Clinical Nutrition Market Report by Product (Infant Nutrition, Parental Nutrition, Enteral Nutrition), Route of Administration (Oral, Enteral, Parenteral), Application (Cancer, Malnutrition, Metabolic Disorders, Gastrointestinal Disorders, Neurological Disorders, and Others), End User (Pediatric, Adults, Geriatric), and Region 2026-2034

Clinical Nutrition Market Overview:

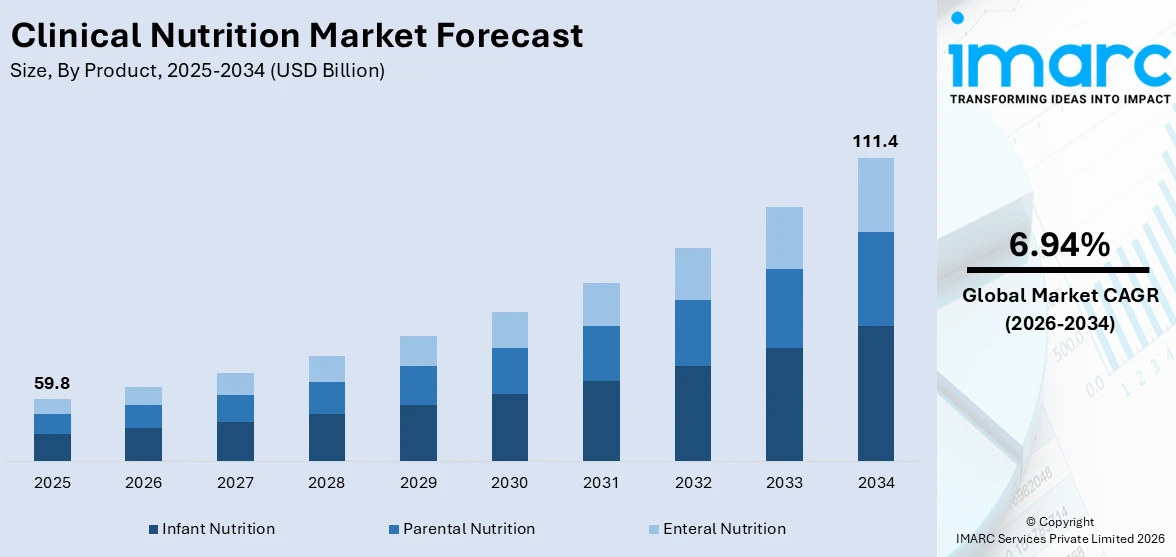

The global clinical nutrition market size reached USD 59.8 Billion in 2025. Looking forward, the market is expected to reach USD 111.4 Billion by 2034, exhibiting a growth rate (CAGR) of 6.94% during 2026-2034. There are various factors that are driving the market, which include increasing prevalence of chronic diseases and aging population worldwide, rising awareness about the importance of nutrition in healthcare, various technological advancements in personalized nutrition and medical nutrition, and changing dietary patterns and lifestyle habits.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 59.8 Billion |

| Market Forecast in 2034 | USD 111.4 Billion |

| Market Growth Rate 2026-2034 | 6.94% |

Clinical Nutrition Market Analysis:

- Major Market Drivers: One of the key market drivers includes collaborations among key players. Moreover, there is an increase in the adoption of functional food products, which is acting as a growth-inducing factor.

- Key Market Trends: The rising geriatric population, along with technological advancements in healthcare, are main trends in the market.

- Geographical Trends: As per the report, Asia Pacific exhibits a clear dominance, accounting for the biggest market share owing to the increasing prevalence of chronic diseases among the masses.

- Competitive Landscape: Numerous players in the clinical nutrition industry are Abbott Laboratories, Ajinomoto Co., Inc., Baxter International Inc., Danone S.A, Fresenius Kabi Ltd, Kate Farms, Medifood, Nestlé Health Science, Perrigo Company plc, Reckitt, among many others.

- Challenges and Opportunities: Regulatory hurdles and the high cost of specialized nutritional products are key market challenges. Nonetheless, the rising focus on personalized nutrition, along with the integration of digital health technologies such as mobile apps, wearable devices, and telemedicine platforms represent clinical nutrition market recent opportunities.

To get more information on this market Request Sample

Clinical Nutrition Market Trends:

Aging Population and Rising Disease Burden

The geriatric individuals are adopting clinical nutrition because they have poor nutrient absorption and slowed metabolism. Furthermore, the need for clinical nutrition is attributed to the rising incidence of chronic illnesses like diabetes, cancer, osteoporosis, and cardiovascular disorders among the masses worldwide. People require specific nutritional therapies as they become older to manage long-term health issues. Clinical nutrition plays a vital role in the management and prevention of disease through the provision of nutritional supplements and medicinal food items. Furthermore, the increasing prevalence of obesity and associated metabolic problems among elderly individuals is bolstering the clinical nutrition market growth. As per the World Health Organization (WHO), the number of people aged 80+ is anticipated to triple by 2050, reaching 426 Million.

