Clot Management Devices Market Size, Share, Trends and Forecast by Product Type, End-User, and Region, 2025-2033

Clot Management Devices Market Size and Share:

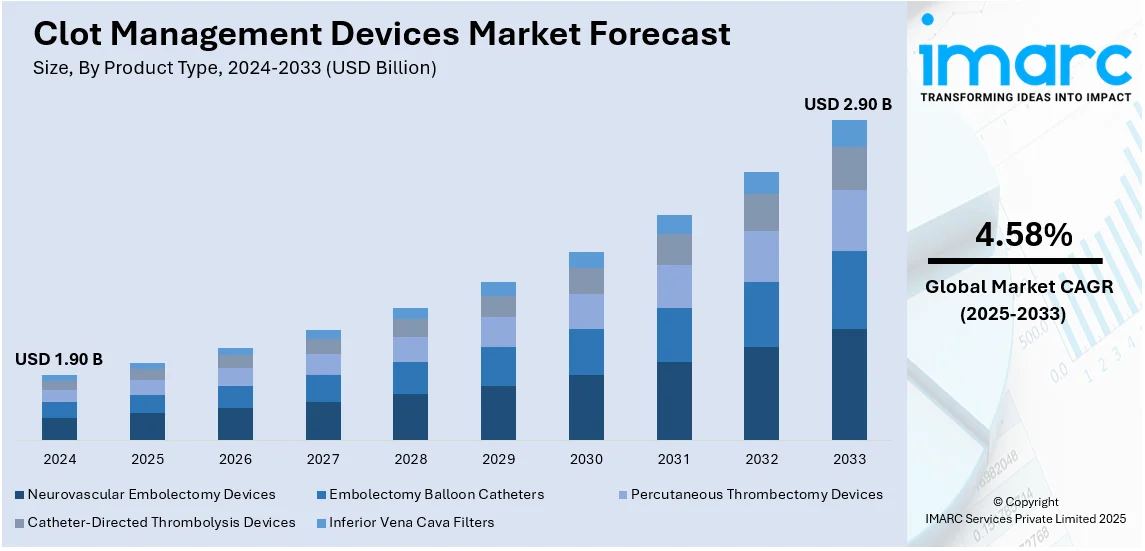

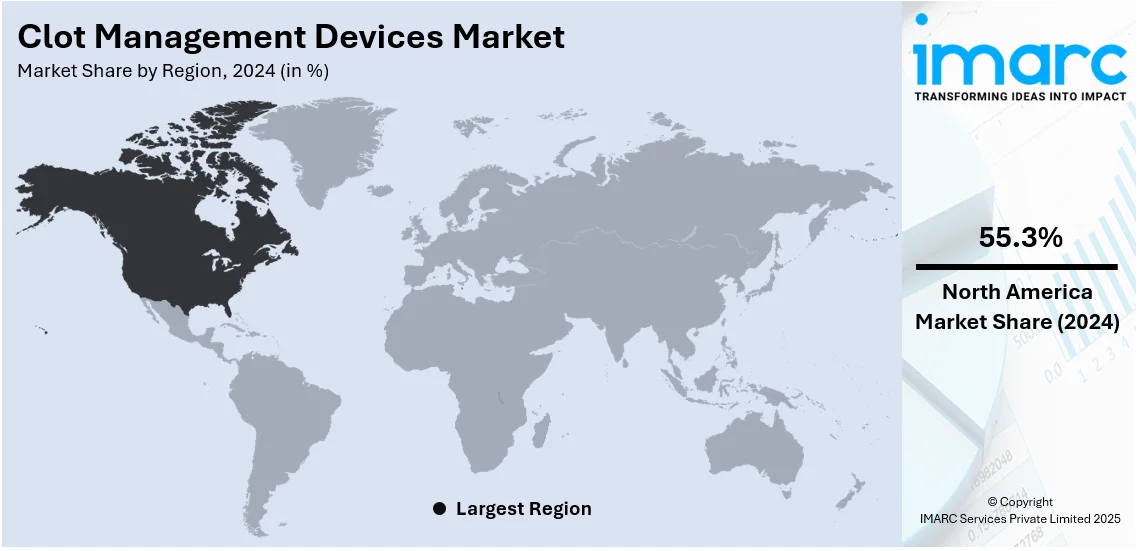

The global clot management devices market size was valued at USD 1.90 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 2.90 Billion by 2033, exhibiting a CAGR of 4.58% during 2025-2033. North America currently dominates the market, holding a significant market share of over 55.3% in 2024. The rising prevalence of cardiovascular diseases, an aging population, increasing demand for minimally invasive procedures, and technological advancements are some of the key factors fueling the clot management devices market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 1.90 Billion |

|

Market Forecast in 2033

|

USD 2.90 Billion |

| Market Growth Rate 2025-2033 | 4.58% |

The market for clot management devices is driven by the rising prevalence of deep vein thrombosis, cardiovascular diseases, stroke, and pulmonary embolism, which increase the demand for effective clot removal solutions. A rapidly increasing geriatric population, more susceptible to thrombotic disease, fuels the market further. Advances in technology for minimally invasive procedures improve patient outcomes with shorter hospital stays and recovery periods. Greater awareness of early detection and treatment of clots and favorable reimbursement practices drive adoption. Additionally, rising healthcare expenditures, government support for advanced medical technologies, and the expansion of specialized treatment centers contribute to market growth. The presence of key medical device manufacturers and ongoing research into innovative thrombectomy techniques also drive the industry's competitive landscape.

The market for clot management devices in the United States is driven by the high prevalence of deep vein thrombosis, cardiovascular diseases, and pulmonary embolism. The country’s advanced healthcare infrastructure, increasing adoption of minimally invasive procedures, and strong presence of leading medical device manufacturers contribute to market growth. Favorable reimbursement policies and high healthcare spending enhance access to advanced treatments. Additionally, rising awareness about early clot detection, a growing geriatric population, and technological advancements in thrombectomy devices fuel demand. For instance, in January 2025, Argon Medical Devices reported the initial patient enrollment in the CLEAN-PE study, which seeks to assess the safety and effectiveness of the Cleaner Pro thrombectomy system for extracting blood clots from the lungs of patients diagnosed with pulmonary embolism (PE). It is anticipated that more than 100 patients are enrolled in CLEAN-PE at different hospitals throughout the United States. Government support, ongoing research and development, and an increasing number of outpatient procedures further propel the market’s expansion in the U.S.

