious snacks. Packed with protein, calcium, and probiotics, yogurt is highly favored for its digestive and immune system benefits. The growing trend toward gut health and wellness has further boosted yogurt's popularity. Flavored, Greek, and plant-based yogurts cater to various dietary preferences, making it a go-to snack option for a broad demographic. Additionally, the rise of on-the-go consumption, with yogurt cups and drinkable options, has driven market growth. Innovation in packaging and flavor combinations continues to strengthen yogurt's dominance in the dairy snacks market.

Analysis by Nature:

- Organic

- Conventional

Organic dairy snacks are a rapidly growing in the dairy snacks market, driven by increasing consumer demand for clean, sustainable, and health-conscious options. These snacks are produced without synthetic pesticides, growth hormones, or antibiotics, appealing to environmentally aware and health-conscious consumers. The organic segment includes products like organic yogurt, cheese, and milk-based snacks, which are perceived as healthier and more natural. As consumers become more mindful of their food's environmental impact, the organic dairy snacks segment continues to gain momentum, attracting a dedicated consumer base seeking healthier, eco-friendly alternatives.

Conventional dairy snacks remain a crucial part of the nature segment in the dairy snacks market, primarily due to their accessibility, affordability, and familiarity. These snacks, including traditional yogurt, cheese sticks, and flavored milk, are made from standard dairy ingredients and are often mass-produced, ensuring wide availability at lower price points. Despite the growing popularity of organic products, conventional dairy snacks continue to appeal to a broad demographic because they are cost-effective and convenient. This segment remains the backbone of the dairy snacks market, catering to everyday consumers seeking reliable, familiar snack options.

Analysis by Distribution Channel:

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Stores

- Others

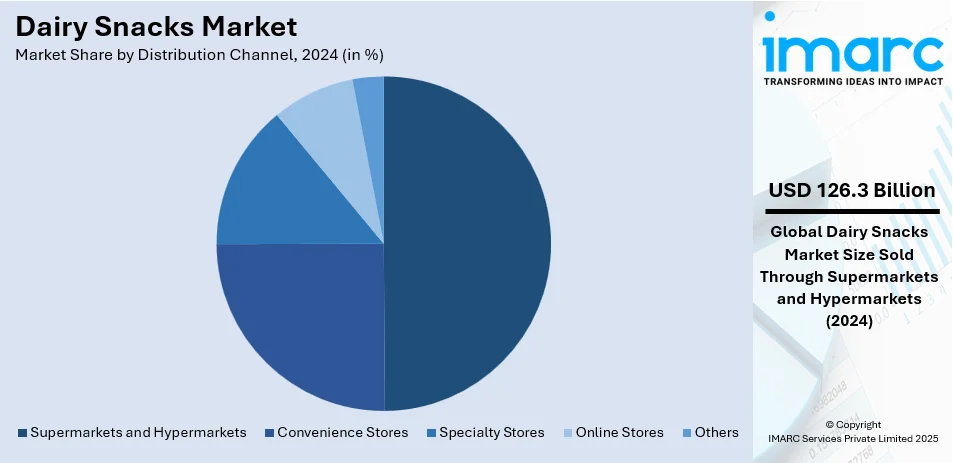

Supermarkets and hypermarkets leads the market with around 49.8% of market share in 2024. Supermarkets and hypermarkets are the leading distribution channels in the dairy snacks market due to their wide reach and convenience. These retail outlets offer a broad selection of dairy snacks, from yogurt and cheese to flavored milk and snackable dairy products, catering to diverse consumer preferences. Their large-scale operations and expansive product assortments make them a one-stop shopping destination for consumers, driving high foot traffic and sales volume. The availability of dairy snacks in supermarkets and hypermarkets is also bolstered by promotional strategies, bulk offerings, and strategic store placements, making it easier for consumers to access a variety of dairy snack options. This dominance is expected to continue, with these stores playing a key role in shaping market trends.

Analysis by End Use:

- HoReCa

- Foods and Beverages Industry

The HoReCa (Hotels, Restaurants, and Cafes) sector plays a significant role in the dairy snacks market as an end-use segment. Hotels, restaurants, and cafes often feature dairy-based snacks, such as yogurt parfaits, cheese platters, and milk-based beverages, on their menus. The growing trend for health-conscious dining has led to an increased demand for nutritious, high-protein dairy options, making them a popular choice in these establishments. As consumers increasingly seek healthier and more convenient snack options when dining out, the HoReCa sector continues to drive the demand for innovative dairy snacks, further shaping the market’s development.

The foods and beverages industry is another key part of the end-use segment of the dairy snacks market. Dairy snacks are widely incorporated into various food and beverage products, such as smoothies, ready-to-eat meals, and packaged snack items. Manufacturers in this sector leverage dairy ingredients like yogurt, cheese, and milk to meet consumer preferences for convenient, nutritious, and tasty products. As the demand for healthier and on-the-go food options rises, the foods and beverages industry increasingly use dairy snacks to cater to busy consumers. This trend is expected to contribute to continued growth in the dairy snacks market.

