Cross-Laminated Timber Market Size, Share, Trends and Forecast by Application, Product Type, Element Type, Raw Material Type, Bonding Method, Panel Layers, Adhesive Type, Press Type, Storey Class, Application Type, and Region, 2026-2034

Global Cross-Laminated Timber Market Size, Share, Trends & Forecast (2026-2034)

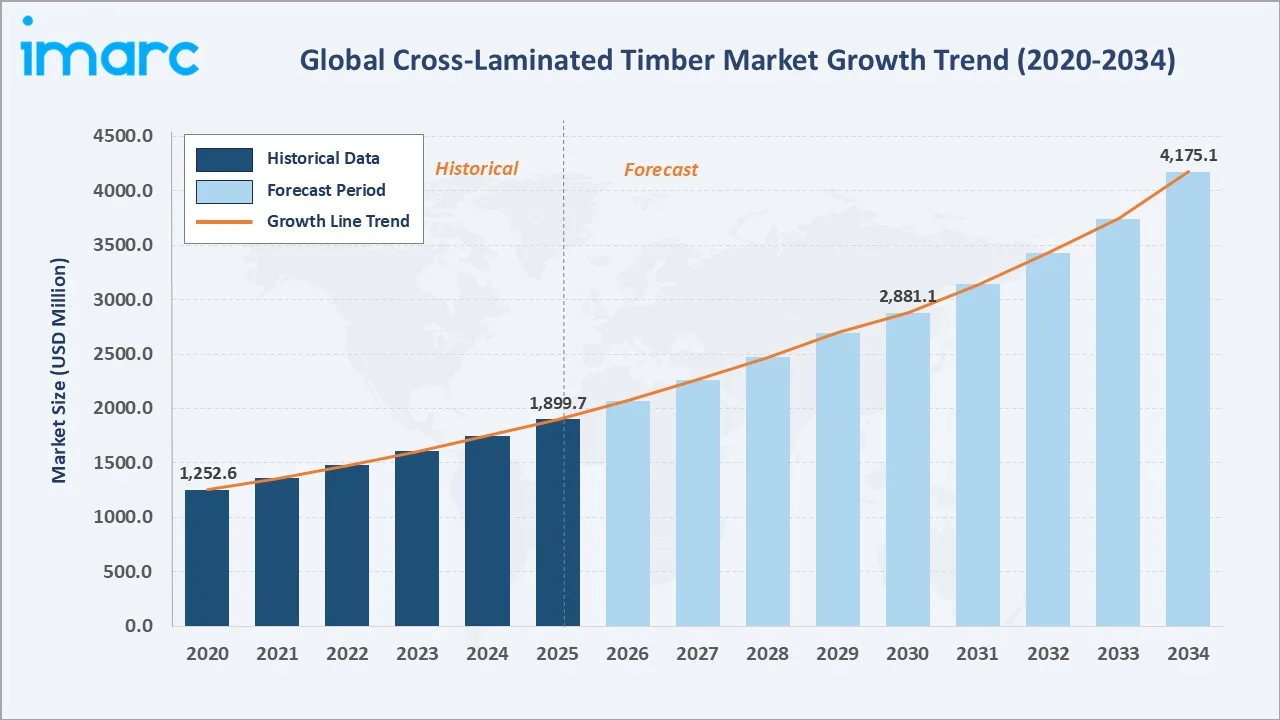

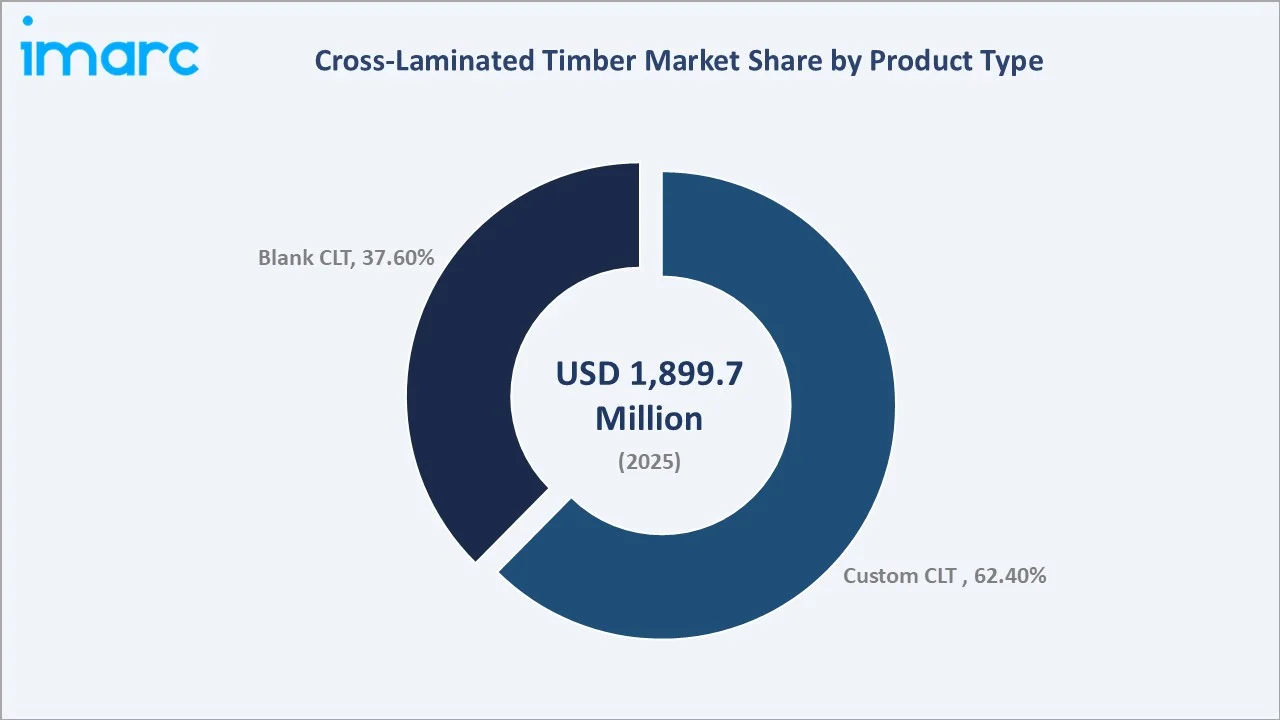

The global cross-laminated timber market was valued at USD 1,899.7 Million in 2025 and is projected to reach USD 4,175.1 Million by 2034, expanding at a CAGR of 8.7% during 2026-2034. The market's expansion is underpinned by the global pivot toward sustainable construction, mass timber adoption in mid- to high-rise buildings, and tightening carbon emission regulations across Europe and North America.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,899.7 Million |

|

Forecast Market Size (2034) |

USD 4,175.1 Million |

|

CAGR (2026-2034) |

8.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Largest Product Type Segment |

Custom CLT (62.4%) |

|

Largest Element Type |

Wall Panels (44.6%) |

|

Leading Region |

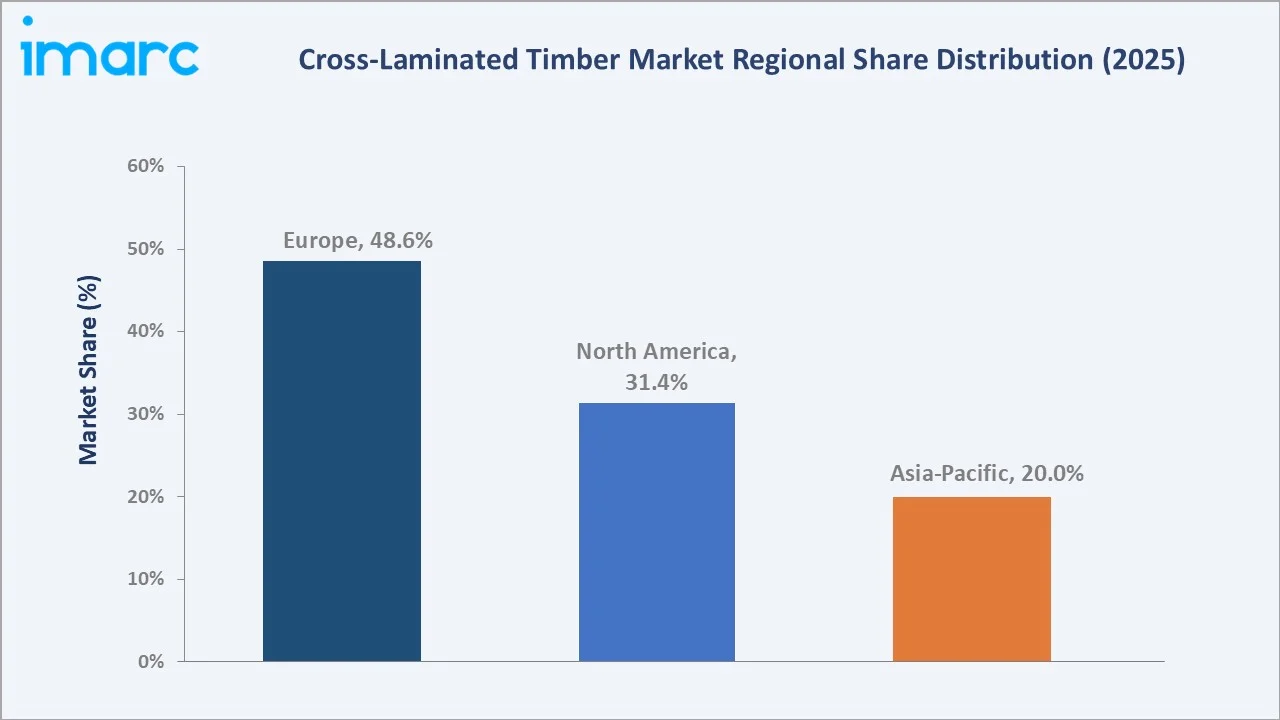

Europe (48.6%) |

Europe dominates the global Cross-Laminated Timber (CLT) market, accounting for 48.6% of revenues in 2025, supported by its well-established mass timber ecosystem, advanced manufacturing capabilities, and strong regulatory backing for sustainable construction.

To get more information on this market, Request Sample

The global CLT market is evolving with a growing emphasis on sustainable and low-carbon building materials, supported by rising environmental awareness and green building initiatives. Growth is further driven by urbanization, increasing adoption of prefabricated construction techniques, and the shift toward efficient, scalable solutions in modern infrastructure development.

Executive Summary

Cross-Laminated Timber is a structural wood panel product engineered by layering timber boards in alternating directions and bonding them with adhesives. The Global Cross-Laminated Timber Market reached USD 1,252.6 million in 2020 and grew to USD 1,899.7 million by 2025.

Key demand drivers include rising urbanization requiring faster, more efficient construction; increasing green building certifications (LEED, BREEAM) that reward timber use; and growing awareness of CLT's superior strength-to-weight ratio compared to steel and concrete.

By 2034, the market is forecast to reach USD 4,175.1 million. Europe will retain its leadership, while North America grows steadily at 31.4% share in 2025. Asia-Pacific, particularly Japan and Australia, is emerging as a high-potential frontier. Custom CLT dominates with 62.4% revenue share, and wall panel elements represent the single largest application at 44.6%.

