Containerized Data Center Market Size, Share, Trends and Forecast by Type of Container, Organization Size, Application, End Use Industry, and Region, 2026-2034

Global Containerized Data Center Market Size, Share, Trends & Forecast (2026-2034)

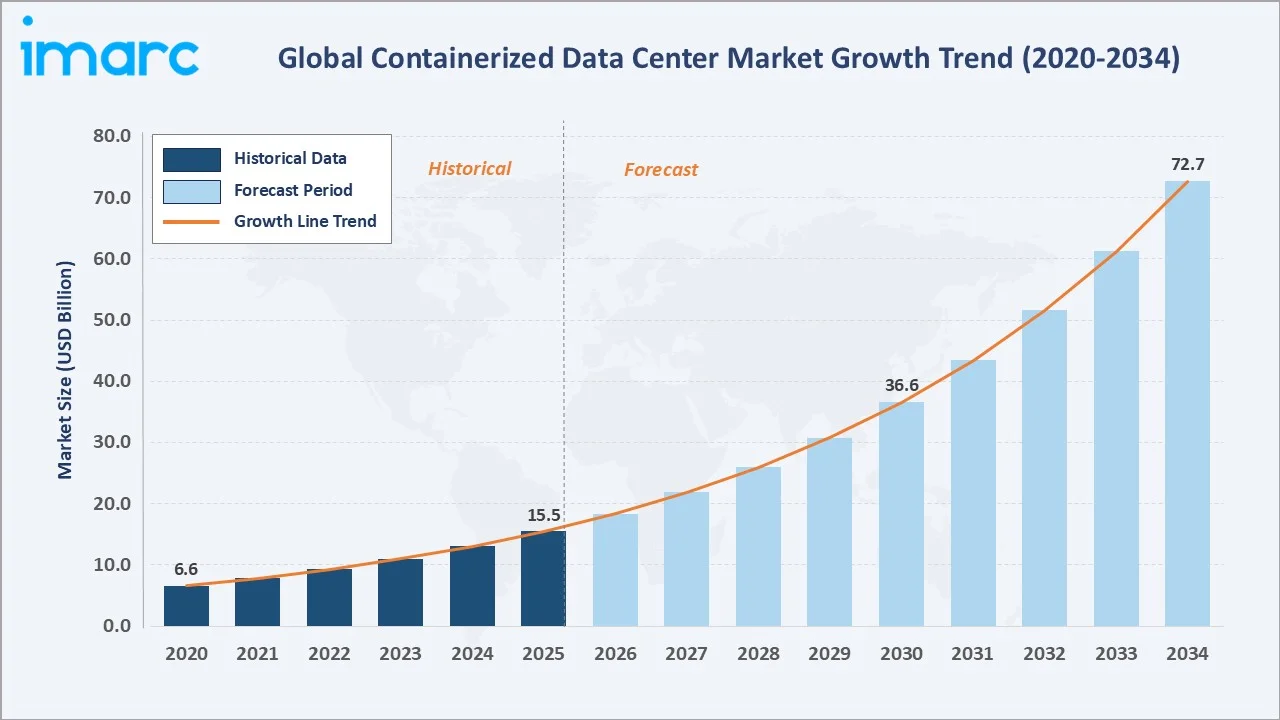

The global containerized data center market size reached USD 15.5 Billion in 2025 and is projected to reach USD 72.7 Billion by 2034, exhibiting a CAGR of 18.71% during 2026-2034. Rapid deployment capabilities, AI infrastructure demand, edge computing integration, and energy efficiency imperatives are the primary forces driving market growth.