Regional Analysis:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, Europe accounted for the largest market share of over 25.4%. Europe is the leading regional segment of the dairy snacks market, driven by strong consumer demand for dairy-based products and a growing preference for healthy, convenient snack options. Countries like Germany, France, and the UK have well-established dairy industries, which play a key role in the popularity of dairy snacks such as yogurt, cheese, and milk-based beverages. The European market also benefits from increasing health-consciousness, with consumers prioritizing protein-rich, low-sugar, and probiotic-rich dairy snacks. Additionally, the growing trend of organic and sustainable food choices has spurred the development of premium dairy snack options. Europe’s diverse consumer base and robust distribution channels further contribute to its dominance in the global dairy snacks market.

Key Regional Takeaways:

United States Dairy Snacks Market Analysis

In 2024, the United States accounts for over 89.80% of the dairy snacks market in North America. Consumer interest in convenience and protein-rich options is responsible for the boost in the U.S. dairy snacks market. According to the U.S. Department of Agriculture, total U.S. dairy consumption per capita is expected to reach 661 pounds by 2023, implying sustained demand for dairy products. Also on the top of the list are cheese snacks, which account for more than 40% of the total market share. They are versatile as well as nutritious in value. Lactose-free and plant-based innovations have added momentum to this sector. Major companies in the U.S. dairy snacks include General Mills and The Kraft Heinz Company, which train as well as adopt product diversification to meet consumer demands. Furthermore, e-commerce expansion along with retail partnerships increases the convenience through which people access these offerings.

Europe Dairy Snacks Market Analysis

The dairy snacks demand in Europe has taken a stride toward improvement due to the high number of dairy intakes as well as innovation in functional foods. Per capita dairy consumption in the EU measured at around 52.81 kg in 2023 according to the European Dairy Association. Most importantly of such cheese-based snacks are France and Germany as top consumers and producers. As a requirement for clean-label organic dairy snacks, strict EU food regulations often resort to satisfy consumer needs for health foods. Leading companies such as Danone and Arla Foods do not hesitate to leverage on improved nutrition benefits as well as sustainability for their innovations. The supermarket private-label brands are also not left behind in rising competition among the sources of dairy snacks. With government support to dairy farming, most of market growth across the region is supplemented with investments in sustainable packaging.

Asia Pacific Dairy Snacks Market Analysis

The Asia Pacific dairy snacks market is experiencing robust growth, fueled by increasing dairy consumption and urbanization. The National Bureau of Statistics of China states that the dairy consumption of the country exceeded 45 million metric tons in 2023, underpinning robust demand for dairy-based snacks. India's largest dairy industry in the world makes a huge contribution, with milk production every year amounting to 239.30 million metric tons, according to the Ministry of Fisheries, Animal Husbandry & Dairying. Yogurt and cheese snack segments in the region are growing due to rising disposable incomes and Western dietary trends. Probiotic dairy snacks are favored by Japanese and South Korean consumers, driving functional food demand. Domestic leading players such as Mengniu Dairy and Yakult Honsha are also investing in R&D for new product launches. The government-initiated programs such as China's Healthy China 2030 policy that encourage the consumption of dairy products further providing a favorable dairy snacks market outlook.

Latin America Dairy Snacks Market Analysis

Latin America's dairy snack market is expanding with rising dairy production and changing consumer tastes. The Government of Brazil states that Brazil produced more than 35 billion liters of milk in 2023, making it the region's largest dairy producer. Cheese and yogurt snacks are becoming popular, with Argentina and Mexico topping per capita dairy consumption. Domestic giants like Nestlé Latin America and Grupo Lala emphasize fortification and organics. Government subsidies and dairy farming programs complement market growth. The growing number of convenience stores and online shopping sites further helps product availability, supporting consistent market growth.

Middle East and Africa Dairy Snacks Market Analysis

The Middle East and Africa market for dairy snacks is growing with increased dairy consumption and a burgeoning retail market. Based on the Gulf Cooperation Council (GCC) Dairy Report, consumption of dairy products in the GCC was anticipated to reach over 5 million metric tons by 2023, with cheese and yogurt-based snacks being the main drivers. Regional consumption is led by Saudi Arabia and the UAE, and premium and organic dairy snacks command good demand. The dairy sector in South Africa in 2023 manufactured about 3 billion liters of milk, as stated by the South African Milk Processors Organization, as support for market expansion. Dominance comes from foreign brands Almarai and Clover Industries, complemented by regional producers offering diversification in variety to appeal to different tastes. Growing urbanization and preference towards healthier snacking contribute towards heightened demand, consolidating the region's market expansion.

