Contrast Media Injectors Market Report by Product Type (Consumables, Injector Systems), Injectors Type (Single-head Injectors, Dual-head Injectors, Syringeless Injectors), Application (Radiology, Interventional Cardiology, Interventional Radiology), End User (Hospitals, Ambulatory Surgery Centers, Diagnostics Imaging Centers), and Region 2025-2033

Contrast Media Injectors Market Size:

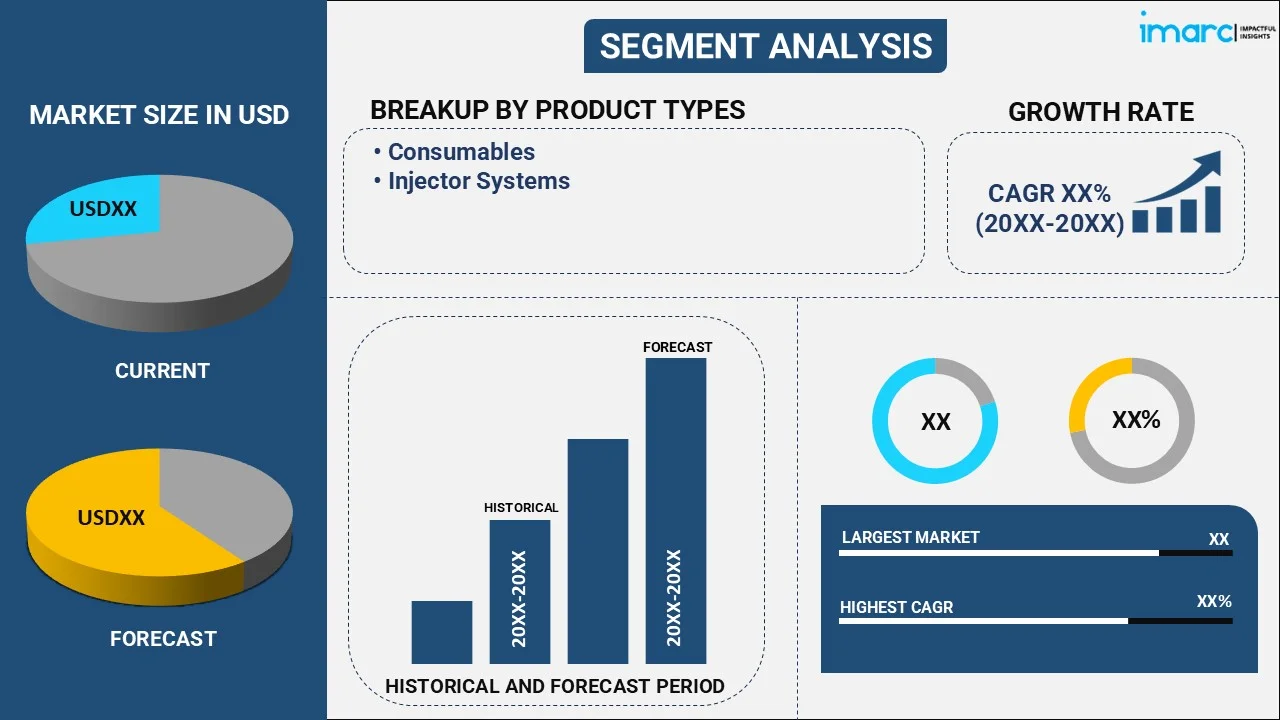

The global contrast media injectors market size reached USD 1.8 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 2.8 Billion by 2033, exhibiting a growth rate (CAGR) of 4.82% during 2025-2033. The market is experiencing significant growth mainly driven by the rising prevalence of chronic diseases, the growing demand for minimally invasive procedures and the rising number of diagnostic imaging procedures. Technological advancements in injector systems are also enhancing the efficiency and liquidity of contrast media delivery, thereby creating a positive market outlook.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 1.8 Billion |

|

Market Forecast in 2033

|

USD 2.8 Billion |

| Market Growth Rate 2025-2033 | 4.82% |

Contrast Media Injectors Market Analysis:

- Major Market Drivers: Key market drivers include the rising prevalence of chronic diseases such as cardiovascular conditions and cancer which demands for frequent diagnostic imaging procedures. The growing preference for minimally invasive procedures which require precise imaging for guidance also boosts the demand for contrast media injectors. Technological advancements in imaging technologies including enhanced injector systems with automated controls and improved safety features further drives the market growth. In line with this, the expansion of healthcare infrastructures in developing regions and the rising healthcare expenditure across the world are contributing positively to the market’s expansion.

