China Two Wheeler Market Size, Share, Trends and Forecast by Type, Propulsion Type, End User, Distribution Channel, and Region 2026-2034

China Two Wheeler Market Size, Share, Trends & Forecast (2026-2034)

The China two wheeler market was valued at USD 23.55 Billion in 2025 and is projected to reach USD 30.50 Billion by 2034, expanding at a CAGR of 2.92% during 2026-2034. Growth is driven by GB 17761-2024 electric bicycle standard enforcement, accelerating the EV quality upgrade cycle, e-commerce delivery platform fleet expansion, creating commercial EV scooter demand, and rising urban congestion driving last-mile two-wheeler adoption. Scooters dominate the type at 61.8%, electric propulsion leads at 56.4%, and East China commands 29.8% of the regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 23.55 Billion |

|

Forecast Market Size (2034) |

USD 30.50 Billion |

|

CAGR (2026-2034) |

2.92% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

East China (29.8%, 2025) |

|

Fastest Growing Region |

Southwest China (~3.8% CAGR) |

The China two wheeler market grew steadily from USD 20.40 Billion in 2020 to USD 23.55 Billion in 2025, sustained through COVID-19’s disruption and China’s subsequent economic recovery. Anchored at USD 27.19 Billion in 2030, the forecast to USD 30.50 Billion by 2034 reflects a mature market’s stable progression driven by electrification upgrade cycles, premium model premiumization, and urban commuter mobility demand.

To get more information on this market, Request Sample

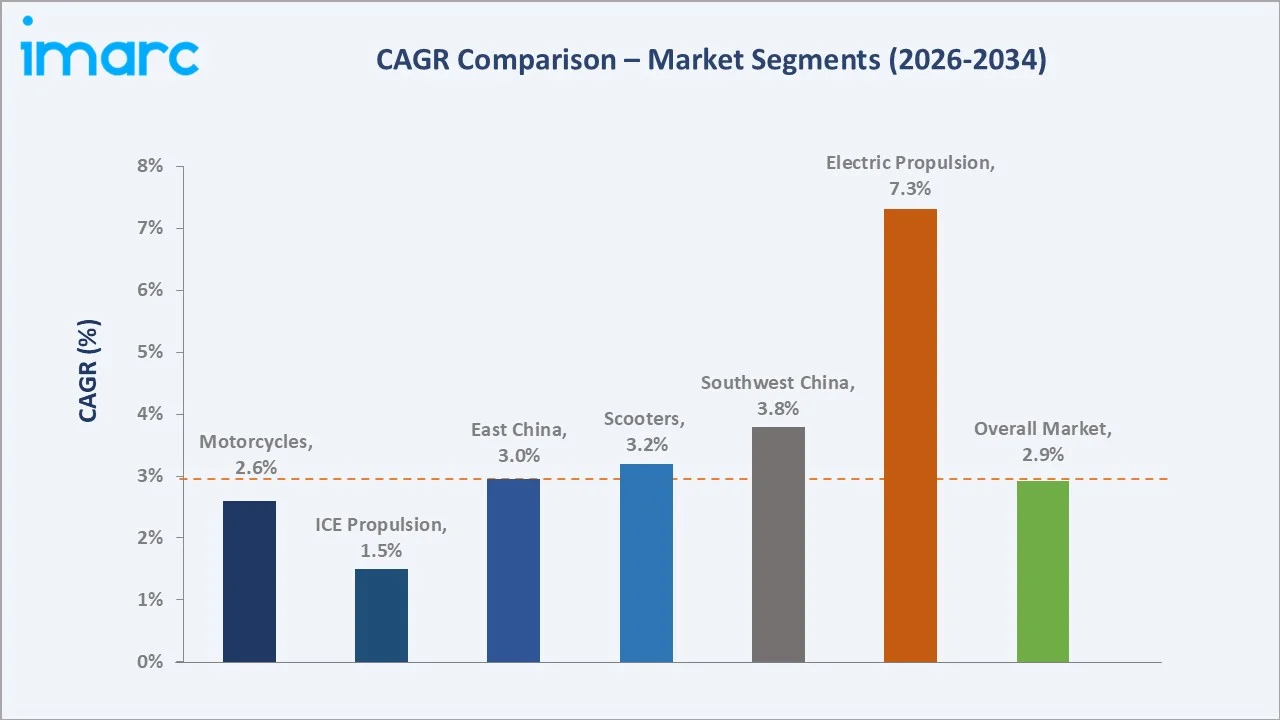

The CAGR across key segments with electric propulsion at ~7.31% CAGR grows fastest, reflecting China’s structural transition from ICE to electric two-wheelers driven by emission zone restrictions, the Li-ion battery cost curve decline, and sodium-ion battery commercialization reducing range anxiety. Southwest China, at ~3.8% CAGR, grows fastest regionally as infrastructure investment opens mountainous terrain to electric mobility.

