Culinary Tourism Market Size, Share, Trends and Forecast by Activity Type, Tour Type, Age Group, Mode of Booking, and Region 2026-2034

Global Culinary Tourism Market Size, Share, Trends & Forecast (2026-2034)

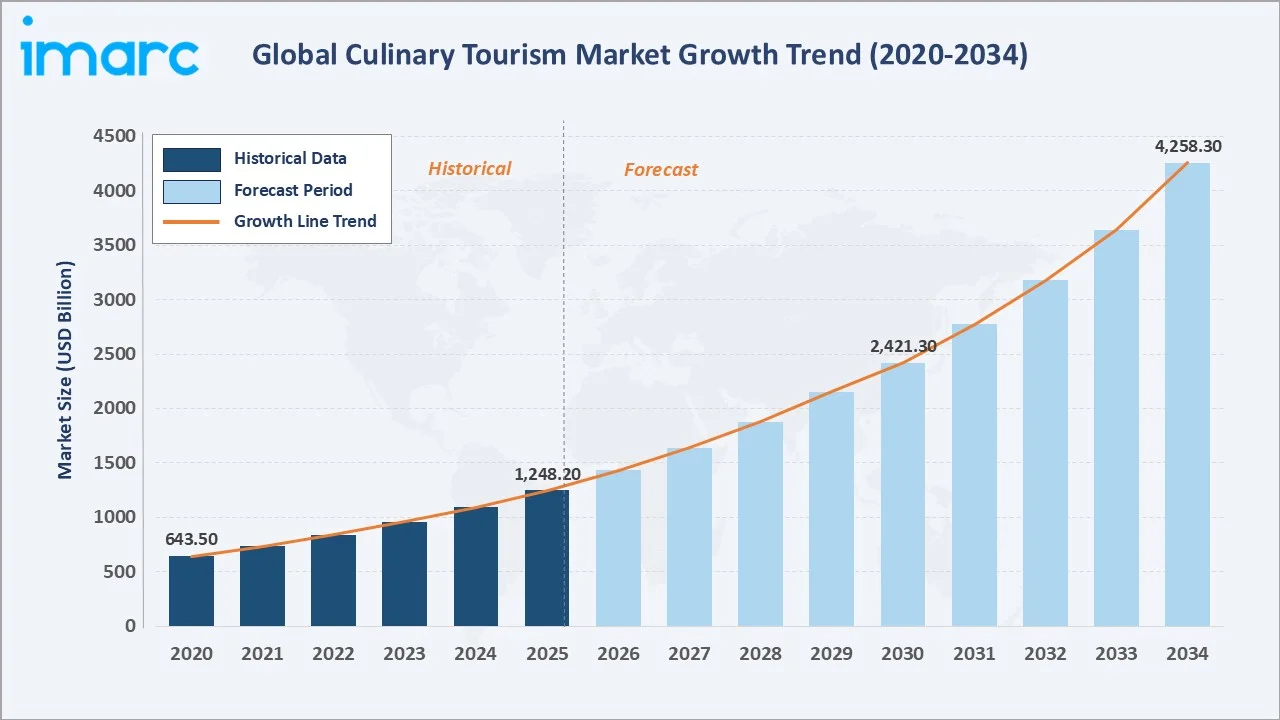

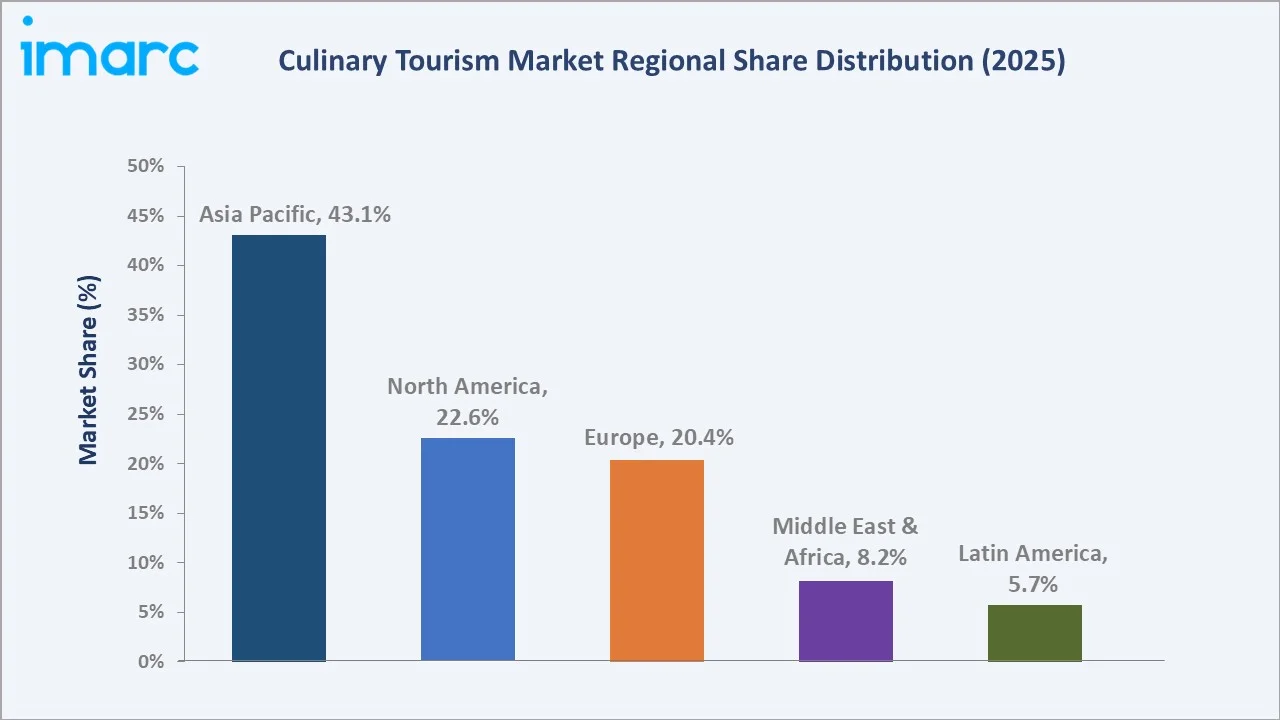

The global culinary tourism market was valued at USD 1,248.2 Billion in 2025 and is projected to reach USD 4,258.3 Billion by 2034, expanding at a CAGR of 14.17% during the forecast period (2026-2034). The market is propelled by rising experiential travel demand, with 95% of travelers around the world being food travelers, social media-driven food discovery, and the rapid growth of online booking platforms. Domestic tours dominate with a 72.9% share (2025), while online travel agents capture 48.5% of bookings. Asia Pacific leads all regions with a 43.1% revenue share (2025).

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,248.2 Billion |

|

Forecast Market Size (2034) |

USD 4,258.3 Billion |

|

CAGR (2026-2034) |

14.17% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest and Fastest Growing Region |

Asia Pacific (43.1%, 2025 and CAGR ~16%, 2026-2034) |

The culinary tourism market from 2020 through 2034 expanded from USD 643.5 Billion in 2020 to USD 1,248.2 Billion in 2025, anchored at USD 2,421.3 Billion in 2030 before reaching USD 4,258.3 Billion by 2034.