Increasing Awareness about the Importance of Nutrition in Healthcare

Healthcare professionals and consumers are recognizing the importance of diet in avoiding and treating illnesses. Healthcare professionals are realizing the importance of evaluating, advising, and intervening in nutrition during clinical practice to improve patient health results. Evidence-based recommendations, assessments of dietary intake, and tools for nutritional screening are crucial in identifying individuals who may be at risk of malnutrition or nutrient deficiencies. Additionally, the increasing need for functional foods, fortified ready-to-drink (RTD) beverages, and personalized nutrition solutions is offering a positive clinical nutrition market outlook. People are consuming food products that provide specific health benefits like immune support, digestive health, and cognitive function. The IMARC Group forecasts that the worldwide RTD beverages market is predicted to surpass US$ 402.0 Billion by 2032.

Technological Advancements in Healthcare

Personalized nutrition and medical nutrition therapy (MNT) are providing individualized solutions to meet nutritional needs and health objectives of each individual. Advancements in technology such as nutrigenomics and metabolomics assist in enabling a deeper understanding of how genetic variations and metabolic pathways influence nutrient metabolism, response to dietary interventions, and susceptibility to chronic diseases. Furthermore, wearable technology, smartphone apps, and digital health platforms offer real time feedback, remote monitoring, and customized coaching. These technological innovations enable individuals to take an active role in managing their health through personalized nutrition and lifestyle modifications, which is catalyzing clinical nutrition demand. On 23 November 2023, FrieslandCampina Ingredients, a global leader in protein and prebiotics, launched Nutri Whey™ ProHeat, a heat-stable whey protein designed for the medical nutrition market. By using the latest microparticulation technology, FrieslandCampina Ingredients created a highly heat-stable whey protein ingredient.

Changing Dietary Patterns and Nutritional Needs

Changing dietary patterns, lifestyle habits, and socioeconomic factors are influencing nutritional needs of individuals. Furthermore, changing lifestyles like sedentary behavior, irregular meal patterns, and high-stress levels, impact nutrient requirements and metabolism, which is increasing the chances of malnutrition, micronutrient deficiencies, and metabolic disorders. Moreover, inadequate intake of essential nutrients, coupled with excessive calorie consumption and nutrient-poor food choices, leads to nutritional imbalances and poor health outcomes. In addition, the rising prevalence of obesity, cancer, diabetes, cardiovascular disease, and other diet-related chronic conditions, necessitates interventions to promote healthier eating habits and improve nutritional status. Over 35 million new cancer cases are expected to occur in 2050, as per the World Health Organization (WHO).

Clinical Nutrition Market Segmentation:

IMARC Group provides an analysis of the key clinical nutrition market trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product, route of administration, application, and end user.

Breakup by Product:

- Infant Nutrition

- Parental Nutrition

- Enteral Nutrition

Infant nutrition accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product. This includes infant nutrition, parental nutrition, and enteral nutrition. According to the report, infant nutrition represented the largest segment.

Infant nutrition addresses the dietary requirements of newborns and infants in the early stages of their development. Breast milk offers a special combination of nutrients, bioactive substances, and antibodies that promote healthy growth, development, and immune system function, which is crucial for an infant's nutrition. On the other hand, infant formula is an ideal substitute as it provides all vital nutrients like proteins, carbs, fats, vitamins, and minerals that a child needs to grow and develop.

Breakup by Route of Administration:

- Oral

- Enteral

- Parenteral

Oral holds the largest share of the industry

A detailed breakup and analysis of the market based on the route of administration have also been provided in the report. This includes oral, enteral, and parenteral. According to the report, oral accounted for the largest market share.

Oral nutritional items are dietary supplements, functional foods, over the counter (OTC) pharmaceuticals, and oral nutritional supplements (ONS). They come in a variety of formats including liquids, powders, capsules, tablets, and bars, making them easily accessible and convenient for people with a range of dietary requirements. These products provide vital nutrients, vitamins, minerals, and macronutrients to support general health, fulfill dietary needs, and treat particular nutritional deficiencies.