Executive Summary

The China two wheeler market expanded from USD 20.40 Billion in 2020 to USD 23.55 Billion in 2025, sustained by one of the world’s most structurally unique two-wheeler market dynamics: China’s simultaneous status as the world’s largest two-wheeler production market and the world’s fastest-transitioning EV two-wheeler ecosystem. China’s 300 million e-bikes constitute the largest national electric mobility fleet of any vehicle type, representing an EV transition scale that no other country’s transport sector has achieved.

Scooters lead at 61.8% as China’s overwhelmingly dominant urban two-wheeler format, serving daily urban commuters and over 200 million gig delivery workers whose EV scooter adoption is the market’s fastest structural volume driver. Electric propulsion surpassed ICE at 56.4%, a historic inflection point achieved through the combination of GB 17761-2024 quality standard enforcement that raised EV product quality to consumer confidence levels, sustained cost advantage, and government EV subsidy programs that reduced EV premium. East China’s 29.8% reflects the world’s most concentrated EV two-wheeler manufacturing cluster in Jiangsu and Zhejiang, combined with the region’s e-commerce delivery fleet density.

Key Market Insights

|

Insight |

Data |

|

Dominant Vehicle Type |

Scooters – 61.8% revenue share (2025) |

|

Dominant Propulsion |

Electric – 56.4% revenue share (2025) |

|

Leading Region |

East China – 29.8% share (2025) |

|

Fastest Growing Region |

Southwest China (~3.8% CAGR) |

Key Analytical Observations Supporting the Above Data:

- Scooters at 61.8% reflecting China’s urban mobility infrastructure alignment: China’s 1.4 billion population with rising urbanization and online delivery options makes e-scooters the most pragmatic door-to-door transport option in China’s dense urban street grid.

- Electric at 56.4%, having crossed the majority threshold in 2024–2025: China has 300+ million e-bikes. China’s electric two-wheeler market reached the majority threshold earlier than any global government’s EV target timeline.

- East China at 29.8% as dual manufacturing-consumption epicentre: Jiangsu Province alone produces a high proportion of China’s EV two-wheelers and simultaneously contains high consumers who are adopting EV scooters at China’s highest penetration rate.

China Two Wheeler Market Overview

China’s two-wheeler market encompasses electric scooters, ICE motorcycles, and ICE scooters. The market serves China’s registered two-wheeler operators across three primary use cases: personal urban commuting, commercial last-mile delivery, and rural/agricultural transport. China’s two-wheeler market’s unique structural characteristic versus global peers is its pre-completed EV transition in the scooter segment: while Europe and North America debate EV scooter adoption timelines, China has already achieved majority-electric status, a structural leadership position creating export opportunity for China’s EV two-wheeler technology and manufacturing to the rest of the world.

Regulatory framework: GB 17761-2024 is the market’s single most consequential regulatory event of the decade, establishing a mandatory speed limit, weight limit, voltage limit, and compulsory pedal feature for all electric bicycles sold in China. MIIT’s electric bicycle national standard update is expected to increase the speed limit to 30 km/h for a new “electric moped” category, expanding the addressable market for EV scooter manufacturers who have been range- and speed-constrained by the current standard.