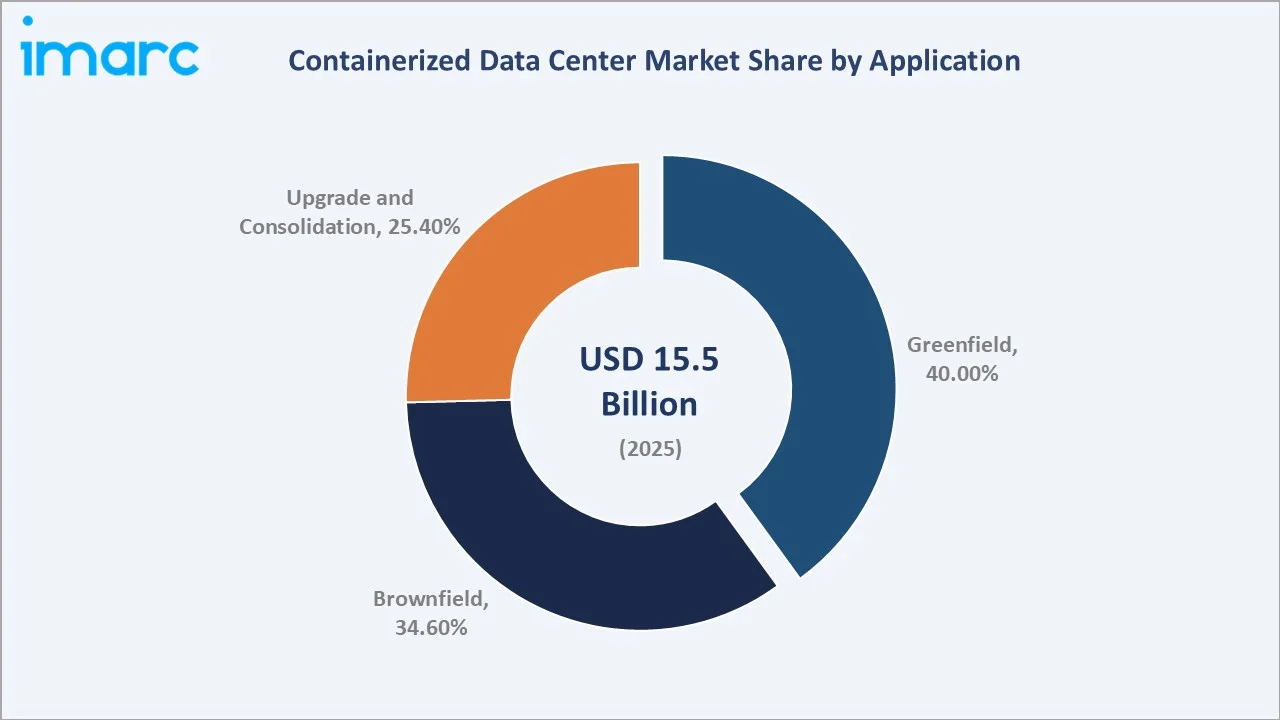

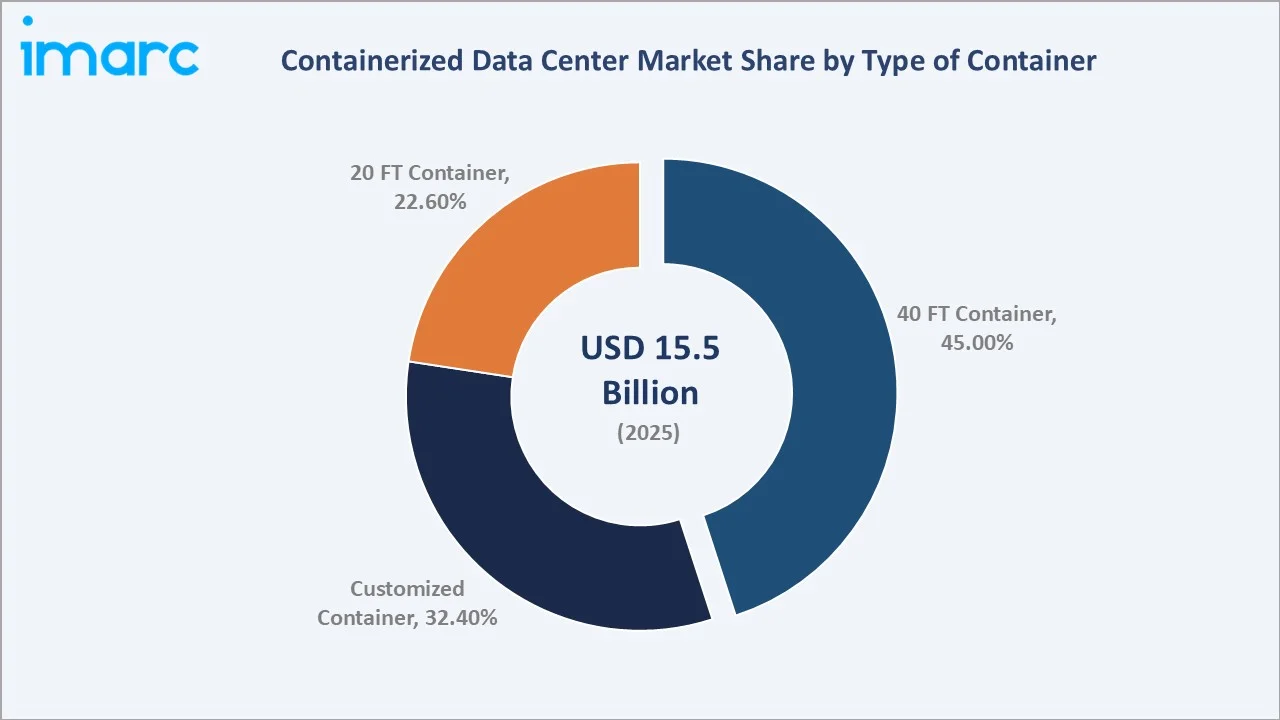

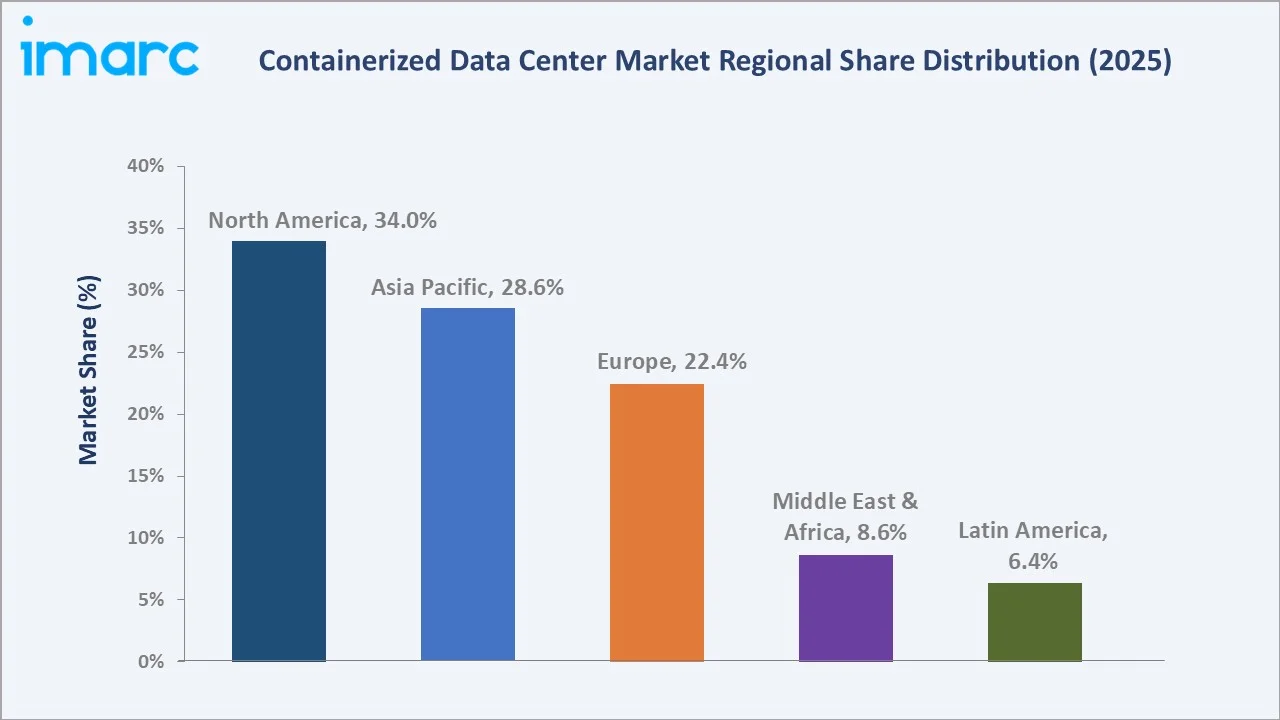

Greenfield deployment dominates the application mix at 40.0% in 2025, while 40 FT Container leads the container type segment at 45.0%. North America commands a dominant 34.0% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.5 Billion |