Clot Management Devices Market Trends:

Rising Prevalence of Cardiovascular Diseases and Thrombotic Disorders

The increasing incidence of cardiovascular diseases, stroke, deep vein thrombosis, and pulmonary embolism is a major driver of the clot management devices market. Sedentary lifestyles, obesity, smoking, and hypertension contribute to higher cases of blood clots, necessitating effective treatment solutions. An aging global population further escalates the risk of thrombotic disorders, increasing demand for advanced clot removal technologies. According to recent industry reports, in 2024, 12% of the global population was aged 60 years and above, equating to 1.2 Billion individuals. This number is expected to rise to 2.1 Billion by 2050, making up 26% of the total population in the world. The growing awareness about early diagnosis and intervention has led to higher adoption of clot management devices in hospitals and specialized clinics. This rising disease burden continues to push the research, development, and commercialization of innovative clot removal technologies.

Technological Advancements in Clot Management Devices

Ongoing innovations in clot management devices, such as percutaneous thrombectomy systems, catheter-directed thrombolysis, and mechanical thrombectomy devices, are revolutionizing patient care. These advancements allow for minimally invasive procedures, reducing recovery time and hospital stays while improving patient outcomes. Modern thrombectomy devices offer enhanced precision and efficiency, making procedures safer and more effective. Artificial intelligence, robotics, and real-time imaging further contribute to improved clot removal techniques. As healthcare providers seek better, faster, and safer treatment options, continuous product development and regulatory approvals drive the adoption of advanced clot management technologies. For instance, in September 2024, The CLEANER VacTM Thrombectomy System, which is intended to remove blood clots from the peripheral venous vasculature, was introduced by Argon Medical Devices, a leading provider of medical device solutions for interventional radiology, vascular surgery, interventional cardiology, and oncology procedures. A single-use, large-bore aspiration tool called the CLEANER Vac Thrombectomy System was developed to quickly and effectively remove blood clots, also known as thrombus, from veins with restricted blood flow.

