CO2 Based Plastics Market Size, Share, Trends and Forecast by Type, Production Process, Application, and Region, 2025-2033

CO2 Based Plastics Market Size and Share:

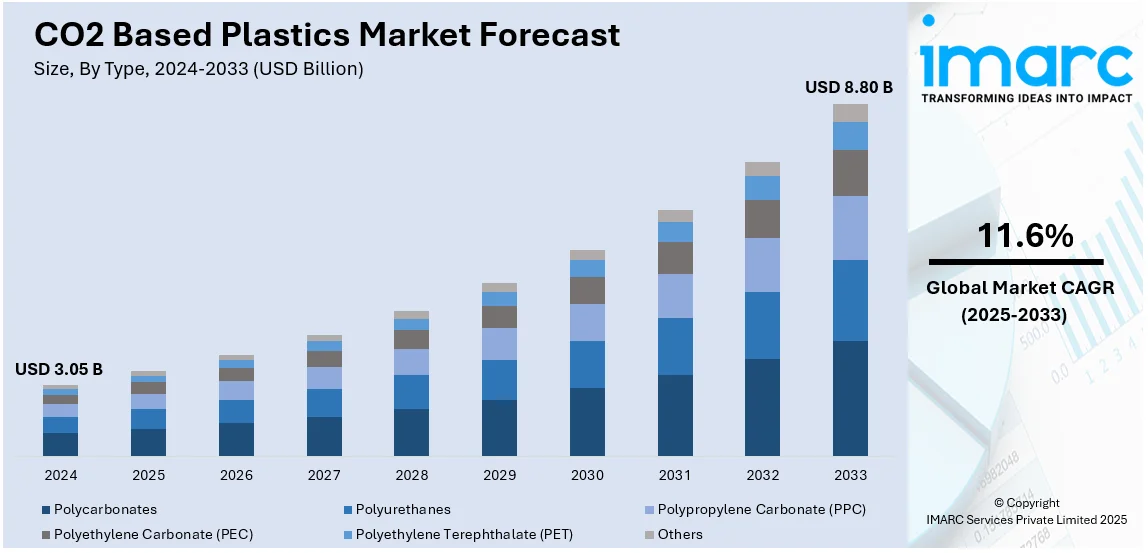

The global CO2 based plastics market size was valued at USD 3.05 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 8.80 Billion by 2033, exhibiting a CAGR of 11.6% from 2025-2033. North America currently dominates the market, holding a market share of over 44.5% in 2024. The increasing carbon capture utilization initiatives, advancements in thermocatalytic and electrochemical polymerization, rising demand for sustainable packaging, regulatory mandates on emission reduction, and growing investments in bio-based feedstocks are some of the major factors positively impacting the CO2 based plastics market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 3.05 Billion |

| Market Forecast in 2033 | USD 8.80 Billion |

| Market Growth Rate (2025-2033) | 11.6% |

The market is primarily driven by the rising emphasis on carbon utilization technologies to reduce industrial emissions. The International Energy Agency (IEA) reports a significant increase in carbon capture as of 2023, utilization, and storage (CCUS) projects, with over 700 initiatives in various development stages. The announced capture capacity for 2030 has risen by 35% and storage capacity by 70%, aiming to reach approximately 435 Million Tonnes of CO2 captured annually by 2030. Furthermore, rising research and development (R&D) investments in polymerization techniques for CO2 derived polycarbonates and polyurethanes toward commercialization are another major growth factor. Additionally, the implementation of supportive regulatory frameworks for sustainable materials is further accelerating CO2 based plastics market growth. Besides that, the increasing demand for biodegradable and recyclable plastics across packaging, textiles, and automotive applications is driving the product adoption.

The market in the United States is experiencing significant growth, driven by favorable incentives supporting carbon capture and utilization. In addition to this, rising corporate commitments to net-zero targets are encouraging the adoption of sustainable polymers. Moreover, the presence of leading research institutions and funding for advanced CO2 conversion technologies is accelerating material innovations. Continual research and development (R&D) activities are leading to innovations and creating market opportunities. For instance, on November 13, 2024, Massachusetts Institute of Technology (MIT) engineers unveiled a novel electrode design that enhances the efficiency of electrochemical reactions, converting carbon dioxide into valuable products like ethylene, which is an extensively utilized chemical that can be converted into a range of fuels and plastics. This advancement could significantly improve the economic viability of carbon capture and utilization technologies. Apart from this, increased public awareness and investor interest in sustainable materials are further strengthening market growth prospects.