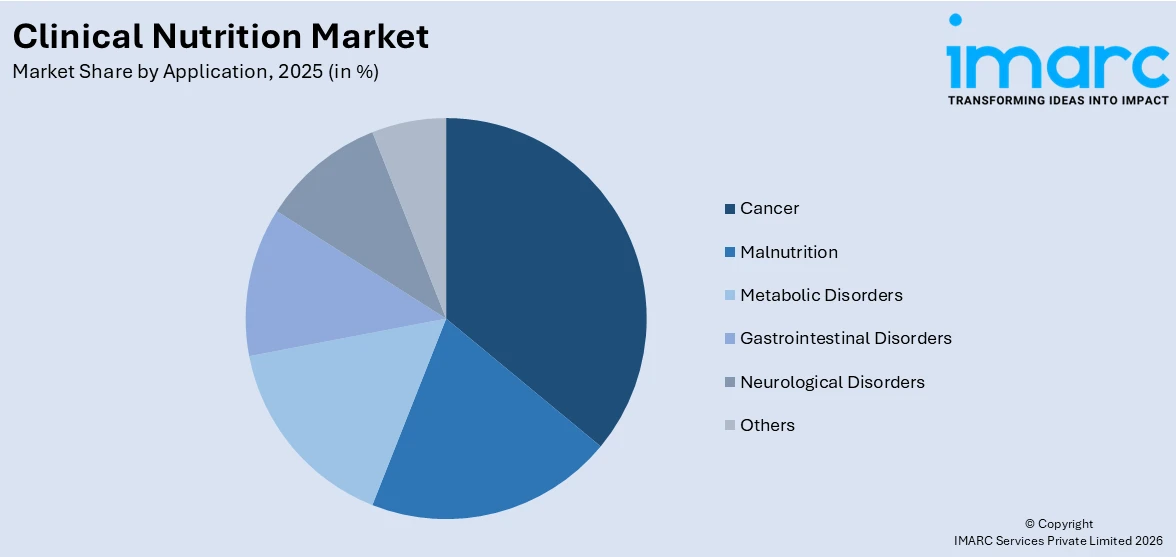

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Cancer

- Malnutrition

- Metabolic Disorders

- Gastrointestinal Disorders

- Neurological Disorders

- Others

The report has provided a detailed breakup and analysis of the market based on the application. This includes cancer, malnutrition, metabolic disorders, gastrointestinal disorders, neurological disorders, and others.

Cancer and its treatments such as chemotherapy, radiation therapy, and surgery can significantly impact the nutritional status of a patient by causing appetite loss, nausea, vomiting, taste alterations, and metabolic changes. Malnutrition is prevalent among cancer patients, leading to compromised immune function, impaired wound healing, muscle wasting, and decreased quality of life. Clinical nutrition interventions for cancer patients focus on providing adequate energy, protein, vitamins, minerals, and fluids to support the nutritional status of patients.

Malnutrition encompasses various conditions characterized by inadequate intake or absorption of nutrients, leading to nutrient deficiencies, weight loss, muscle wasting, and impaired immune function. Malnutrition can result from underlying medical conditions such as gastrointestinal disorders, chronic diseases, infections, trauma, or surgical procedures, as well as factors like aging, social isolation, and economic insecurity. Clinical nutrition interventions for malnutrition aim to address nutrient deficiencies, restore energy balance, promote weight gain, and improve overall nutritional status, thereby influencing the clinical nutrition market revenue.

Metabolic disorders are characterized by abnormalities in energy metabolism, hormone regulation, nutrient utilization, or enzyme function. Clinical nutrition plays a pivotal role in managing metabolic disorders by optimizing dietary patterns, controlling blood glucose levels, managing body weight, and reducing cardiovascular risk factors. Nutrition therapy for metabolic disorders emphasizes balanced macronutrient intake, portion control, carbohydrate counting, glycemic index management, and dietary fiber consumption to achieve glycemic control.

Breakup by End User:

- Pediatric

- Adults

- Geriatric

Pediatric exhibits a clear dominance in the market

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes pediatric, adults, and geriatric. According to the report, pediatric accounted for the largest market share.

As per the United Nations Children's Fund (UNICEF), there were approximately 2,397,435,502 people under age 18 in 2023 across the globe. The pediatric segment represents a critical demographic with unique nutritional needs and health considerations. Clinical nutrition plays a pivotal role in supporting growth, development, and overall health during critical stages of life. For infants, breastfeeding and formula feeding provide essential nutrients crucial for optimal growth and development, while specialized infant formulas cater to specific dietary requirements for infants with allergies, intolerances, or medical conditions. Pediatric clinical nutrition focuses on promoting balanced diets, addressing nutrient deficiencies, and preventing childhood obesity and related health problems.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the largest clinical nutrition market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for clinical nutrition.