To get more information on this market, Request Sample

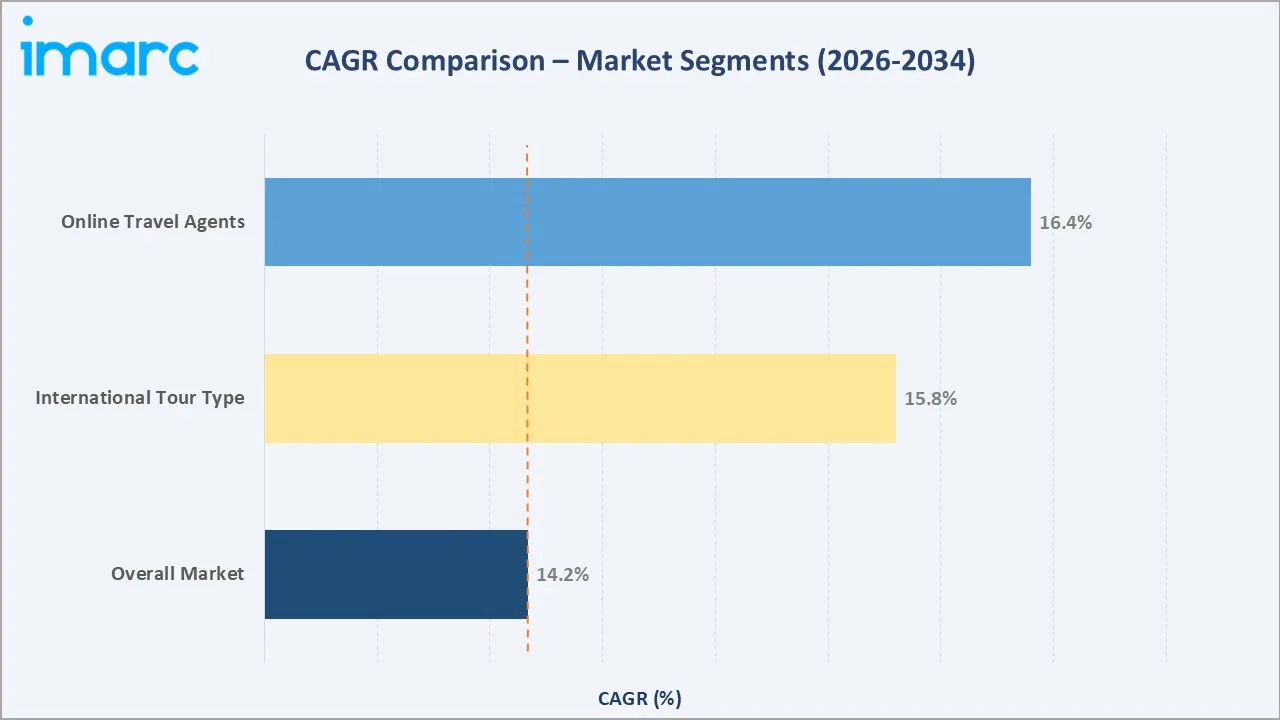

The overall market CAGR is 14.17%, the international tour type segment is growing at a CAGR of 15.8%, and the online travel agents segment is growing at a CAGR of 16.4%.

Executive Summary

The global culinary tourism market represents one of the fastest-growing segments within the broader travel and hospitality industry. Valued at USD 1,248.2 Billion in 2025, the market is forecast to exceed USD 4,258.3 Billion by 2034 at a CAGR of 14.17%. This growth is powered by a global shift toward experience-led travel, where food and beverage culture serves as the primary motivation for trip planning. 45% of Indian travellers considering food as an “integral part of their travel planning” significantly influence destination choices.

Domestic culinary tourism commands a 72.9% market share (2025), reflecting strong intra-regional food discovery among populations in Asia Pacific, North America, and Europe. However, international culinary tourism is growing faster at an estimated CAGR of 15.8%, driven by cross-border food trail programs and the rise of cuisine-specific travel packages to destinations such as Japan, Italy, Peru, and Thailand. Online travel agents account for 48.5% of all culinary tour bookings in 2025, underscoring the digital transformation reshaping the distribution landscape.

Asia Pacific leads globally with a 43.1% market share (2025), anchored by diverse street food cultures in Thailand, Vietnam, India, and China, and rapidly growing middle-class outbound tourism. North America and Europe follow with 22.6% and 20.4% respectively, supported by wine tourism, farm-to-table experiences, and Michelin-starred food trails.

Key Market Insights

|

Insight |

Data |

|

Leading Tour Type |

Domestic – 72.9% share (2025) |

|

Leading Mode of Booking |

Online Travel Agents – 48.5% share (2025) |

|

Leading Region |

Asia Pacific – 43.1% revenue share (2025) |

Key Analytical Observations Supporting The Above Data:

- Domestic culinary tourism dominates with a 72.9% share (2025), driven by post-pandemic preference for local food exploration, government-sponsored food tourism campaigns, and lower travel costs for intra-regional trips.

- Online travel agents hold 48.5% of bookings (2025), reflecting a structural shift toward digital-first trip planning. Platforms like Tourradar and Viator registered higher culinary tour bookings.

- Asia Pacific commands 43.1% of global market revenue (2025), driven by Japan's Washoku UNESCO designation and China's rapidly expanding domestic food tourism sector.

Global Culinary Tourism Market Overview

Culinary tourism encompasses all travel activities where food and beverage experiences are the primary or significant motivation. It spans a broad ecosystem, from street food walking tours and Michelin-starred restaurant visits to farm stays, wine trails, cooking masterclasses, and food festival attendance. The global culinary tourism ecosystem connects experience providers, tour operators, digital booking platforms, hospitality providers, and destination marketing organizations.

Applications span individual leisure tourism, corporate retreat programming, educational culinary travel, and health-focused wellness food tourism. Macroeconomic tailwinds, including rising global middle-class populations projected at 5.3 billion by 2030, increasing per capita disposable income in Asia and Latin America, and post-COVID experiential spending recovery, are driving sustained demand.