Key Market Insights

|

Insight |

Data Point |

|

Largest Product Type Segment |

Custom CLT (62.4% share in 2025) |

|

Largest Element Type |

Wall Panels (44.6% share in 2025) |

|

Leading Region |

Europe (48.6% market share in 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Market Size (2025) |

USD 1,899.7 Million |

|

Projected Market Size (2034) |

USD 4,175.1 Million |

|

CAGR (2026-2034) |

8.7% |

|

Top Companies |

Binderholz GmbH, Stora Enso, KLH Massivholz GmbH, Mercer Mass Timber LLC, Mayr-Melnhof Holz Holding AG, Nordic Structures, Holzwerk Gebr. Schneider GmbH |

Key Analytical Observations Supporting The Above Data:

- Custom CLT held 62.4% revenue share in 2025, driven by architect-specific designs in high-rise residential and commercial buildings that demand precision-cut panels.

- Wall Panels accounted for 44.6% of element type revenue in 2025, favored for their load-bearing structural efficiency and ease of prefabrication.

- Europe accounted for 48.6% of Global Cross-Laminated Timber Market revenue in 2025, backed by long-standing mass timber regulations, building codes, and a mature supplier base.

- The CLT market is projected to more than double from USD 1,899.7 million (2025) to USD 4,175.1 million by 2034, creating USD 2.28 billion in incremental market opportunity.

- Asia-Pacific is the fastest-growing region, with Japan, Australia, and South Korea driving demand through new mass timber building codes introduced post-2022.

- Flooring Panels hold 26.8% share in 2025, with growing adoption in prefabricated modular housing and multi-storey CLT apartment blocks.

Global Cross-Laminated Timber Market Overview

Cross-Laminated Timber (CLT) is a prefabricated solid timber panel product made by gluing multiple layers of timber boards in perpendicular orientations. CLT is used primarily in residential, commercial, and institutional construction as a sustainable substitute for concrete and steel.

The industry ecosystem spans forestry management, sawmill operations, CLT manufacturing, digital fabrication, logistics, and end-user construction. Macroeconomic tailwinds include global decarbonization commitments (Paris Agreement targets), rising timber prices creating demand for efficient engineered wood products, and government subsidies for green infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

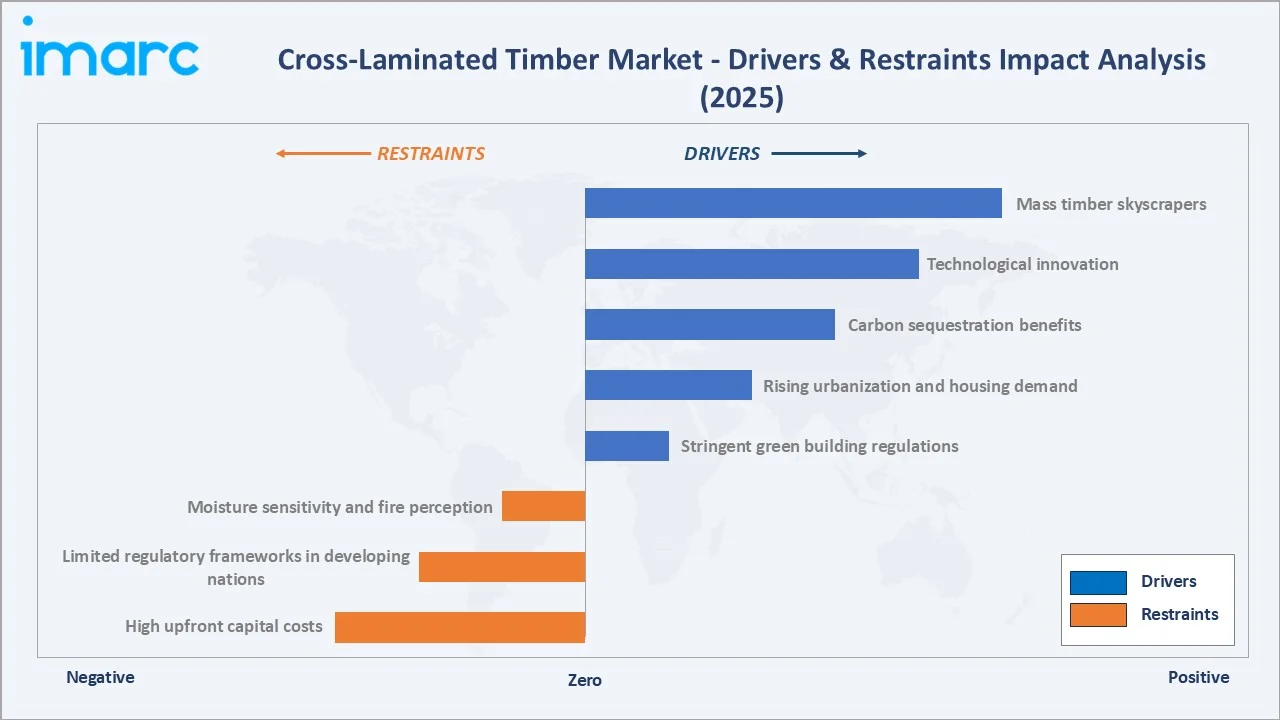

Market Drivers

- Stringent Green Building Regulations: Europe's Energy Performance of Buildings Directive (EPBD) and the UK Net Zero Carbon Buildings Standard are compelling architects and developers to adopt low-carbon CLT, with the EU construction sector accounting for 40% of total energy consumption as of 2024.