Market Dynamics

To evaluate market opportunities, Request Sample

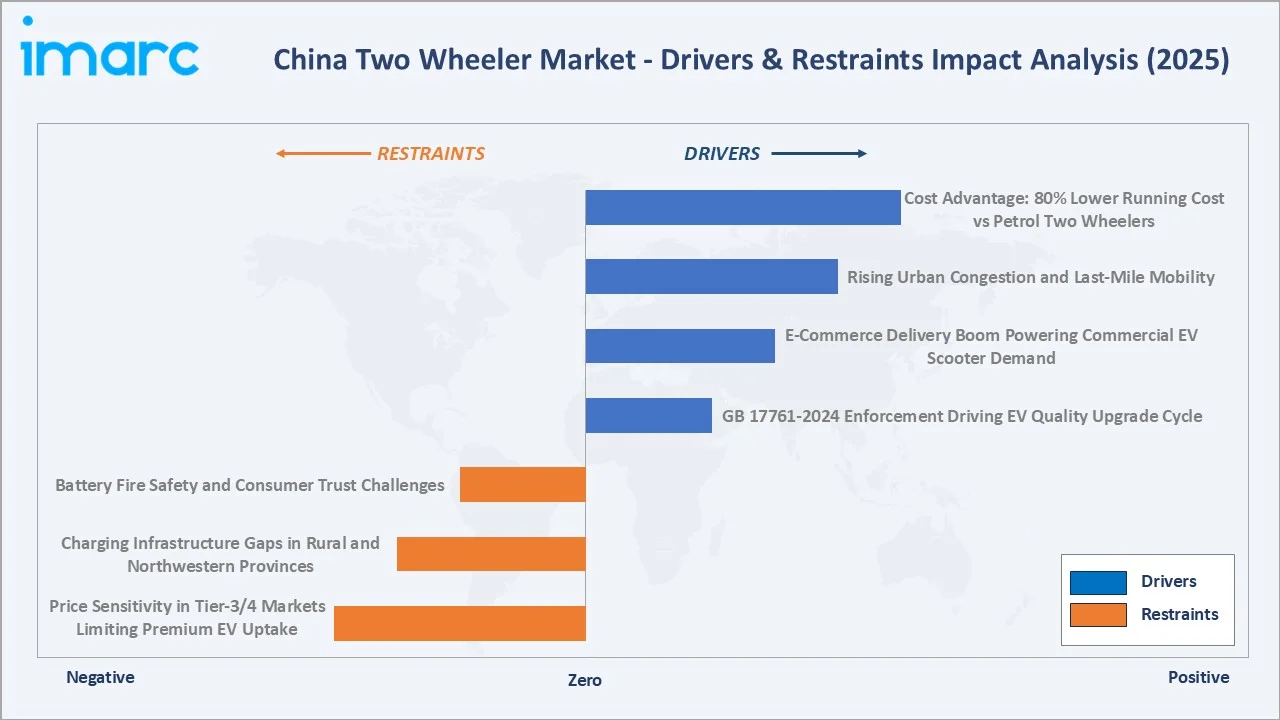

Market Drivers

- GB 17761-2024 Enforcement Driving EV Quality Upgrade Cycle: The mandatory retirement of non-compliant pre-standard electric bicycles across China’s e-bike fleet is creating China’s most significant two-wheeler replacement cycle in history.

- E-Commerce Delivery Boom Powering Commercial EV Scooter Demand: China’s e-commerce and food delivery platforms have collectively deployed the world’s largest commercial EV scooter fleet, generating collective EV scooter procurement.

- Rising Urban Congestion and Last-Mile Mobility: China’s urbanization rate will reach 67.8% by 2030. China’s cities face an average commute time of 43 minutes one-way, where two-wheeler commuting delivers 15‐30-minute time savings versus public transport plus walking for door-to-door urban trips under 15 km.

- Cost Advantage: 80% Lower Running Cost vs Petrol Two Wheelers: The current gasoline price in China is CNY 9.56 per liter creates a 4–5× per-kilometer fuel cost disadvantage for ICE scooters versus EV equivalents. For a delivery worker covering 80–120 km daily, the annual fuel savings make EV scooter adoption economically compelling as a livelihood improvement decision rather than a lifestyle choice.

Market Restraints

- Price Sensitivity in Tier-3/4 Markets Limiting Premium EV Uptake: While China’s tier-1 and tier-2 cities have largely completed the transition to lithium-battery compliant EV scooters, China’s county-level cities and rural areas remain price-sensitive in their two-wheeler purchase decisions.

- Charging Infrastructure Gaps in Rural and Northwestern Provinces: Northwest China’s EV charging infrastructure density is 8‐12× lower than East China’s Jiangsu and Zhejiang provinces, creating range anxiety barriers for EV scooter adoption in Xinjiang, Gansu, Qinghai, and rural Shaanxi, where round-trip commute distances of 30‐60 km exceed single-charge range without charging infrastructure at destination.

Market Opportunities

- China as Global EV Two-Wheeler Export Platform: In China, the cumulative exports of electric two-wheeler reached $2.65 billion from January to May 2025. China’s EV two-wheeler industry’s cost and technology maturity create a structural export opportunity that is just beginning to be realized at scale.

- GB 17761 Revision: New Electric Moped Category: MIIT’s anticipated revision to GB 17761 proposes a new “electric moped” category with 30‐45 km/h maximum speed, 75 kg weight limit, and 60V battery maximum.

Market Challenges

- Battery Fire Safety and Consumer Trust: China recorded 640 electric vehicle fire accidents in Q1 2022. The GB17761-2018 standard’s battery safety requirements and local government apartment building EV charging ban enforcement create conflicting regulatory pressures, where governments simultaneously mandate electric two-wheeler adoption and restrict the most accessible charging locations, creating range anxiety and consumer purchasing hesitation that slows the premium electric segment’s growth potential.

- Rural Market Infrastructure Gap Limiting Nationwide Electrification: Despite urban China’s electric propulsion penetration, rural China’s electric two-wheeler penetration remains significantly lower due to charging infrastructure gaps, distance requirements exceeding current electric range capabilities on single charges, and consumer price sensitivity in rural markets.

Emerging Market Trends

1. China’s Premium Motorcycle Renaissance: Domestic Brands vs. Japanese Incumbents

China’s premium motorcycle segment is experiencing a structural disruption as domestic brands achieve product quality parity at 30‐50% lower price points, systematically displacing Japanese and European brands in China’s growing performance motorcycle enthusiast community.