Competitive Landscape:

Several leading companies are focusing on product innovation by introducing new flavors, packaging formats, and functional benefits, such as high-protein, low-sugar, and probiotic-enriched snacks. As health-conscious consumers increasingly seek nutritious alternatives, brands are developing dairy snacks that offer added benefits like gut health, immune support, and weight management. Additionally, many companies are expanding their product lines to include plant-based alternatives, catering to the growing demand for dairy-free and lactose-free options. To enhance consumer convenience, companies are also investing in portable, ready-to-eat formats such as yogurt cups, cheese sticks, and drinkable yogurts. Furthermore, key players are increasingly focusing on sustainability by sourcing organic and responsibly produced dairy ingredients, aligning with the rise of eco-conscious consumer preferences. In terms of distribution, major brands are strengthening their presence in supermarkets, hypermarkets, and online retail channels to increase accessibility. Collaborations and partnerships with the foodservice sector, including restaurants, hotels, and cafes, have also become essential, expanding the reach of dairy snacks in the HoReCa industry. With these efforts, leading dairy brands are effectively addressing consumer preferences, driving market growth, and shaping the future of the dairy snacks industry.

The report provides a comprehensive analysis of the competitive landscape in the dairy snacks market with detailed profiles of all major companies, including:

- Arla Foods Ingredients Group

- Dairy Farmers of America Inc.

- Danone S.A.

- Fonterra Co-operative Group Limited

- Friesland Campina

- Lactalis International

- Megmilk Snow Brand Co.Ltd

- Meiji Holdings Co. Ltd.

- Nestle S.A

- Organic Valley

- The Kraft Heinz Company

- Unilever PLC

Recent Developments:

- January 2025: Woodlands Dairy expands its First-Choice range with the Low Fat Fruited Dairy Snack, featuring real fruit pieces. Available in classic and new flavors, including Mixed Berry and Guava + Custard, the launch underscores the brand’s commitment to innovation and quality in dairy snacks.

- January 2025: Organic Valley, known for its dairy creamers, has launched its first organic oat-based creamer line. Available nationwide, the new creamers come in four flavors: vanilla, caramel, oatmeal cookie, and cinnamon spice, catering to consumers seeking plant-based alternatives.

- December 2024: General Mills partnered with the US Dairy Checkoff to launch YoBark, a yogurt-based snack featuring Nature Valley granola. Available at Albertson’s, Safeway, and Walmart, it targets tweens with a fun, shareable format while meeting parents' health standards. Expansion to more retailers is planned.

- September 2024: Arla Foods Ingredients launched the ‘Go High in Protein’ campaign to support dairy manufacturers in developing high-protein products. Featuring Nutrilac® ProteinBoost, the initiative includes a virtual seminar and showcases innovative concepts like ambient yoghurts and high-protein ice cream, addressing processing, taste, and texture challenges.

- April 2024: Danone North America introduced Remix, a new yogurt and dairy snack line targeting growing consumer snacking trends. The portfolio spans Oikos, Too Good & Co., and Light + Fit, featuring mix-in toppings with flavors like s’mores, strawberry cheesecake, and banana dark chocolate almond.

Dairy Snacks Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Cheese, Yogurt, Ice Cream, Others |

| Natures Covered | Organic, Conventional |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Stores, Others |

| End Uses Covered | HoReCa, Foods and Beverages Industry |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Arla Foods Ingredients Group, Dairy Farmers of America Inc., Danone S.A., Fonterra Co-operative Group Limited, Friesland Campina, Lactalis International, Megmilk Snow Brand Co.Ltd, Meiji Holdings Co. Ltd., Nestle S.A, Organic Valley, The Kraft Heinz Company, Unilever PLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the dairy snacks market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global dairy snacks market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the dairy snacks industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The dairy snacks market was valued at USD 253.5 Billion in 2024.

The dairy snacks market is projected to exhibit a CAGR of 5.0% during 2025-2033.

The dairy snacks market is driven by increasing health consciousness, demand for convenient on-the-go snacks, and growing interest in protein-rich and probiotic-packed options. Additionally, product innovation, including new flavors and plant-based alternatives, alongside rising awareness of gut health benefits, further fuels market growth and consumer preference.

Europe currently dominates the market driven by rising health consciousness, demand for high-protein and probiotic-rich options, and the preference for convenient, on-the-go snacks.

Some of the major players in the dairy snacks market include Arla Foods Ingredients Group, Dairy Farmers of America Inc., Danone S.A., Fonterra Co-operative Group Limited, Friesland Campina, Lactalis International, Megmilk Snow Brand Co.Ltd, Meiji Holdings Co. Ltd., Nestle S.A, Organic Valley, The Kraft Heinz Company and Unilever PLC.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)