- Rising Urbanization and Housing Demand: With the 68% of the world population projected to live in urban areas by 2050, demand for prefabricated, fast-erect CLT buildings is surging. CLT construction timelines are 20-30% faster than concrete, reducing labor costs.

- Carbon Sequestration Benefits: CLT sequesters approximately 0.9 tonnes of CO2 per cubic meter, making it a preferred material under carbon trading markets. This benefit is increasingly priced into project economics.

- Technological Innovation: CNC precision cutting combined with BIM-driven design streamlines CLT fabrication by optimizing material usage and minimizing offcuts, thereby reducing waste and enhancing cost competitiveness compared to traditional materials like concrete.

Market Restraints

- High Upfront Capital Costs: CLT panels often come at a higher cost compared to conventional concrete, which can limit their adoption among cost-sensitive developers, particularly in emerging markets where access to financing is constrained.

- Limited Regulatory Frameworks in Developing Nations: Asia-Pacific and Latin American nations lack established mass timber building codes, creating uncertainty for developers and insurers. Only Japan (post-2022 law revision) and Australia (NCC 2022) have introduced enabling frameworks.

- Moisture Sensitivity and Fire Perception: Despite CLT's proven char-layer fire resistance, public perception and insurer risk models still penalize timber buildings, increasing project financing costs.

Market Opportunities

- Mass Timber Skyscrapers: Building codes in the US, such as the IBC 2021, now permit the construction of taller CLT structures, supporting buildings up to multiple storeys. This regulatory progress has contributed to a growing pipeline of mass timber projects across the Americas, particularly for mid- to high-rise developments, reflecting increasing investment and adoption in the sector.

- Asia-Pacific Construction Boom: Japan, South Korea, and Australia are revising building codes to enable mass timber construction. Japan has strengthened its push toward timber use in public infrastructure through dedicated government funding aimed at encouraging wider implementation of wood-based building materials.

Market Challenges

- Supply Chain Fragmentation: CLT manufacturing is largely concentrated in a few regions, including Austria, Germany, and Canada, leading to supply constraints in other markets. The need to transport large panels over long distances increases logistics complexity and adds to overall project costs in regions located far from production hubs.

- Skilled Labor Shortage: CLT construction requires specialized carpentry and digital fabrication skills. FIEC estimates that around 2 million additional construction workers will be needed by 2030 in the EU, constraining project execution capacity.

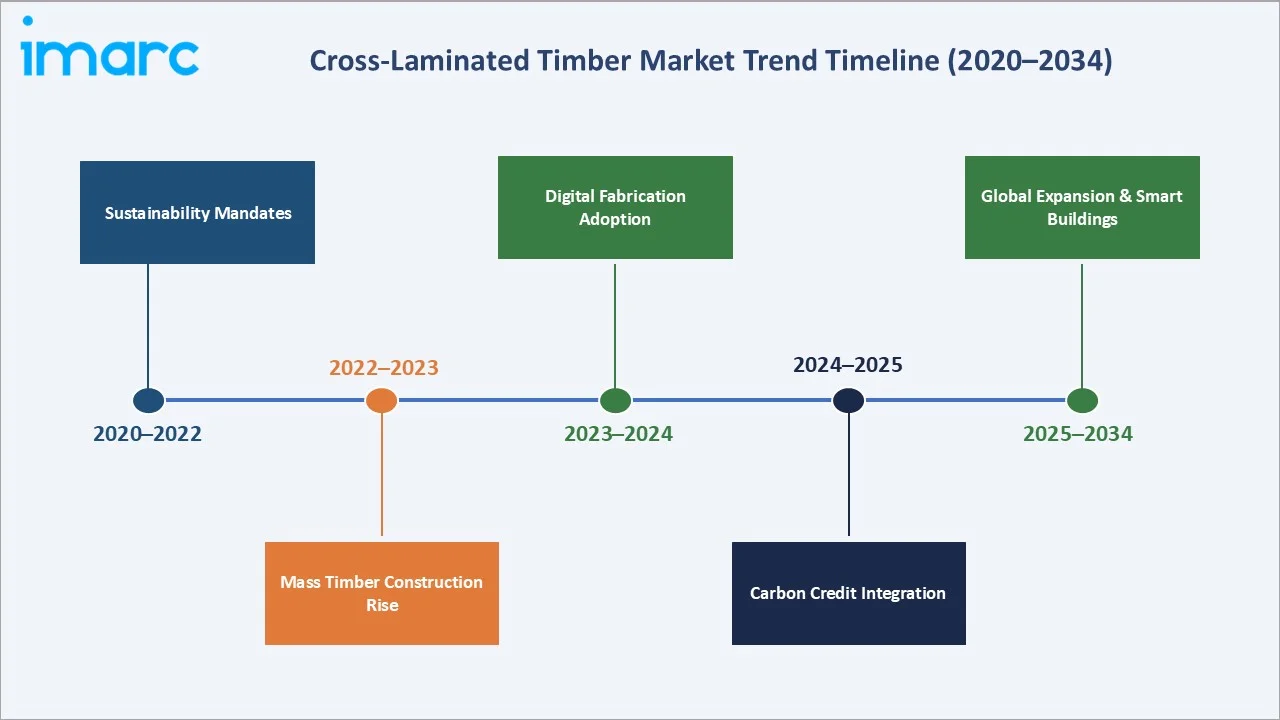

Emerging Market Trends

1: Mass Timber in High-Rise Construction

The international adoption of mass timber skyscrapers is accelerating. The Brock Commons Tallwood House (18 storeys, Vancouver) and Mjosa Tower (18 storeys, Norway) demonstrated structural viability for tall timber. Over 600 mass timber buildings have now been completed in Canada, with 124 projects under construction or in planning stages. This trend is reshaping urban skylines and converting conventional concrete markets to CLT.

