Cryogenic Equipment Market Size, Share, Trends and Forecast by Equipment, Cryogen, Application, End Use Industry, and Region, 2025-2033

Cryogenic Equipment Market Size and Share:

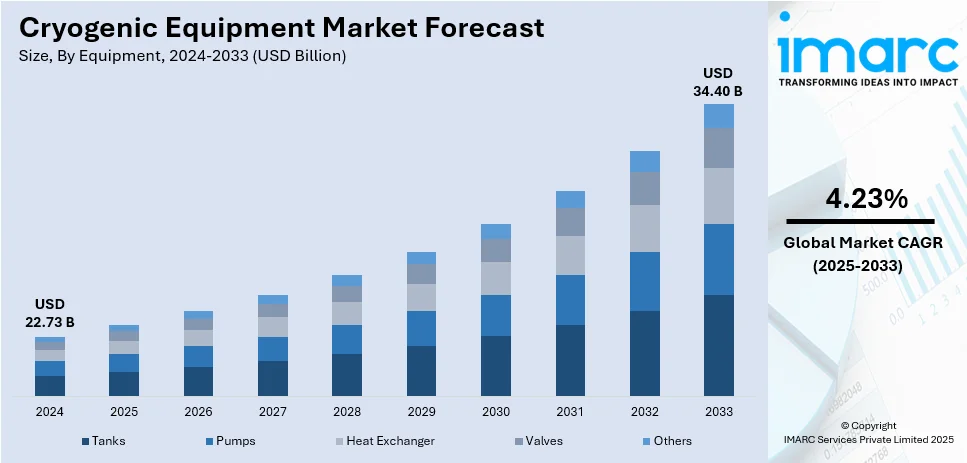

The global cryogenic equipment market size was valued at USD 22.73 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 34.40 Billion by 2033, exhibiting a CAGR of 4.23% during 2025-2033. Asia Pacific currently dominates the market, holding a significant market share of over 37.8% in 2024. The widespread adoption of advanced technology, the rising product demand in the healthcare industry for several applications, the growing product uptake in various food processing applications, and the escalating uptake of renewable energy sources are some of the factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024 |

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 22.73 Billion |

| Market Forecast in 2033 | USD 34.40 Billion |

| Market Growth Rate (2025-2033) | 4.23% |

The cryogenic equipment market growth is primarily driven by the growing demand for liquefied natural gas (LNG) as a cleaner energy source coupled with the increasing need for industrial gases in sectors such as metallurgy, food processing and electronics. According to the report published by IEA, the demand for gas across the globe is set to reach a record 4,200 bcm in 2024 growing over 2.5% year-on-year. However, LNG supply increased only 2% in Q1-Q3 2024 with geopolitical conflicts and project delays affecting growth. Expanding healthcare applications including cryotherapy and cryopreservation significantly boost demand for cryogenic systems. The global shift toward renewable energy and hydrogen-based technologies further propels market growth as these sectors require advanced cryogenic solutions for storage and transportation. Ongoing technological innovations, rising investments in space exploration and stringent environmental regulations promoting clean energy adoption are key factors driving the market forward.

The United States cryogenic equipment market is driven by the rising demand for liquefied natural gas (LNG) as a cleaner energy source supported by the country’s robust natural gas production. For instance, in January 2025, Freeport LNG in Texas announced the landmark shipment of its 800th liquefied natural gas cargo since operations began. JERA, a notable customer further announced the enhancement of its investment and infrastructure support for the expanding LNG facility. Growth in healthcare applications including cryotherapy, cryopreservation and medical gas storage plays a significant role. The expansion of hydrogen-based energy systems driven by the push for decarbonization further accelerates demand. The aerospace and defense sectors leverage cryogenic technologies for propulsion and material testing. Increasing industrial gas usage in food preservation, metal processing and electronics manufacturing also contributes to market growth alongside advancements in cryogenic technologies for efficiency and safety.

