Cancer/Tumor Profiling Market Size, Share, Trends, and Forecast by Cancer Type, Technology, Technique, Application, and Region, 2025-2033

Cancer/Tumor Profiling Market Size and Share:

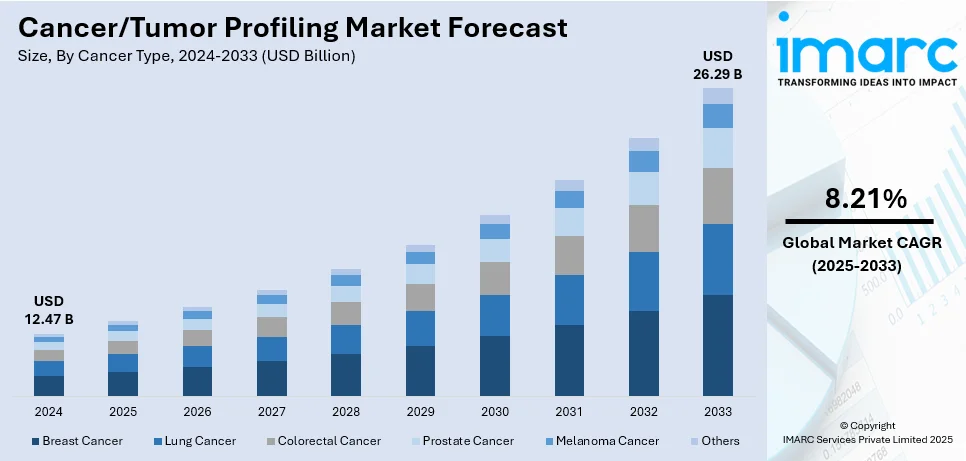

The global cancer/tumor profiling market size was valued at USD 12.47 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 26.29 Billion by 2033, exhibiting a CAGR of 8.21% during 2025-2033. North America currently dominates the market, holding a significant market share of over 42.8% in 2024. The market is experiencing significant growth driven by advancements in precision medicine, rising cancer prevalence and increasing adoption of personalized treatment approaches. Growing demand for biomarker-based diagnostics coupled with technological innovations in genomic and proteomic profiling, further fuels market expansion.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 12.47 Billion |

|

Market Forecast in 2033

|

USD 26.29 Billion |

| Market Growth Rate (2025-2033) | 8.21% |

The cancer/tumor profiling market is driven by advancements in genomic and proteomic technologies enabling precise molecular diagnostics. Increasing prevalence of cancer globally coupled with the rising demand for personalized medicine accelerates cancer/tumor profiling market growth. For instance, in December 2024, Aster DM Healthcare announced the launch three initiatives Precision Oncology Clinics, the Aster Cancer Grid and Onco Collect during the Aster Cancer Conclave. These programs aim to enhance personalized data-driven cancer care through genomic approaches promote collaborative research and improve patient outcomes positioning India as a leader in innovative cancer treatment. Government funding and private investments in oncology research also play a pivotal role. Next-generation sequencing (NGS) and biomarker discovery are becoming increasingly adopted for early detection and targeted therapies while technological innovations in liquid biopsy improve profiling accuracy and enhance market expansion.

The United States cancer/tumor profiling market is driven by the high prevalence of cancer and the increasing demand for personalized medicine. According to the data published by the National Library of Medicine, in 2024 an estimated 2,001,140 new cancer cases and 611,720 deaths are projected in the U.S. Advancements in genomic and proteomic technologies such as next-generation sequencing (NGS) enhance the accuracy of tumor profiling. Substantial government funding and investments in oncology research further support market growth.

Cancer/Tumor Profiling Market Trends:

Rising Prevalence of Cancer

The increasing prevalence of cancer in the world has provided a considerable thrust to this growth. Cancer incidence is at its peak, as with an ever-growing focus on exact and specific diagnosis solutions towards the betterment of patient results, the necessity of advanced methods for tumor profiling keeps increasing every year. The American Cancer Society reported that nearly 20 million cases of cancer were diagnosed worldwide in 2022, resulting in 9.7 million deaths due to the disease. This concerning trend highlights the urgent need for better diagnostic and treatment options. Additionally, it is projected that the number of cancer cases could rise to 35 million by 2050, driven by factors such as an aging population, lifestyle changes, and environmental impacts. These statistics point out how tumor profiling plays an increasingly pivotal role in serving the needs for tailored therapies and improved survival in cancer care.