|

Forecast Market Size (2034) |

USD 72.7 Billion |

|

CAGR (2026-2034) |

18.71% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (34.0% share, 2025) |

|

Second Region |

Asia Pacific (28.6% share, 2025) |

|

Leading Application |

Greenfield (40.0%, 2025) |

|

Leading Container Type |

40 FT Container (45.0%, 2025) |

The global containerized data center market growth trajectory from 2020 through 2034, with historical expansion to USD 15.5 Billion in 2025, reflects consistent digitalization-driven demand. The forecast to USD 72.7 Billion captures accelerating AI workload adoption, cloud infrastructure investment, and emerging market digitalization.

To get more information on this market, Request Sample

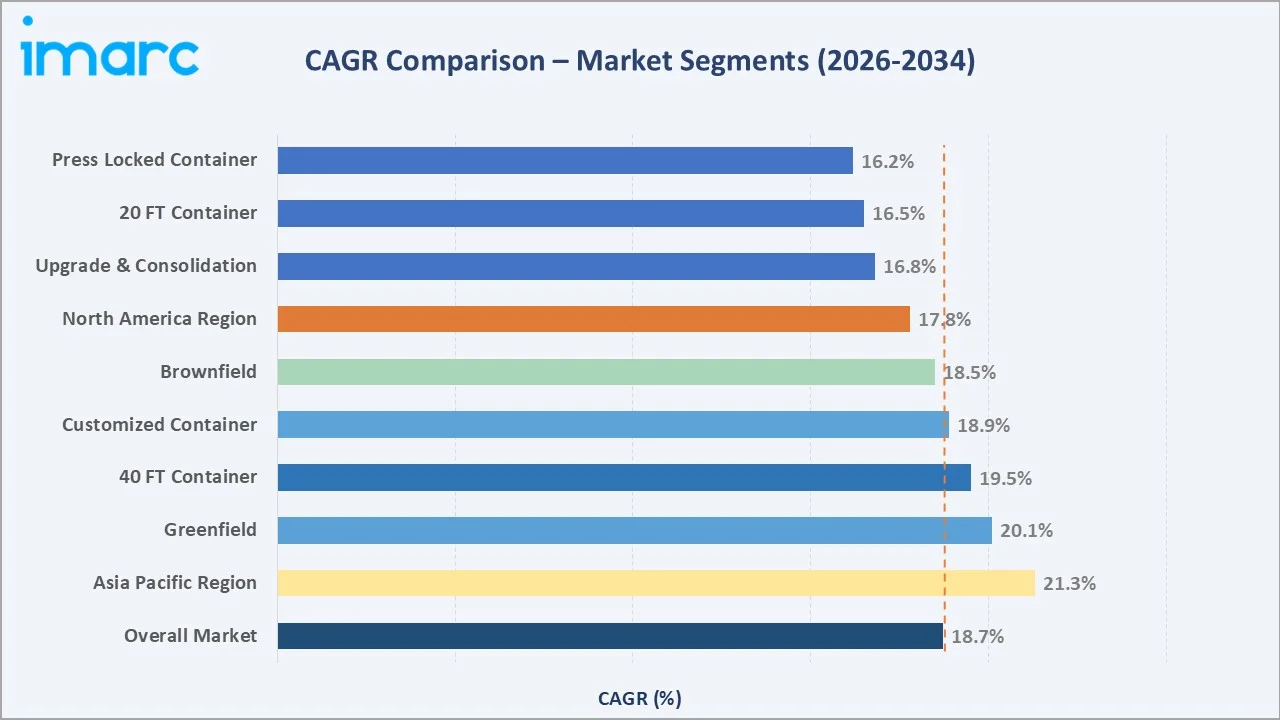

The CAGR trajectories across key application, container type, and regional sub-segments highlight Asia Pacific and Greenfield deployments as the fastest-growing categories within the global containerized data center industry analysis through 2034.

Executive Summary

The global containerized data center market is on an accelerated growth trajectory from USD 15.5 Billion in 2025 to USD 72.7 Billion by 2034. Containerized data centers, portable and modular IT infrastructure units pre-installed inside shipping containers, serve as rapid-deployment computing facilities supporting AI, cloud, and edge applications.

Greenfield deployment dominates application at 40.0% in 2025, enabling purpose-built, optimized digital infrastructure on new sites. Brownfield deployments (34.6%) address capacity augmentation for existing facilities, while Upgrade and Consolidation (25.4%) reflect enterprise technology refresh cycles. The 40 FT Container leads container type at 45.0%, providing superior rack density and compute capacity for hyperscale and enterprise use cases.

North America (34.0%) leads regionally, reflecting cloud computing maturity, AI infrastructure investment, and hyperscaler capex. Asia Pacific (28.6%) and Europe (22.4%) follow, driven by digital transformation investment and data sovereignty requirements respectively.

Key Market Insights

|

Insight |

Data |

|

Largest Application Segment |

Greenfield – 40.0% share (2025) |

|

Leading Container Type |

40 FT Container – 45.0% share (2025) |

|

Leading Region |

North America – 34.0% revenue share (2025) |

|

Second Region |

Asia Pacific – 28.6% revenue share (2025) |

|

Top Companies |

HPE, Dell Technologies, Cisco, Schneider Electric, Vertiv, Huawei, Delta Electronics |

Key analytical observations expanding on the above data:

- Greenfield deployment at 40.0% in 2025 dominates because purpose-built containerized sites eliminate legacy infrastructure constraints. New hyperscale sites, government digital hubs, and telecom edge nodes can be deployed in weeks rather than the 18-24 months required for traditional data center construction.