- Key Market Trends: Key trends in the market include the integration of advanced technologies like AI and machine learning to enhance precision and automate injection protocols. There is also a growing shift towards consumable based injector systems to improve efficiency and reduce waste. The market is witnessing a rise in dual head injectors allowing for simultaneous use of different contrast agents. Furthermore, the rising focus on patient safety has led to development of injectors with improved safety and automated data recording.

- Geographical Trends: Geographical trends in the market show significant growth in North America and Europe due to advanced healthcare infrastructure and high demand for diagnostic imaging. In Asia-Pacific, rapid urbanization, expanding healthcare facilities, and increasing prevalence of chronic diseases are driving market expansion. Emerging markets in Latin America and the Middle East are also witnessing growth, supported by rising healthcare investments and the adoption of advanced imaging technologies. These regions are increasingly adopting innovative injectors to enhance diagnostic capabilities.

- Competitive Landscape: Some of the major market players in the contrast media injectors industry include APOLLO RT Co. Ltd., Bayer AG, Bracco Imaging S.p.A., General Electric Company, Guerbet, Medtron AG, Nemoto Kyorindo Co. Ltd., Shenzhen Anke High-tech Co. Ltd., Shenzhen Seacrown Electromechanical Co. Ltd., Sino Medical-Device Technology Co. Ltd. and ulrich GmbH & Co. KG, among many others.

- Challenges and Opportunities: Market faces various challenges including the high cost of advanced injectors and contrast media, which can limit accessibility in lower-income regions. Regulatory hurdles and stringent approval processes also pose barriers to market entry for new players. However, opportunities are emerging due to the increasing demand for personalized medicine and precision diagnostics, which require sophisticated imaging techniques. Technological advancements, such as automated injectors and AI integration, present significant growth prospects. Additionally, the rising incidence of chronic diseases and expanding healthcare infrastructure in developing regions offer new markets for contrast media injectors, driving innovation and adoption in diverse healthcare settings.

Contrast Media Injectors Market Trends:

Integration of Advanced Technologies

The integration of advanced technologies, such as artificial intelligence (AI) and machine learning (ML), in contrast media injectors is transforming the market by enhancing the precision and safety of injection processes. AI algorithms can analyze patient-specific data to optimize contrast media dosage, minimizing risks and improving diagnostic outcomes. Machine learning helps automate injection protocols, reducing human error and ensuring consistent performance across various procedures. These technologies also facilitate real-time monitoring and adjustments, providing better control over the injection process. As healthcare providers increasingly adopt these smart injectors, the market is poised for growth, driven by the demand for more accurate and efficient imaging solutions. For instance, in November 2023, German medical device manufacturer Ulrich Medical partnered with Bracco Imaging for the distribution of an MRI contrast media injector in the U.S. Ulrich Medical has submitted a premarket notification 510(k) to the U.S. Food and Drug Administration for the syringeless MRI injector, marking the finalization of the distribution agreement. This strategic cooperation is set to make the MRI injector available as soon as it is commercially released in the U.S.

Rising Adoption of Dual-Head Injectors

Dual-head injectors are becoming increasingly popular because they allow simultaneous injection of two different contrast agents, which improves workflow efficiency and patient throughput in diagnostic imaging procedures. This technology enables more complex imaging studies without the need for multiple injections or manual handling of different agents. By reducing preparation time and enhancing the accuracy of contrast delivery, dual-head injectors streamline radiology workflows, minimize patient discomfort, and optimize resource utilization, making them a valuable addition to modern imaging departments seeking to improve operational efficiency. For instance, in March 2023, Medtron AG introduced the Accutron CT-D Vision, a state-of-the-art CT double-piston contrast agent injector for computed tomography. The injector boasts a user-friendly interface, RIS/PACS interface, comprehensive traceability of injection data, and flexible mobility in radiology environments. Additionally, it has been approved for contrast-enhanced mammography, enhancing imaging quality, supporting efficient workflow, and improving patient safety by reducing contrast agent exposure in the veins.