Favorable Healthcare Policies and Reimbursement Support

Supportive government policies and reimbursement frameworks create a positive clot management devices market outlook by making advanced clot management treatments more accessible. Many countries, including the United States, offer favorable insurance coverage for thrombectomy procedures, encouraging more hospitals and healthcare providers to adopt these technologies. Regulatory approvals from agencies like the FDA and CE mark certification for new clot management devices further drive market expansion. For instance, in March 2023, Penumbra received approval from the Food and Drug Administration to introduce Lightning Bolt 7, a revolutionary arterial thrombectomy system. The technology employs pressure sensors and an algorithm to determine whether the device is pulling in blood or a clot and modulates aspiration to remove blood clots. Penumbra, situated in Alameda, California, anticipates a 23% to 25% increase in sales in 2023 due to the Lightning Bolt 7 product and the recent introduction of Lightning Flash, another vascular device. Additionally, increasing healthcare expenditures and investments in medical infrastructure create opportunities for manufacturers to introduce innovative clot management solutions, ensuring broader patient access to life-saving treatments.

Clot Management Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global clot management devices market, along with forecasts at the global, regional, and country levels from 2025-2033. The market has been categorized based on product type, and end-user.

Analysis by Product Type:

- Neurovascular Embolectomy Devices

- Embolectomy Balloon Catheters

- Percutaneous Thrombectomy Devices

- Mechanical Thrombectomy

- Aspiration Thrombectomy

- Percutaneous Mechanical Thrombectomy (PMT)

- Catheter-Directed Thrombolysis Devices

- Inferior Vena Cava Filters

- Permanent

- Retrievable

Percutaneous thrombectomy devices stand as the largest product type in 2024, holding around 37.6% of the market due to their effectiveness in rapidly removing blood clots with minimal invasiveness. These devices are widely used in treating deep vein thrombosis, pulmonary embolism, and arterial thrombosis, reducing the risk of complications and improving patient outcomes. Advancements in technology have enhanced their precision and efficiency, making them a preferred choice among healthcare professionals. Additionally, the growing prevalence of cardiovascular diseases, an aging population, and increasing demand for faster recovery times further drive their adoption. Their ability to minimize hospital stays and healthcare costs also boosts market growth.

Analysis by End-User:

- Hospitals

- Diagnostic Centers and Specialty Clinics

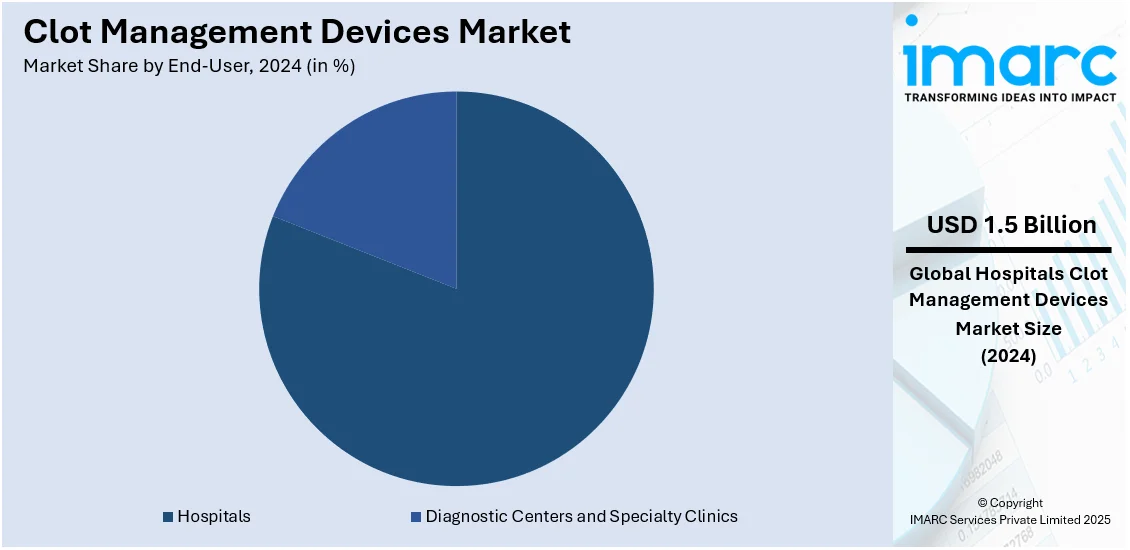

Hospitals leads the market with around 80.9% of market share in 2024 due to their advanced infrastructure, skilled healthcare professionals, and ability to handle complex thrombectomy procedures. They offer a wide range of clot management treatments, including percutaneous thrombectomy, catheter-directed thrombolysis, and surgical thrombectomy, ensuring comprehensive patient care. The increasing prevalence of cardiovascular diseases and emergency cases requiring immediate clot removal further drive demand. Additionally, hospitals have better access to cutting-edge medical technologies and government funding, enhancing treatment efficiency. The rising number of hospital admissions for thrombotic disorders and the availability of reimbursement policies also contribute to their market dominance.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 55.3%. The clot management devices demand in North America is influenced by the high prevalence of cardiovascular diseases, stroke, deep vein thrombosis, and pulmonary embolism. The region’s advanced healthcare infrastructure, strong presence of key medical device manufacturers, and increasing adoption of minimally invasive procedures contribute to market growth. Favorable reimbursement policies, high healthcare spending, and government support for advanced medical technologies further enhance accessibility. Additionally, rising awareness of early clot detection and treatment, coupled with a growing geriatric population prone to thrombotic disorders, fuels demand. Technological advancements and an increasing number of outpatient procedures also play a significant role.

Key Regional Takeaways:

United States Clot Management Devices Market Analysis

In 2024, the United States accounted for over 89.80% of the clot management devices market in North America. The United States clot management devices market is primarily driven by the rising incidence of cardiovascular diseases, such as deep vein thrombosis (DVT), pulmonary embolism (PE), and stroke, driven by an increasing geriatric population and growing obesity rates. According to the Population Reference Bureau, the number of individuals aged 65 and above in the United States will reach 82 million by 2050, accounting for 23% of the population of the country. Moreover, the prevalence of atrial fibrillation, a key risk factor for thromboembolic events, is also rising, propelling the need for advanced clot removal solutions. Technological advancements in thrombectomy and embolectomy devices, such as catheter-directed thrombolysis and aspiration thrombectomy, are also improving procedural efficiency and patient outcomes, fueling adoption in hospitals and ambulatory surgical centers. Additionally, the growing preference for minimally invasive procedures over conventional surgical interventions is further contributing to industry expansion, as these devices reduce complications, hospital stays, and recovery times. Favorable reimbursement policies and guidelines from organizations such as the American Heart Association (AHA) and the U.S. Food and Drug Administration (FDA) further support the adoption of innovative clot management technologies. Besides this, expanding clinical research on novel clot management approaches is expected to further propel industry advancements.