- The 40 FT Container leads at 45.0% in 2025 due to its superior compute-per-dollar economics. With double the floor space of 20 FT units, 40 FT containers support higher rack density, 400-800 kW power capacity per container, and integrated cooling systems that reduce infrastructure overhead for medium-to-large deployments.

- North America's 34.0% dominance reflects the combined effect of hyperscaler capex (Microsoft, AWS, Google collectively investing over USD 200 Billion annually in infrastructure), federal AI initiatives, and the Inflation Reduction Act's data center incentives driving rapid modular deployment.

- Asia Pacific, with 28.6% in 2025, is the highest-growth region reflecting China's national digital infrastructure program, India's data localization requirements driving domestic deployment, and Southeast Asia's rapid cloud adoption generating demand for rapid, cost-effective modular deployments.

Global Containerized Data Center Market Overview

A containerized data center is a modular, portable IT infrastructure solution pre-configured inside standard intermodal shipping containers of 20 FT or 40 FT dimensions or custom-engineered enclosures. Each unit integrates servers, storage systems, networking equipment, power distribution, uninterruptible power supplies, cooling systems, and physical security within a self-contained, factory-tested environment.

The global ecosystem integrates component manufacturers, system integrators, containerization specialists, logistics and deployment service providers, managed operations teams, and diverse end-use industries spanning BFSI, IT and telecommunications, government, healthcare, defense, education, and entertainment and media sectors.

Market Dynamics

To evaluate market opportunities, Request Sample

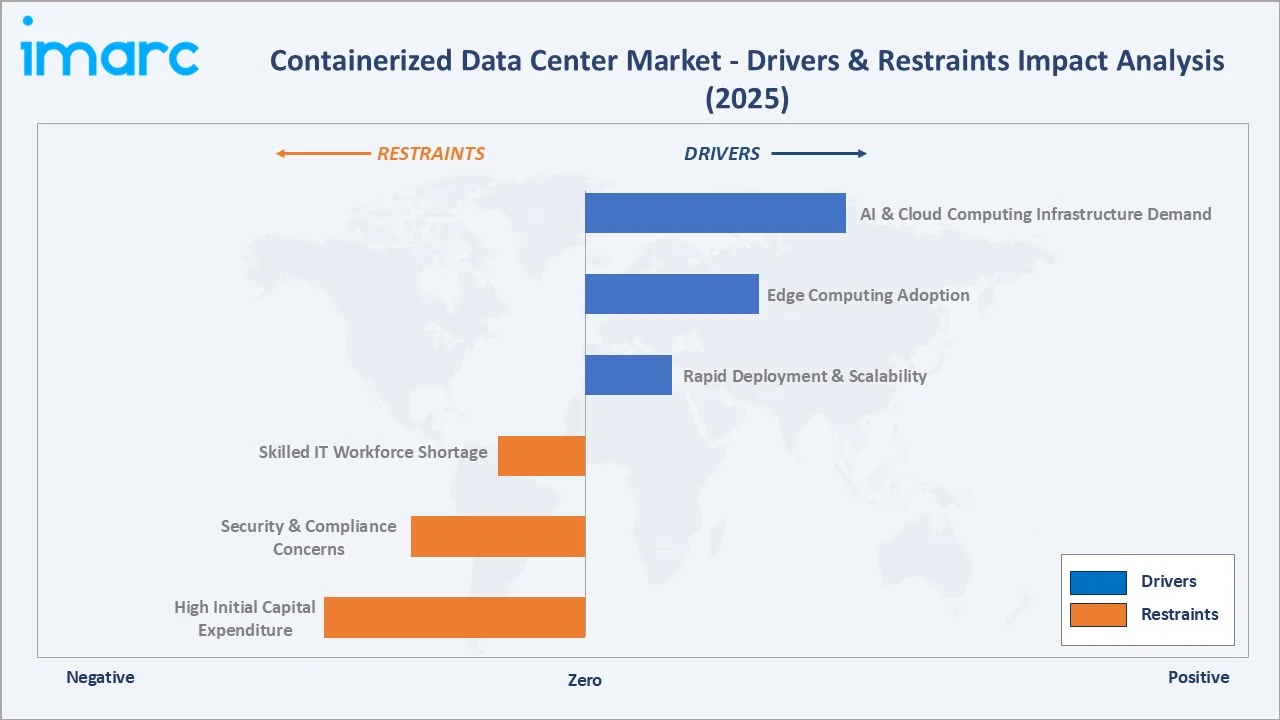

Market Drivers

- AI and High-Performance Computing Infrastructure Demand: The Stargate Project, a joint venture involving OpenAI, SoftBank, and Oracle, announced USD 500 Billion in AI infrastructure investment through 2029. Each AI training cluster deployment generates demand for GPU-optimized containerized units with advanced liquid cooling and high-density power.

- Edge Computing and 5G Network Expansion: Omdia predicts 5.9 billion cellular IoT connections by 2035, thereby driving telecom operators to deploy micro data centers at cell tower base stations.

- Rapid Deployment and Capital Efficiency: Containerized data centers reduce time-to-operation from 18-24 months for traditional builds to 8-12 weeks, with factory-integrated testing eliminating on-site commissioning complexity. This capital efficiency and speed advantage is critical for organizations scaling digital capacity under competitive pressure.

Market Restraints

- High Initial Capital Expenditure: Enterprise-grade containerized data center systems require upfront investment depending on power density, cooling configuration, and IT equipment integration. This capital threshold creates adoption barriers for small and mid-market organizations without established IT investment cycles.

- Security and Compliance Complexity: Containerized deployments in public or semi-public locations face heightened physical security requirements, and multi-jurisdictional deployments create complex data sovereignty compliance scenarios under GDPR, India's PDPB, China's PIPL, and sector-specific frameworks like HIPAA and PCI-DSS.

Market Opportunities

- Emerging Market Digitalization: According to the latest GSMA‘State of Mobile Internet Connectivity 2024’ report, 160 million people started using mobile internet last year, similar to 2022 levels but a drop from 2015-2021 when more than 200 million new users were added each year. Containerized data centers provide cost-effective, rapid-deployment solutions for markets where traditional construction is impractical or uneconomical.