Market Dynamics

To evaluate market opportunities, Request Sample

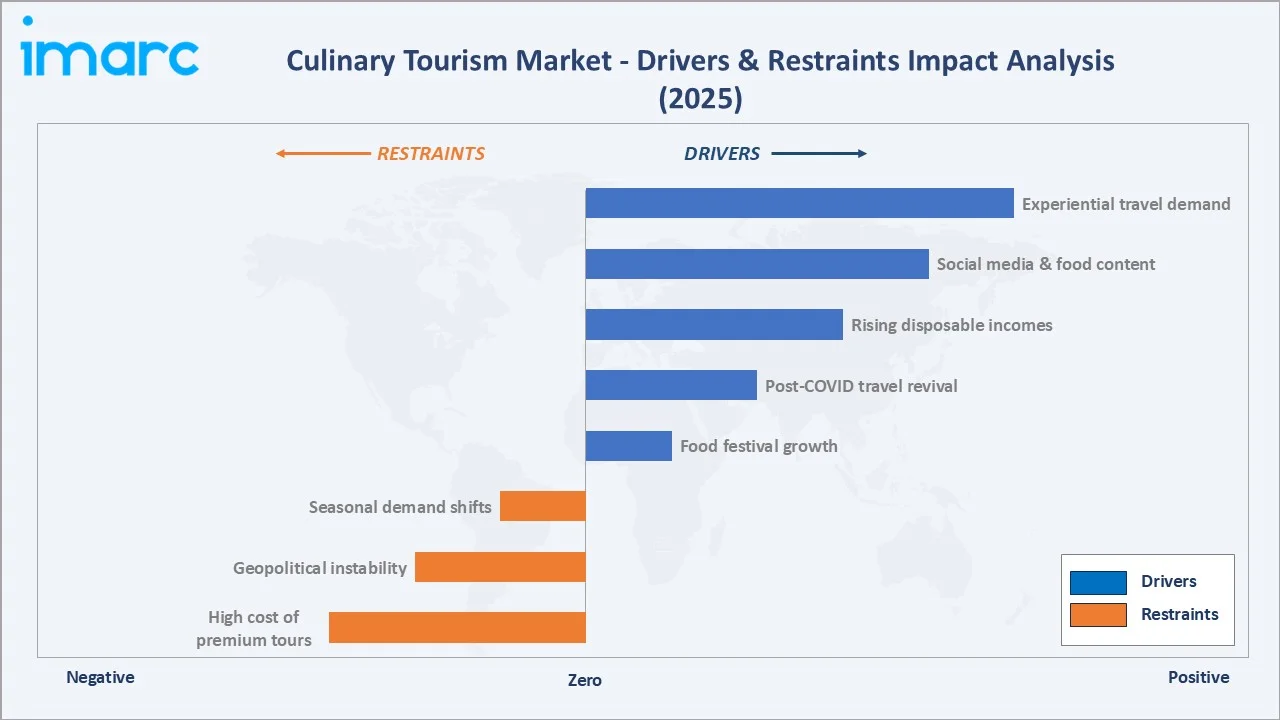

Market Drivers

- Experiential Travel Demand Surge: 65% of global travelers prioritize experiences over material goods, with food-centric activities ranking as the top experience motivator, directly fueling culinary tour bookings worldwide.

- Social Media and Food Content Explosion: Instagram, TikTok, and YouTube food content generate more views. 87.1% of food experts predict people will travel more to experience culinary culture and cuisine in India.

- Post-COVID Travel Spending Revival: Global international tourist arrivals recovered to 1.4 billion in 2024, surpassing pre-pandemic levels. Culinary tourism, as a high-value segment, for premium travel spending recovery.

Market Restraints

- High Cost of Premium Culinary Experiences: Luxury culinary tours costs high, limiting accessibility for budget-conscious travelers and constraining total addressable market depth outside high-income segments.

- Geopolitical Instability and Travel Advisories: Travel disruptions from geopolitical tensions in Eastern Europe and the Middle East reduced cross-border culinary tour demand in affected corridors.

Market Opportunities

- Sustainable and Farm-to-Table Tourism: 62% of Gen Z consumers prefer sustainable brands. Operators offering agritourism, zero-waste dining, and community-supported culinary experiences command revenue premiums over standard offerings.

- Digital Platform and AI Personalization: AI-powered culinary itinerary builders, conversational booking assistants, and predictive taste-profile matching represent a high technology investment opportunity within culinary tourism.

Market Challenges

- Climate Change Impact on Food Destinations: Changing weather patterns are disrupting harvest seasons, food festival schedules, and farm tour availability across key destinations.

- Regulatory and Visa Complexity: Multi-destination culinary tours across ASEAN, EU, and African regional blocs face fragmented visa requirements, increasing booking friction and reducing conversion rates among first-time international food tourists.