Advancements in Genomics and Precision Medicine

Advances in genomic technologies, including NGS and proteomics, have revolutionized the study of cancer and treatment processes. It is because of this that growth in the tumor profiling market has taken a massive pace. With such advanced technologies, comprehensive tumor profiling is achieved that leads to developing personalized therapies on the basis of the genetic make-up of each individual patient. The results of treatment are improving, and there is a greater emphasis on providing precise care for cancer patients. Reports indicate that global investments in cancer medicine totaled around USD 196 billion in 2022, with an average growth rate of approximately 12% over the last five years. The growing requirement for innovative diagnostics and therapeutic applications has led to an increased utilization of advanced genomic technologies for profiling tumors. These developments are creating positive cancer/tumor profiling market outlook by changing the oncology landscape, opening the way for more effective and targeted cancer treatments.

Government and Research Funding

Investment and funding for cancer and precision medicine are growing largely and thus boosting tumor profiling. The governments, pharmaceutical companies, and other research organizations collaborate on the development of more advanced profiling solutions, which speed up the advancement in early diagnosis and treatment methods for cancer. The UK Government has committed to increasing its total investment in research and development (R&D) to 2.4% of GDP by the year 2027, as reported by Cancer Research UK. Such programs underscore the growing focus on innovation in cancer diagnostics and treatments, which drives cancer/tumor profiling market demand. These investments do not only make precision medicine more accessible but also fuel breakthrough innovations in the personalized treatment of cancer, thereby fueling the market growth.

Cancer/Tumor Profiling Industry Segmentation:

IMARC Group provides an analysis of the key trends in each sub-segment of the global cancer/tumor profiling market report, along with forecasts at the global, regional and country level from 2025-2033. Our report has categorized the market based on cancer type, technology, technique, and application.

Analysis by Cancer Type:

- Breast Cancer

- Lung Cancer

- Colorectal Cancer

- Prostate Cancer

- Melanoma Cancer

- Others

Breast cancer leads the cancer/tumor profiling market due to its high global prevalence and the increasing adoption of personalized medicine in oncology. Advanced profiling techniques such as next-generation sequencing (NGS) and immunohistochemistry (IHC) play a crucial role in identifying biomarkers for targeted therapies improving patient outcomes. The growing focus on early detection coupled with the rising availability of breast cancer-specific diagnostic tests and therapies drives market growth. Continuous research efforts and clinical trials further strengthen breast cancer's leadership in this sector.

Analysis by Technology:

- Next-Generation Sequencing (NGS)

- Polymerase Chain Reaction (PCR)

- Immunohistochemistry (IHC)

- In-Situ Hybridization (ISH)

- Microarray

- Others

NGS is one of the most prominent technologies in the cancer/tumor profiling market which enables the comprehensive genomic analysis for identifying cancer mutations and biomarkers. Its high-throughput capability and precision facilitate personalized treatments and diagnostics. Increasing adoption of NGS in clinical oncology and its application in targeted therapies and companion diagnostics significantly drive its demand in cancer profiling research.

PCR is highly used in cancer/tumor profiling because of its high sensitivity and specificity in detecting genetic mutations and alterations. It is also very important in the analysis of minimal DNA samples which makes it ideal for early cancer detection. The advancements in real-time and digital PCR further enhance its utility which has fostered its growth as a critical technology in oncology diagnostics.

IHC is one of the core technologies used to identify the tumor's specific protein and biomarkers profiles. This method's usefulness in finding hormone receptors status for example in breast cancer is confirmed by determining the expression of HER2 in cancer. IHC supports personalized treatment approaches through the selection of targeted therapies by a clinician based on biomarker expression patterns.

ISH technology is also used for cancer profiling. This technology can accurately visualize genetic abnormalities directly in tissue samples. It is highly efficient in detecting gene amplifications, translocations and deletions. Applications include the identification of HER2/neu in breast cancer and other chromosomal aberrations. Its use is continuously propelled by the rising demand for accurate molecular diagnostics.

Microarray technology supports cancer profiling by analyzing gene expression patterns and identifying biomarkers associated with tumor development. It enables large-scale screening of genetic data providing insights into cancer classification and progression. The utility of the technology in discovering therapeutic targets and stratifying patients for clinical trials makes it a valuable tool in oncology research and diagnostics.