Asia Pacific Clot Management Devices Market Analysis

The Asia Pacific clot management devices market is growing due to rising cases of atrial fibrillation and hypertension, both significant risk factors for thromboembolic disorders. Moreover, the increasing prevalence of cardiovascular diseases and venous thromboembolism (VTE), driven by aging populations, rising urbanization, and lifestyle-related risk factors such as diabetes, is also propelling the market. According to industry reports, 52.9% of the total population of Asia lived in urban areas in 2024, equating to 2,545,230,547 individuals. Additionally, rising awareness about stroke prevention and early treatment, driven by national health programs, is also encouraging the adoption of advanced clot removal technologies. Furthermore, the expansion of private healthcare facilities and the increasing presence of multinational medical device companies in emerging markets are improving access to cutting-edge thrombectomy and embolectomy solutions. Growing disposable incomes and improved insurance coverage are also making high-cost clot management procedures more accessible, supporting overall market growth.

Europe Clot Management Devices Market Analysis

The Europe clot management devices market is experiencing growth, fueled by the increasing prevalence of thromboembolic disorders, driven by aging demographics and sedentary lifestyles. The growing burden of non-communicable diseases, including hypertension, diabetes, and cardiovascular disorders, further elevates the risk of thromboembolic events. According to the World Health Organization (WHO), cardiovascular diseases (CVDs) account for more than 42.5% of all deaths each year in Europe, making them the leading cause of premature death in the region. The widespread implementation of national stroke prevention programs and guidelines by organizations such as the European Society of Cardiology (ESC) and the European Stroke Organisation (ESO) is driving the adoption of advanced thrombectomy and thrombolysis devices. Increasing healthcare investments across Europe, particularly in digital health integration and AI-powered clot detection technologies, is further improving diagnosis and treatment precision. Additionally, the rising number of stroke centers and specialized vascular care units across countries such as Germany, the UK, France, and Italy is also boosting demand for advanced clot management technologies. Increasing awareness campaigns and training programs for healthcare professionals on thromboembolic disease management are further driving adoption. The rise in surgical procedures, particularly orthopedic and cancer-related surgeries, is also leading to a higher incidence of post-operative blood clots, propelling the need for effective clot management solutions.

Latin America Clot Management Devices Market Analysis

The Latin America clot management devices market is expanding due to the increasing prevalence of hypertension and metabolic disorders, which elevate the risk of thromboembolic events. Growing healthcare expenditure and government initiatives aimed at improving stroke care are enhancing access to advanced thrombectomy and thrombolysis procedures. For instance, as per the International Trade Administration (ITA), 9.47% of the GDP of Brazil is spent on healthcare, making it the largest market for healthcare in Latin America. The expansion of private hospitals and specialized stroke centers, particularly in Brazil, Mexico, and Argentina, is further supporting market growth. According to the ITA, 62% of the hospitals in Brazil are private. Besides this, strengthening regulatory frameworks and faster approval processes are also facilitating the introduction of new clot removal technologies in the region.

Middle East and Africa Clot Management Devices Market Analysis

The Middle East and Africa clot management devices market is propelled by an increasing geriatric population and a higher incidence of risk factors such as hypertension and dyslipidemia, increasing the likelihood of thromboembolic events. Expanding health insurance coverage and government subsidies in countries such as Saudi Arabia and the UAE are improving access to advanced clot removal procedures. For instance, according to the International Trade Administration, the Saudi Arabian government intends to invest more than USD 65 billion under Vision 2030 to build the nation's healthcare system and restructure and privatize insurance and health care. Additionally, local manufacturing initiatives and partnerships with international medical device companies are improving product availability and affordability. Growing medical tourism in the region is further supporting the adoption of advanced clot management technologies.

Competitive Landscape:

The market for clot management devices is extremely competitive, and major competitors are concentrating on product improvements, strategic mergers, and technology breakthroughs to improve their market positions. Major companies like Medtronic, Boston Scientific, Terumo Corporation, and Abbott Laboratories dominate the industry with a broad product portfolio and global presence. Startups and mid-sized firms are also entering the market, introducing novel minimally invasive solutions. Collaborations with healthcare providers and research institutions drive innovation. Regulatory approvals, reimbursement policies, and clinical trial success significantly impact market dynamics. Companies compete based on product efficacy, pricing, and distribution networks, making innovation and strategic expansion crucial.

The report provides a comprehensive analysis of the competitive landscape in the clot management devices market with detailed profiles of all major companies, including:

- AngioDynamics Inc.