2: Carbon Credit Integration

CLT manufacturers are increasingly engaging in voluntary carbon markets by leveraging the carbon sequestration benefits of timber. By certifying and verifying the stored carbon in CLT panels, they can bundle these products with carbon credits, creating an additional revenue stream. This approach is also encouraging ESG-driven procurement, as corporations with net-zero targets seek low-carbon construction materials.

3: Biophilic Design Integration

Architects and interior designers are integrating exposed CLT surfaces as a biophilic design feature, boosting demand for aesthetics-grade Custom CLT. Wellness-focused commercial real estate segments - particularly offices, hotels, and healthcare facilities are driving a premium pricing tier for exposed-grain CLT applications.

4: Public Procurement Mandates

Governments in France, the Netherlands, and Canada have legislated minimum timber content in new public buildings. France's RE2020 regulation (2022) mandates 50% bio-sourced materials in new public construction. These mandates are creating stable, policy-backed demand floors for CLT manufacturers.

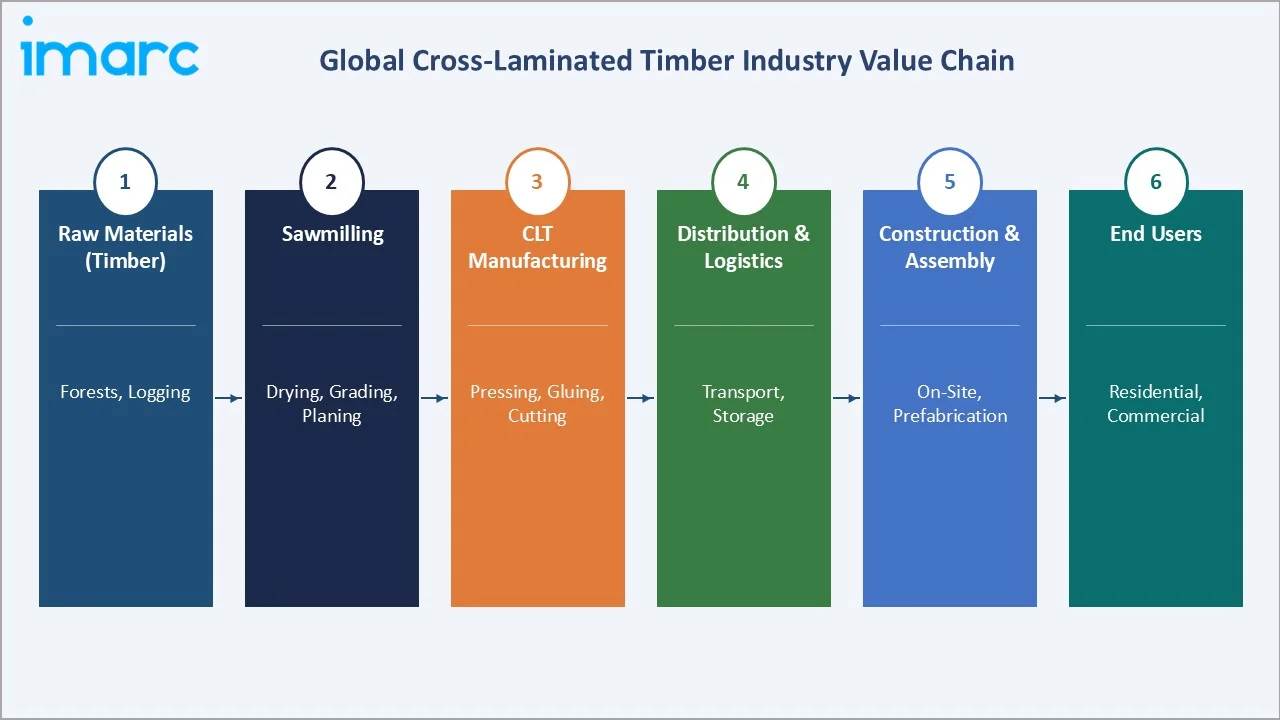

Industry Value Chain Analysis

The CLT industry value chain encompasses six core stages, from raw material sourcing to end-user delivery. Each stage contributes to the total delivered cost of CLT, with manufacturing representing the highest value-add.

|

Stage |

Key Activities |

Key Players |

|

Raw Materials (Timber) |

Sustainable forest harvesting, FSC/PEFC certification |

Forest owners, timber estates |

|

Sawmilling |

Log grading, kiln drying, dimensional cutting of boards |

Binderholz Sawmills |

|

CLT Manufacturing |

Board lay-up, pressing, adhesive bonding, CNC profiling |

Binderholz, KLH, Stora Enso |

|

Distribution & Logistics |

Panel transport, customs clearance, on-site delivery |

Freight carriers, timber distributors |

|

Construction & Assembly |

Panel installation, MEP integration, finishing |

General contractors, specialist timber builders |

|

End Users |

Residential, commercial, institutional building occupants |

Property developers, governments, REITs |

Margins are highest at the CLT manufacturing stage, where differentiation through precision fabrication, species selection, and sustainability certifications drives premium pricing. Distribution costs represent a significant share of total delivered price, especially for transcontinental trade flows from European manufacturers to Asia-Pacific buyers.

Technology Landscape

1 Advanced Adhesive Systems

Polyurethane (PUR) and melamine-formaldehyde (MF) adhesives dominate CLT bonding, accounting for a majority of bonding method market share in the coming years. Emerging formaldehyde-free adhesive technologies are gaining regulatory approval in Europe, addressing indoor air quality concerns and enabling CLT adoption in healthcare and educational facilities.