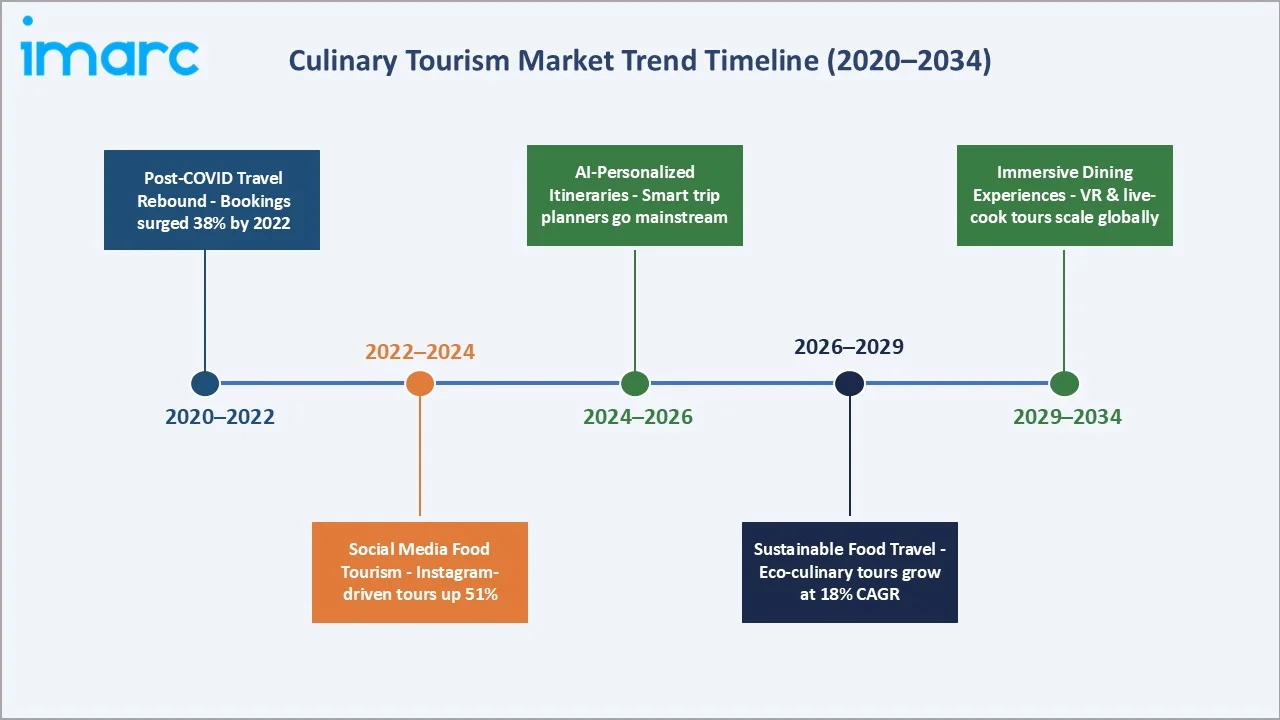

Emerging Market Trends

1. Rise of Social Media-Driven Food Destination Tourism

Food destinations featured in viral social media content are experiencing dramatic tourism surges. Japan is the top destination for food tourism with 64% in 2024 and Thailand's ranks second with 53% in 2024; these are highly influenced by the social media.

2. AI-Powered Personalized Culinary Itineraries

Artificial intelligence is transforming how culinary tours are designed and sold. Taste-profile algorithms that match travelers with local cuisine experiences based on dietary preferences and past travel data are now standard features among leading OTAs.

3. Culinary Tourism as Wellness Travel

The convergence of food tourism and wellness travel is creating a new high-value subsegment. Gut-health retreats, Ayurvedic cooking tours in India, and Mediterranean diet immersion programs in Greece and Italy generate demand in niche culinary wellness revenue.

4. Virtual and Hybrid Culinary Experiences

Post-pandemic, virtual cooking masterclasses and hybrid food tourism formats have become established product lines. Several major tour operators now offer hybrid culinary memberships combining monthly at-home ingredient boxes with one annual in-person food tour.

Industry Value Chain Analysis

The culinary tourism industry value chain is a multi-stakeholder ecosystem connecting food experience creators with global travelers through digital and physical touchpoints. Each stage adds distinct value and is subject to different competitive dynamics, margin structures, and growth trajectories.

|

Stage |

Key Players / Examples |

|

Experience Providers |

Local chefs, restaurants, farms, wineries, street food vendors |

|

Tour Operators |

Abercrombie & Kent, G Adventures, Classic Journeys |

|

Booking Platforms |

OTAs, direct booking portals |

|

Hospitality & Logistics |

International hotel chains, airlines, and ground transport providers |

|

Marketing & Media |

National tourism boards, food bloggers, influencers, travel media |

|

End Travelers |

Millennials, Gen Z, Baby Boomers, food-focused global tourists |

The tour operator stage captures the highest margin within the value chain, with leading operators generating gross margins of 28–38% on premium culinary tour packages. Digital booking platforms (OTAs) are rapidly increasing their share of value capture, with commission rates between 12–20% now standard across online culinary tour marketplaces.

Technology Landscape in the Culinary Tourism Industry

Digital Booking and OTA Platforms

Online travel agents account for 48.5% of culinary tourism bookings, with platforms such as Tourradar, Viator, and GetYourGuide increasingly specializing in curated culinary experience verticals. Mobile booking now represents 60% of all OTA transactions, driven by last-minute, location-based food experience discovery among younger travelers.

Artificial Intelligence and Machine Learning

AI is being deployed across the culinary tourism value chain, from personalized itinerary generation and dynamic pricing optimization to real-time sentiment analysis of food tour reviews. Leading platforms report that AI-driven recommendation engines improve customer satisfaction scores and repeat booking rates.