Cryogenic Equipment Market Trends:

Rapid Industrialization

Rapid industrialization worldwide is offering numerous opportunities for the market. As industries expand and diversify, the demand for cryogenic equipment rises in tandem. In the chemical sector, cryogenic equipment is used to liquefy gases, with global LNG production reaching 401 million tons in 2023 (as per an industry report), driving demand. These industries often require extremely low-temperature solutions for various applications. In the chemical and petrochemical sector, for instance, this equipment is essential for the separation and liquefaction of gases, aiding in producing industrial gases, chemicals, and LNG, which, in turn, is facilitating the cryogenic equipment market demand. Additionally, the expanding pharmaceutical industry relies on it for the cryopreservation of biological materials, such as cell cultures and vaccines, ensuring their stability and efficacy. Furthermore, the food processing industry utilizes cryogenic freezing and cooling systems to maintain product quality, extend shelf life, and meet stringent safety standards. As developing countries undergo rapid industrialization, there's an increasing need for cryogenic equipment in these emerging markets, further fueling market growth.

Increasing Product Demand in Research and Development Activities

The increasing product demand in research and development (R&D) activities represents one of the key cryogenic equipment market trends. For instance, quantum computing advancements require cooling superconductors to temperatures below 1 Kelvin, while cryogenic systems enable the study of chemical reactions at extreme temperatures, impacting material science and pharmaceuticals. Cryogenic equipment is indispensable in various scientific disciplines, such as physics, chemistry, and biology, where ultra-low temperatures are required for experiments and analysis. It cools superconducting materials in physics, enabling breakthroughs in quantum computing and energy transmission. In chemistry, it aids in studying chemical reactions at extremely low temperatures, contributing to the development of new materials and pharmaceuticals. Additionally, it plays a pivotal role in biotechnology and life sciences by preserving biological samples, facilitating genetic research, and storing cells and tissues for regenerative medicine. As R&D efforts intensify across industries, including pharmaceuticals, electronics, and material science, the demand for precise and reliable cryogenic equipment grows. This equipment empowers researchers to explore new frontiers and make innovative discoveries, driving the market's expansion. Furthermore, advancements in cryogenic technology continue to enhance its versatility and efficiency, making it an indispensable tool for scientists and researchers worldwide.

Rising Product Utilization to Store and Transport Renewable Energy Sources

The rising product utilization to store and transport renewable energy sources fosters market growth. Cryogenic systems, particularly liquid hydrogen, and liquid oxygen storage are crucial in the emerging field of renewable energy. These systems play a pivotal role in storing excess energy generated from renewable sources, such as wind and solar power, which can be used during low energy production or high demand. As the renewable energy market grows, with global wind and solar capacity expected to reach 2,400 GW by 2027 (as per an industry report), the demand for cryogenic equipment increases. Moreover, cryogenic energy storage offers a scalable and environmentally friendly solution for grid stability, helping to balance the intermittency of renewable sources and ensuring a consistent power supply. The transition to clean energy sources has prompted increased investments in cryogenic infrastructure, including liquefied natural gas (LNG) for energy storage and transportation. As the world shifts towards sustainable energy solutions, the demand for cryogenic equipment in this context will continue rising, creating substantial growth opportunities for the cryogenic equipment market. This factor aligns with global efforts to reduce carbon emissions and transition to more environmentally friendly energy solutions, making cryogenic equipment a vital component in the renewable energy landscape.

Cryogenic Equipment Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global cryogenic equipment market report, along with forecasts at the global, country, and regional levels for 2025-2033. Our report has categorized the market based on equipment, cryogen, application and end use industry.

Analysis by Equipment:

- Tanks

- Pumps

- Heat Exchanger

- Valves

- Others

Tanks leads the market with around 63.3% of market share in 2024. Cryogenic tanks are indispensable for storing and transporting liquefied gases, such as liquid nitrogen, liquid oxygen, and liquefied natural gas (LNG). The increasing demand for LNG as a cleaner energy source and the expanding applications of cryogenic gases across industries like healthcare, aerospace, and electronics are propelling the need for these tanks. Furthermore, the development of smaller, more portable cryogenic tanks is opening new avenues for applications in healthcare, laboratories, and even emerging industries like space tourism.

The ever-growing focus on sustainability and reducing carbon emissions also drives the adoption of cryogenic tanks for storing renewable energy sources. As these tanks evolve to meet diverse requirements and environmental standards, they continue to be a linchpin in the market's expansion, facilitating the safe and efficient handling of cryogenic materials across various industries.