- Sustainable and Green Data Center Designs: Vendors integrating 800V HVDC power architectures, liquid cooling achieving PUE below 1.1, and renewable energy microgrid components (hydrogen fuel cells, solar panels, battery storage) are accessing a rapidly growing sustainability-driven procurement category commanding 15-25% price premiums.

Market Challenges

- Skilled IT Operations Workforce Shortage: The global shortage of data center operations specialists, estimated at 300,000+ by the Uptime Institute, creates deployment and management bottlenecks for distributed containerized deployments, particularly in remote and emerging market locations.

- Standardization and Interoperability Limitations: The absence of universal standards for containerized data center physical configurations, power interfaces, and management software APIs creates integration complexity for enterprises managing multi-vendor containerized deployments across hybrid and multi-cloud environments.

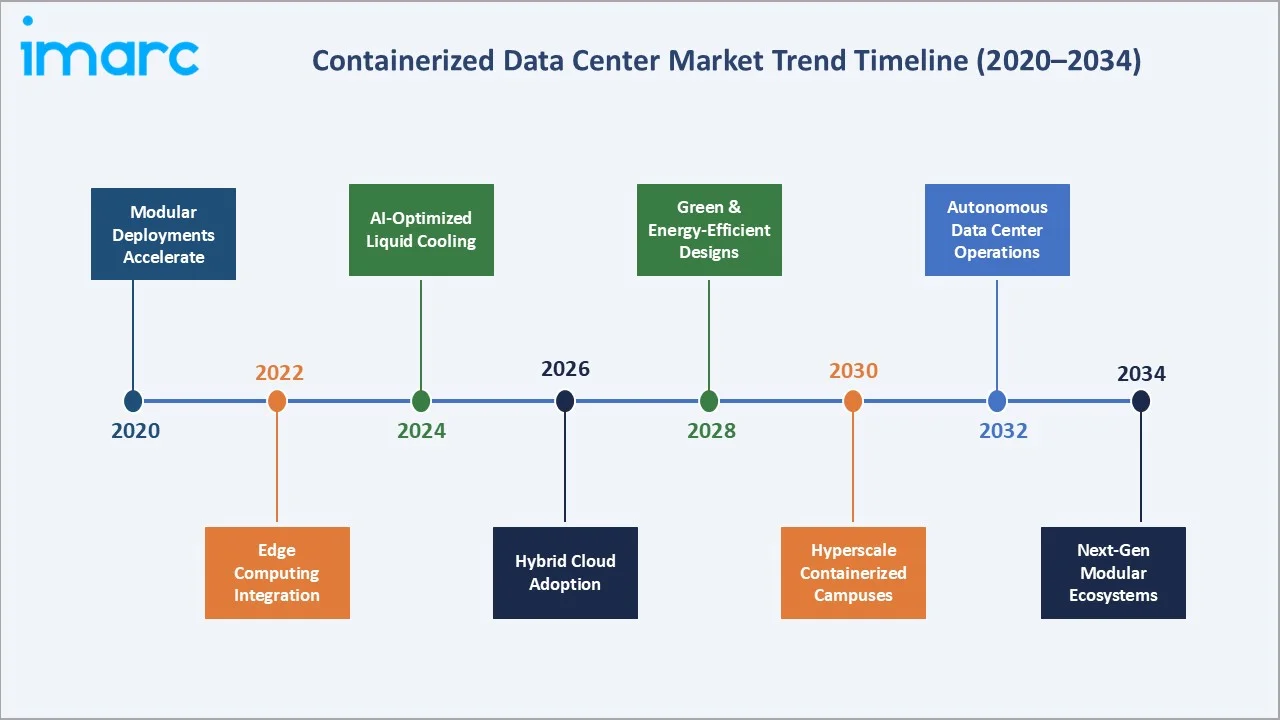

Emerging Market Trends

1. AI-Optimized Liquid Cooling Transforming Container Design

Direct-to-chip and immersion cooling technologies are enabling GPU cluster densities of 100-200 kW per rack within containerized systems. Liquid systems capture up to 90% of waste heat for reuse, reducing total cooling energy consumption by 40-60% versus traditional air-cooled configurations, making high-density AI deployments economically viable.

2. Hybrid Cloud and Containerized Edge Integration

Enterprise hybrid cloud architectures increasingly incorporate containerized on-premises units as consistent extensions of cloud environments. Kubernetes-orchestrated containerized data centers enable seamless workload portability across on-premises, edge, and public cloud, driving adoption across financial services and healthcare sectors requiring data locality.

3. Prefabricated Modular Campus Architecture

Hyperscalers and co-location providers are deploying containerized campuses of 50-200+ units, creating scalable, incremental capacity expansion models that reduce stranded capital risk. Campus architectures with shared power and cooling distribution achieve cost structures approaching traditional built facilities while maintaining deployment speed advantages.

4. Renewable Energy Microgrid Integration

Next-generation containerized systems integrate renewable energy microgrids combining solar panels, battery storage, hydrogen fuel cells, and advanced power management. Delta Electronics' 2025 launch of an 800V HVDC containerized AI data center exemplifies the convergence of energy technology and IT infrastructure in single-containerized deployments.