Rapid urbanization, changing dietary habits, and a rising burden of chronic diseases in the Asia Pacific region are impelling the market growth. Moreover, inflating income levels of individuals and expanding healthcare access contribute to the growing demand for clinical nutrition products and services in the region. Besides this, varying nutritional needs and cultural preferences are creating opportunities for customized nutritional solutions tailored to specific demographics and healthcare needs. Furthermore, the rising geriatric population, particularly in India and China, is bolstering the market growth. According to the United Nations Fund for Population Activities (UNFPA), the population of people aged 80+ years will grow at a rate of around 279% between 2022 and 2050 in India.

Competitive Landscape:

Clinical nutrition companies are undertaking strategic initiatives to maintain and expand their market share. These companies are focusing on research and development (R&D) activities to innovate new products and formulations that address evolving healthcare needs such as personalized nutrition solutions and functional foods targeting specific health conditions. Additionally, they are engaging in strategic partnerships, acquisitions, and collaborations to enhance their product portfolios, expand their geographic presence, access new markets, and increase their revenue. Apart from this, they are focusing on marketing efforts and the introduction to enhance the efficacy, safety, and value proposition of their products. On 25 January 2023, Nutricia launched its first plant based, RTD, oral nutritional supplement, Fortimel® PlantBased Energy, specifically formulated to meet the nutritional needs of people who are malnourished or at risk of malnutrition due to illness. It is nutritionally complete, with a blend of high-quality plant protein made from pea and soy sources 3,4,5, and is suitable for vegan, vegetarian, or flexitarian diets as well as for patients with cow milk protein allergy.

The report provides a comprehensive analysis of the competitive landscape in the global clinical nutrition market with detailed profiles of all major companies, including:

- Abbott Laboratories

- Ajinomoto Co., Inc.

- Baxter International Inc.

- Danone S.A

- Fresenius Kabi Ltd

- Kate Farms

- Medifood

- Nestlé Health Science

- Perrigo Company plc

- Reckitt

Clinical Nutrition Market Recent Developments:

- 16 February 2023: Nestlé Health Science and EraCal Therapeutics Ltd. announced that they entered a research collaboration aiming to identify novel nutraceuticals relevant to control food intake. The joint program combines Nestle’s unique nutraceutical resources with EraCal’s differentiated drug discovery platform. These synergies aim to provide a new paradigm for first-line nutraceuticals for people suffering from metabolic diseases.

- 3 May 2024: Danone completed the acquisition of Functional Formularies, a leading whole foods tube feeding business in the US, from Swander Pace Capital. As part of the Renew Danone strategy, this acquisition strengthens Danone’s Medical Nutrition portfolio in the US by further expanding its enteral tube feeding ranges.

Clinical Nutrition Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Infant Nutrition, Parental Nutrition, Enteral Nutrition |

| Route of Administration Covered | Oral, Enteral, Parenteral |

| Applications Covered | Cancer, Malnutrition, Metabolic Disorders, Gastrointestinal Disorders, Neurological Disorders, Others |

| End Users Covered | Pediatric, Adults, Geriatric |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, Ajinomoto Co., Inc., Baxter International Inc., Danone S.A, Fresenius Kabi Ltd, Kate Farms, Medifood, Nestlé Health Science, Perrigo Company plc, Reckitt, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, clinical nutrition market forecasts, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global clinical nutrition market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the clinical nutrition industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key companies.

Frequently Asked Questions About the Clinical Nutrition Market Report

The global clinical nutrition market was valued at USD 59.8 Billion in 2025.

We expect the global clinical nutrition market to exhibit a CAGR of 6.94% during 2026-2034.

The rising popularity of clinical nutrition, as it assists in reducing the consequences of malnutrition, enhancing the response to disease treatment, boosting immunity levels, etc., is primarily driving the global clinical nutrition market.

The sudden outbreak of the COVID-19 pandemic has led to the increasing demand for immunity-boosting alternatives, including clinical nutrition, to prevent the risk of the coronavirus infection.

Based on the product, the global clinical nutrition market can be categorized into infant nutrition, parental nutrition, and enteral nutrition. Currently, infant nutrition holds the majority of the total market share.

Based on the route of administration, the global clinical nutrition market has been segregated into oral, enteral, and parenteral. Among these, oral currently exhibits a clear dominance in the market.

Based on the end user, the global clinical nutrition market can be bifurcated into pediatric, adults, and geriatric. Currently, pediatric accounts for the largest market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where Asia-Pacific currently dominates the global market.

Some of the major players in the global clinical nutrition market include Abbott Laboratories, Ajinomoto Co., Inc., Baxter International Inc., Danone S.A, Fresenius Kabi Ltd, Kate Farms, Medifood, Nestlé Health Science, Perrigo Company plc, and Reckitt.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)