Analysis by Technique:

- Genomics

- Proteomics

- Epigenetics

- Metabolomics

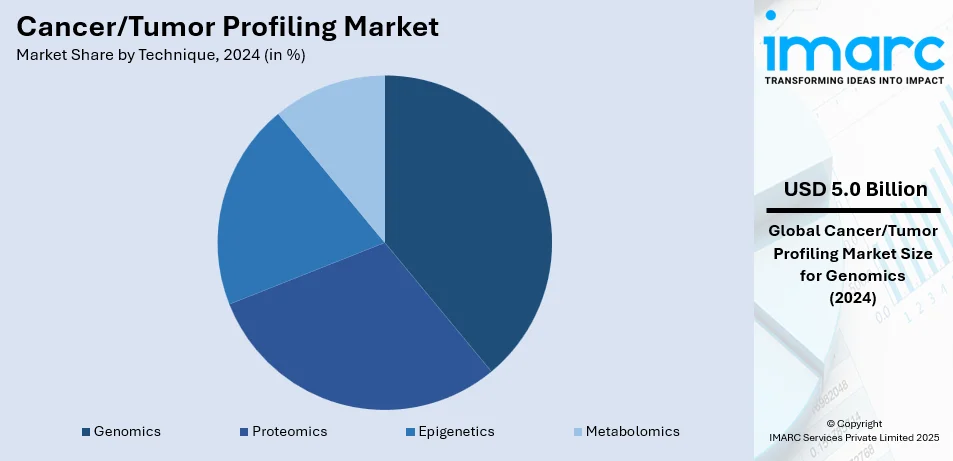

Genomics leads the market with around 39.8% of cancer/tumor profiling market share in 2024. Genomics is the largest technique in the cancer/tumor profiling market because it plays a central role in understanding the genetic basis of cancer. Genomic profiling allows for the identification of mutations, gene expression patterns and biomarkers critical for personalized oncology. Technologies such as next-generation sequencing (NGS) and microarrays drive this segment by offering high-throughput and precise analyses. The rise in targeted therapies advancements in companion diagnostics and the increasing adoption of genomics within clinical oncology heighten its presence further while promoting successful treatment outcomes and new areas for research.

Analysis by Application:

- Personalized Medicine

- Diagnostics

- Biomarker Discovery

- Prognostics

- Others

The personalized medicine segment is highly important in the cancer/tumor profiling market as it provides for treatment based on an individual's genetic and molecular profile. This improves the effectiveness of therapy while minimizing side effects targeting the specific biomarkers. Increasing precision oncology adoption and advancement in tumor profiling techniques propel this segment's growth significantly which also enhances patient outcomes.

The market is dominated by the diagnostics segment mainly because of the accurate type and stage of cancer identification via advanced tumour profiling techniques. Technologies such as PCR, NGS and IHC enable early diagnosis and improved decision-making in treatment plans. The demand for early screening of cancer and non-invasive diagnostic solutions is therefore driving further expansion in this critical application area.

Biomarker discovery is one of the key applications of cancer profiling focused on identifying molecular markers associated with cancer development and progression. This helps in targeted drug development and companion diagnostics that drive the evolution of precision medicine. Continuous genomics and proteomics research coupled with increased investments in oncology studies propel this segment in the market.

The prognostics segment is used to predict the progression of cancer, survival rate of patients and possible treatment response through tumor profiling. It supports the planning of treatment on an individual basis by analyzing genetic mutations and biomarkers. Rising awareness of the benefits of prognostic tools and advancements in molecular diagnostics contribute to the growing adoption of prognostic applications in the cancer/tumor profiling market.

Regional Analysis:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 42.8%. North America dominates the cancer/tumor profiling market with the region witnessing an advanced healthcare infrastructure, high adoption of precision medicine and substantial investments in oncology research. The region benefits from the widespread availability of advanced diagnostic technologies such as NGS and PCR along with a strong presence of key market players. Rising cancer prevalence and government initiatives to support cancer screening and biomarker research further propel market growth. With higher clinical trials and research collaborations among research institutes North America leads this market.