CO2 Based Plastics Market Trends:

Growing Research and Development (R&D) Activities

The CO2-based plastics market is experiencing intensified research and development efforts focused on improving polymerization processes, which is enhancing the CO2-based plastics market outlook. The main areas that are being worked on include reaction efficiency, monomer compatibility, and optimization of reaction catalysts to improve the commercial viability of CO2-derived polymers. Research establishments and collaborators from the industry are also working on new co-polymerization techniques for improving the mechanical and thermal characteristics of CO2 based plastics. On December 19, 2024, scientists at The University of Manchester announced a significant advancement in converting carbon dioxide into bio-based plastics. Utilizing cyanobacteria, commonly known as blue-green algae, the team enhanced the production of citramalate, a precursor for renewable plastics like Perspex achieving a 23-fold increase through optimized process parameters. With increased funding and collaboration with academia, advancements in research and development (R&D) are expected to accelerate the transition and drive market growth.

Innovation in CO2 Capturing Technologies

The market for CO2-based plastics is expanding as industries look for sustainable substitutes for fossil materials, which is a significant CO2 based plastics market trend. The latest advances in carbon capture technologies render CO2 an acceptable feedstock for polymerization while decreasing the emissions generated during the process. These new catalytic conversions, microbial fermentations, and electrochemical processes will work together to improve efficiency, cut costs, and enable large-scale implementation. On November 6, 2024, SINTEF researchers introduced the continuous swing adsorption reactor (CSAR), a new technology for enhanced carbon capture from industrial flue gas. It produces CO2 adsorption and release with minimum consuming energy through its heat and vacuum pumps. Regulatory policies promoting carbon neutrality and corporate sustainability commitments are accelerating investment in this sector. With applications in packaging, automotive, and consumer goods, and the shift to a low-carbon and circular economy, CO2-based plastics are positioned as a crucial solution.

Expansion of CO2-Based Plastics Production Facilities

Increasing production capacities by companies due to the CO2-based plastics market demand is leading to market development. Investments in mega factories is on the rise, with dedicated facilities for CO2 polycarbonates and polyurethanes being built by key players in the industry. Emerging economies are also witnessing infrastructure development to support localized production, reducing supply chain dependencies and transportation emissions. As regulatory frameworks tighten around fossil-based plastics, companies are accelerating facility expansions to ensure stable supply chains and wider market penetration for CO2-based alternatives. On August 20, 2024, VTT Technical Research Centre of Finland and LUT University inaugurated a CO2 conversion pilot plant in Espoo, Finland. Housed within sea containers, this facility is designed to transform captured carbon dioxide emissions into plastic materials, aiming to replace fossil-based raw materials with sustainable alternatives.

CO2 Based Plastics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global CO2 based plastics market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on type, production process, and application.

Analysis by Type:

- Polycarbonates

- Polyurethanes

- Polypropylene Carbonate (PPC)

- Polyethylene Carbonate (PEC)

- Polyethylene Terephthalate (PET)

- Others

Polycarbonates leads the market with around 60% of market share in 2024 due to their high-performance properties and sustainable potential. These engineering thermoplastics are widely recognized for their impact resistance, optical clarity, and thermal stability, which makes them ideal for applications in automotive, electronics, construction, and consumer goods. The concerns about carbon emissions led to the increase in CO2 derived polycarbonates, which is an eco-friendly alternative to conventional petroleum-based plastics. These materials use captured CO₂ as a feedstock, thereby reducing the fossil resources dependence and aiding in reducing carbon footprint. Companies are now investing in advanced polymerization technologies that help scale up and commercial viability of CO2based polycarbonates to boost market growth further. Regulatory support for low-carbon materials and better consumer demand for products that are made with sustainability considerations have also been contributing to the market growth.