2 Digital Fabrication & BIM

CNC 5-axis routing machines enable cutting tolerances of ±0.5 mm, essential for modular CLT construction. BIM-to-fabrication software (e.g., Cadwork, ArchiCAD) allows direct data transfer from design to machine.

3 Smart Connectivity & Sensor Integration

Embedded IoT sensors in CLT panels are an emerging technology being piloted in smart building projects. These sensors monitor moisture, structural load, and temperature in real time, enabling predictive maintenance and reducing building operational costs. Three commercial projects utilizing embedded CLT sensors were operational in Europe as of 2024.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Application | Residential | 🔒 | 2025 |

| Product Type | Custom CLT | 62.4% | 2025 |

| Element Type | Wall Panels | 44.6% | 2025 |

| Raw Material Type | Spruce | 🔒 | 2025 |

| Bonding Method | Adhesively Bonded | 🔒 | 2025 |

| Panel Layers | 3-Ply | 🔒 | 2025 |

| Adhesive Type | PUR (Polyurethane) | 🔒 | 2025 |

| Press Type | Hydraulic Press | 🔒 | 2025 |

| Storey Class | Low-Rise Buildings (1-4 Storeys) | 🔒 | 2025 |

| Application Type | Structural Applications | 🔒 | 2025 |

| Region | Europe | 48.6% | 2025 |

By Product Type

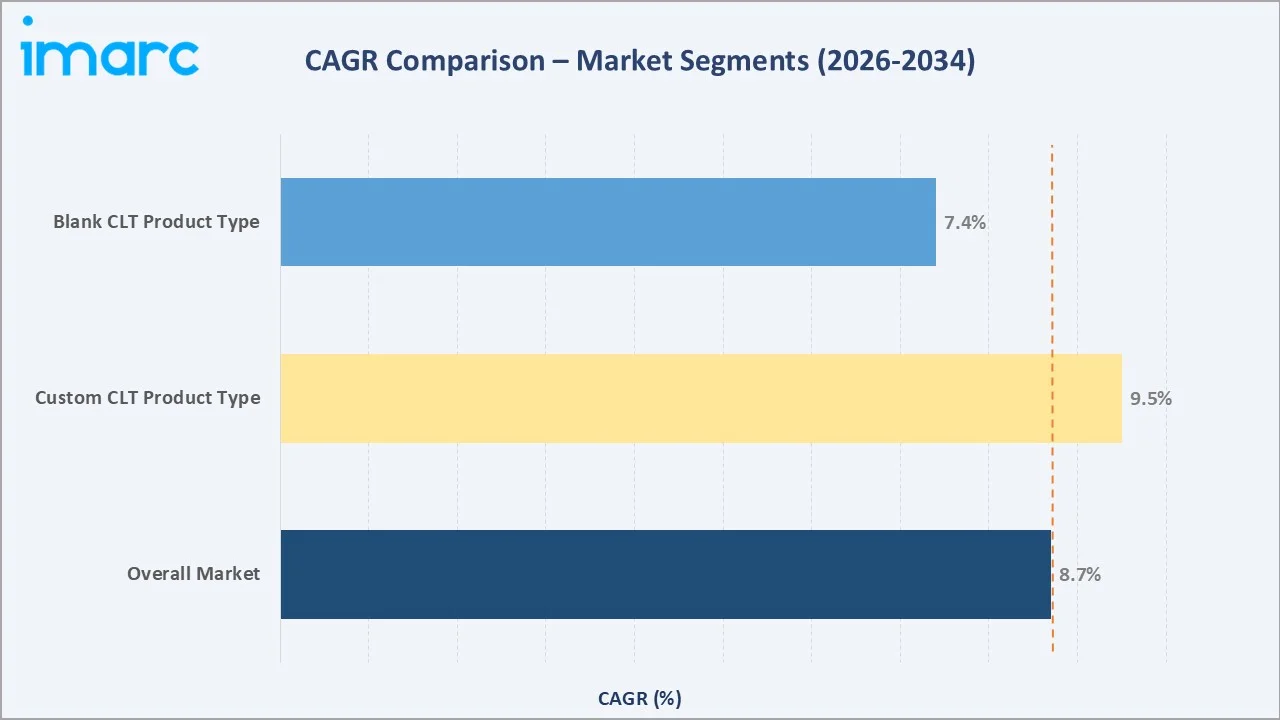

Custom CLT (62.4% share, 2025): Custom CLT panels are precision-manufactured to architect-specified dimensions, angles, and surface finishes. They serve the premium residential, commercial, and institutional segments. The segment is growing at above-market rates due to rising demand for bespoke mass timber architecture, biophilic office interiors, and complex structural geometries enabled by CNC fabrication.

To access detailed market analysis, Request Sample

The Custom CLT segment is expected to maintain its lead through 2034, supported by expanding green building certification requirements and the growing pipeline of high-rise mass timber projects globally. Blank CLT growth will be driven by modular housing and government-backed affordable housing programs in Asia-Pacific and the Americas.

By Element Type

Wall Panels (44.6% share, 2025): Wall panels represent the single largest CLT element type, used as both load-bearing and non-structural wall systems in residential and commercial construction. Their versatility in achieving Passive House and net-zero energy standards makes them the preferred choice for envelope systems. The segment benefits from favorable thermal mass properties and the ease of prefabricating window and door openings at the factory, reducing on-site labor by 25-35%.