2. Electric Motorcycle Performance Category Emergence

China’s first generation of commercially viable electric performance motorcycles represents a product category that merges the premium motorcycle enthusiast audience with China’s EV technology leadership. These electric performance motorcycles compete with other brands on performance metrics while delivering near-zero running cost and eliminating urban ICE motorcycle ban exemptions.

3. Export Market: China EV Two-Wheeler Brands Going Global

Chinese cumulative exports of electric two-wheeler reached $2.65 billion from January to May 2025, increased 21.7% year-on-year. China’s EV two-wheeler industry is executing the most consequential automotive export expansion strategy of any EV category globally for China’s EV two-wheeler manufacturers.

4. Smart City Integration: E-Scooters as Connected Mobility Nodes

China’s smart city initiatives are progressively integrating e-scooters as connected mobility nodes within the urban traffic management ecosystem. MIIT’s national electric bicycle IoT standard will mandate GPS, speed sensor, and cellular connectivity in all new-standard electric bicycles, transforming China’s new EV scooter registrations into a connected urban mobility data asset that smart city platform operators are positioning to monetize.

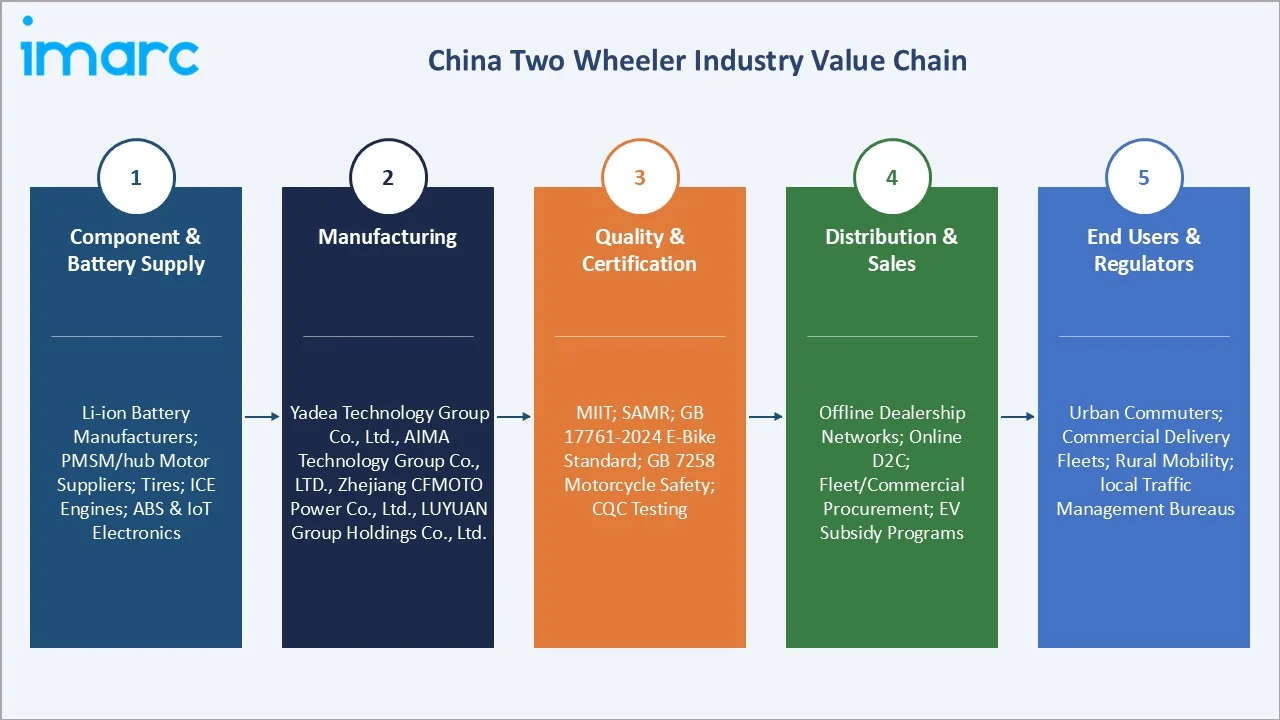

Industry Value Chain Analysis

China’s two-wheeler value chain integrates lithium battery and PMSM motor component supply, OEM manufacturing, quality certification, multi-channel distribution, charging/swapping infrastructure, and end-user fleet operations.