Analysis by Cryogen:

- Nitrogen

- Liquified Natural Gas

- Helium

- Others

Liquified natural gas leads the market with around 47.7% of the total cryogenic equipment market share in 2024. LNG is a supercooled form of natural gas, stored and transported at extremely low temperatures. The global transition toward cleaner energy sources has propelled the demand for LNG, making it a focal point in the cryogenic equipment market. Cryogenic technology, including specialized storage tanks and transport infrastructure, is pivotal in LNG's liquefaction, storage, and regasification. Its versatility spans multiple sectors, from powering vehicles to serving as a feedstock for various industries.

Compared to traditional fossil fuels, its role in reducing greenhouse gas emissions aligns with environmental goals. The LNG supply chain, reliant on cryogenic equipment, continuously evolves to meet growing energy demands and regulatory standards. As nations seek to reduce carbon footprints and embrace cleaner energy alternatives, the LNG sector's expansion underscores the importance of cryogenic equipment. This segment not only contributes to energy accessibility but also aligns with global sustainability efforts, emphasizing its prominent role in the future of energy and the cryogenic equipment market.

Analysis by Application:

- Storage

- Transportation

- Processing

- Others

Storage leads the market with around 45.2% of market share in 2024. Cryogenic storage involves safely preserving and containing materials at ultra-low temperatures, typically below -150 degrees Celsius (-238 degrees Fahrenheit). This application is fundamental in various industries, such as healthcare, biotechnology, energy, and aerospace. In healthcare, cryogenic storage is vital for preserving biological specimens, including cells, tissues, and genetic material, ensuring their viability for research, diagnostics, and medical treatments. Biotechnology companies rely on it to maintain valuable samples and compounds, supporting drug development and bioprocessing.

Furthermore, the energy sector utilizes cryogenic storage for liquefied natural gas (LNG), enabling efficient transportation and storage of clean energy. The aerospace industry depends on it for safely handling propellants like liquid oxygen and liquid hydrogen, which are essential for space exploration. As the demand for cryogenic storage solutions grows across these diverse industries, the cryogenic equipment market witnesses consistent expansion. Advancements in cryogenic storage technologies and the need for secure and environmentally friendly storage solutions further drive this segment's importance, underlining its crucial role in various sectors and the overall market.

Analysis by End Use Industry:

- Oil and Gas

- Energy and Power

- Food and Beverages

- Healthcare

- Marine and Aerospace

- Chemicals

- Others

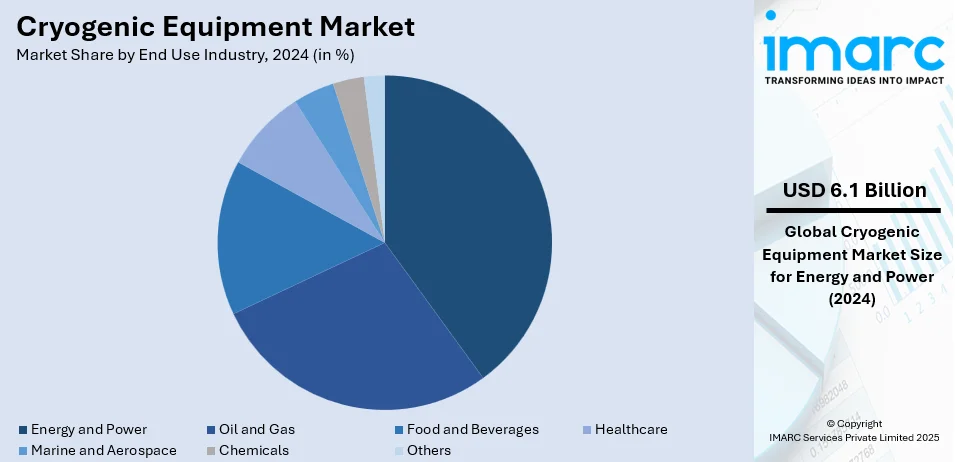

Energy and power leads the market with around 26.9% of market share in 2024. The energy and power sector is the largest end-use industry in the Cryogenic Equipment Market because of its critical need for efficient storage and transportation of liquefied gases. Cryogenic equipment is crucial for the production of liquefied natural gas (LNG) where it helps cool and store gas at ultra-low temperatures for easy transport and distribution. Growing global demand for LNG as an alternative source of energy further pushes the need for cryogenic solutions. Moreover, with the advancement in cryogenic technology, the generation of power especially through carbon capture and storage processes has become one of the biggest contributors to the industry's growth.