Regional Market Insights

The CLT market exhibits distinct regional dynamics, shaped by regulatory environments, construction culture, timber availability, and building code maturity.

|

Region |

Market Share (2025) |

Key Growth Drivers |

Key Countries |

|

Europe |

48.6% |

Mature mass timber codes, EPBD mandates, large timber supply base |

Austria, Germany, UK, Norway, France |

|

North America |

31.4% |

IBC 2021 tall timber codes, US federal green building programs |

USA, Canada |

|

Asia-Pacific |

20.0% |

New timber building codes (Japan 2022, NCC Australia 2022) |

Japan, Australia, South Korea |

Europe (48.6% share, 2025): Europe is the global Cross-Laminated Timber market leader, benefiting from decades of mass timber construction experience originating in Austria and Germany in the 1990s. These countries collectively account for 70% of the global production of cross-laminated timber (CLT).

Competitive Landscape

The Global Cross-Laminated Timber Market is moderately concentrated. The top 5 players collectively account for approximately 45-55% of global production capacity. European manufacturers dominate, while North American players lead in the Americas market. New entrants from Asia-Pacific are expanding regional production capacity.

|

Company Name |

Brand / Division |

Headquarters |

Market Position |

|

Binderholz GmbH |

binderholz CLT BBS |

Austria |

Market Leader |

|

Stora Enso |

Sylva |

Finland |

Market Leader |

|

KLH Massivholz GmbH |

KLH |

Austria |

Strong Challenger |

|

Mercer Mass Timber LLC |

Mercer Mass Timber (MMT) |

USA |

Regional Leader |

|

Mayr-Melnhof Holz Holding AG |

MMcrosslam |

Austria |

Established Player |

|

Nordic Structures |

Nordic X-Lam |

Canada |

Emerging |

|

Holzwerk Gebr. Schneider GmbH |

best wood SCHNEIDER GmbH |

Germany |

Niche Player |

The competitive landscape is defined by manufacturing scale, geographic reach, species diversity, and sustainability certification portfolios.

Key Company Profiles

Binderholz GmbH

Binderholz GmbH is Austrian family-owned timber company founded in 1950; one of the world's largest CLT producers with more than 6,000 employees are working at the overall 60 company locations.

- Product Portfolio: Structural CLT panels, glulam, and solid timber construction elements

- Recent Developments: In 2022, The binderholz Group has completed the acquisition of BSW Timber Ltd, the largest sawmill group in the UK, through its subsidiary Binderholz UK Holding GmbH. With this deal, the company strengthens its position as Europe’s largest player in the sawmill and solid wood processing industry.

- Strategic Focus: Vertical integration from forest management to finished CLT; expanding distribution to the US and UK markets.

Stora Enso

Stora Enso Oyj is a leading Finnish-Swedish forest industry company and one of the world’s largest providers of renewable, wood-based solutions. Headquartered in Helsinki, Finland, the company focuses on replacing fossil-based materials with sustainable alternatives.

- Product Portfolio: CLT, glulam, LVL, and building systems solutions; offers complete mass timber building packages.

- Recent Developments: In 2023, Stora Enso Oyj is advancing low-carbon construction through its Sylva range of prefabricated wood-based building elements. The customizable solutions support diverse building types, including residential, commercial, and institutional projects, while utilizing sustainably sourced wood from European forests.

- Strategic Focus: Scaling mass timber building systems globally

KLH Massivholz GmbH

KLH Massivholz GmbH is Austrian CLT pioneer founded in 1999; credited with early CLT commercialization in Europe. Operates two production facilities in Austria.

- Product Portfolio: KLH CLT panels, custom widths up to 4.8 m and lengths up to 16.5 m.

- Recent Developments: In 2026, KLH Massivholz GmbH has introduced a major update to its statics2d software, adding advanced calculation capabilities for structural analysis of CLT systems.

- Strategic Focus: Premium custom CLT for iconic architecture and sustainable urban developments.

Market Concentration Analysis

The Global Cross-Laminated Timber Market exhibits moderate concentration. The top 5 manufacturers including Binderholz GmbH, Stora Enso, KLH Massivholz GmbH, Mercer Mass Timber LLC, Mayr-Melnhof Holz Holding AG collectively hold an estimated 45-55% of global production capacity as of 2025. The remaining share is distributed across 50+ smaller regional and national manufacturers.

The market is moderately fragmented at the regional level, with Europe having the most consolidated production base. In North America, the market is evolving rapidly with new capacity investments. Asia-Pacific remains highly fragmented, with most producers serving local or sub-regional markets.

Investment & Growth Opportunities

Fastest Growing Segments

- Custom CLT for high-rise mass timber: The growing pipeline of planned tall timber projects in North America represents a significant multi-billion-dollar opportunity for precision CLT manufacturers with advanced CNC capabilities.

- Flooring panels for modular housing: Government-backed affordable housing programs in the UK, Australia, and USA are driving demand for prefabricated CLT floor systems, with lead times as short as 8 weeks versus 16 weeks for concrete.

Emerging Markets

- Japan (post-2022 building code reform): The Japanese government’s timber building promotion fund is driving increased demand for imported CLT, as domestic production capacity remains insufficient to meet growing requirements.

- Southeast Asia: Singapore's Building and Construction Authority (BCA) launched a mass timber roadmap in 2023. Vietnam and Indonesia are exploring CLT for eco-tourism and mid-rise urban housing applications.

Venture Investment Trends

- Mass timber technology startups are attracting significant annual VC and private equity investment globally, focusing on areas such as digital fabrication, carbon credit platforms for CLT, and integrated mass timber building solutions.

- The U.S. Department of Energy and United States Department of Agriculture are co-funding multiple mass timber research and demonstration projects, creating strong innovation opportunities for domestic CLT manufacturers.