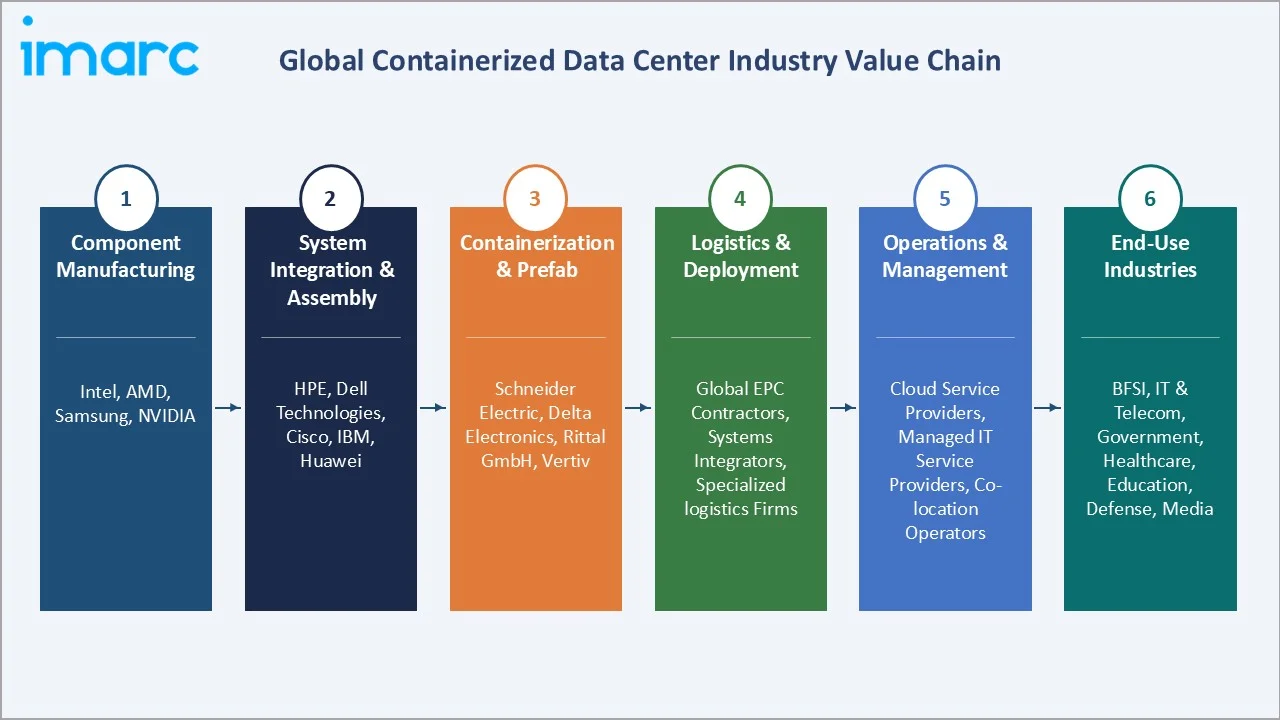

Industry Value Chain Analysis

The containerized data center value chain spans six stages from component manufacturing through end-use industry deployment. System integration and containerization capture the highest value-add margins, while logistics, rapid deployment capabilities, and managed operations services generate recurring revenue streams.

|

Stage |

Key Players / Examples |

|

Component Manufacturing |

Intel, AMD, Samsung, NVIDIA |

|

System Integration & Assembly |

HPE, Dell Technologies, Cisco, Huawei |

|

Containerization & Prefabrication |

Schneider Electric, Delta Electronics, Rittal GmbH, Vertiv |

|

Logistics & Deployment |

Global EPC contractors, systems integrators, specialized logistics firms |

|

Operations & Management |

Cloud service providers, managed IT service providers, co-location operators |

|

End-Use Industries |

BFSI, IT & Telecom, Government, Healthcare, Education, Defense, Media |

Integrated vendors combining hardware manufacturing, containerization, logistics, and managed services capture disproportionate margin across the value chain. HPE, Dell, and Schneider Electric's full-stack containerized offerings achieve higher customer lifetime value than point-solution providers, enabling premium pricing and sticky service relationships.

Technology Landscape in the Containerized Data Center Industry

Power Architecture: HVDC and Intelligent Power Distribution

High-voltage direct current (HVDC) at 800V is emerging as the standard for high-density containerized AI data centers, reducing power conversion losses by 30-40% versus legacy 208V AC systems. Intelligent power distribution units (iPDUs) with per-outlet metering enable granular power usage optimization and automated load balancing across GPU clusters.

Cooling Technology: Liquid Cooling and Immersion Systems

Air-cooled designs remain standard for general-purpose deployments (up to 20 kW/rack), while direct-to-chip liquid cooling (20-100 kW/rack) and single-phase immersion cooling (100+ kW/rack) enable GPU cluster deployments previously impossible in containerized formats. Closed-loop liquid cooling eliminates water evaporation and enables indoor deployment without evaporative cooling towers.

Software-Defined Infrastructure and AI Operations

DCIM (Data Center Infrastructure Management) platforms integrating AI-driven predictive maintenance, automated cooling optimization, and digital twin capabilities are standard in premium containerized products. API-first management architectures enable integration with enterprise ITSM and cloud management platforms, enabling unified operations across distributed containerized deployments.

Market Segmentation Analysis

By Application

Greenfield deployment commands a 40.0% majority share in 2025, reflecting the strong preference for purpose-built containerized infrastructure that avoids legacy system constraints. New enterprise campuses, government digital hubs, telecom edge nodes, and industrial IoT facilities increasingly specify containerized solutions for their speed-to-operational and capital efficiency advantages.

To access detailed market analysis, Request Sample

Brownfield deployment at 34.6% in 2025 addresses the large installed base of organizations needing to augment existing data center capacity without major construction. Containerized add-ons to existing facilities provide incremental capacity at 30-50% lower cost per kW than traditional buildout. Upgrade and Consolidation (25.4%) reflects enterprise technology refresh programs and data center consolidation mandates reducing facilities from multiple aging sites into modern containerized infrastructure.

By Type of Container

The 40 FT Container dominates the container type segment at 45.0% in 2025, offering the superior computing capacity, rack density, and integrated systems architecture required by enterprise and hyperscale customers. A standard 40 FT container accommodates 8-24 equipment racks with 400-800 kW total IT load capacity, enabling meaningful compute deployments without requiring multiple containerized units.

Customized Container at 32.4% in 2025 addresses specialized requirements including military-grade hardening, extreme temperature operation, offshore deployment, or non-standard power configurations. Customized containers command 40-80% price premiums over standard configurations, generating revenue share disproportionate to unit volume. The 20 FT Container (22.6%) serves edge computing, remote site, and rapid-response deployments where portability and ease of single-truck transport are primary requirements.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.0% |

AI infrastructure investment; cloud expansion; tech company capex |

|

Asia Pacific |

28.6% |

Digital transformation; emerging market adoption; 5G rollout |

|

Europe |

22.4% |

Green data center mandates; edge computing growth; EU digital agenda |

|

Middle East & Africa |

8.6% |

Vision 2030 digitalization; smart city infrastructure; rapid deployment needs |

|

Latin America |

6.4% |

Cloud infrastructure buildout; remote deployment needs; cost-effective IT scaling |

North America's 34.0% market dominance in 2025 is driven by the most advanced hyperscaler investment cycle and AI infrastructure buildout globally. Microsoft, Amazon, Google, and Meta are collectively deploying tens of billions of dollars annually in modular and containerized capacity expansion to support AI training and inference workloads.