Analysis by Production Process:

- Electrochemistry

- Microbial Synthesis

- Thermocatalysis

Thermocatalysis leads the market with around 42.5% of market share in 2024. It enables efficient and scalable conversion of carbon dioxide into valuable polymer precursors. Thermocatalysis is a catalytic transformation of CO₂ into monomers (cyclic carbonates) or polyols (glycols), which is subsequently used in the manufacture of new sustainable plastics such as polycarbonates and polyurethanes under conditions of control in temperature. Thermocatalysis is the most relevant technology for the reduction of emissions of carbon as it permits the utilization of captured CO₂ with minimum mineral feedstock. New developments in catalyst design, particularly heterogeneous and organometal catalysts, are likely to improve overall efficiency, selectivity, and cost-effectiveness of reactions, making CO2 derived plastics more commercially feasible. The growing interest in carbon utilization technologies, along with the increasing regulatory incentives for low-emission materials, further drives the uptake of the thermocatalytic process. Industries in search of sustainability inevitably use thermocatalysis as an emerging technology for the production process.

Analysis by Application:

- Packaging

- Films

- Bottles

- Containers

- Trays

- Others

- Automotive Components

- Interior Components

- Structural Parts

- Construction Materials

- Pipes

- Panels

- Insulation

- Others

- Electronic Components

- Casings

- Connectors

- Circuit Boards

- Others

- Textile Processing

- Fibers

- Non-Woven Fabrics

- Others

Packaging leads the market with around 52.5% of market share in 2024 due to the augmenting demand for sustainable materials that reduce carbon footprints and dependency on fossil-based plastics. CO2derived polymers, including polycarbonates and polyurethanes, are being developed for packaging solutions due to their durability, flexibility, and recyclability. These materials offer an eco-friendly alternative for food, beverage, and consumer goods packaging by utilizing captured carbon dioxide as a feedstock, contributing to carbon reduction efforts. Companies invest in adding advanced polymerization techniques, thereby increasing the performance of CO2 based plastics to industry standards. Increasing regulation to reduce single-use plastic waste and rising consumer preference for sustainable packaging is quickening the market adoption pace. As industries continue to look upon innovative avenues in packaging to lower environmental impacts, CO2 based plastics are proving to be the suitable option.

Regional Analysis:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East

- Africa

In 2024, North America accounted for the largest market share of over 44.5% driven by strong regulatory support, technological advancements, and increasing sustainability initiatives. The region is home to key players investing in carbon capture and utilization (CCU) technologies to develop CO2 derived plastics. Government policies promoting low-carbon materials, alongside corporate commitments to net-zero emissions, are accelerating the adoption of CO2 based plastics in automotive, packaging and consumer goods. In addition, research institutions and startups around the U.S. and Canada continue to focus on catalysis and polymerization processes in improving commercial viability for CO2 based solutions. With more focus on reducing waste produced by plastics and, subsequently, the carbon footprint due to plastic use, industries are emerging toward sustainable solutions. With increasing demand for eco-friendly materials and an expanded circular economy framework, North America has sustained its position as one of the major regions in the market.

Key Regional Takeaways:

United States CO2 Based Plastics Market Analysis

The United States holds a substantial share of the North American CO2 based plastics market at 84.50%. The growing CO2 based plastics market in the U.S. is attributed to increased sustainability goals and encouraging government policies toward carbon capture. For example, in December 2024, OCED released a Notice of Funding Opportunity (NOFO) to provide up to USD 1.3 Billion for revolutionary large-scale carbon capture, utilization, and storage technologies. Additionally, further investments in CO2-based plastic technologies are driven by the Inflation Reduction Act (IRA) and federal incentives for carbon usage. Companies commercialize bioplastics based on captured carbon, which provides an impetus to the market. The packaging industry, particularly food and beverage containers, is a major application area due to the growing consumer preference for eco-friendly alternatives. Corporate sustainability commitments also fuel the market as many brands create commitments for using CO2-derived materials. Also, research and development (R&D) activities are being focused on improving the performance of polymers while trying to reduce production costs through changes in catalyst technologies. The circular economy perspective supports the market. The increasing pressure from regulatory and environmental fronts will push the market growth in the region.