Regional Analysis:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

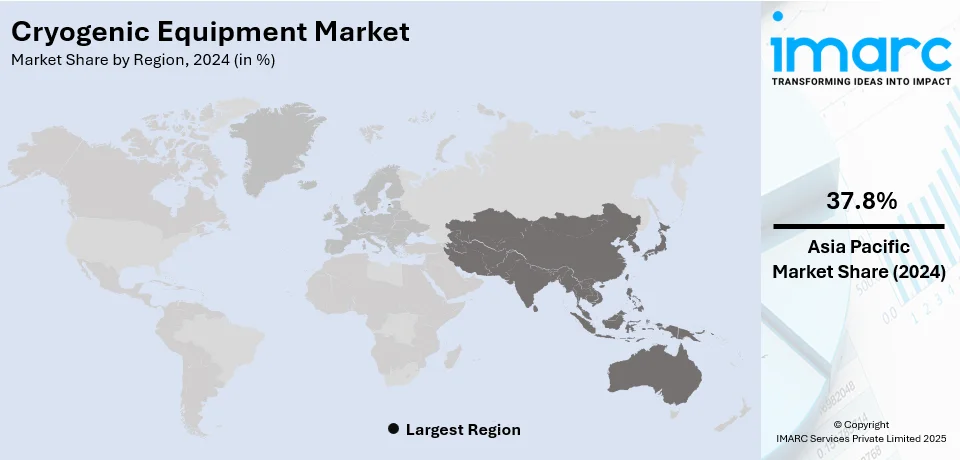

In 2024, Asia Pacific accounted for the largest market share of over 37.8%. Rapid industrialization and urbanization creating a positive cryogenic equipment market outlook across the region. Robust growth in sectors like manufacturing, chemicals, and healthcare necessitates using cryogenic technology for processes, storage, and transportation. Furthermore, the growing population and increasing disposable income levels in countries like China and India propel the healthcare and pharmaceutical sectors. Cryogenic equipment is integral in these sectors for storing and preserving medical samples, vaccines, and biological materials.

Moreover, the region is witnessing substantial advancements in space exploration and research, creating a need for cryogenic equipment in aerospace applications. Besides, as countries in the region prioritize sustainable and eco-friendly energy solutions, the use of cryogenic equipment for liquefied natural gas (LNG) production and storage is expanding. Additionally, the region's strong manufacturing base and growing technological capabilities contribute to the production and innovation of cryogenic equipment.

Key Regional Takeaways:

North America Cryogenic Equipment Market Analysis

The North American cryogenic equipment market is experiencing robust growth driven by rising demand for LNG exports and infrastructure expansion. The United States, a global leader in LNG exports benefits from competitive pricing and favorable geographic positioning fostering increased trade with key markets like Asia and Europe. The Canadian market is also contributing with investments in LNG export terminals and cryogenic technologies for hydrogen energy and carbon capture projects. Advancements in healthcare applications such as cryopreservation and cryosurgery and the growing use of industrial gases in food processing and manufacturing further fuel demand for cryogenic solutions. Government support for clean energy initiatives including hydrogen and LNG infrastructure enhances market growth. Key players in the region are leveraging these trends to strengthen their market presence and address the growing need for efficient, and high-quality cryogenic equipment.

United States Cryogenic Equipment Market Analysis

In 2024, the United States captured 86.70% of revenue in the North American market. The U.S. cryogenic equipment market is highly growing due to the growth in LNG exports from the country and its infrastructural development. According to industrial reports, in 2023, the United States overtook the UAE as India's second-largest LNG supplier, with exports reaching 3.09 million tonnes (MT) compared to 2.16 MT in 2022. LNG exports are driven by the competitive pricing of U.S. LNG due to weakening international LNG prices and favorable geographic positioning through the Cape of Good Hope, making it more competitive for markets like India. Increased LNG demand is mostly on the rise in Asia. As a result, liquefaction, transportation, and regasification processes for natural gas require higher quality cryogenic equipment. Therefore, the U.S. cryogenic equipment market benefits from this increase in the volume of trade in LNG due to further investment by the country in LNG infrastructure and expansion capacity. As the United States cements its position in international LNG exports, cryogenic equipment has an essential role to play in safeguarding and efficiently transporting LNG for a successful energy transition for the United States and in strengthening its foothold on global energy markets.

