Clinical Trial Management Systems Market Report by Component (Software, Services), Deployment Mode (Web-based CTMS, On-premise, Cloud-based CTMS), End User (Pharmaceutical and Biotechnology Firms, Contract Research Organizations, and Others), and Region 2026-2034

Clinical Trial Management Systems Market Size:

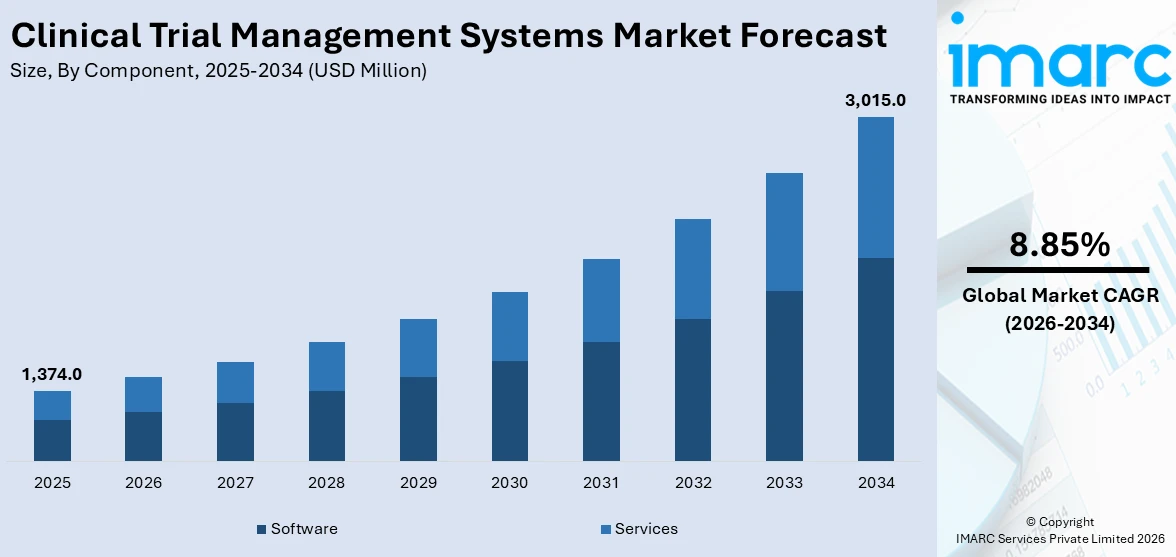

The global clinical trial management systems market size reached USD 1,374.0 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 3,015.0 Million by 2034, exhibiting a growth rate (CAGR) of 8.85% during 2026-2034. The clinical trial management systems (CTMS) market is propelled by factors such as increasing clinical trial complexity, rising adoption of cloud-based CTMS solutions for remote collaboration, stringent regulatory requirements, and the growing emphasis on patient-centric trials for improved efficiency and data quality.

| Report Attribute | Key Statistics |

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 1,374.0 Million |

|

Market Forecast in 2034

|

USD 3,015.0 Million |

| Market Growth Rate (2026-2034) | 8.85% |

Clinical Trial Management Systems Market Analysis:

- Major Market Drivers: The clinical trial management systems market growth is fueled by the growing complexity of multisite clinical trials and the gradual adoption of cloud technology. The market size will potentially grow to a considerable extent considering enhanced requirement for trial management modules.

- Key Market Trends: The clinical trial management system outlook showcases trends such as the rise in utilization of decentralized clinical trials, the virtual trial platforms, and risk-based monitoring methods. Moreover, there is an increasing emphasis on interconnectivity and integration with existing trial systems and software platforms.

- Geographical Trends: North America owns the leading position in CTMS market as it has developed advanced healthcare infrastructure and is conducting numerous research and development activities. However, the Asia-Pacific and Latin America regions, which are undergoing rapid market growth because of medical tourism and improving infrastructure, are also offering clinical trial outsourcing services.

- Competitive Landscape: Some of the major market players in the clinical trial management systems industry include Advarra, Anju Software, Clario, ICON plc, IQVIA Inc., MasterControl Solutions, Inc., Medidata, Mednet, Oracle, Parexel International (MA) Corporation, Pharmaseal, RealTime Software Solutions, LLC, Veeva Systems Inc., among many others.