|

Stage |

Key Participants |

|

Component & Battery Supply |

Lithium-ion battery manufacturers; PMSM/hub motor suppliers; tires; ICE engines; ABS braking systems; electronics/IoT |

|

Manufacturing |

Yadea Technology Group Co., Ltd., AIMA TECHNOLOGY GROUP CO., LTD., Zhejiang CFMOTO Power Co., Ltd., and LUYUAN Group Holdings Co., Ltd. |

|

Quality & Certification |

MIIT (Ministry of Industry and Information Technology); SAMR (State Administration for Market Regulation); GB 17761-2024 electric bicycle standard mandatory compliance for e-bikes; GB 7258 motor vehicle safety technical conditions for motorcycles; China Quality Certification Centre (CQC) testing |

|

Distribution & Sales |

Offline dealership networks; Online direct-to-consumer; fleet/commercial procurement; local government EV subsidy programs directing purchases through provincial dealers |

|

End Users & Regulators |

Urban personal commuters; Commercial delivery fleet; rural mobility; local traffic management bureaus |

Two-wheeler OEMs capture 20‐30% gross margin on branded EV scooters versus 12‐18% on mass-market ICE motorcycles and entry-level EV scooters. The battery and motor supply chain represents 35‐45% of EV scooter manufacturing cost, with battery costs declining 8‐12% annually through scale and LFP chemistry optimization. Distribution captures 18‐25% retail margin for offline dealers and 12‐18% for online/direct channels. The highest-margin value chain position is battery swapping infrastructure, where per-swap economics provide 40‐55% gross margin on energy and battery lease revenue independent of hardware sale margin.

Technology Landscape in the China Two Wheeler Industry

LFP vs. NMC Battery Chemistry Transition

China’s EV scooter battery chemistry is completing a transition from NMC (Nickel Manganese Cobalt) to LFP (Lithium Iron Phosphate): LFP’s advantages in thermal safety, cycle life, and lower cell cost make it the optimal chemistry for Chinese e-scooters’ daily cycle use case.

IoT Connectivity and Smart Two-Wheeler Ecosystem

China’s four leading EV scooter platforms, Ninebot App, Yadea App, Aima App, and Hello App (battery swapping), collectively serve China’s registered users, creating the largest consumer IoT connected vehicle ecosystem for any two-wheeler platform.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Scooters | 61.8% | 2025 |

| Propulsion Type | Electric | 56.4% | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Distribution Channel | 🔒 | 🔒 | 2025 |

| Region | East China | 29.8% | 2025 |

By Type

To access detailed market analysis, Request Sample

Scooters lead at 61.8% as China’s structurally dominant urban mobility two-wheeler. China’s scooter market encompasses electric bicycles, electric scooters above standard, and ICE scooters. Motorcycles at 38.2% serve four distinct segments: mass-market commuter/utility; mid-class leisure; premium performance; and electric motorcycle.

By Propulsion Type

Electric leads at 56.4%. Electric’s market value majority reflects both unit dominance in the scooter category and rapid value share growth from the premium EV scooter and electric motorcycle product launch. The electric propulsion segment reflects the scooter market’s continuation of ICE-to-electric conversion, the electric motorcycle segment’s rapid growth from a low base, and the ASP premium that technology-enabled EV products command versus commodity ICE equivalents.

ICE at 43.6% is declining in scooters but sustaining at a high share in the motorcycle category. ICE’s resilience in the motorcycle segment reflects the fundamental range, power density, and refueling speed advantages of ICE for long-distance touring, agricultural utility, and export market requirements where electric infrastructure does not yet exist.