Asia Pacific, with 28.6% in 2025, is experiencing the fastest growth trajectory. China's national digital infrastructure policy, India's data localization mandates driving domestic investment, and Southeast Asia's digital economy expansion collectively create demand for hundreds of containerized deployments annually. Europe's 22.4% share reflects the EU Digital Decade targets and Green Deal sustainability requirements accelerating adoption of energy-efficient modular infrastructure.

Competitive Landscape

The global containerized data center market is moderately fragmented, with established IT infrastructure leaders holding strong positions globally while specialized vendors compete on niche capabilities. North America and Europe are served by full-stack technology giants, while Asia Pacific features both global players and strong domestic manufacturers like Huawei.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Hewlett Packard Enterprise (HPE) |

HPE Mod Pods/HPE AI Mod Pods, Modular Data Center Systems |

Leader |

Global; cloud-ready modular; AI infrastructure |

|

Dell Technologies Inc. |

Dell Modular Data Center (MDC) and PowerEdge-based containerized solutions, Integrated Rack Solutions |

Leader |

Global; enterprise hybrid cloud; AI workloads |

|

Cisco Systems Inc. |

Network Solutions, Cisco AI PODs, Cisco UCS X-Series Modular System |

Established |

Global; networking-centric; hyperscale edge |

|

Schneider Electric SE |

EcoStruxure Micro Data Center |

Leader |

Global; energy efficiency; green data centers |

|

Vertiv Group Corp. |

SmartAisle |

Challenger |

Global; critical IT infrastructure; co-location |

|

Huawei Technologies Co., Ltd. |

FusionModule, iCooling systems |

Leader |

APAC & Global; AI-integrated; smart cooling |

|

Delta Electronics, Inc. |

20 FT AI Containerized Data Center |

Challenger |

Global; HVDC power; green modular deployment |

|

Rittal GmbH & Co. KG |

RiMatrix |

Challenger |

Europe & Global; precision cooling; industrial IT |

|

Fsas Technologies Inc. (Fujitsu Limited) |

Primergy, Cloud-ready systems |

Emerging |

APAC; AI servers; sustainable data centers |

The competitive positioning of key global containerized data center market participants across global market presence and strategic investment dimensions in 2025. Key players include Hewlett Packard Enterprise (HPE), Dell Technologies Inc., Cisco Systems Inc., Schneider Electric SE, Vertiv Group Corp., Huawei Technologies Co., Ltd., Delta Electronics, Inc., Rittal GmbH & Co. KG, and Fsas Technologies Inc. (Fujitsu Limited).

Key Company Profiles

Hewlett Packard Enterprise (HPE)

Hewlett Packard Enterprise is the world's leading provider of enterprise IT infrastructure, networking, and hybrid cloud solutions. HPE's containerized data center portfolio encompasses the Modular Data Center product lines, delivering pre-integrated compute, storage, power, and cooling systems optimized for rapid deployment in enterprise and edge environments.

- Product Portfolio: HPE AI Mod POD, HPE Modular Data Center Series, GreenLake edge-to-cloud platform integration

- Recent Developments: In 2025, HPE expanded its liquid-cooled containerized AI infrastructure portfolio with NVIDIA GPU-optimized configurations, supporting deployments for Tier 1 telecommunications and financial services customers.

- Strategic Focus: HPE's containerized strategy leverages its GreenLake consumption model to offer containerized data center capacity as a managed service, reducing upfront capex barriers and creating recurring revenue relationships with enterprise customers scaling AI and hybrid cloud infrastructure.

Dell Technologies Inc.

Dell Technologies is a global technology leader offering end-to-end infrastructure solutions spanning servers, storage, networking, and containerized data center systems. Dell's containerized portfolio integrates PowerEdge servers, PowerStore storage, and Networking into factory-configured, deployment-ready modular units.

- Product Portfolio: Dell DCS Modular Data Center System, Dell Integrated System for Microsoft Azure Stack HCI, PowerEdge-based containerized configurations

- Recent Developments: In November 2025, Dell Technologies announced a strategic partnership with a leading cloud service provider to develop integrated containerized solutions enhancing hybrid cloud capabilities.

- Strategic Focus: Dell's strategy focuses on enterprise hybrid cloud integration, providing containerized units that serve as consistent on-premises extensions of AWS, Azure, and Google Cloud environments, enabling unified management through VMware and Kubernetes orchestration.

Schneider Electric SE

Schneider Electric is the global leader in energy management and automation, operating as the dominant force in power distribution and cooling solutions for containerized data centers. Schneider's EcoStruxure Micro Data Center product line defines the market standard for prefabricated, energy-optimized containerized deployments.

- Product Portfolio: EcoStruxure Micro Data Center, Prefabricated Modular IT Pod, EcoStruxure Pod Data Center, Modular Data Center All-in-One Essential, and Power Module

- Recent Developments: In June 2025, Schneider Electric launched a new line of eco-friendly containerized data centers engineered to minimize energy consumption, aligning with global sustainability mandates and achieving PUE below 1.15.

- Strategic Focus: Schneider's containerized strategy differentiates on industry-leading energy efficiency, certified sustainability credentials, and EcoStruxure digital management platform integration, targeting enterprise and hyperscale customers with strong ESG commitments requiring measurable carbon footprint reduction.

Huawei Technologies Co., Ltd.

Huawei is Asia Pacific's leading technology infrastructure company, providing comprehensive containerized data center solutions through its FusionModule product family. Huawei's iCooling AI-powered cooling optimization and prefabricated module architecture define the standard for high-density containerized deployments in China and emerging markets globally.