Europe Cryogenic Equipment Market Analysis

The cryogenic equipment market in Europe is bound to experience growth with growing demand from sectors like energy, healthcare, and food preservation. The European Green Deal, proposed by the European Commission, plans to mobilize USD 1.07 Trillion in sustainable investments in the next ten years directly supporting energy infrastructure, such as LNG terminals and cryogenic storage solutions. The Connecting Europe Facility (CEF) Energy program will provide around USD 5.72 Billion between 2021 and 2027 for projects to interconnect the EU's energy networks, thereby improving security of supply. Among key players are Germany, UK, and France; by 2025, Germany will spend USD 2.68 billion upgrading LNG terminals that will positively affect demand for cryogenic storage and transportation solutions. The healthcare sector's dependence on cryogenic technologies for biobanking and cryosurgery, combined with population growth and sustainability goals, are also fueling the demand for cryogenic solutions in Europe. The leading companies, Air Liquide and Messer Group, are capitalizing on these trends and thus strengthening their position in the market.

Latin America Cryogenic Equipment Market Analysis

In Latin America, there is a growth of the cryogenic equipment market caused by the growing demand for LNG and infrastructure investments. LNG imports in the region increased by almost 6% from August 2023, driven in part by rising demand from Brazil and Colombia, an industrial report indicated. Also, as of January 2023, the overall LNG volume imported to Latin America and the Caribbean was at 0.46 metric tons, according to an industrial report. Such an uptrend in imports also demonstrates the increasing demand for cryogenic storage and transportation solutions that are necessary for the supply of LNG. Brazil is one of the largest economies in this region and is currently investing in LNG infrastructure. Some of the new import terminals and regasification projects that are being developed. The increasing demand for cleaner energy sources and expanding use of natural gas in power generation and industrial applications is driving the demand for advanced cryogenic technologies. Yara International and Linde are among companies which play a key role in fulfilling the growing cryogenic needs in the region. The Latin American region is also benefited by energy security enhancement initiatives by their governments, which contribute significantly to the growth of this cryogenic equipment market within the region.

Middle East and Africa Cryogenic Equipment Market Analysis

In the Middle East, demand for cryogenic equipment is on the rise, especially in the UAE, due to the expansion of oil, gas, and LNG infrastructure by ADNOC. The company is actively engaged in offshore natural gas exploration with discoveries like the one in February 2022 off Abu Dhabi, International Trade Administration stated. The UAE will be self-sufficient in its gas supply by 2030, a move that will raise the demand for cryogenic storage and transport equipment for LNG, among other things. This is further heightened by ADNOC's new LNG plant in Fujairah, which it expects to double its export capacity to 9.6 million tons annually. Ongoing investments in the UAE include expansion downstream activities of USD 45 Billion and investment in Ruwais Derivatives Park at a value of USD 5 Billion, providing further significant opportunities for suppliers of cryogenic equipment. This investment also increases potential for sectors like industrial gas production and LNG processing. Efforts by ADNOC towards decarbonization and renewable energy investment, clean hydrogen, and carbon capture technology reflect a growth trend toward advanced cryogenic infrastructure within the region. As industrial projects like the first hydrogen electrolyzer plant are set up in the UAE, the Middle East will rely much on cryogenic technologies as the energy transition takes place. Combined with higher LNG production and export capacity, the UAE is taking the lead in the market for cryogenic equipment in the Middle East, providing significant opportunities for international suppliers.

Competitive Landscape:

Top companies are strengthening market growth through a combination of strategic initiatives. They are heavily investing in research and development, continually innovating and improving the efficiency and performance of cryogenic equipment. This not only caters to the growing demands of various industries but also promotes the adoption of these advanced solutions. Additionally, these companies are expanding their global presence by establishing partnerships, distribution networks, and manufacturing facilities in key regions, ensuring a wider reach and accessibility for their products. Furthermore, they prioritize sustainability by developing eco-friendly and energy-efficient cryogenic systems, aligning with global environmental regulations and the demand for greener technologies. Moreover, top players actively engage in mergers and acquisitions to broaden their product portfolios and gain access to complementary technologies, strengthening their market position. They also provide comprehensive customer support and after-sales services, enhancing customer satisfaction and loyalty. They leverage digitalization and Industry 4.0 technologies like IoT and data analytics to offer predictive maintenance and remote monitoring solutions, improving equipment reliability and minimizing downtime.