Social Media and Content Commerce

Social media platforms function as both marketing channels and discovery engines for culinary tourism. The #foodtravel hashtag became a powerful tool for TikTok creators, with more than 27.2 thousand posts and 835.9 million views in total. Content creators with culinary travel focus are commanding partnerships, reflecting the outsized influence of influencer-led food destination promotion on actual booking behavior.

Sustainability and Traceability Technology

Farm-to-fork traceability tools, carbon footprint calculators embedded in tour booking flows, and blockchain-verified local producer partnerships are emerging as technology-driven differentiators for premium culinary operators.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Activity Type |

Food Festivals and Events |

32.2% |

2025 |

|

Tour Type |

Domestic |

72.9% |

2025 |

|

Age Goup |

Generation Y |

40.5% |

2025 |

|

Mode of Booking |

Online Travel Agents |

48.5% |

2025 |

|

Region |

Asia Pacific |

43.1% |

2025 |

By Tour Type

Domestic culinary tourism is the dominant segment, capturing 72.9% of total market revenue in 2025. Local food discovery drives demand, with government food tourism campaigns in China, India, Thailand, and Japan. Domestic tours offer lower price points, higher booking frequency, and reduced trip planning complexity.

To access detailed market analysis, Request Sample

International culinary tourism holds a 27.1% market share (2025) but represents the higher-value segment, with average international culinary tour packages. Japan, Thailand, China, South Korea and Singapore consistently rank among the top five international culinary destinations. This segment is forecast to grow at ~15.8% CAGR through 2034, outpacing the domestic segment.

By Mode of Booking

Online Travel Agents (OTAs) lead with a 48.5% market share (2025), reflecting the irreversible digitization of culinary tour discovery and purchase. Platforms such as Tourradar, Viator (Tripadvisor), and GetYourGuide offers unique culinary experiences globally. OTA penetration is highest among Generation Y and Z travelers, with bookings via mobile apps.

Direct booking holds a 32.4% share (2025), representing the preferred channel for repeat customers and premium culinary tour seekers who value personalized service from specialist operators. Traditional agents capture 19.1%, primarily serving older demographics and complex multi-destination itineraries.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

43.1% |

Street food culture, rising middle class, food festival growth |

|

North America |

22.6% |

Food TV influence, culinary school tourism, farm-to-table trend |

|

Europe |

20.4% |

Wine trail tourism, Michelin-starred routes, cultural heritage |

|

Middle East & Africa |

8.2% |

Saudi Vision 2030, halal food tourism, UAE food festival boom |

|

Latin America |

5.7% |

Peru & Mexico as global food capitals, agritourism growth |

Asia Pacific's 43.1% market dominance (2025) is anchored by extraordinary food culture diversity across 48 countries and the region's status as home to six of the world's top ten food destinations. Japan alone attracted approximately 36.87 million international visitors in 2024, which increases the demand for food-related travel spend. China's domestic culinary tourism market growth is the largest single-country culinary tourism market globally.

North America's 22.6% share (2025) is driven by the U.S.’s deeply embedded food culture economy, from Napa Valley wine tourism to New Orleans’ culinary festival circuit and New York’s restaurant tourism. Canada’s “Flavours of Canada” national culinary tourism strategy is further driving the market growth in the region. Europe's 20.4% share (2025) reflects its status as the world's most mature culinary tourism destination region.

Competitive Landscape

The global culinary tourism market is highly fragmented. The top five operators, Abercrombie & Kent, G Adventures, Tourradar, Butterfield & Robinson, and Classic Journeys, collectively account for approximately 18–22% of the premium culinary tour segment revenue.

|

Company Name |

Product / Services |

Market Position |

Core Strength |

|

Abercrombie & Kent |

A&K Culinary Journeys |

Market Leader |

Ultra-luxury culinary experiences |

|

G Adventures |

G Adventures Food Tours |

Market Leader |

Adventure-style culinary tours |

|

TourRadar |

TourRadar Platform |

Strong Challenger |

Digital-first OTA for group culinary tours, AI-driven personalization |

|

Butterfield and Robinson Inc. |

Gastronomy |

Strong Challenger |

Premium biking and walking food tours, high-net-worth clientele |

|

Classic Journeys LLC |

Classic Journeys |

Specialist Leader |

Guided walking food tours, 50+ destinations, small-group model |

|

Gourmet On Tour Ltd. |

Gourmet On Tour |

Specialist |

Dedicated gourmet itineraries, wine & cheese trails, Europe focus |

|

Greaves Travel |

India Food Tours |

Established |

India and the Indian Subcontinent culinary experiences, heritage food routes |

|

International Culinary Tours |

International Culinary Tours |

Niche Specialist |

Custom chef-hosted culinary immersions, cooking class integration |

|

Top Deck Tours Limited |

Topdeck |

Emerging |

Youth-focused food travel, social dining formats, 18–32 age group |

The broader market’s long tail consists of thousands of local and regional operators. Digital platform aggregation via OTAs is the primary consolidation mechanism reshaping competitive dynamics.