Key Regional Takeaways:

United States Cancer/Tumor Profiling Market Analysis

In 2024, the United States captured 88.9% of revenue in the North American market. The American Cancer Society anticipates more than 1.9 million new cancer cases in the U.S. for 2024. It's estimated that 1 in 23 men and 1 in 24 women will be diagnosed with colorectal cancer at some point in their lives. Current projections for 2023 suggest that there will be 106,970 new cases of colon cancer and 46,050 new cases of rectal cancer in the U.S. With this trend in cancer, growing need is being seen to develop diagnostic and prognostic tools at more advanced levels such as tumor profiling. Tumor profiling provides more informative molecular data which helps identify mutations, biomarkers, and targets of therapy. As healthcare systems look to the earlier diagnosis and tailoring of therapy to improve outcomes in patients there will be immense opportunities for the growth of the cancer/tumor profiling market.

Europe Cancer/Tumor Profiling Market Analysis

The Europe cancer/tumor profiling market is experiencing significant growth driven by the rising burden of cancer particularly due to an ageing population. From 2010 to 2020, the European population living with cancer saw an annual increase of 3.5% leading to an overall rise of 41% according to the EU Science Hub. With the aging population the prevalence of cancer is anticipated to grow which will increase the need for advanced diagnostic technologies such as tumor profiling. These technologies such as next-generation sequencing (NGS) and liquid biopsy enable early cancer detection and personalized treatment strategies improving patient outcomes. With an increased focus on precision medicine and the growing recognition of the benefits of early and accurate cancer detection Europe is seeing an uptick in the adoption of tumor profiling solutions. Additionally, the region's strong healthcare infrastructure and government support for cancer research are expected to continue driving market expansion in the coming years.

Asia Pacific Cancer/Tumor Profiling Market Analysis

The Asia Pacific region experiences a considerable burden from cancer with the five most prevalent types being lung cancer (1,315,136 new cases), breast cancer (1,026,171 cases), colorectal cancer (1,009,400 cases), stomach cancer (819,944 cases) and liver cancer (656,992 cases) as reported by NIH data. This rising incidence is fueling the demand for advanced cancer diagnostics including tumor profiling technologies like next-generation sequencing (NGS) and liquid biopsy. As healthcare infrastructure improves across countries like China, India and Japan there is a strong push for precision medicine and personalized therapies. These innovations are driving the adoption of tumor profiling tools to enhance early detection, guide treatment decisions and improve patient outcomes. Government initiatives, increased healthcare spending and strategic partnerships with global biotech and pharmaceutical firms are accelerating the adoption of these technologies in the region. The Asia Pacific cancer/tumor profiling market is poised for significant growth driven by the need for more effective tailored cancer care solutions.

Latin America Cancer/Tumor Profiling Market Analysis

As cited by the ESMO 2022 report Latin America presents a significant burden of cancer. An estimated 1.5 million new cases and 700,000 deaths are reported yearly. The cancer incidence and mortality rates in this region stand at 186.5 and 86.6 per 100,000, indicating a pressing requirement for advanced diagnostic solutions. Cancer has recently been a new tool for tackling cancer by way of personalising the treatment processes to suit every patient's specific genetic makeup. This, besides enhancing patient results, has managed to tackle cancer mortality rates across the region. Governments in Latin America are pouring more investments in healthcare infrastructure; the emphasis lies on early detection and precision medicine to curb rising cancer burdens. The innovation in diagnostic techniques is driven by collaborations between regional healthcare providers and global biotechnology firms, increasing access to next-generation sequencing and other tumor profiling technologies. Such efforts are expected to fuel the growth of the tumor profiling market, bringing hope for better cancer management across the region.

Middle East and Africa Cancer/Tumor Profiling Market Analysis

The Middle East and Africa (MEA) region is undergoing a significant change in the increasing number of cancer cases. Ingestion of lifestyle changes, aging populations, and a burgeoning environmental risk factor are widespread. Cancer incidence is projected to increase 1.8-fold by 2030 in Arab countries, according to the NIH, further necessitating advanced diagnostic and treatment solutions. The demand for cancer/tumor profiling is accelerating as healthcare systems in the region focus on early detection and personalized treatment approaches to improve patient outcomes. Governments and private organizations are increasingly investing in healthcare infrastructure, research initiatives, and collaborations with global biotechnology companies to bring state-of-the-art technologies, such as next-generation sequencing (NGS) and liquid biopsy solutions, to the region. It can be attributed to the presence of initiatives like UAE National Cancer Registry and healthcare targets set in Saudi Arabia through its Vision 2030, leading to an advance in cancer profiling. This, too, will foster growth for the MEA market on cancer/tumor profiling.