Expansion in Emerging Markets

The expansion in emerging markets is a significant trend in the contrast media injectors market, driven by increased healthcare investments and the broader availability of advanced medical technologies. Countries in Asia-Pacific, Latin America, and the Middle East are witnessing rapid urbanization and economic growth, which fuels the development of healthcare infrastructure. Governments and private sectors are investing in modern medical equipment, including imaging technologies that require contrast media injectors. Additionally, the rising incidence of chronic diseases in these regions is facilitating the demand for diagnostic imaging. This growing accessibility to advanced healthcare services creates opportunities for market players to introduce innovative injectors, thereby boosting the market growth. According to industry reports, India's healthcare sector, valued at US$110 billion in 2016, is projected to reach US$638 billion by 2025. With 7.5 million employees, the sector faces a growing demand for healthcare professionals, driven by a shortage in the workforce. Aiming to increase public expenditure on healthcare, the Health Ministry targets 2.5% of GDP by FY25. The government allocated Rs. 90,659 crore for the Ministry of Health and Family Welfare in the Interim Union Budget 2024-25.

Contrast Media Injectors Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2025-2033. Our report has categorized the market based on product type, injectors type, application and end user.

Breakup by Product Type:

- Consumables

- Syringes

- Tubes

- Others

- Injector Systems

- CT Injectors

- MRI Injectors

- Angiography Injectors

- Accessories

Consumables accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product type. This includes consumables (syringes, tubes, others) and injector systems (CT injectors, MRI injectors, angiography injectors, and accessories). According to the report, the consumables segment accounted for the largest market share.

Consumables, such as syringes, tubing, and disposable injector parts, account for the majority of the contrast media injectors market share due to their recurring use in imaging procedures. These items are essential for each contrast injection, driving constant demand regardless of the type of injector system used. Hospitals and imaging centers prioritize consumables to ensure safety, hygiene, and compliance with regulations. The single-use nature of consumables minimizes cross-contamination risks, making them crucial in maintaining high standards of patient care. As diagnostic imaging procedures increase globally, the steady requirement for consumables continues to dominate the market, providing ongoing revenue for manufacturers. These factors are creating a positive contrast media injectors market outlook, highlighting the importance of consumables in ensuring safe and effective imaging procedures.

Breakup by Injectors Type:

- Single-head Injectors

- Dual-head Injectors

- Syringeless Injectors

Single-head Injectors holds the largest share of the market

A detailed breakup and analysis of the market based on the injectors type have also been provided in the report. This includes single-head injectors, dual-head injectors, and syringeless injectors. According to the report, the single-head injectors segment accounted for the largest market share.

Single-head injectors hold the largest share of the contrast media injectors market due to their widespread use and cost-effectiveness. These injectors are designed for administering a single type of contrast agent, making them ideal for a range of standard imaging procedures like CT scans and X-rays. Their simplicity and ease of use make them a preferred choice in hospitals and imaging centers, particularly in regions with budget constraints or lower imaging volumes. Single-head injectors also have lower maintenance costs compared to dual-head injectors, further enhancing their appeal. According to the contrast media injectors market forecast, the demand for single-head injectors is expected to remain strong, driven by ongoing advancements in technology and the need for reliable, straightforward solutions in medical imaging.

Breakup by Application:

- Radiology

- Interventional Cardiology

- Interventional Radiology

Radiology represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the application. This includes radiology, interventional cardiology, and interventional radiology. According to the report, the radiology segment accounted for the largest market share.

Radiology represents the leading segment in the contrast media injectors market due to its central role in diagnostic imaging. The growing prevalence of chronic diseases such as cancer, cardiovascular conditions, and neurological disorders has increased the need for accurate diagnostic tools, making radiology essential in healthcare. According to the report published by WHO, cardiovascular diseases claim 10,000 lives daily in European Region, with men more affected than women. The report reveals that over 42.5% of annual deaths are due to CVDs. Radiology departments utilize contrast media injectors extensively for procedures like CT, MRI, and X-ray, which require precise contrast agent administration to enhance image quality. According to the contrast media injectors market overview, the rising number of diagnostic imaging procedures, driven by the high incidence of chronic diseases, has significantly boosted the adoption of contrast media injectors in radiology departments worldwide. Advancements in radiology imaging techniques and the integration of advanced injector systems have further driven demand. Consequently, radiology remains the dominant segment, accounting for the highest usage and revenue generation in the market.

Breakup by End User:

- Hospitals

- Ambulatory Surgery Centers

- Diagnostics Imaging Centers

Hospitals represents the largest market share

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes hospitals, ambulatory surgery centers, and diagnostics imaging centers. According to the report, the hospitals segment accounted for the largest market share.