- Product Portfolio: FusionModule2000 Containerized Data Center, iCooling Energy Optimization, iPower intelligent power systems

- Recent Developments: Huawei expanded FusionModule AI-optimized containerized deployments across Southeast Asia and Middle East markets, targeting government digital infrastructure programs and enterprise digital transformation projects.

- Strategic Focus: Huawei's containerized strategy focuses on full-stack AI integration from chip to container management, targeting Asian government and enterprise customers with deployments emphasizing domestic technology supply chains, digital sovereignty, and AI-ready infrastructure at competitive total cost of ownership.

Market Concentration Analysis

The global containerized data center market is moderately fragmented at the global level, with the top five vendors holding an estimated 50-60% of total market revenue. Unlike the steel grating market, containerized data center concentration is driven by technology capability rather than geography, with HPE, Dell, Cisco, and Schneider Electric competing across all major regions.

Consolidation is occurring through established IT infrastructure conglomerates acquiring specialized containerized data center vendors and integrating their capabilities into broader digital infrastructure platforms. Schneider Electric's acquisition of several edge infrastructure specialists and HPE's GreenLake service integration exemplify this consolidation pattern.

Investment & Growth Opportunities

Fastest-Growing Segments

AI-optimized containerized data centers with liquid cooling at approximately 25-30% CAGR through 2034 represent the highest-growth product segment. These high-density GPU cluster deployments command 3-5x the ASP of standard containerized configurations, generating revenue concentration disproportionate to unit volume. Edge containerized deployments for 5G and industrial IoT at approximately 22% CAGR through 2034 represent the broadest-based growth opportunity.

Emerging Markets

Middle East and Africa, with 8.6% share and an accelerating CAGR, represent the fastest-growing region for containerized data centers through 2034. Saudi Arabia's Vision 2030 digital infrastructure investment, UAE smart city projects, and African mobile-first digital economy expansion are creating large-scale deployments in markets with limited traditional data center supply.

Venture & Investment Trends

Private equity and venture investment in containerized data center platform companies is growing, driven by recurring revenue models from managed containerized deployments and the capital-efficient scaling characteristics of prefabricated infrastructure. Sustainability-certified containerized deployments are accessing green bond financing at preferential rates, improving project economics for large-scale sustainable deployments.

Future Market Outlook (2026-2034)

The global containerized data center market is forecast to expand from USD 15.5 Billion in 2025 to USD 72.7 Billion by 2034 at a CAGR of 18.71%, adding USD 57.2 Billion in incremental annual market value over the forecast period. This accelerated, sustained growth reflects the market's technology-led, infrastructure-essential demand characteristics.

Three technological forces will most significantly shape the containerized data center industry through 2034. AI compute infrastructure, with leading technology companies committing trillions in aggregate investment through 2030, will generate specialized high-density containerized deployments at unprecedented scale. Autonomous data center operations, using AI to manage power, cooling, and workload distribution, will reduce operational costs and expand addressable use cases.

Research Methodology

Primary Research

Primary research encompassed structured interviews with containerized data center industry stakeholders including senior technology executives, EPC procurement specialists, data center operators, cloud service provider infrastructure teams, and enterprise IT decision-makers. Primary data validated market sizing, application and container type segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Uptime Institute Data Center Industry Survey (2024), IEA Data Centres and Data Transmission Networks report, Gartner Data Center infrastructure forecasts, IDC Cloud and Edge Computing market reports, GWEC Global Wind Report, company annual reports, investor presentations, and trade publications including Data Center Dynamics, Data Center Knowledge, and DCD Magazine.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating digital infrastructure investment data, cloud adoption indices, AI compute demand trajectories, and historical market evolution patterns. Scenario analysis incorporating base, optimistic, and conservative cases accounts for macroeconomic and technology adoption uncertainty.

Containerized Data Center Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Type of Containers Covered | 20 FT Container, 40 FT Container, Customized Container |

| Organization Sizes Covered | Small Organization, Midsize Organization, Large Organization |

| Applications Covered | Greenfield, Brownfield, Upgrade and Consolidation |

| End Use Industries Covered | BFSI, IT and Telecommunications, Government, Education, Healthcare, Defense, Entertainment and Media, Others |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Hewlett Packard Enterprise (HPE), Dell Technologies Inc., Cisco Systems Inc., Schneider Electric SE, Vertiv Group Corp., Huawei Technologies Co., Ltd., Delta Electronics, Inc., Rittal GmbH & Co. KG, Fsas Technologies Inc. (Fujitsu Limited), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the containerized data center market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global containerized data center market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the containerized data center industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Containerized Data Center Market Report

The global containerized data center market reached USD 15.5 Billion in 2025, driven by accelerating adoption of modular IT infrastructure, edge computing, and AI-driven data processing demands across industries.

The market is projected to reach USD 72.7 Billion by 2034, growing at a CAGR of 18.71% during 2026-2034, driven by cloud expansion, AI workload deployments, and rapid digitalization in emerging markets.

Greenfield deployments lead with a 40.0% application share in 2025, valued for enabling purpose-built, energy-efficient containerized infrastructure on new sites without legacy constraints.

The 40 FT Container leads at 45.0% in 2025, offering greater computing capacity per unit, superior scalability, and optimal rack density for medium-to-large enterprise and hyperscale deployments.

North America commands 34.0% market share in 2025, driven by large-scale cloud investments, AI infrastructure buildouts, and the presence of major hyperscale technology companies.

Asia Pacific, with a 28.6% share and accelerating CAGR, is the fastest-growing region, driven by 5G expansion, digital transformation, and rising cloud adoption across China, India, and Southeast Asia.

Leading companies include Hewlett Packard Enterprise (HPE), Dell Technologies Inc., Cisco Systems Inc., Schneider Electric SE, Vertiv Group Corp., Huawei Technologies Co., Ltd., Delta Electronics, Inc., Rittal GmbH & Co. KG, and Fsas Technologies Inc. (Fujitsu Limited).

Key applications include greenfield deployments at new sites, brownfield upgrades to existing facilities, and upgrade/consolidation of aging infrastructure, supporting industries from BFSI to defense and healthcare.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)