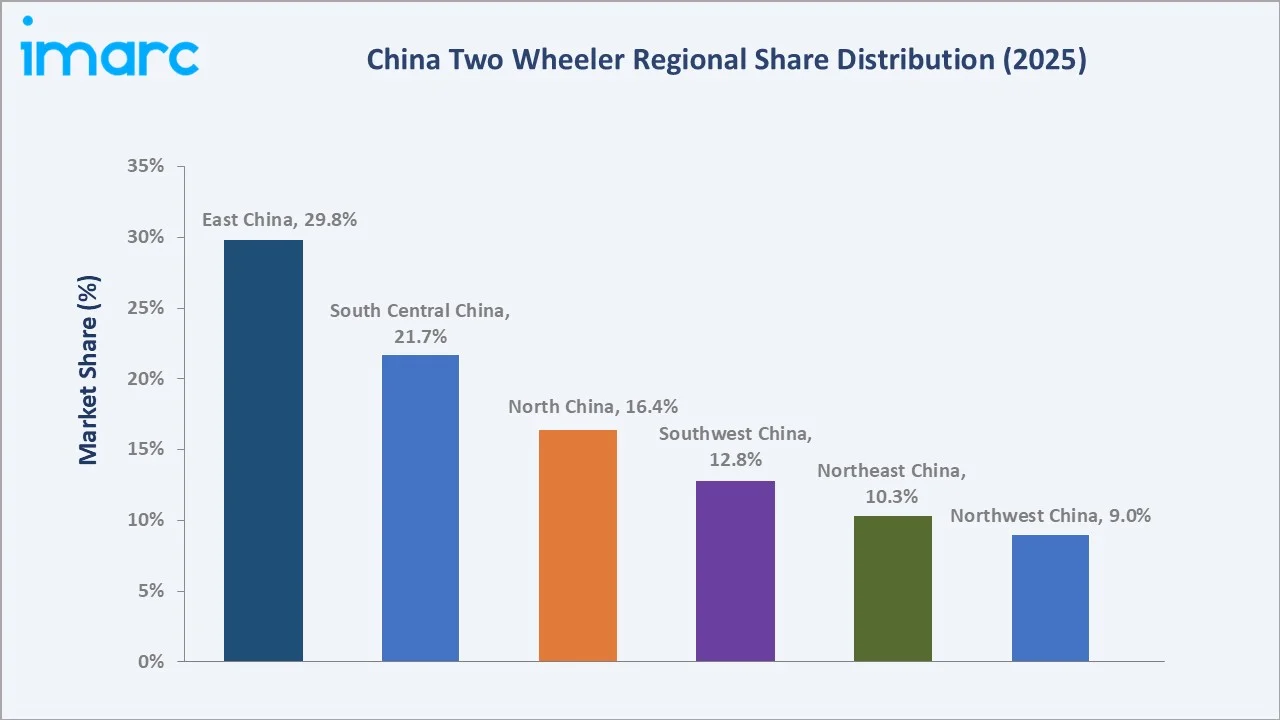

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

East China |

29.8% |

East China collectively represent China’s most densely populated and economically advanced mega-region, generating the highest per-capita two-wheeler demand intensity nationally |

|

South Central China |

21.7% |

South Central China collectively represent China’s second most important two-wheeler market, with Guangdong as South Central’s economic anchor |

|

North China |

16.4% |

North China’s highest demand for premium EV scooters, driven by stringent air quality regulations mandating a transition from petrol-powered motorcycles to electric two-wheelers |

|

Southwest China |

12.8% |

Southwest China hosting companies with motorcycle manufacturers generating high annual motorcycle production value |

|

Northeast China |

10.3% |

Northeast China is generating large working-class commuter EV scooter demand as traditional heavy industry workers transition to lighter urban service sector employment requiring flexible two-wheeler commuting |

|

Northwest China |

9.0% |

Northwest China is China’s most sparsely populated region, with the lowest per-capita two-wheeler market penetration |

East China’s 29.8% dominance is structurally reinforced by Jiangsu and Zhejiang’s dual role as China’s largest EV two-wheeler manufacturing and consumption provinces simultaneously. East China’s average EV scooter ASP is above the national average, reflecting the region’s higher income levels and stronger preference for premium lithium-battery products.

South Central China’s 21.7%, with Guangdong’s warm year-round climate and Pearl River Delta’s delivery worker density, creates South Central’s structural advantage as China’s highest-intensity commercial EV scooter usage region. Southwest China’s 12.8%, with Chongqing’s motorcycle manufacturing heritage, creates the only Chinese region where ICE motorcycles remain the growth segment rather than EV scooters.

Competitive Landscape

China’s two-wheeler market exhibits high concentration in the EV scooter segment and moderate concentration in the motorcycle segment.

|

Company Name |

Product Line |

Market Position |

Core Strength |

|

Yadea Technology Group Co., Ltd. |

Electric Motorcycles (Kemper, Keeness), Electric Scooters (YADEA GS80, YADEA T5L, YADEA VEKOO, YADEA Cooljoy, Orla, VoltGuard, Fierider, YADEA VELAX, YADEA GS70, YADEA OSTA, YADEA OVA), Electric Bicycle (TROOPER-01 PLUS) |

Market Leader |

Yadea is one of the largest electric two-wheeler companies with cumulative sales of electric two-wheelers |

|

AIMA TECHNOLOGY GROUP CO., LTD. |

AIMA Luna, AIMA Tiger X6 Pro, AIMA HyHawk, AIMA Big Sur, AIMA CargoE Pro |

Market Leader |

Aima is one of China’s largest EV two-wheeler companies by units |

|

Zhejiang CFMOTO Power Co., Ltd. |

250CL-C, 450CL-C, 450CL-C BOBBER, 450CL-C AMT, 450MT, 700MT, 800MT SPORT, 800MT EXPLORE, 800MT-X, 1000MT-X, 125NK, 250NK, 300NK, 450NK, 675NK, 800NK, 250SR, 300SR, 450SR, 450SR-S, 500SR VOOM, 675SR-R, 750SR-S, XO PAPIO RACER, XO PAPIO TRAIL |

Strong Challenger |

CFMoto is China’s leading premium motorcycle manufacturer. CFMoto’s premium positioning demonstrates China’s domestic motorcycle industry’s maturation. |

|

LUYUAN Group Holdings Co., Ltd. |

E-Scooters (S95, S90, MNK6, MQN7, MKK, S75, S70, ZQQ2, MODA6, DM 01), E-Bikes (G01, EB-S1E, EB-S1, EB-S2, EB-2M, EB-2C, EB-E3, EB-1M, FB-03), E-Kick Scooter (KS 01) |

Established |

Luyuan is one of China’s largest EV two-wheeler companies by units. Luyuan’s competitive positioning emphasizes battery technology leadership |

The competitive structure is evolving as domestic brands displace Japanese incumbents in the premium motorcycle segment through a combination of localized product development, competitive pricing, and digital-native marketing that connects with China’s motorcycle enthusiast community.