Future Market Outlook (2026-2034)

The CLT market is positioned for sustained, above-construction-industry-average growth through 2034. The market will reach an estimated USD 2,881.1 million by 2030 and USD 4,175.1 million by 2034, implying a CAGR of 8.7% during the forecast period.

Key transformative forces shaping the outlook include: (1) Carbon pricing mechanisms in will increase the cost of conventional concrete, making CLT economically competitive on a lifecycle basis. (2) Asia-Pacific regulatory maturation - Japan, South Korea, Australia, and potentially China introducing enabling building codes will create a new, large demand center by 2028-2030.

The CLT market is transitioning from a niche, premium-project material to a mainstream structural option. By 2034. This transition represents a generational growth opportunity across the entire CLT value chain.

Research Methodology

This report is based on a multi-layer research framework combining primary data collection, secondary intelligence synthesis, and proprietary forecasting models.

Primary Research

Over 200 structured interviews were conducted with CLT manufacturers, architects, construction developers, building product distributors, regulatory bodies, and industry associations across Europe, North America, and Asia-Pacific. Primary sources provided current production capacity data, pricing intelligence, and demand pipeline visibility.

Secondary Research

Secondary research encompassed analysis of company annual reports, government construction statistics (Eurostat, US Census Bureau, ABS Australia), patent databases, trade association publications (WoodWorks, European Wood), and peer-reviewed academic studies on mass timber performance and lifecycle carbon analysis.

Forecasting Models

Market sizing employs a bottom-up and top-down triangulation approach. Bottom-up modeling aggregates manufacturer production data and regional demand. Top-down modeling benchmarks CLT's share of overall construction activity by region. CAGR projections are validated against macroeconomic construction forecasts (Oxford Economics, IHS Markit) and regional building permit data through 2025.

Cross-Laminated Timber Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD, Cubic Metres |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Residential, Educational Institutes, Government/Public Buildings, Commercial Spaces |

| Product Types Covered | Custom CLT, Blank CLT |

| Element Types Covered | Wall Panels, Flooring Panels, Roofing Slabs, Others |

| Raw Material Types Covered | Spruce, Pine, Fir, Others |

| Bonding Methods Covered | Adhesively Bonded, Mechanically Fastened |

| Panel Layers Covered | 3-Ply, 5-Ply, 7-Ply, Others |

| Adhesive Types Covered | PUR (Polyurethane), PRF (Phenol Resorcinol Formaldehyde), MUF (Melamine-Urea-Formaldehyde), Others |

| Press Types Covered | Hydraulic Press, Vacuum Press, Pneumatic Press, Others |

| Storey Class Covered | Low-Rise Buildings (1-4 Storeys), Mid-Rise Buildings (5-10 Storeys), High-Rise Buildings (More than 10 Storeys) |

| Application Types Covered | Structural Applications, Non-Structural Applications |

| Regions Covered | Asia Pacific, Europe, North America |

| Countries Covered | United States, Canada, Austria, Germany, Italy, Switzerland, Czech Republic, Spain, Norway, Sweden, United Kingdom, Australia, New Zealand, Japan, China, Taiwan |

| Companies Covered | Binderholz GmbH, Stora Enso, KLH Massivholz GmbH, Mercer Mass Timber LLC, Mayr-Melnhof Holz Holding AG, Nordic Structures, Holzwerk Gebr. Schneider GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cross-laminated timber market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global cross-laminated timber market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cross-laminated timber industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cross Laminated Timber Market Report

The Global Cross-Laminated Timber Market was valued at USD 1,899.7 million in 2025, up from USD 1,252.6 million in 2020, reflecting strong demand growth driven by sustainable construction mandates and mass timber adoption.

The market is forecast to grow at a CAGR of 8.7% between 2026 and 2034, reaching USD 4,175.1 million by 2034, driven by green building regulations and expanding mass timber building codes globally.

Europe dominates with a 48.6% market share in 2025, backed by Austria's large CLT production base, EU green building directives, and long-established mass timber construction practices in Germany, Norway, and the UK.

Custom CLT holds 62.4% of the market in 2025. Its dominance reflects strong architect-driven demand for precision-fabricated panels used in complex mass timber building designs and high-rise residential projects.

Asia-Pacific is the fastest-growing region, driven by Japan's revised 2022 building code, Australia's NCC 2022, and South Korea's mass timber pilot programs. The region held 20.0% of global market share in 2025.

Wall panels lead with 44.6% share in 2025, preferred for their load-bearing efficiency, prefabrication compatibility, and superior thermal insulation properties enabling energy-efficient building envelopes.

Key players include Binderholz GmbH, Stora Enso, KLH Massivholz GmbH, Mercer Mass Timber LLC, Mayr-Melnhof Holz Holding AG, Nordic Structures, and Holzwerk Gebr. Schneider GmbH.

Key drivers include green building regulations (EPBD, RE2020), the mass timber skyscraper boom enabled by updated building codes (IBC 2021), carbon credit incentives, and the 20-30% faster construction timelines CLT offers versus concrete.

Major challenges include limited building codes in developing markets, moisture sensitivity concerns, perception barriers with fire safety insurers, and concentrated supply chain in Central Europe.

The Global Cross-Laminated Timber Market is projected to reach USD 2,881.1 million by 2030.

Custom CLT is precision-cut to specific dimensions and profiles for bespoke architectural applications. Blank CLT uses standard dimensions for repetitive construction, prioritizing cost efficiency over design flexibility.

Asia-Pacific offers substantial growth opportunities, supported by Japan’s timber promotion initiatives, Australia’s expanding mass timber project pipeline, and South Korea’s pilot programs. Together, these developments are expected to significantly increase demand and add considerable value to the CLT market by 2030.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)