- Challenges and Opportunities: The market faces challenges such as data protection issues, interoperability issues and regulatory challenges. It also offers opportunities, such opportunities can be determined from implementation of the advanced analytics, real-world evidence integration, and decentralized trial models.

To get more information on this market Request Sample

Clinical Trial Management Systems Market Trends:

Increasing Clinical Trial Complexity

The evolution of precision and personalized medicine has intensified the intricacies of clinical trials, demanding sophisticated management solutions. CTMS platforms play a pivotal role in managing these intricate trials by providing comprehensive solutions for study planning, protocol design, patient enrollment, and data management. By streamlining processes and facilitating collaboration among stakeholders, CTMS platforms help organizations effectively navigate the complexities of modern clinical research, ensuring adherence to rigorous protocols and accelerating the development of innovative therapies. These platforms leverage advanced technologies such as artificial intelligence and machine learning to optimize trial design and execution, enhancing efficiency and generating clinical trial management systems revenue.

Stringent Regulatory Requirements

Regulatory bodies impose rigorous guidelines to uphold patient safety and data integrity, necessitating robust compliance management offered by CTMS platforms. CTMS solutions offer robust tools and functionalities to assist organizations in meeting these regulatory obligations. From ensuring protocol adherence and documentation management to facilitating audit readiness and regulatory reporting, CTMS platforms help organizations navigate the complex regulatory landscape with confidence, reducing compliance risks and ensuring adherence to regulatory standards. Additionally, CTMS platforms incorporate features such as automated compliance monitoring and real-time risk assessment to proactively identify and address regulatory issues, enhancing overall compliance efficiency and effectiveness. For instance, the regulations for clinical trials in the United States are governed by stringent guidelines such as the Food and Drug Omnibus Reform Act of 2022 (FDORA), Privacy Act of 1974, and the NIH Policy Manual on Privacy and Confidentiality.

Emphasis on Patient-Centric Trials

With a shift toward patient-centricity, CTMS platforms prioritize features like patient recruitment portals and remote monitoring to enhance patient engagement and trial success. There is a growing recognition of the importance of patient-centricity in clinical research, with a focus on enhancing patient engagement, experience, and retention. CTMS platforms support this paradigm shift by incorporating features such as patient recruitment portals, remote monitoring capabilities, and electronic patient-reported outcomes (ePRO). By empowering patients with tools for active participation and communication, CTMS platforms improve patient compliance, enhance data quality, and ultimately contribute to the success of patient-centric trials. This is creating a positive clinical trial management systems market overview.

Clinical Trial Management Systems Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on component, deployment mode, and end user.

Breakup by Component:

- Software

- Services

Software accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the component. This includes software, and services. According to the report, software represented the largest segment.

The expanding penetration of software in the CTMS market is mainly induced by the potential for added flexibility, scalability, and customization. Software offerings provide bespoke functions for trial design, subject recruitment, data management, and regulatory conformity as clinical trial ecosystem has different stakeholders. Apart from this, SaaS models facilitate in having cost-effective deployment and easy accessibility, especially for the small and mid-sized organizations. The growing sophistication of the clinical trials and implicit need for advanced analytics and real-time insights has placed software at the heart of trial workflow management, process improvement, and drug development speedup. For instance, the U.S. Federal Government, through the Department of Health and Human Services (HHS) and the National Institutes of Health (NIH), has proposed policy changes to improve clinical trial transparency by expanding trial registration requirements and data sharing to enhance research transparency.

Breakup by Deployment Mode:

- Web-based CTMS

- On-premise

- Cloud-based CTMS

Web-based CTMS holds the largest share of the industry

A detailed breakup and analysis of the market based on the deployment mode have also been provided in the report. This includes web-based CTMS, on-premise, and cloud-based CTMS. According to the report, web-based CTMS accounted for the largest market share.

The web-based CTMS as a deployment mode dominates the CTMS market as web-based methods provide more availability and convenience as users can access the system from any location worldwide where there is internet connection. This makes it possible for a stakeholder team to work remotely and have ready data access, ensuring the smooth running of trials. Moreover, online CTMS systems typically have lower initial costs and fewer IT infrastructure investments than on-site installations making them to be terrific options to small and mid-sized organization looking for an economical and scalable trials management solutions. For instance, Sitero recently acquired the Clario eClinical suite including, Mentor CTMS, a web-based CTMS solution offer benefits, such as easy and affordable third-party eTMF integration, unrestricted access, a familiar Microsoft Office-based interface, rapid implementation, and mobility-enabled features, catering to the demand for efficient and user-friendly CTMS platforms.