Key Company Profiles

Yadea Technology Group Co., Ltd.

Yadea is one of the largest electric two-wheeler companies by annual units and is the uncontested leader of China’s EV scooter market.

- Product Portfolio: Electric Motorcycles (Kemper, Keeness), Electric Scooters (YADEA GS80, YADEA T5L, YADEA VEKOO, YADEA Cooljoy, Orla, VoltGuard, Fierider, YADEA VELAX, YADEA GS70, YADEA OSTA, YADEA OVA), Electric Bicycle (TROOPER-01 PLUS).

- Recent Developments: In January 2025, Yadea hosted a launch event in Hangzhou, China, to unveil its latest electric two-wheeler and showcased the brand's new sodium battery technology.

- Strategic Focus: Premium brand elevation targeting average selling price uplift through technology premiumization; Smart city integration through Yadea IoT platform connecting as a model for national smart city e-scooter integration.

Zhejiang CFMOTO Power Co., Ltd.

CFMOTO is China’s most internationally credible motorcycle brand, achieving a domestic-to-premium positioning.

- Product Portfolio: 250CL-C, 450CL-C, 450CL-C BOBBER, 450CL-C AMT, 450MT, 700MT, 800MT SPORT, 800MT EXPLORE, 800MT-X, 1000MT-X, 125NK, 250NK, 300NK, 450NK, 675NK, 800NK, 250SR, 300SR, 450SR, 450SR-S, 500SR VOOM, 675SR-R, 750SR-S, XO PAPIO RACER, XO PAPIO TRAIL.

- Recent Developments: In May 2023, CFMOTO unveiled six exciting new models, including the 1250TR-G MY 2023, 800MT EXPLORE Edition, XO PAPIO TRAIL, 450SR S, 450NK, and 450CL-C, spanning five key series: SR, NK, PAPIO, MT, and TR-G. Additionally, CFMOTO introduced its new CL-C series (Classic Cruiser).

- Strategic Focus: 450SR series expansion into Southeast Asia.

Market Concentration Analysis

China’s EV scooter segment is highly concentrated: Yadea (32‐35% volume share) + AIMA (18‐20%) + Luyuan (12‐14%) + CFMOTO (5–6%) collectively represent 68‐75% of China’s annual new EV scooter registrations, with the top-3 alone commanding more combined volume than all remaining 350+ compliant manufacturers combined. This concentration emerged from GB 17761-2024’s enforcement, eliminating sub-standard manufacturers and Yadea/Aima’s scale-driven cost advantages that reinforce market leadership.

The motorcycle segment is less concentrated. Market concentration is increasing in the premium motorcycle segment as CFMoto captures share from Japanese incumbents, while consolidating further in the mass-market motorcycle segment as smaller manufacturers exit amid thinner margins and rising quality compliance costs.

Investment & Growth Opportunities

Fastest Growing Segments

Electric propulsion (~7.3% CAGR), East China region (~2.9% CAGR), premium motorcycle segment (~15‐20% CAGR), battery swapping infrastructure (~25‐30% CAGR), and electric motorcycle (~35‐40% CAGR from small base) represent China’s two-wheeler market’s highest-growth investment vectors.

Investment Themes

Listed equity access: Yadea, AIMA, Luyuan, CFMOTO; private investment: battery swapping infrastructure, electric motorcycle startups, IoT smart two-wheeler platform, solid-state battery technology for EV two-wheelers.

- Technology investment themes: Sodium-ion battery cells for entry EV scooter; solid-state battery pilot for premium electric scooter/motorcycle; hub motor integration with ABS and regenerative braking; smart city IoT connectivity module; cold-weather LFP battery system for Northeast and Northwest China EV adoption acceleration.

- Export market investment: Southeast Asia EV two-wheeler distribution partnerships; African utility EV scooter for gig economy delivery; EU L1e-B certified Chinese EV scooter import.

Future Market Outlook (2026-2034)

The China two-wheeler market is entering a decade of structured value transformation rather than dramatic volume expansion. From USD 23.55 Billion in 2025, the market will reach USD 30.50 Billion by 2034 at a 2.92% CAGR, a moderate growth rate that masks profound structural changes in the market’s composition, technology content, and competitive dynamics. The 2.92% CAGR is not an indicator of market weakness but of market maturity: China’s two-wheeler penetration has already achieved very high saturation in urban and semi-urban markets, meaning growth derives from premiumization rather than fleet expansion.