- Argon Medical Devices Inc.

- Boston Scientific Corporation

- DePuy Synthes Inc.

- Edwards Lifesciences Corporation

- iVascular S.L.U.

- Lemaitre Vascular Inc.

- Medtronic Inc.

- Straub Medical AG

- Stryker Corporation

- Teleflex Incorporated

- Vascular Solutions

Latest News and Developments:

- February 2025: Retriever Medical, a leading provider of advanced medical services, secured a patent from the United States Patent and Trademark Office (USPTO) for its groundbreaking clot removal device. The device has been created to revolutionize the management and treatment of vascular occlusions by providing unprecedented levels of accuracy, versatility, and effectiveness in eliminating undesired material and clots from an individual's body.

- February 2025: Surmodics Inc., a global leader in medical and in-vitro diagnostic solutions, successfully completed the clinical trial of its Pounce XL Thrombectomy System. With the inclusion of this device, which is intended to be used in 5.5–10 mm peripheral arteries, the Pounce™ Thrombectomy System will be able to quickly eliminate chronic or acute clots throughout the lower extremities without the need for thrombolysis, aspiration, or expensive instruments.

- December 2024: The groundbreaking Liquet Versus Catheter, invented by Dr. Patrick Kelly, a renowned vascular surgeon, secured FDA 510(k) clearance. The device was created to revolutionize the treatment and management of pulmonary artery blood clots, catering to the vital need for better patient outcomes.

- September 2024: Stryker Corporation, a leading provider of medical solutions, successfully acquired NICO Corporation, a renowned provider of navigation devices for the brain that can remove clots and tumors, as well as collect tissue. With this acquisition, Stryker has added minimally invasive technologies for the removal of brain tumors and clots to its wide range of medical devices, strengthening the company’s dedication to innovations in neurotechnology.

- April 2024: Penumbra, one of the leading thrombectomy companies globally, introduced Lightning Flash 2.0, the newest computer-assisted vacuum thrombectomy (CAVT) technology developed for the elimination of blood clots. The device comes equipped with innovative Lightning Flash algorithms that display great speed and sensitivity to blood flow and thrombus and can treat pulmonary emboli (PE) and eliminate venous thrombus. The Lightning Flash 2.0 has secured U.S. Food and Drug Administration (FDA) approval and clearance.

Clot Management Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| End Users Covered | Hospitals, Diagnostic Centers and Specialty Clinics |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AngioDynamics Inc., Argon Medical Devices Inc., Boston Scientific Corporation, DePuy Synthes Inc., Edwards Lifesciences Corporation, iVascular S.L.U., Lemaitre Vascular Inc., Medtronic Inc., Straub Medical AG, Stryker Corporation, Teleflex Incorporated, Vascular Solutions |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the clot management devices market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global clot management devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the clot management devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The clot management devices market was valued at USD 1.90 Billion in 2024.

The clot management devices market is projected to exhibit a CAGR of 4.58% during 2025-2033, reaching a value of USD 2.90 Billion by 2033.

The clot management devices market is driven by the rising prevalence of cardiovascular diseases, deep vein thrombosis, and pulmonary embolism. Increasing demand for minimally invasive procedures, technological advancements, a growing geriatric population, and improved healthcare infrastructure further boost market growth. Favorable reimbursement policies and higher healthcare spending also contribute to expansion.

North America currently dominates the clot management devices market due to high cardiovascular disease prevalence, advanced healthcare infrastructure, technological advancements, reimbursement policies, and growing demand for minimally invasive procedures drive growth.

Some of the major players in the clot management devices market include AngioDynamics Inc., Argon Medical Devices Inc., Boston Scientific Corporation, DePuy Synthes Inc., Edwards Lifesciences Corporation, iVascular S.L.U., Lemaitre Vascular Inc., Medtronic Inc., Straub Medical AG, Stryker Corporation, Teleflex Incorporated, Vascular Solutions, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)