Key Company Profiles

Abercrombie & Kent

Abercrombie & Kent (A&K) is the world's leading ultra-luxury travel company. A&K's culinary journey portfolio represents its fastest-growing product line, with culinary-focused departures growth.

- Product Portfolio: A&K Culinary Journeys covering culinary cruise through France, popular destinations to Morocco and Colombia for culinary experiences.

- Recent Developments: In June 2024, Abercrombie & Kent introduced its largest collection of Luxury Small Group Journeys for 2025, offering 22 new itineraries tailored to the changing preferences of discerning travelers worldwide. The updated offerings include popular destinations such as Morocco and Colombia, with new plans focused on delivering richer cultural experiences and culinary adventures.

- Strategic Focus: Ultra-high-net-worth traveler segment; bespoke private culinary journeys; expansion into India and Southeast Asia culinary heritage routes through 2026.

G Adventures

G Adventures is the world's largest small-group adventure travel company, with culinary tours forming a major product pillar.

- Product Portfolio: Hilltribes & street food in Thailand, Malaysia, and Singapore, Tuscany San Gimignano in Italy, Speed Trains & Street Food in Japan, Spice Gardens & Seasides in Sri Lanka.

- Recent Developments: Launched G Adventures’ “Food & Wine” dedicated trip category, partnered with National Geographic Society.

- Strategic Focus: Millennial and Gen Z food travelers; sustainable and community-impact culinary experiences; digital-first distribution through OTAs and its own award-winning app.

TourRadar

TourRadar is the world's leading online marketplace for multi-day culinary and group tours. The company specializes in culinary tour transactions, with AI-powered search and recommendation engines in culinary category bookings.

- Product Portfolio: Most popular destinations for foodie tours company offering are Italy, France, Spain, Portugal, Peru, and India.

- Recent Developments: In September 2025, TourRadar introduced AI Discovery, a set of three new integrations that enable travelers to book products from global tour operators using the AI tools they already use, such as ChatGPT and Instagram, along with a new MCP Server.

- Strategic Focus: Digital platform leadership; AI-driven personalization; B2B white-label solutions for hotel chains and airlines to offer culinary tour add-ons to existing bookings.

Butterfield and Robinson Inc.

Butterfield & Robinson (B&R) is a premium Canadian tour operator specializing in slow travel – walking, biking, and culinary immersion experiences.

- Product Portfolio: Wine & Gastronomy walking tours in Burgundy, Tuscany; biking culinary tours in France and Spain; private barge cruises with on-board chef experiences along European waterways.

- Recent Developments: Introduced “B&R Private” fully customizable culinary journeys in for groups of 2–8 travelers; launched Japan culinary walking tour collection, its fastest-selling new destination.

- Strategic Focus: Premium and ultra-premium culinary walking tours; direct booking model; expanding into South America (Argentina wine trails, Peru gastronomy) and Japan through 2026.

Market Concentration Analysis

The global culinary tourism market is characterized by high fragmentation across the mid and lower-tier operators globally. The top five companies, Abercrombie & Kent, G Adventures, Tourradar, Butterfield & Robinson, and Classic Journeys, collectively hold an estimated 18–22% share of the premium culinary tour market (2025). This concentration is significantly lower than in package tourism more broadly, reflecting the artisanal and local-expertise-driven nature of culinary tourism experiences.

The digital platform layer (OTAs) is exhibiting the most rapid consolidation, with Tourradar, Viator (Tripadvisor), and GetYourGuide. These platforms benefit from network effects, more operators attract more travelers, who generate more reviews, which attract more operators. This dynamic is squeezing the revenue capture of individual tour operators while improving market efficiency and consumer choice.

Investment & Growth Opportunities

Fastest Growing Segments

International culinary tourism is growing at a CAGR of ~15.8%, sustainable and regenerative food travel at a CAGR of ~18%, and culinary wellness tourism at a CAGR of ~19% represent the three highest-growth investment vectors through 2034. These segments collectively address a total addressable market, with Japan, Peru, India, and Morocco as the most commercially compelling destination-specific opportunities.

Emerging Market Expansion

The Middle East presents a transformational culinary tourism investment opportunity. Saudi Arabia’s Vision 2030 for tourism infrastructure, with halal food tourism identified as a priority vertical. India’s culinary tourism market is growing, emerging as a top-five global culinary destination.