Three structural forces will define this value transformation: the completion of China’s electric scooter transition, driven by the GB 17761-2024 compliance deadline enforcement forcing pre-standard e-bike replacements, the continued decline in LFP battery costs and commercial delivery platform electrification mandates; the emergence of China’s domestic premium motorcycle industry as a genuinely globally competitive sector; and China’s EV two-wheeler export transformation from domestic-consumption market to global supply platform, where Yadea’s annual export target (2030), Aima’s Southeast Asia JV strategy, and CFMoto ZEEHO’s European electric motorcycle homologation collectively establish China as the world’s default EV two-wheeler supplier to emerging markets undergoing their own electric transition.

Research Methodology

Primary Research

Primary research included 115+ structured interviews with China two-wheeler industry stakeholders in 2025, comprising EV scooter OEM commercial directors, market intelligence officers, delivery platform fleet procurement managers, MIIT two-wheeler standardization office, CAAM (China Association of Automobile Manufacturers) two-wheeler segment analysts, and battery swap network operators.

Secondary Research

Secondary research encompassed MIIT electric bicycle product announcement registration data, CAAM China two-wheeler production and sales monthly statistics, SAMR CCC certification two-wheeler product registry, GACC China motorcycle and e-bike export customs data, company annual reports, provincial traffic management bureau two-wheeler registration statistics, IMARC automotive intelligence database, and China EV Two-Wheeler Industry White Paper. Over 110 secondary sources were reviewed.

Forecasting Models

IMARC’s Bottom-Up and Top-Down dual estimation methodology was applied. Bottom-Up aggregates China two-wheeler market revenue by type (scooters, motorcycles), propulsion type (electric, ICE), and region (East China, South Central China, North China, Southwest China, Northeast China, Northwest China), weighted by OEM production capacity schedules, battery technology cost curves, government electrification mandate timelines, urbanization projections, per capita income growth, and gig economy fleet expansion rates.

Top-Down validates against China Ministry of Industry and Information Technology’s annual production and sales data, total motor vehicle registration statistics, and China two-wheeler market revenue estimates from comparable automotive intelligence providers.

China Two Wheeler Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Scooters, Motorcycle |

| Propulsion Types Covered | ICE, Electric |

| End Users Covered | Personal, Commercial |

| Distribution Channels Covered | Offline, Online |

| Regions Covered | North China, East China, South Central China, Southwest China, Northwest China, Northeast China |

| Companies Covered | Yadea Technology Group Co., Ltd., AIMA TECHNOLOGY GROUP CO., LTD., Zhejiang CFMOTO Power Co., Ltd., LUYUAN Group Holdings Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the China two wheeler market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the China two wheeler market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the China two wheeler industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the China Two Wheeler Market Report

The China two wheeler market was valued at USD 23.55 Billion in 2025 and is projected to reach USD 30.50 Billion by 2034.

The China two wheeler market is forecast to grow at a CAGR of 2.92% during 2026-2034, driven by GB 17761-2024 replacement cycle, commercial EV delivery fleet expansion, urban congestion-driven adoption, and EV cost advantage economics.

Scooters lead with 61.8% revenue share (2025), encompassing China’s annual e-bike unit sales and commercial delivery fleet serving Meituan, Ele.me, and JD Logistics delivery partners.

Electric leads with 56.4% share (2025) – an historic majority achieved through GB 17761-2024 quality standard enforcement, lower running cost versus ICE, and commercial delivery platform electrification mandates.

East China leads with 29.8% share (2025), anchored by Jiangsu’s dual role as the EV scooter manufacturing province and high-income consumption market.

Key companies include Yadea Technology Group Co., Ltd., AIMA TECHNOLOGY GROUP CO., LTD., Zhejiang CFMOTO Power Co., Ltd., and LUYUAN Group Holdings Co., Ltd.

Key drivers include GB 17761-2024 compliance enforcement, creating pre-standard e-bike replacement demand, Meituan/Ele.me/JD Logistics 100% EV fleet commitment, urban congestion driving two-wheeler adoption.

Key trends include China’s domestic premium motorcycle brands, smart connected IoT e-scooter ecosystem, electric motorcycle commercial launch, and China's EV two-wheeler export expansion to countries.

Key challenges include price sensitivity in Tier-3/4 markets where non-compliant legacy models persist, charging infrastructure gaps in Northwest China, reducing EV adoption in Xinjiang and Gansu, urban ICE motorcycle ban ambiguity extending to performance electric motorcycles, reducing premium EV motorcycle urban market access, and apartment building e-scooter charging fire risk bans forcing reliance on battery swapping infrastructure.

Top opportunities include battery swap network pre-IPO; Southeast Asia EV scooter distribution partnerships; sodium-ion battery cell supply for EV scooter OEMs; MIIT IoT standard-driven smart two-wheeler connectivity module supply; and premium electric motorcycle technology investment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)