Breakup by End User:

Access the comprehensive market breakdown Request Sample

- Pharmaceutical and Biotechnology Firms

- Contract Research Organizations

- Others

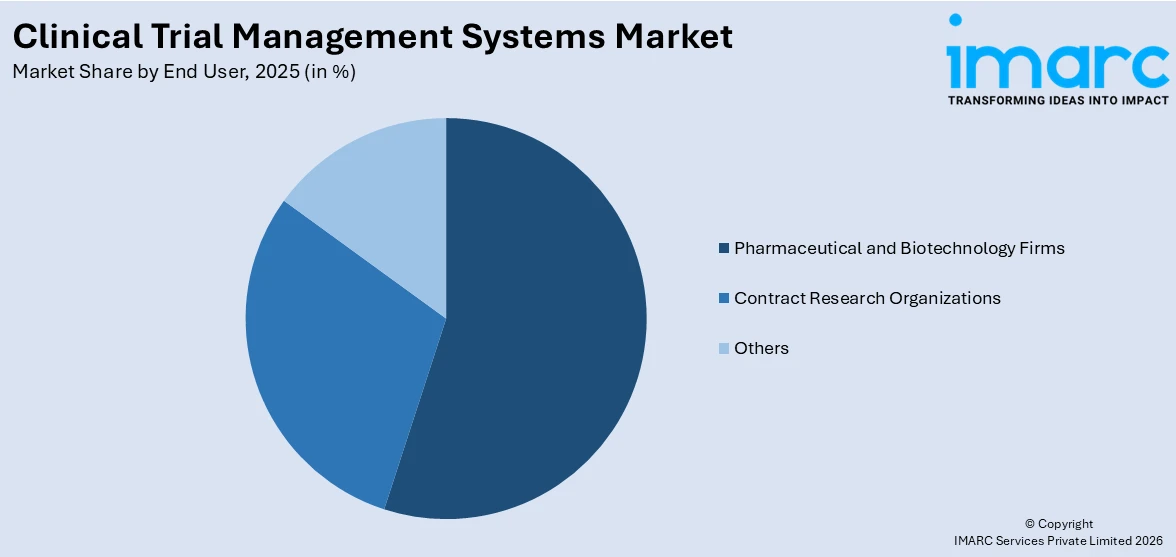

Pharmaceutical and biotechnology firms represent the leading market segment

The report has provided a detailed breakup and analysis of the market based on the end user. This includes pharmaceutical and biotechnology firms, contract research organizations, and others. according to the report, pharmaceutical and biotechnology firms represented the largest market share.

Clinical trials are becoming more complex and highly scrutinized making it necessary for pharmaceuticals and biotechnology companies to incorporate CTMS solutions on a daily basis as the end users. CTMS platforms furnish with all-encompassing features that are meant to be customized for the use of the pharmaceutical and biotech companies, and hence trials operations can be seamlessly carried out. The collaboration of different stakeholders is enhanced and, besides, regulatory compliance is maintained, and therapies developed much faster. Furthermore, CTMS systems are useful to these entities in reducing resources utilization, controlling the clinical trial costs and improving the overall organization productivity, thus improving the clinical trial management systems market statistics.

Breakup by Regional:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest clinical trial management systems market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America holds the leading position in the market for clinical trial management systems.

North America drives the CTMS market due to its robust healthcare infrastructure, extensive clinical research activities, and stringent regulatory standards. The region hosts numerous pharmaceutical, biotechnology, and medical device companies conducting clinical trials, creating a significant demand for CTMS solutions. Additionally, the prevalence of chronic diseases and the need for innovative therapies further fuel the adoption of advanced trial management tools. Moreover, North America's substantial investments in research and development, coupled with its technological advancements and focus on precision medicine, contributing to the the CTMS market growth.