Hospitals exhibit clear dominance in the contrast media injectors market due to their high patient volumes and extensive range of diagnostic imaging procedures. As primary healthcare providers, hospitals frequently perform CT scans, MRIs, and X-rays, which require the use of contrast media injectors to enhance image clarity and accuracy. The need for reliable, high-performance injectors in these settings drives continuous demand. Additionally, hospitals have greater budgets and resources to invest in advanced injector technologies, including automated systems that improve efficiency and patient safety. This dominance is further reinforced by the growing prevalence of chronic diseases, increasing the demand for diagnostic imaging services.

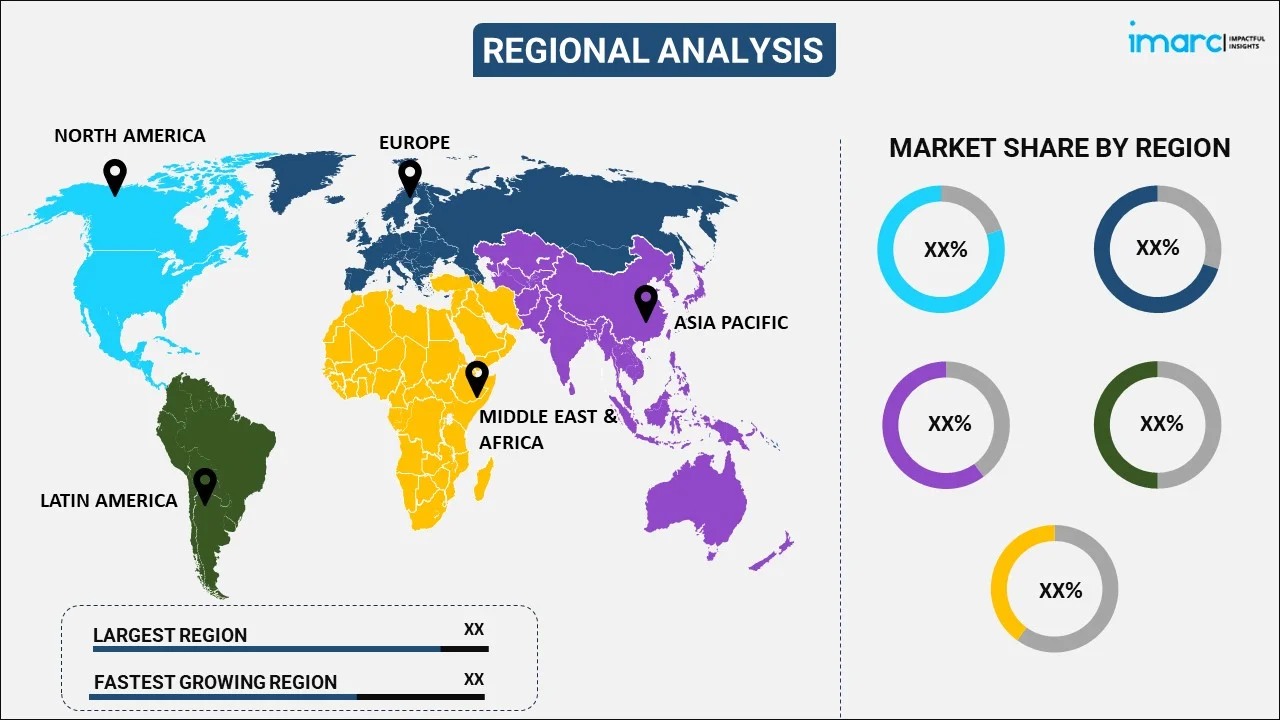

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest contrast media injectors market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America represents the largest regional market for contrast media injectors.

North America leads the contrast media injectors market, accounting for the largest market share due to several factors, including advanced healthcare infrastructure and a high prevalence of chronic diseases requiring diagnostic imaging. The region’s strong emphasis on early disease detection and preventive healthcare has led to the widespread adoption of imaging procedures like CT scans, MRIs, and X-rays, driving demand for contrast media injectors. Additionally, North America benefits from substantial investments in healthcare technology, encouraging the development and uptake of advanced injector systems. For instance, in July 2024, San Mateo County Health announced its partnership with Innovaccer to implement its healthcare AI platform, with a focus on enhancing patient care services. The platform aims to modernize technology infrastructure by aggregating patient data from multiple sources, enabling the creation of unified patient records. This integrated approach empowers providers to make more informed decisions that improve population health management and clinical outcomes, ultimately striving to promote longer and healthier lives for everyone in San Mateo County, California. Favorable reimbursement policies and the presence of key market players also contribute to North America’s leading position in the market.