Competitive Landscape:

The cancer/tumor profiling market is highly competitive with key players focusing on innovation, strategic partnerships and product development to strengthen their market presence. Leading companies are driving advancements in genomic and molecular diagnostics. These firms invest heavily in research and development to introduce advanced profiling technologies such as NGS and biomarker-based diagnostics. Additionally, collaborations between biotechnology companies, research institutions and healthcare providers are fueling market expansion. Emerging players are also leveraging technological advancements and targeting niche segments to gain a competitive edge further intensifying the market's dynamic landscape.

The report provides a comprehensive analysis of the competitive landscape in the cancer tumor profiling market with detailed profiles of all major companies, including:

- Abbott Laboratories

- Becton Dickinson and Company

- Caris Life Sciences

- Exact Sciences Corporation

- F. Hoffmann-La Roche Ltd

- Hologic Inc.

- HTG Molecular Diagnostics Inc.

- Illumina Inc.

- Laboratory Corporation of America Holdings

- NeoGenomics Laboratories

- Qiagen N.V.

- Siemens AG

- Sysmex Corporation

Latest News and Developments:

- October 2024: Illumina announced its partnership with AstraZeneca to develop innovative next-generation sequencing (NGS)-based companion diagnostics, strengthening its capabilities in oncology-related solutions.

- September 2024: Thermo Fisher launched the Oncomine Comprehensive Assay Plus, a targeted NGS tool designed to detect essential mutations in solid tumors, demonstrating its dedication to improving diagnostic options in cancer genomics.

- November 2023: Illumina unveiled the latest version of its liquid biopsy assay for genomic profiling, the TruSight Oncology 500 ctDNA v2. This assay is intended to deliver thorough genomic insights from blood samples, especially useful for patients when tissue testing is not feasible.

- May 2023: Pfizer announced its partnership with Thermo Fisher Scientific in a strategic collaboration aimed at increasing the availability of NGS-based testing for lung and breast cancer patients across more than 30 countries.

Cancer/Tumor Profiling Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Cancer Types Covered | Breast Cancer, Lung Cancer, Colorectal Cancer, Prostate Cancer, Melanoma Cancer, Others |

| Technologies Covered | Next-Generation Sequencing (NGS), Polymerase Chain Reaction (PCR), Immunohistochemistry (IHC), In-Situ Hybridization (ISH), Microarray, Others |

| Techniques Covered | Genomics, Proteomics, Epigenetics, Metabolomics |

| Applications Covered | Personalized Medicine, Diagnostics, Biomarker Discovery, Prognostics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, Becton Dickinson and Company, Caris Life Sciences, Exact Sciences Corporation, F. Hoffmann-La Roche Ltd, Hologic Inc., HTG Molecular Diagnostics Inc., Illumina Inc., Laboratory Corporation of America Holdings, NeoGenomics Laboratories, Qiagen N.V., Siemens AG and Sysmex Corporation. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cancer/tumor profiling market from 2019-2033.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global cancer/tumor profiling market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the cancer/tumor profiling industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The cancer/tumor profiling market was valued at USD 12.47 Billion in 2024.

IMARC estimates the cancer/tumor profiling market to reach USD 26.29 Billion by 2033, exhibiting a CAGR of 8.21% during 2025-2033.

Key factors driving the cancer/tumor profiling market include rising cancer prevalence, advancements in precision medicine, and growing demand for personalized treatments. Increasing adoption of genomic technologies like NGS and biomarker-based diagnostics, along with heightened investments in oncology research and government initiatives for early cancer detection, further fuel market growth.

In 2024, North America accounted for the largest market share of over 42.8%, driven by advanced healthcare infrastructure, high adoption of precision medicine, significant investments in cancer research, and the presence of key market players. The region’s robust oncology research ecosystem and increasing demand for early cancer detection further contribute to its dominance in the global market.

Some of the major players in the cancer/tumor profiling market include Abbott Laboratories, Becton Dickinson and Company, Caris Life Sciences, Exact Sciences Corporation, F. Hoffmann-La Roche Ltd, Hologic Inc., HTG Molecular Diagnostics Inc., Illumina Inc., Laboratory Corporation of America Holdings, NeoGenomics Laboratories, Qiagen N.V., Siemens AG and Sysmex Corporation., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)