Competitive Landscape:

Key players in the CTMS market are focusing on innovation and strategic partnerships to enhance their offerings and expand their market presence. They are investing in advanced technologies such as artificial intelligence and machine learning to improve trial efficiency and data analytics capabilities, thereby providing the global clinical trial management systems market opportunities. Additionally, these companies are collaborating with pharmaceutical firms, contract research organizations, and academic institutions to develop integrated solutions that address the evolving needs of clinical research. Moreover, they are expanding their global footprint through acquisitions and regional expansions to tap into emerging markets and capitalize on the growing demand for CTMS solutions worldwide. For instance, On 27 September 2023, Emmes, known for its clinical research services and technology solutions, is now utilizing telehealth features of its advantage eClinical platform. Emmes' move of combining these productivity and operating tools under a single strategic plan confirms its commitment to delivering more integrated services and meeting the requirements of the continuously shifting terrain in clinical research.

The report provides a comprehensive analysis of the competitive landscape in the global clinical trial management systems market with detailed profiles of all major companies, including:

- Advarra

- Anju Software

- Clario

- ICON plc

- IQVIA Inc.

- MasterControl Solutions, Inc.

- Medidata

- Mednet

- Oracle

- Parexel International (MA) Corporation

- Pharmaseal

- RealTime Software Solutions, LLC

- Veeva Systems Inc.

Clinical Trial Management Systems Market Recent Developments:

- October 17, 2022: Veeva Systems Inc., the high-tech company supplying cloud- based software solutions for the life sciences sector, signed a strategic agreement with over 40 Contract Research Organizations (CROs). The collaboration sought to deploy a complete trial solutions technology, which is the award-winning Veeva Vault CTMS (Clinical Trial Management System) among others. Through leveraging the experience and operational capabilities of a broad spectrum of CROs with a common goal, Veeva aimed at the increased usage of its state-of-the-art CTMS platform.

- June 27, 2022: Medidata Solutions Inc. (Dassault Systèmes SE), world-renowned vendor of life sciences based in the cloud, has recently introduced clinical operation technologies. These novel products are invented to cope with major needs of these players in clinical trials management and monitoring. Harnessing advanced technologies, such as artificial intelligence and predictive analytics, Medidata strives for better trial performance, improved data quality, and enhanced patient safety. The introduction of these novel technologies underlines Medidate's dedication to innovation in clinical research as well as equipping companies with tools to address the intricacies of drug development of the current time with assuredness.

Clinical Trial Management Systems Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Services |

| Deployment Modes Covered | Web-based CTMS, On-premise, Cloud-based CTMS |

| End Users Covered | Pharmaceutical and Biotechnology Firms, Contract Research Organizations, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Advarra, Anju Software, Clario, ICON plc, IQVIA Inc., MasterControl Solutions, Inc., Medidata, Mednet, Oracle, Parexel International (MA) Corporation, Pharmaseal, RealTime Software Solutions, LLC, Veeva Systems Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the clinical trial management systems market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global clinical trial management systems market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the clinical trial management systems industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Clinical Trial Management Systems Market Report

The global clinical trial management systems market was valued at USD 1,374.0 Million in 2025.

We expect the global clinical trial management systems market to exhibit a CAGR of 8.85% during 2026-2034.

The sudden outbreak of the COVID-19 pandemic has led to the growing prominence of cloud-based CTMS to conduct clinical trials of medical products, which play a vital role in treating the critical coronavirus-infected patients.

The rising prevalence of new infectious and chronic diseases, along with the increasing adoption of advanced diagnostics and drug discovery tools, is primarily driving global clinical trial management systems market.

Based on the component, the global clinical trial management systems market can be categorized into software and services. Currently, software exhibits clear dominance in the market.

Based on the deployment mode, the global clinical trial management systems market has been segmented into web-based CTMS, on-premise, and cloud-based CTMS. Among these, web-based mode currently holds the largest market share.

Based on the end user, the global clinical trial management systems market can be bifurcated into pharmaceutical and biotechnology firms, contract research organizations, and others. Currently, the pharmaceutical and biotechnology firms account for the majority of the total market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global clinical trial management systems market include Advarra, Anju Software, Clario, ICON plc, IQVIA Inc., MasterControl Solutions, Inc., Medidata, Mednet, Oracle, Parexel International (MA) Corporation, Pharmaseal, RealTime Software Solutions, LLC, and Veeva Systems Inc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)