Venture Investment Trends

Key investment themes include AI-powered culinary itinerary platforms, virtual food experience streaming, blockchain-verified local producer certification, and subscription-based culinary travel memberships.

- Key growth bets: AI personalization engines for culinary taste-profile matching, virtual-to-in-person hybrid culinary memberships, and sustainable food trail certification platforms.

- ESG-aligned investors are targeting community-based culinary tourism operators that demonstrate measurable local economic impact, a requirement increasingly mandated by institutional travel buyers.

- Institutional interest in OTA platform consolidation and premium culinary tour operator roll-ups remains strong, particularly in the Asia Pacific and Middle East markets, where culinary tourism infrastructure is scaling fastest.

Future Market Outlook (2026-2034)

The global culinary tourism market is positioned for broad-based, sustained expansion through 2034. From a base of USD 1,248.2 Billion in 2025, the market is forecast to reach USD 4,258.3 Billion by 2034, an absolute value addition of USD 3,010.1 Billion over nine years. This growth is anchored by three structural trends: the rising primacy of experiences in travel spending, the digital transformation of culinary tour discovery and booking, and the emergence of new high-potential culinary tourism destination markets.

Between 2026 and 2030, technology will serve as the primary market accelerator. AI-personalized culinary itineraries, real-time food experience booking via voice assistants, and AR-enhanced food storytelling during tours will redefine traveler expectations and operator service delivery. Operators that invest in proprietary digital experiences alongside physical tour excellence will command a sustainable premium and capture above-market growth rates.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys with over 160 industry stakeholders in 2025, comprising culinary tour operators, hospitality group executives, OTA platform product managers, national tourism board representatives, and food and travel media professionals across North America, Europe, Asia Pacific, and the Middle East. Primary insights validated quantitative market size estimates and surfaced emerging consumer preference shifts.

Secondary Research

Secondary research encompassed a comprehensive review of operator annual reports, tourism board statistical releases, UNWTO and WTTC data publications, industry databases, food media trade publications, and regulatory filings across 30 countries. Over 280 secondary sources were triangulated and synthesized into a consistent global market model.

Forecasting Models

Market size estimations were developed using a hybrid bottom-up and top-down forecasting approach. GDP per capita growth indices, international tourist arrival projections (UNWTO), food experience consumer spending data, and OTA booking volume trends were incorporated as key input variables.

Culinary Tourism Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Activity Types Covered | Culinary Trials, Cooking Classes, Restaurants, Food Festivals and Events, Others |

| Tour Types Covered | Domestic, International |

| Age Groups Covered | Baby Boomers, Generation X, Generation Y, Generation Z |

| Mode of Bookings Covered | Online Travel Agents, Traditional Agents, Direct Booking |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abercrombie & Kent, G Adventures, TourRadar, Butterfield and Robinson Inc., Classic Journeys LLC, Gourmet On Tour Ltd., Greaves Travel, International Culinary Tours, Top Deck Tours Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, culinary tourism market forecast, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global culinary tourism market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the culinary tourism industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Culinary Tourism Market Report

The global culinary tourism market was valued at USD 1,248.2 Billion in 2025 and is projected to reach USD 4,258.3 Billion by 2034, growing at a CAGR of 14.17%.

Asia Pacific dominates with a 43.1% revenue share (2025), anchored by Japan, China, India, Thailand, and Vietnam as top global culinary tourism destinations attracting food-motivated travelers.

Asia Pacific is also the fastest growing region, supported by China's domestic food tourism boom, India's culinary heritage program, and Southeast Asia's rapidly expanding food tourism infrastructure.

Key drivers include rising experiential travel demand, social media food content explosion, post-COVID travel revival, higher disposable incomes in emerging markets, and food festival proliferation globally.

Domestic culinary tourism is the largest segment with a 72.9% market share (2025), driven by government food promotion campaigns and growing local food discovery culture in Asia Pacific and North America.

Online Travel Agents lead with 48.5% of culinary tourism bookings (2025), reflecting the digital-first behavior of Millennial and Gen Z food travelers who prefer mobile-based tour discovery and booking.

The leading companies include Abercrombie & Kent, G Adventures, TourRadar, Butterfield and Robinson Inc., Classic Journeys LLC, Gourmet On Tour Ltd., Greaves Travel, International Culinary Tours, and Top Deck Tours Limited.

Key trends include AI-personalized food itineraries, sustainable farm-to-table tourism, culinary wellness travel, social media-driven food destination tourism, and virtual cooking experience integration.

Key challenges include high cost of premium experiences, seasonal demand volatility, geopolitical instability impacting cross-border travel, climate change effects on food destinations, and quality-authenticity standardization gaps.

AI personalization, OTA platform aggregation, AR-enhanced food storytelling, social media content commerce, and blockchain-verified producer authentication are the five primary technology forces reshaping culinary tourism through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)