Europe CO2 Based Plastics Market Analysis

Europe is one of the leaders in the CO2 based plastics market, driven by stringent environmental regulations, carbon pricing mechanisms, and strong circular economy initiatives. Government policies encourage investment in carbon capture and utilization (CCU) technologies, thereby fostering innovations. For example, on February 6, 2024, the European Commission adopted the Industrial Carbon Management Communication, outlining a strategy to enhance the deployment of technologies for capturing, storing, transporting, and utilizing CO2 emissions from industrial facilities within the EU. The goal of this effort is to construct at least 50 million tons of CO2 storage capacity annually by 2030, with the aim of achieving net-zero CO2 emissions by 2050.Germany, the Netherlands, and France are the countries with great potential, with enterprises being pioneers in the production of CO2-based polyols and polycarbonates. The packaging and automotive sectors consume the most, with the latter seeking lightweight, sustainable alternatives to their vehicles' interiors and components. The commitments towards the net-zero targets emphasize reducing dependencies on fossil-based plastics, a regional effort. The region's leadership in sustainability policies and growing consumer demand for bio-based and recycled materials drive steady market expansion. Europe's long-term focus on decarbonization and circular economy models ensures CO2-based plastic market growth.

Asia Pacific CO2 Based Plastics Market Analysis

Asia Pacific's CO2-based plastics market is growing due to increasing industrialization, government sustainability initiatives, and rising demand for eco-friendly materials in packaging and consumer goods. China, Japan, and South Korea are leading adopters, with investments in carbon capture and utilization projects supporting polymer production. According to reports, China is dedicated to attaining carbon neutrality by 2060 and reaching its peak carbon emissions by 2030. The combination of this target with incentives for green manufacturing strengthens the market growth. Companies are spending money on CO2-derived plastic technology as a step toward decreasing dependence on petroleum-derived polymers. The region's vast manufacturing base and strong consumer goods sector create demand for sustainable materials, particularly in food packaging and electronics. Research works focus on enhancing polymer properties and producing CO2-derived plastics. Asia Pacific has become the most important player in CO2-based plastic expansion with long-term growth prospects due to its position as a hub for global manufacturing and support from regulatory authorities.

Latin America CO2 Based Plastics Market Analysis

Latin America is an emerging region in the market, driven by environmental concerns, government policies, and industry initiatives to reduce plastic waste. Brazil and Mexico are leading markets due to their strong industrial sectors and growing interest in sustainable materials. Brazil's bioeconomy focus and Mexico's initiatives to reduce plastic pollution lead to opportunities for plastics derived from CO2. The region's food and beverage packaging sectors are currently investigating alternative sustainable solutions to traditional plastics. Companies in this region are also forming partnerships to link with businesses in other countries, focusing on gaining access to CO2-based polymer technologies. Brazil, on October 23, 2024, launched the Brazil Investment Platform (BIP) in a side event among the G20 finance ministers and central bank governors in Washington, D.C. The purpose of this new initiative is to bring in international investments targeting climate and ecological projects in the areas of energy, industry, mobility, and nature-based solutions that are critical for scaling CO2 utilization technologies. The region's abundant natural resources and increasing investment in green technologies provide a foundation for future expansion.

Middle East and Africa CO2 Based Plastics Market Analysis

The Middle East and Africa's CO2-based plastics market is in its developing stage. The region's petrochemical dominance and growing sustainability initiatives are creating opportunities for CO2-derived plastics. The UAE and Saudi Arabia are investing in carbon capture and utilization technologies as part of their net-zero strategies. By 2030, the UAE aims to have 5 Million tons per annum (MTPA) of CCUS capacity. Saudi Aramco and Masdar are exploring CO2 conversion projects that could support polymer production. The packaging and construction sectors present potential growth areas for the market due to the demand for sustainable materials on the rise. Furthermore, Africa's focus on reducing plastic pollution and the rise of circular economy initiatives may drive future adoption, particularly in South Africa and Kenya. Also, strategic partnerships with global firms and technology transfers accelerate market development. In line with this, the increasing investment in sustainability and carbon management is expected to foster long-term growth in the CO2-based plastics market in the Middle East and Africa region.