The report provides a comprehensive analysis of the competitive landscape in the cryogenic equipment market with detailed profiles of all major companies, including:

- Air Liquide S.A.

- Air Products and Chemicals Inc.

- Chart Industries Inc.

- Cryofab Inc.

- Cryoquip LLC (Nikkiso Co. Ltd.)

- Emerson Electric Co.

- Flowserve Corporation

- Herose GmbH

- INOX India Pvt. Ltd

- Linde Plc

- Parker-Hannifin Corporation

- Wessington Cryogenics

Recent Developments:

- November 2024: Inox India announced that they will deliver five cryogenic, specialized tanks to Highview Power for the Liquid Air Energy Storage (LAES) project in Manchester, UK. The order will be INOX India's maiden LAES contract. These tanks will enable the transition of the UK towards a cleaner form of energy by supporting a 300 MWh storage facility.

- September 2024: Air Products successfully completed the USD 1.81 billion divestiture of its LNG process technology and equipment business to Honeywell. The divestiture is a strategic step for Air Products towards more industrial gases and clean hydrogen focus. All assets, intellectual properties, manufacturing capabilities, and approximately 475 employees moved to Honeywell.

- July 2024: Flowserve Corporation purchased NexGen Cryo's LNG pumping technology, intellectual property rights, and related research and development in cryogenic LNG submerged pumps. This further develops LNG portfolio for Flowserve; it supports the strategy for a decarbonization, besides providing more efficient, reliable solutions for the markets related to liquefaction, shipping, and regasification.

- June 2024: Nikkiso Cryoquip LLC has achieved ISO 9001 certification. This is a testament to the company's commitment to quality and excellence in operations. The DNV issued the certification, which covers facilities in Kuala Lumpur, Houston, and Canterbury, and shows that Nikkiso Cryoquip is committed to high standards in cryogenic equipment manufacturing.

- March 2024: Chart Industries will produce jumbo cryogenic tanks up to 1,700 cubic meters for industries such as aerospace, hydrogen, LNG, and decarbonization, thus sustaining local job growth and the development of the economy.

Cryogenic Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Equipments Covered | Tanks, Pumps, Heat Exchanger, Valves, Others |

| Cryogens Covered | Nitrogen, Liquified Natural Gas, Helium, Others |

| Applications Covered | Storage, Transportation, Processing, Others |

| End Use Industries Covered | Oil and Gas, Energy and Power, Food and Beverages, Healthcare, Marine and Aerospace, Chemicals, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Air Products and Chemicals Inc., American Roller Company LLC, Durum Verschleißschutz GmbH, Lincotek Rubbiano S.p.A, Metallizing Equipment Co. Pvt. Ltd., Montreal Carbide Co. Ltd., Powder Alloy Corporation, Praxair Surface Technologies Inc. (Linde plc), Progressive Surface Inc., Wall Colmonoy Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cryogenic equipment market from 2019-2033.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global cryogenic equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the cryogenic equipment industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The cryogenic equipment market was valued at USD 22.73 Billion in 2024.

IMARC estimates the cryogenic equipment market to reach USD 34.40 Billion by 2033, exhibiting a CAGR of 4.23% during 2025-2033.

Key factors include growing LNG demand as a cleaner energy source, increasing healthcare applications like cryopreservation, the rise of renewable energy and hydrogen-based technologies, and advancements in space exploration.

In 2024, Asia Pacific accounted for the largest share of the Cryogenic Equipment Market, holding over 37.8% of the total market share. This dominance is driven by the rapid industrialization in countries like China, India, and Japan, which have significant demand for cryogenic equipment in sectors such as energy, healthcare, and manufacturing.

Some of the major players in the cryogenic equipment market include Air Products and Chemicals Inc., American Roller Company LLC, Durum Verschleißschutz GmbH, Lincotek Rubbiano S.p.A, Metallizing Equipment Co. Pvt. Ltd., Montreal Carbide Co. Ltd., Powder Alloy Corporation, Praxair Surface Technologies Inc. (Linde plc), Progressive Surface Inc., Wall Colmonoy Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)