Competitive Landscape:

- The market research report has also provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the major market players in the contrast media injectors industry include APOLLO RT Co. Ltd., Bayer AG, Bracco Imaging S.p.A., General Electric Company, Guerbet, Medtron AG, Nemoto Kyorindo Co. Ltd., Shenzhen Anke High-tech Co. Ltd., Shenzhen Seacrown Electromechanical Co. Ltd., Sino Medical-Device Technology Co. Ltd. and ulrich GmbH & Co. KG.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

- The Contrast Media Injectors market is highly competitive, characterized by the presence of several key players, including Bayer HealthCare, Bracco Imaging, Guerbet Group, and GE Healthcare. Contrast media injectors manufacturers focus on innovation, developing advanced injector systems that integrate features like automated injection protocols and improved safety mechanisms to enhance user experience and patient outcomes. The market also sees competition in pricing strategies, technological advancements, and expanding geographical presence. Smaller players and new entrants aim to capture market share through cost-effective solutions and niche market focus. Strategic partnerships, mergers, and acquisitions are common as companies seek to strengthen their market positions and expand their product portfolios.

Contrast Media Injectors Market News:

- In May 2023, MEDTRON AG launched a custom-made adapter for Guerbet's Elucirem™ contrast media, offering enhanced compatibility for MEDTRON's Accutron® MR contrast media injector. The new adapter responds to the growing demand for a solution tailored to the pre-filled Elucirem™ syringe.

- In January 2023, Bayer's Ultravist™-300 and Ultravist™-370 announced that they have received approval in the EU for contrast-enhanced mammography (CEM), providing an alternative imaging option for diagnosing breast cancer. CEM combines digital mammography with a contrast agent, creating a sensitive and cost-effective examination method. This approval expands Bayer's radiology portfolio, assisting healthcare professionals in delivering precise diagnostics for patients.

Contrast Media Injectors Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Injectors Types Covered | Single-Head Injectors, Dual-Head Injectors, Syringeless Injectors |

| Applications Covered | Radiology, Interventional Cardiology, Interventional Radiology |

| End Users Covered | Hospitals, Ambulatory Surgery Centers, Diagnostics Imaging Centers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | APOLLO RT Co. Ltd., Bayer AG, Bracco Imaging S.p.A., General Electric Company, Guerbet, Medtron AG, Nemoto Kyorindo Co. Ltd., Shenzhen Anke High-tech Co. Ltd., Shenzhen Seacrown Electromechanical Co. Ltd., Sino Medical-Device Technology Co. Ltd., ulrich GmbH & Co. KG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the contrast media injectors market from 2019-2033.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global contrast media injectors market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the contrast media injectors industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global contrast media injectors market was valued at USD 1.8 Billion in 2024.

We expect the global contrast media injectors market to exhibit a CAGR of 4.82% during 2025-2033.

The sudden outbreak of the COVID-19 pandemic had led to postponement of elective medical imaging procedures to reduce the risk of coronavirus infection upon hospital visits and interaction with medical equipment, thereby negatively impacting the global market for contrast media injectors.

The growing adoption of automated contrast media injectors in cardiac imaging, which enhances patient safety and improves image quality, is primarily driving the global contrast media injectors market.

Based on the product type, the global contrast media injectors market has been divided into consumables and injector systems, where consumables currently exhibit a clear dominance in the market.

Based on the injectors type, the global contrast media injectors market can be categorized into single-head injectors, dual-head injectors, and syringeless injectors. Currently, single-head injectors hold the majority of the total market share.

Based on the application, the global contrast media injectors market has been segmented into radiology, interventional cardiology, and interventional radiology. Among these, radiology currently accounts for the largest market share.

Based on the end user, the global contrast media injectors market can be bifurcated into hospitals, ambulatory surgery centers, and diagnostics imaging centers. Currently, hospitals hold the majority of the global market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global contrast media injectors market include APOLLO RT Co. Ltd., Bayer AG, Bracco Imaging S.p.A., General Electric Company, Guerbet, Medtron AG, Nemoto Kyorindo Co. Ltd., Shenzhen Anke High-tech Co. Ltd., Shenzhen Seacrown Electromechanical Co. Ltd., Sino Medical-Device Technology Co. Ltd., and ulrich GmbH & Co. KG.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)