Competitive Landscape:

The market is highly competitive, driven by existing technological advancements and increasing investments in carbon capture and utilization (CCU). Players in the market compete in the manufacturing of high-performance polymers with improved mechanical and heat characteristics. Companies invest in research and development (R&D) to enhance durability, biodegradability, and recyclability while improving production efficiency. Collaborations with research organizations and the government are established to improve cost-effectiveness and scalability. Expansion in applications such as packaging, automotive, and consumer goods drives innovation in production processes. Some of the factors, such as regulatory compliance, patents, and proprietary technologies, create entry barriers. Competition intensifies as firms seek to optimize feedstock sourcing, enhance production efficiency, and expand distribution networks to meet growing sustainability demands.

The report provides a comprehensive analysis of the competitive landscape in the CO2 based plastics market with detailed profiles of all major companies, including:

- Asahi Kasei Corporation

- Avantium

- Cardia Bioplastics

- ChangHua Chemical Technology Co.,Ltd.

- Covestro AG

- Empower Materials

- LanzaTech

- NatureWorks LLC.

- Plastipak Holdings, Inc.

- Saudi Arabian Oil Co.

- TotalEnergies Corbion

Latest News and Developments:

- March 20, 2024: LG Chem unveiled Polyethylene Carbonate (PEC), an eco-friendly plastic produced from captured carbon dioxide, at Cosmoprof Bologna 2024 in Italy. Developed using proprietary catalysts and process technologies, PEC achieves the highest productivity among existing CO2 based plastics. Primarily intended for cosmetic containers and food packaging, PEC exemplifies LG Chem's commitment to sustainable materials and global warming mitigation.

- October 15, 2024: Fortum Recycling & Waste announced the successful production of biodegradable plastic from CO2 emissions at its Riihimäki plant in Finland. This achievement, part of the Carbon2x program, utilizes carbon capture and utilization (CCU) technology to convert emissions from waste incineration into sustainable raw materials for the plastics industry. The initiative aims to reduce reliance on fossil-based resources and promote circular economy solutions.

- October 17, 2024: CO2BioClean inaugurated a pilot plant at Industriepark Höchst in Frankfurt, Germany, to convert industrial CO2 emissions into biodegradable plastics using a proprietary fermentation process. This facility aims to reduce CO2 emissions and produce compostable bioplastics for applications in cosmetics, packaging, and agriculture. The project received support from Hessen's economic development programs and the Enterprise Europe Network at Hessen Trade & Invest GmbH.

CO2 Based Plastics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | USD Billion |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Polycarbonates, Polyurethanes, Polypropylene Carbonate (PPC), Polyethylene Carbonate (PEC), Polyethylene Terephthalate (PET), Others |

| Production Processes Covered | Electrochemistry, Microbial Synthesis, Thermocatalysis |

| Applications Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Asahi Kasei Corporation, Avantium, Cardia Bioplastic, ChangHua Chemical Technology Co.,Ltd., Covestro AG, Empower Materials, LanzaTech, NatureWorks LLC., Plastipak Holdings, Inc., Saudi Arabian Oil Co., TotalEnergies Corbion ., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the CO2 based plastics market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global CO2 based plastics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the CO2 based plastics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The CO2 based plastics market was valued at USD 3.05 Billion in 2024.

The CO2 based plastics market is projected to exhibit a CAGR of 11.6% during 2025-2033, reaching a value of USD 8.80 Billion by 2033.

The market is driven by increasing demand for sustainable alternatives, stringent environmental regulations on carbon emissions, and advancements in carbon capture and utilization (CCU) technologies. Growing investments in circular economy initiatives, rising consumer preference for eco-friendly products, and government incentives for CO2-derived materials further boost adoption.

North America currently dominates the CO2 based plastics market, accounting for a share of 44.5% in 2024. The dominance is fueled by strong government policies supporting carbon capture utilization, investments in sustainable polymer research, rising demand for eco-friendly packaging, corporate net-zero commitments, and advancements in thermocatalysis and polymerization technologies.

Some of the major players in the CO2 based plastics market include Asahi Kasei Corporation, Avantium, Cardia Bioplastic, ChangHua Chemical Technology Co.,Ltd., Covestro AG, Empower Materials, LanzaTech, NatureWorks LLC., Plastipak Holdings, Inc., Saudi Arabian Oil Co., and TotalEnergies Corbion, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)